SWN - Chesapeake Energy Faces Near-Term Headwinds And May Have A Strong H2 2024

2024-01-03 03:59:15 ET

Summary

- Chesapeake Energy is focusing on building capacity for future LNG export and remains optimistic about the opportunity presented by the new LNG export capacity coming online in late 2024.

- The company is well-positioned for increased LNG export capacity, with 2.7Bcf/d of capacity coming online by the end of 2024.

- Management is making the right decision to pull back production in the Haynesville Basin and anticipates adding a rig in 2H24 as they ramp up production in anticipation of new export capacity.

As Chesapeake Energy ( CHK ) works through tough 2022 comps, the firm is making strides in positioning its focus towards building out capacity for future LNG export. Despite the low strip pricing going into 2024, management remains laser-focused on the opportunity presented for late 2024 with new LNG export capacity coming online. CHK shares trade at a relatively low valuation when compared to their natural gas-producing peers at 2.19x TTM EV/EBITA. With the near-term gas pricing headwinds coming into 2024 and the long-term opportunity towards the back half of 2024, I provide CHK shares a HOLD recommendation as a “show me” story with a near-term price target of $82.68/share.

Operations

Chesapeake Energy is well-positioned for the increased LNG export capacity coming online at the end of 2024. The EIA estimates an additional 2.7Bcf/d of nominal capacity and 3.2Bcf/d of peak capacity coming online between the Golden Pass and the Plaquemines facilities. This will increase nominal and peak US LNG export capacity, to 14.1Bcf/d and 17Bcf/d, respectively.

“What we're all excited about in the industry is the step change that will come to the fundamentals when we have the incremental export capacity come online. We still think that happens around the end of 2024. We will watch that very, very closely. That's the signal we're really focused on from a macro perspective is will we have that connectivity to markets that are underserved, such that there is a call on US gas. If that happens, we believe we have an important asset to meet that call in the Haynesville, and we would expect to add a rig if that looks like it's coming in line with that projection.”

Nick Dell’Osso

I believe management is making the right decision to pull back production in the Haynesville Basin as pricing doesn’t currently reflect the total economic value of the basin. Despite the near-term curtailment, management did suggest an additional rig being placed in the basin in 2h24 as they ramp up production in anticipation of this new export capacity.

{kind=link}

In conjunction with the two new export facilities coming online, Chesapeake announced a 15-year supply heads of agreement that will be indexed to the Japan Korea Marker ("JKM") for 1MTPA (million tons per annum) of LNG commencing in 2028. Comparing the prices of each contract, it’s clear that selling gas indexed to the JKM as opposed to being indexed to Henry Hub or Gulf Coast will provide Chesapeake more value.

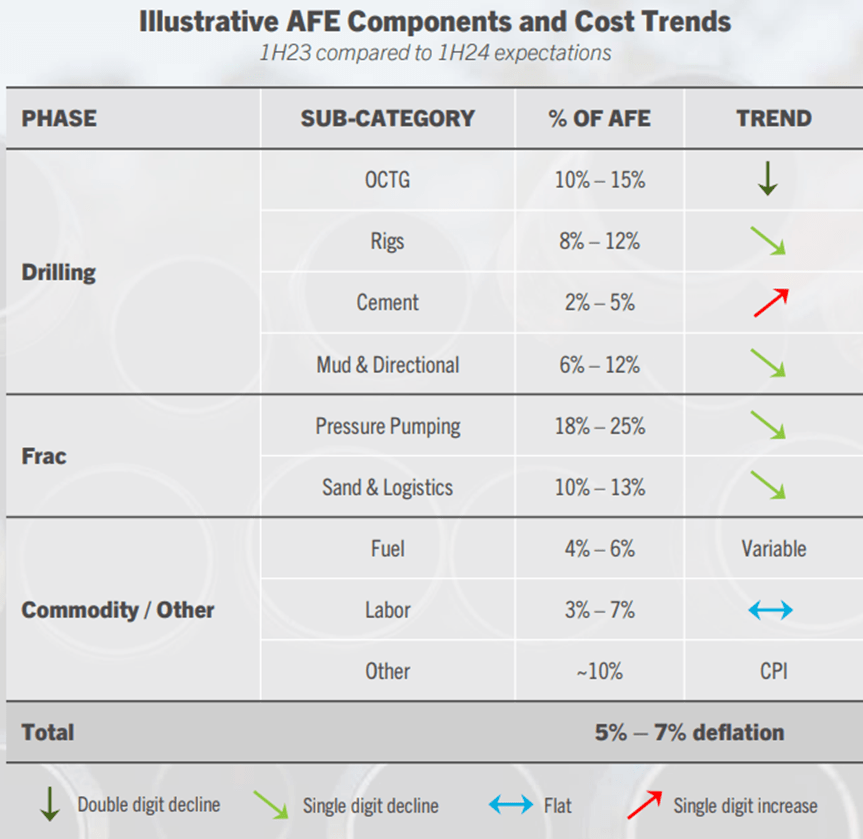

In addition to top-line strength, management has 50% of FY24’s D&C spend contracted out with 1h24 D&C costs coming in significantly lower when compared to 1h23.

{kind=link}

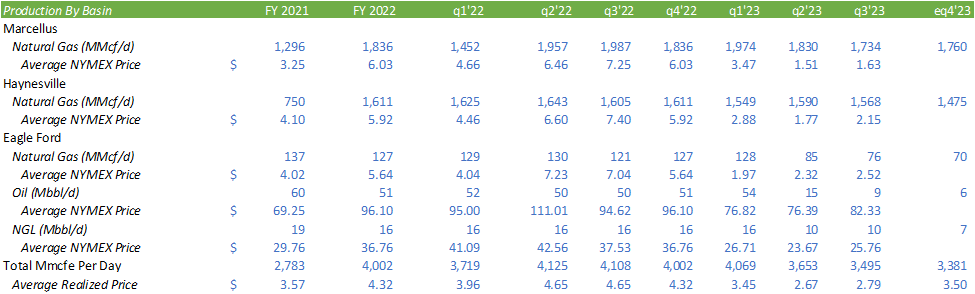

Q4’23 should be relatively strong with 70% of gas production, or 218Bcf, hedged with a floor of $3.54/MMbtu. This should overall provide Chesapeake with some breathing room as they faced lower gas prices in the latter portion of q4’23.

{kind=link}

My expectation for q4’23 as well as the first half of 2024 is for it to be relatively mundane when compared to what’s in store for the firm in the latter portion of 2024. In the near term, I anticipate management to continue pulling some production out of the Haynesville Basin to preserve its value as the firm awaits LNG export capacity to come online. Chesapeake is also poised to conclude operations in the Eagle Ford in February 2024 with the final asset sale to SilverBow for $700mm. Management did make some comments relating to industry consolidation but mentioned no specifics to any potential deals.

“Overall, we've continued to say that we're very happy with the portfolio that we own. So, we don't feel compelled to do anything and we certainly don't feel compelled to do anything on a near-term timetable. But at the same time, we believe in consolidation. We believe in the merits of attempting to have consolidation make the industry a more profitable, more productive place and we've been also very consistent in talking about how we would define that for ourselves.” – Nick Dell’Osso

As mentioned in previously released reports covering Southwestern ( SWN ) and Comstock ( CRK ), I believe Comstock is in the weakest position when compared to their peers and may be a prime target for the sale of their Haynesville/Bossier assets. Nothing has been mentioned by any of these firms; however, M&A interest had generally been discussed across each firm, independently.

Valuation/Shareholder Value

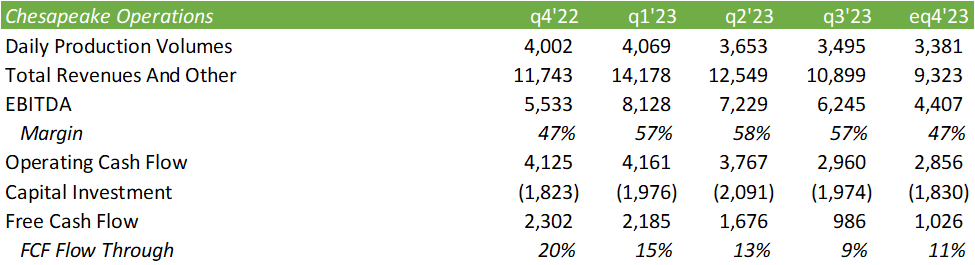

Management made the decision to cut the variable dividend in q3’23 to bolster the balance sheet and to increase both the base dividend and share buybacks. The base dividend was increased by 4.5% to $2.30/share and cash allocated to buybacks increased to $130mm in the quarter.

Despite these strong shareholder values, the firm continues to trade at a low relative multiple when compared to its peers.

{kind=link}

I don’t believe this will be an appropriate price for CHK shares, at least in the near future as the firm overcomes the near-term natural gas pricing headwinds. As the LNG market opens up to Chesapeake, I do believe the stock has the ability to realize such a price target.

Considering the market opportunity ahead of the firm along with the short-term challenges, I believe CHK should be trading closer to 3x EV/EBITDA based on historical pricing. Given the near-term risks involved and the long-term value, I provide CHK shares with a HOLD recommendation with a price target of $82.68/share. I believe q2’24 will be a more appropriate time to start building a position in CHK shares as the firm works through the challenging gas market. I believe investors will show more interest in the firm as gas prices firm up and LNG terminal projects near completion.

{kind=link}

For further details see:

Chesapeake Energy Faces Near-Term Headwinds And May Have A Strong H2 2024