PDCE - Chevron Indicates There Might Be A Reason To Invest (Rating Upgrade)

2023-07-24 15:51:14 ET

Summary

- Chevron Corporation is a stock we've discussed before as being overvalued, and since then it has underperformed the S&P 500.

- The company has recently made the well-timed acquisition of PDC Energy, something that should quickly be accretive for the company.

- The company has the ability to continue driving reasonable double-digit returns, impressive in an expensive market.

Chevron Corporation ( CVX ) is one of the largest oil companies in the world, with a market capitalization of just under $300 billion. The company has gone up just under 2% since we last recommended selling versus almost 10% with the S&P 500 (SP500), so it has underperformed. However, in a more expensive market, with the company's recent decisions, it could be interesting.

Chevron Q2 2023 Performance

Chevron announced some Q2 2023 numbers as a sneak peek a week early ( full report due pre-market July 28).

{kind=link}

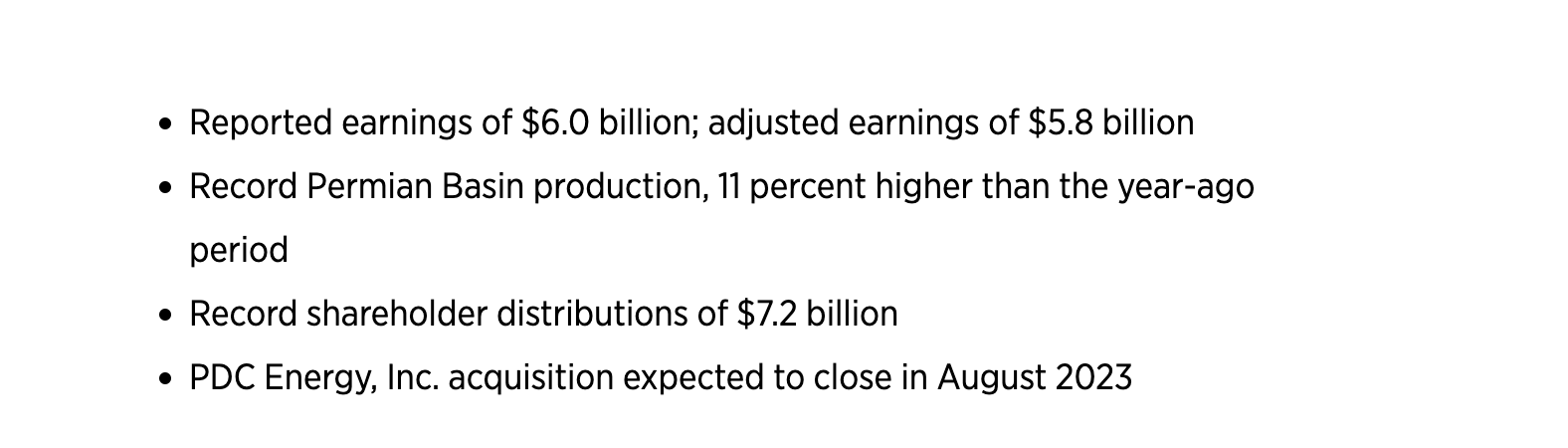

The company announced $6 billion in reported earnings, $5.8 billion in adjusted earnings. That's versus the 1Q where the company earned $6.6 billion in earnings and $6.7 billion in adjusted earnings. The company's earnings did decline by 10% QoQ, but at times when prices are much lower, it's continued to perform well.

The company did provide $7.2 billion in shareholder distributions, above its earnings, and annualized at almost $29 billion. That gives the company a shareholder return ratio of ~10%, but with its earnings closer to 8% or so, it won't necessarily continue. Still, with a more expensive market, those are reasonable returns to have.

Chevron PDC Energy Acquisition

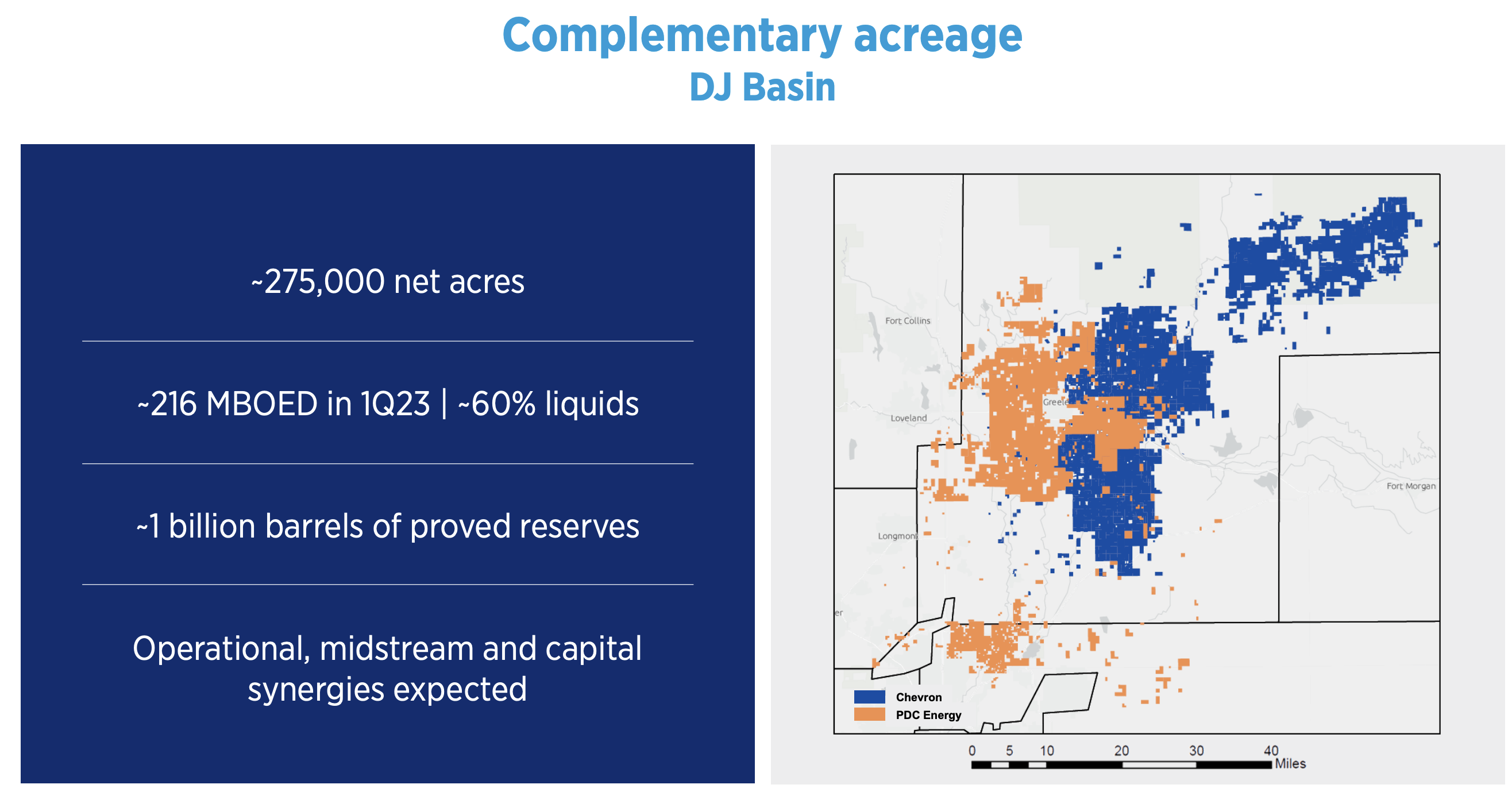

The company has also announced a $6.4 billion acquisition of PDC Energy , one of its larger recent acquisitions, taking advantage of lower prices.

{kind=link}

The acquisition of PDC Energy provides strong synergies which will provide $400 million in annual capex savings and $100 million in annual opex savings. Overall, that will result in $1 billion in additional FCF for the company. That's incredibly cheap versus the acquisition price for the company, and it'll be accretive to all sorts of metrics.

From an asset base, the acquisition with substantial reserves is especially accretive in the DJ Basin. In the Delaware Basin, there's less assets (25k acres) but that acreage is still accretive with Chevron's existing assets. The DJ Basin is really where the synergy happens though, giving Chevron billions of dollars in value.

In our view, these synergies mean the acquisition has long-term potential.

Chevron Capital Spending

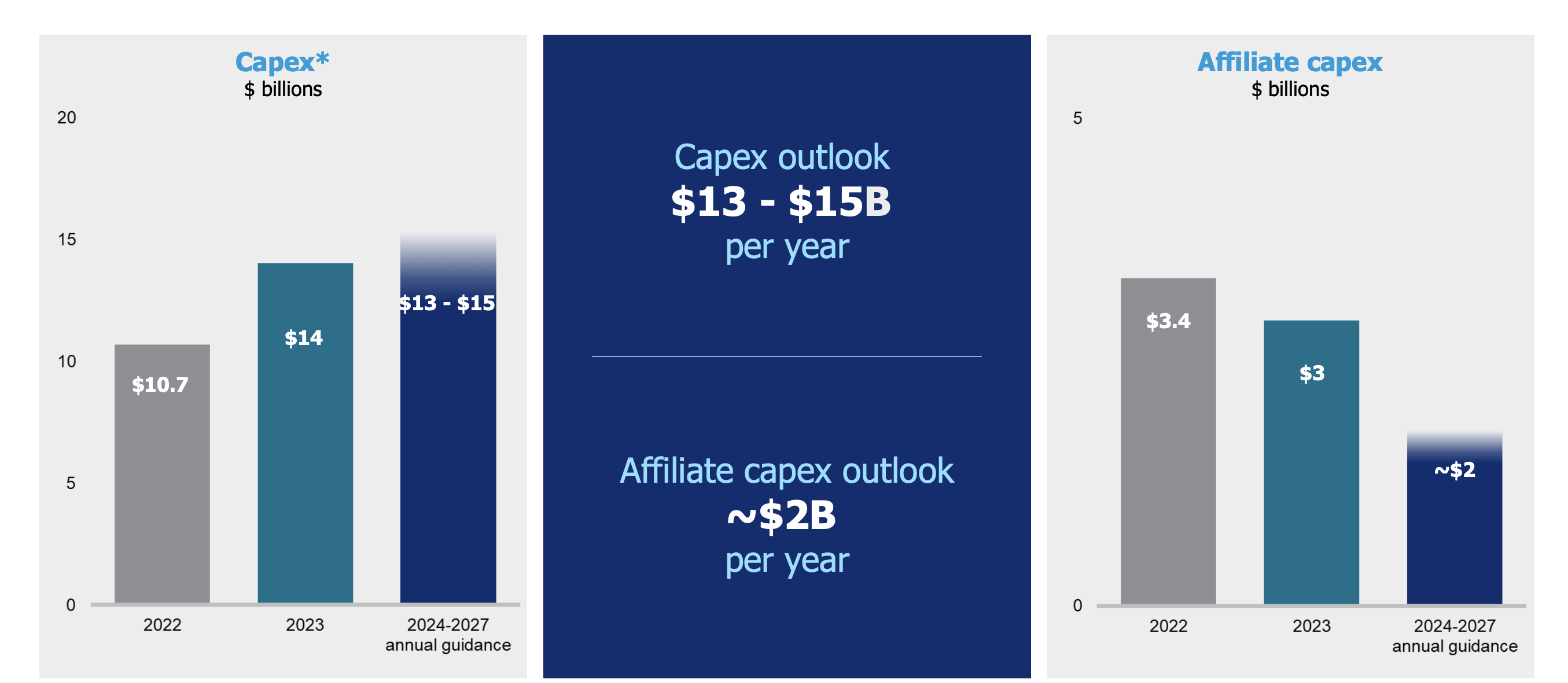

The company is continuing to keep its capital spending lofty. The company's reserves are just 100 million barrels less than 2020.

{kind=link}

From 2022 capital spending of less than $11 billion, the company is targeting 2023-2027 guidance of roughly $14 billion / year. Affiliate capex is expected to decline, but that still means that total capex of $14 billion in 2022 is expected to be $17 billion in 2023 and sit around or just under that level for the following 3 years.

That ramp up in capital spending could potentially result in the company's reserves growing faster as it targets growing production.

Chevron Production and The Permian Basin

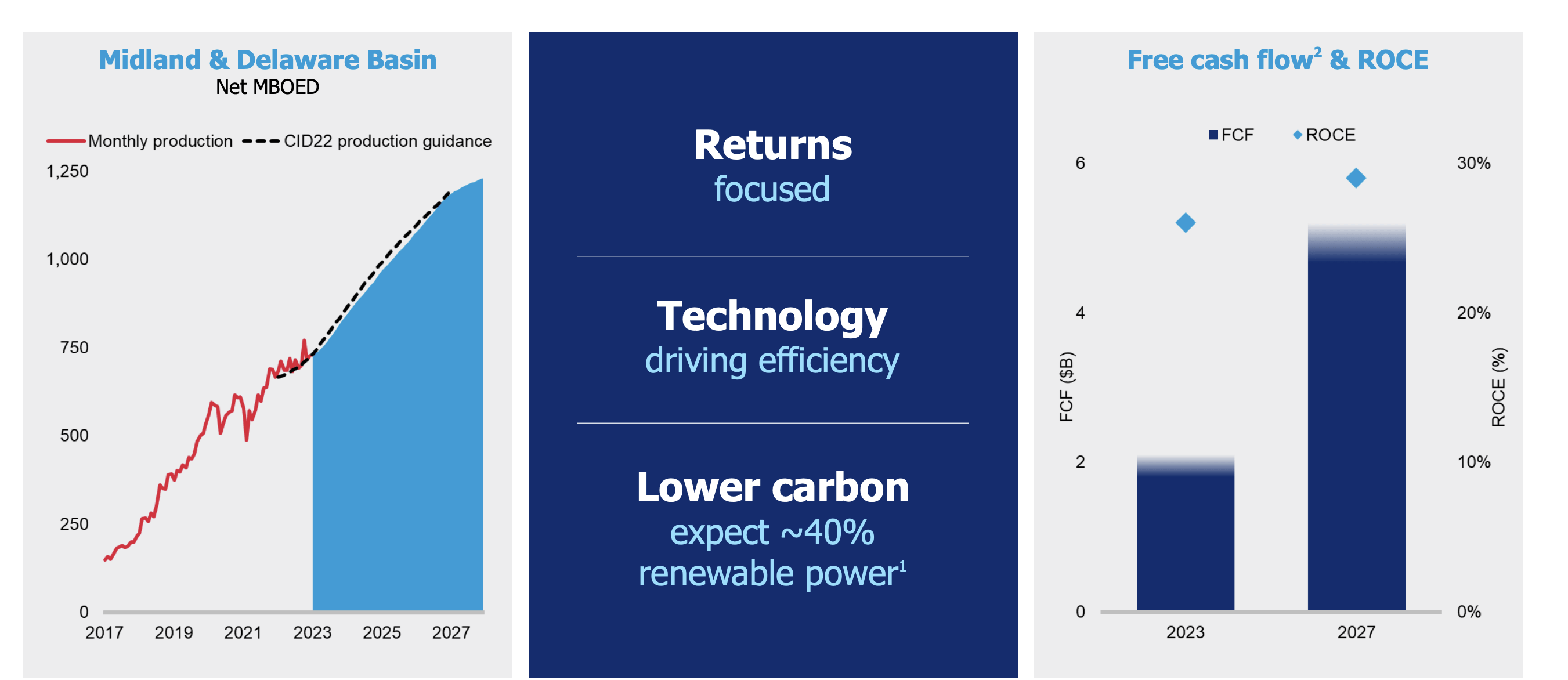

The star of Chevron's current production growth is the Permian Basin.

{kind=link}

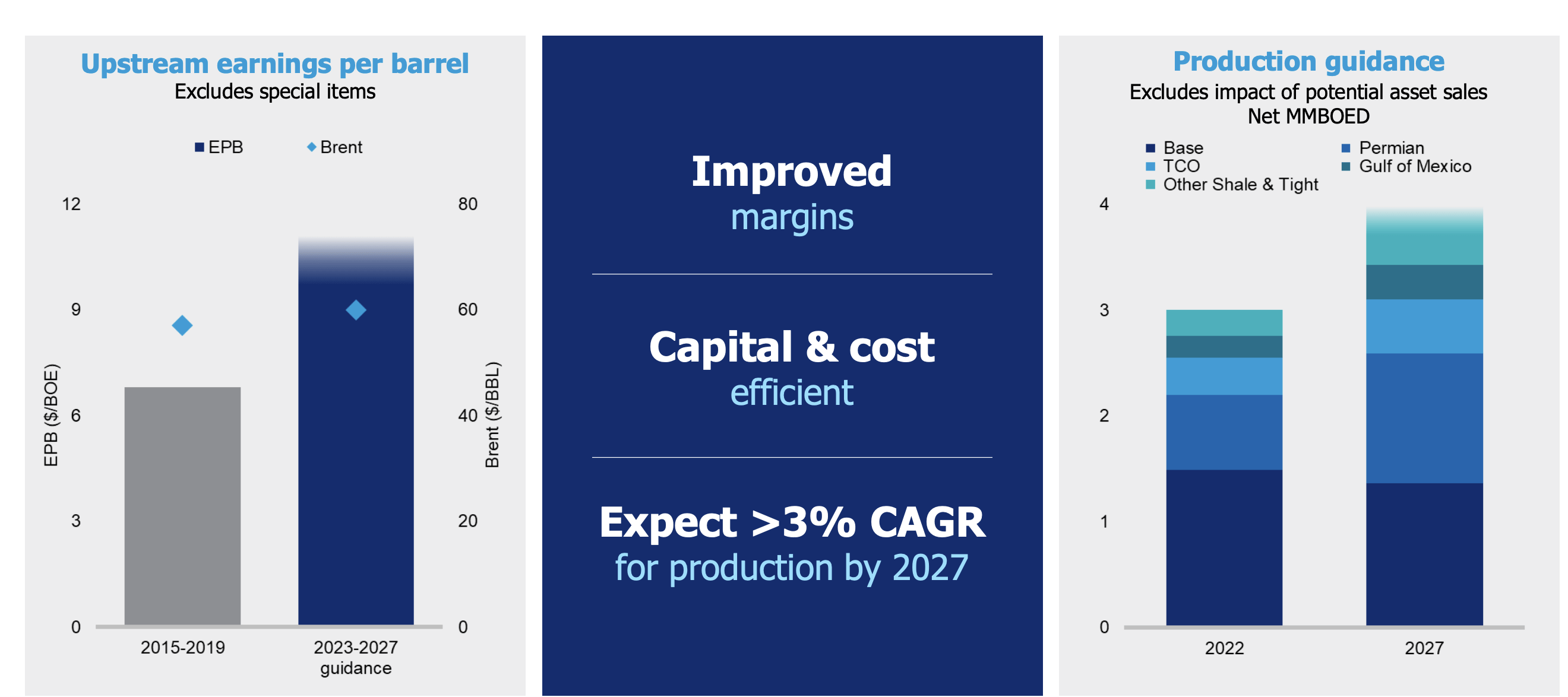

The company as part of its limited initial earnings release announced an 11% growth in production YoY. The company expects a continued faster ramp for its Permian Basin production, and the PDC Energy acquisition will help to support it. The company's guidance for production by 2027 is almost 1.25 million barrels / days.

That's roughly 500 thousand barrels / day in production growth for the company from that alone over the next 5 years.

{kind=link}

Overall, the company expects both upstream earnings $60 / barrel Brent and production / earnings to increase substantially by 2027. The company expects 2022 production of 3 million barrels / day to increase to almost 4 million barrels / day by 2027. That's some of the fastest growth in the company's history to be supported by TCO and the Permian Basin.

The company expects earnings per barrel at that price range to increase from $7 in 2015-2019, a tough time for prices, to more than $10 / barrel in the 2023-2027 range. That growth in margins along with production will help overall earnings to grow.

Chevron Shareholder Returns

The company's shareholder returns are expected to be strong in a higher price environment.

{kind=link}

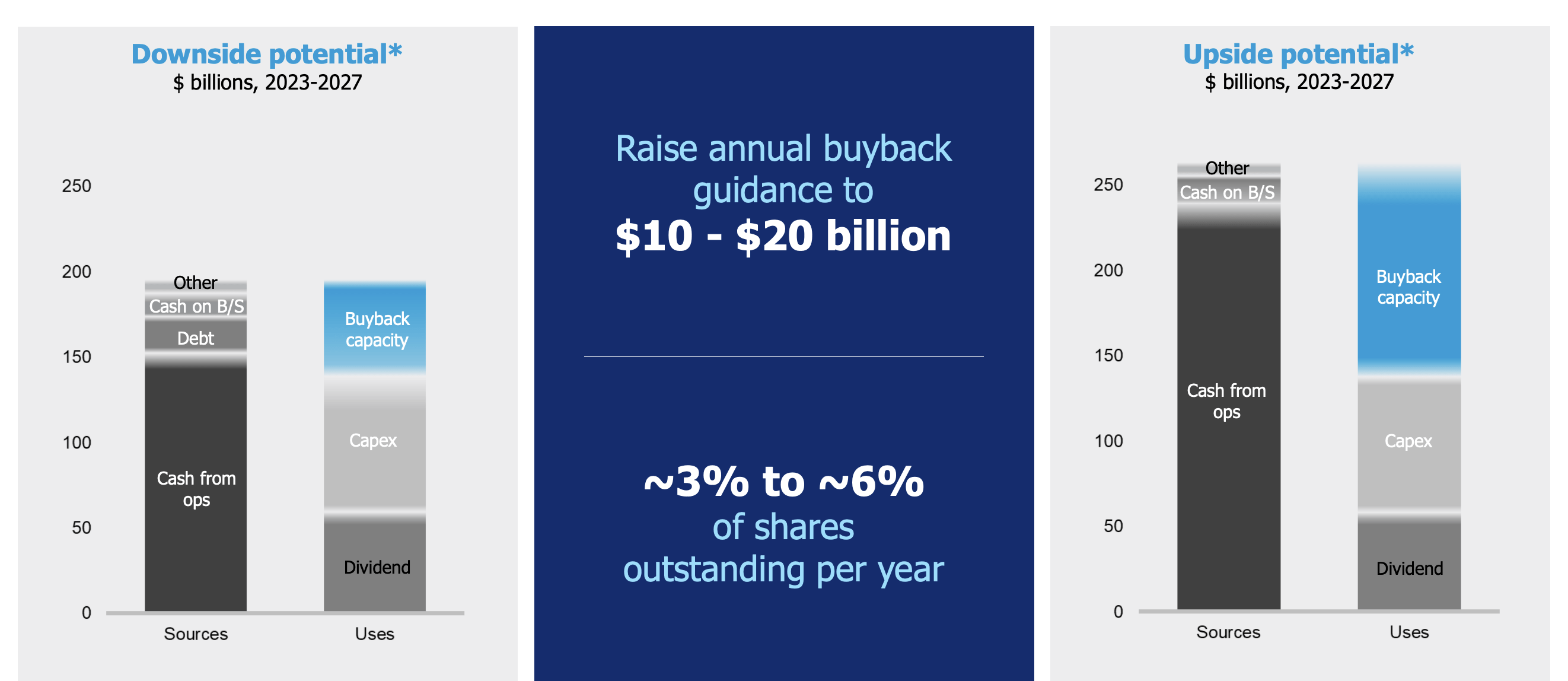

The downside scenario for the company is $60 / barrel Brent for the 2023-2027 5-year period, while the company's upside scenario is $85 / barrel average for the 5-year period. The company is assuming higher prices earlier and lower prices later, but a flip of that could result in it outperforming at the same average price.

Still, given current prices, the company is currently averaging closer to the upstream scenario. In that scenario, its base case is a roughly $50 billion dividend, a continuation of its dividend of almost 4%. The real kicker, though, is the buyback capacity. In that scenario, the company can buy back $100 billion in stock, or $20 billion / year. That's almost 7%.

Together, that's an ability to drive barely double-digit returns for the next 5-years at a time when the market is more expensive. More so the company that emerges from the 5-year period will have higher earnings in a stronger position.

Thesis Risk

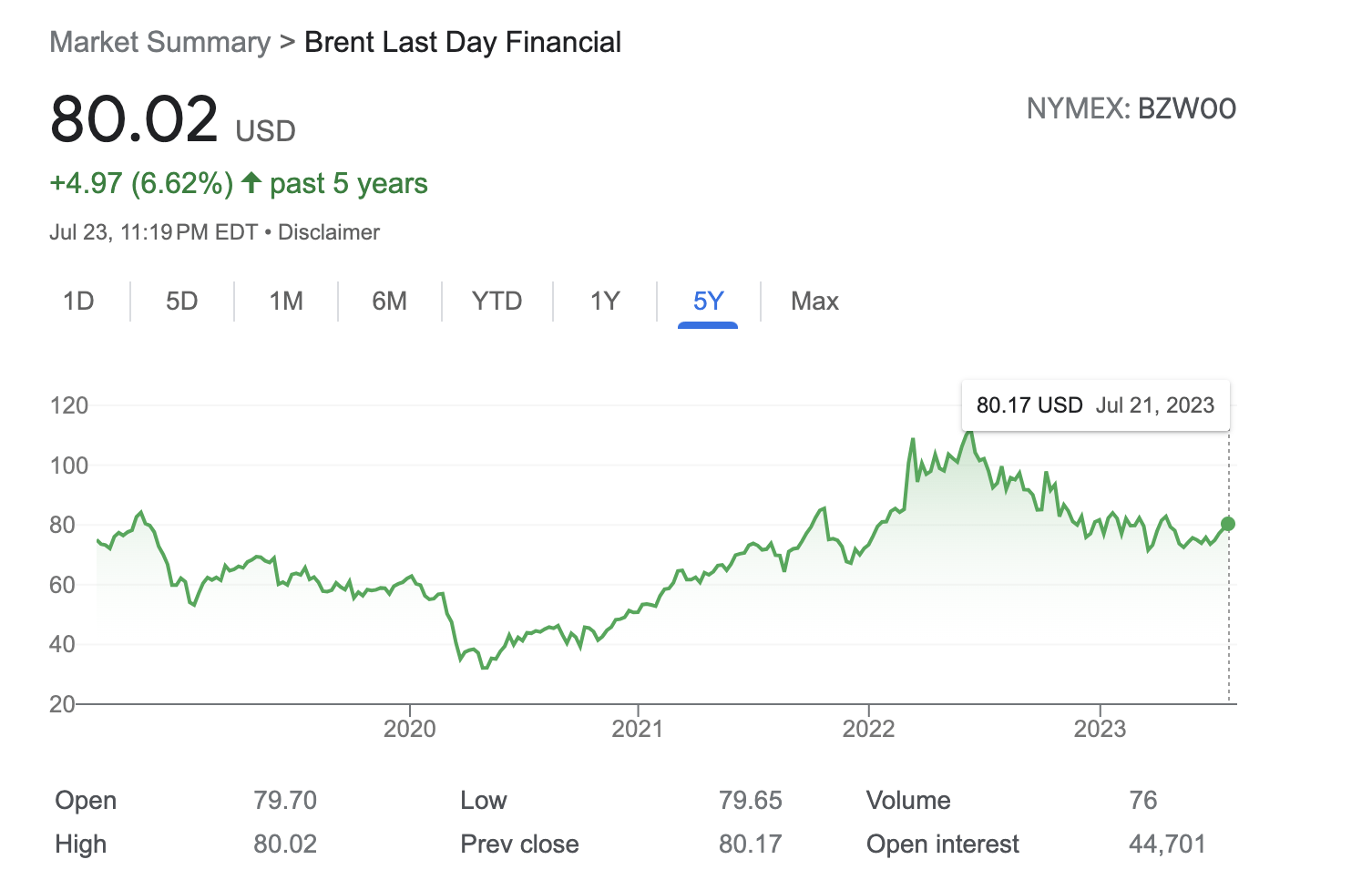

The largest risk to our thesis is crude oil prices.

{kind=link}

Crude oil outperformed after Russia's invasion of Ukraine. Prices peaked at more than $130 / barrel and for more of the first half of the year sat at $100+ barrel. Since then, they've dropped down. That's despite strong work by OPEC+ to lower volume and support prices. Prices have turned up some recently, but they remain weak.

Conclusion

Chevron is a stock that we've recommended against before. The company was expensive. It still is by most metrics, although it's always had a premium given its management team. The acquisition of PDC Energy is another example of this company's management team and their work to continue recognizing opportunities. The acquisition will add $1 billion in FCF annualized.

Given that since recommending against Chevron Corporation, its share price has increased 2% versus almost 10% by the S&P 500, we stand by that recommendation. However, we're now moving to neutral, with a potential buy as prices start to recover, as the company has the ability to drive long-term returns. Let us know your thoughts in the comments below.

For further details see:

Chevron Indicates There Might Be A Reason To Invest (Rating Upgrade)