DIA - Chevron: Recent Developments And Preview Of Q1 Report Due Friday

2023-04-24 07:37:00 ET

Summary

- Chevron's first quarter earnings report is due out this coming Friday, April 28.

- I will review the company's primary investment thesis, recent corporate developments, and Q1 earnings estimates.

- Chevron has a strong and balanced portfolio of assets across the Permian Basin, global LNG, chemicals, and refining.

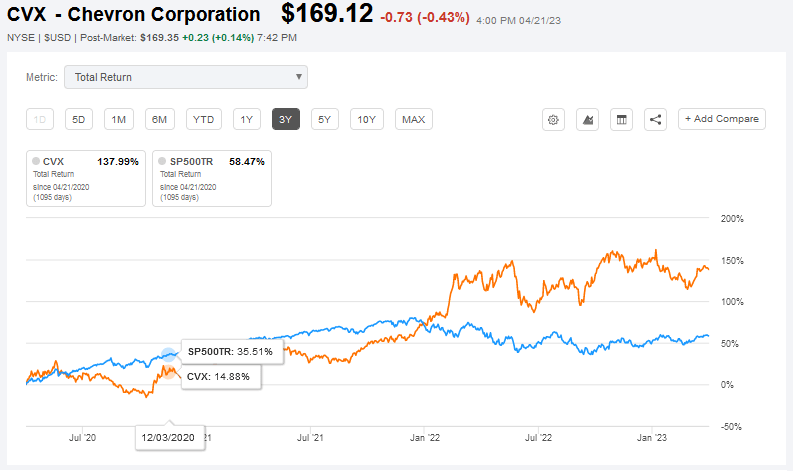

- Chevron has more than doubled the total returns of the S&P 500 over the past three years, pays an annual dividend of $6.04/share, and currently yields 3.57%.

Chevron ( CVX ) - the only oil and gas company left in the Dow 30 since Exxon ( XOM ) was replaced by Salesforce ( CRM ) in August of 2020 - will report its Q1 FY2023 earnings report on Friday, April 28. The results are expected to be relatively flat yoy, which is surprising since O&G prices in Q1 of last year were boosted by high commodity prices as a result of Russia's conflict in Ukraine. Today, I'll give an overview of the investment thesis in Chevron, review the Q1 earnings estimates, and discuss recent corporate developments. Meantime, it's important to note that Chevron has more than doubled the returns of the S&P 500 over the past three years, trades with forward P/E of only 11.8x, pays an annual dividend of $6.04/share, and yields 3.57%.

{kind=link}

Investment Thesis

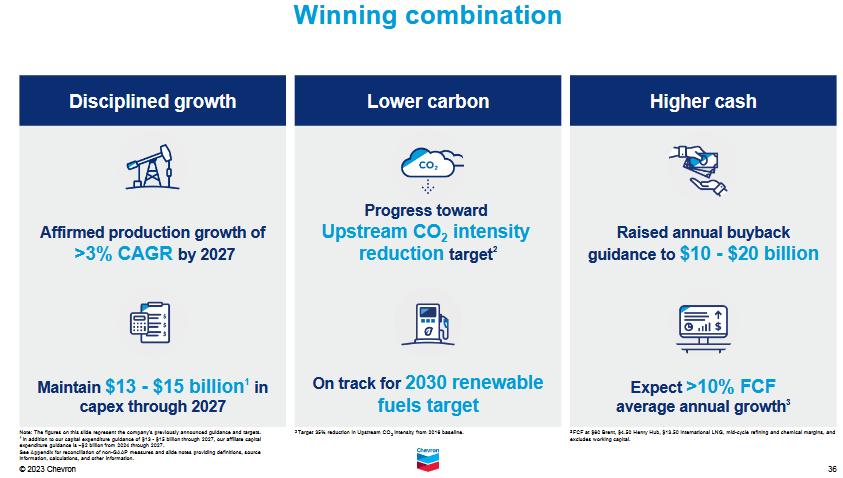

As shown in the slide below from Chevron's recent 2023 Investor Day Presentation, the investment thesis is relatively straight forward:

Chevron Investor Day Presentation

{kind=link}

As can be seen in the graphic, Chevron expects to return an average >10% CAGR in its free-cash-flow through 2027 by a combination of relatively disciplined spending (~$14 billion annually) that will generate a production CAGR of >3%. During that same time frame, Chevron expects to average a ~$15 billion annual share buyback rate. Over five years, that would equate to an estimated 23% of the company's current market cap of $320.4 billion. Note that Chevron's FCF expectations are based on the fine print: Brent at $60/bbl, $4.50 Henry Hub gas, $13.50 international LNG, and mid-cycle refining and chemical margins. The estimates shown also exclude working capital.

Chevron didn't choose to forecast 10 years out as ConocoPhillips ( COP ) did in its Investor Day Presentation a couple weeks ago (see COP: Refuting The Mizuho Downgrade ). In my opinion, that ' because Chevron doesn't have near as high a percentage of short-cycle shale drilling inventory that COP has. As a result, it doesn't have the clear line of sight that COP has for the next decade.

Much of Chevron's Investor Day presentation was devoted to lower-carbon solutions (primarily renewable biogas/liquids, carbon capture and storage ("CCS"), and hydrogen). However, there's still no indication that Chevron is planning significant investments in solar and/or wind electric power generation any time soon. As a result, Chevron is still very much focused on oil and gas production even as it touts a "lower carbon" future.

Recent Developments

Last week, Seeking Alpha cited a Reuters report that Chevron is shopping to secure a drill-ship to exploit its natural gas reserves in the Mediterranean Sea. Chevron is expected to start drilling in 2024 for a year and is reportedly seeking an option to extend the drill-ship contract for "several years."

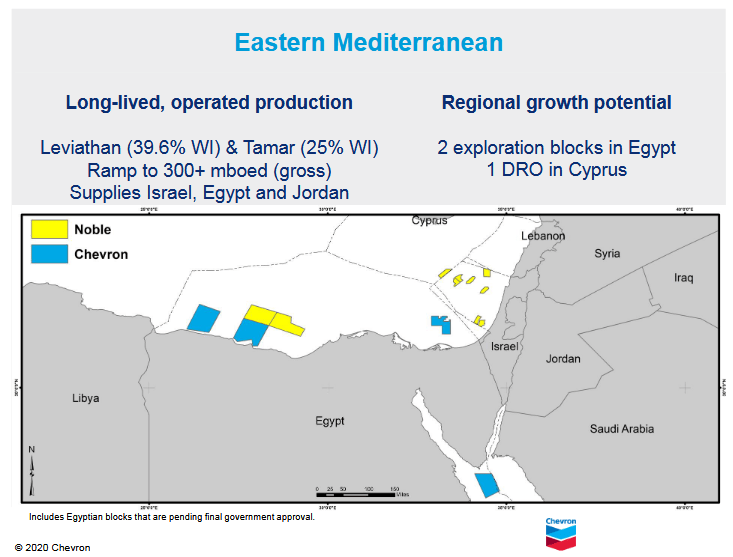

As I mentioned in a previous Seeking Alpha article, Chevron's Eastern Mediterranean natural gas resources are one of the best organic growth opportunities in its portfolio (see Chevron's Investor Day: Perfectly Positioned For The Next 10-Years ). Chevron acquired the bulk of its Med Sea natural gas position via the Noble deal it made during the pandemic down-cycle (a $13 billion deal that closed in October of 2020). The reserves are offshore Cyprus, Israel and Egypt and are geographically close to fast growing demand in the EU. The Noble acquisition turned out to be a strategic and well-timed coup for Chevron considering that, last year, Putin cut-off gas supplies to the EU in response to sanctions placed on Russia by the U.S. and its NATO and Democratic allies.

The slide below was taken from Chevron's Noble acquisition presentation in 2020 and shows the location of the Eastern Mediterranean assets it acquired in the deal:

{kind=link}

With the new drill ship, Chevron is looking to expedite development of the Aphrodite gas field southeast of Cyprus. Aphrodite is a world-class field that's estimated to contain ~4.5 trillion cubic meters ("Tcm") of gas. Chevron is investigating the best way to transport the gas to the EU mainland. One option is a pipeline, but Chevron also is reportedly considering construction of a floating LNG facility to enable transport by ship.

Through the Noble acquisition, Chevron is a now a major player in the region because it's the operator of the giant Leviathan field offshore Israel with a 39.66% ownership stake . Leviathan currently produces 12 Bcm of gas annually that supplies Israel, Egypt and Jordan. Chevron and its Leviathan partners - NewMed Energy and Ratio Energies - plan to nearly double the field's production to 21 to 24 Bcm by 2027.

In addition, and after the Noble deal closed, Chevron also made a " significant discovery " offshore Egypt when the Nargis-1 exploration well found 61 meters net of Miocene and Oligocene gas-bearing sandstones.

The bottom line is that Chevron has multiple large gas fields to exploit in the Eastern Mediterranean - right on the doorstep of highly profitable and growing demand in the EU.

Clean Energy

On the clean energy front, Chevron continues to dither around the periphery with several recently announced initiatives:

- Teaming up with Walmart ( WMT ) and Cummins ( CMI ) on a 15-liter compressed natural gas ("CNG") engine that will be incorporated into Walmart's private fleet and refueled at Chevron's CNG stations.

- Established a joint-study agreement with the Angelicoussis Group to explore how tankers can be used to transport ammonia, a potentially lower-carbon marine fuel.

- A collaboration with Corteva Agriscience and Bunge ( BG ) to produce winter canola as a feedstock for lower-carbon renewable fuels.

- A memorandum of understanding ("MOU") with JERA to collaborate on carbon capture and storage ("CCS") projects located in the United States and Australia.

However, as I mentioned earlier, Chevron still appears focused on liquids fuels and apparently has no interest in developing renewable at-scale wind and solar electric power generation capacity. Indeed, Mark Nelson - EVP of Chevron Strategy & Sustainability, Corporate Affairs, and Corporate Business Development - said as much during the Investor Q&A Exchange last month:

Let's start with wind and solar. Chevron is not planning large-scale investment in mature, onshore wind or solar , as this is a crowded space with low barriers to entry, and quite frankly, low returns. We don't have a competitive advantage in that space, nor the full electricity value chain. We'll buy wind and solar power in support of our operations, but we don't see producing it ourselves as something that will add significant value.

Chevron's take, that renewable solar and wind are "low return" and don't "add significant value," is interesting considering the "lost decade" where the energy sector was the worst performing sector of the entire market (by far), while solar and wind energy arrays were delivering low double-digit returns. It seems to me those would be excellent assets in the portfolio in order to smooth out the very volatile commodity up-n-down price cycles.

Q1 Earnings Estimates

The graphic below displays current consensus EPS estimates for Chevron per Yahoo Finance :

Yahoo Finance

As you can see in the Q1 estimate, and unlike many O&G companies that profited from the run-up in commodity prices last year due to Russia's invasion of Ukraine, Chevron is expected to announce earnings relatively in line with those of Q1 last year. That's likely largely due to a combination of factors that will offset the relatively weaker yoy O&G price environment:

- Continued Permian and overall production growth.

- Significant share buybacks that have reduced the overall outstanding share count from 1,947,553,346 as of February 10, 2022 versus 1,906,674,044 shares as of February 10th, 2023 (-40.88 million shares, or an 2.1%).

- Continuing structural efficiency gains combined with relatively disciplined capex spending as compared to the past decade. For example, development costs in the Permian have dropped by ~25% since 2019.

Given where the stock closed on Friday ($169.12), the full-year FY23 EPS estimate of $14.15/share equates to a forward P/E=12x. That compares to 11.5x for Exxon ( XOM ) and 10.4x for ConocoPhillips, Chevron's two largest U.S. O&G peers. Obviously the two international integrated companies are trading at a premium as compared to upstream-only COP because they both have downstream refining and chemicals operations that are viewed as sustainable cash flow generators during a potential recession and oil price down cycle. Also, Chevron's chemicals exposure is primarily through its 50/50 CPChem joint-venture with Phillips 66 ( PSX ).

Risks

Chevron is an O&G producer and, as such, is a commodity price taker. Therefore, the biggest risk is obviously a decline in the price of oil and gas.

At the end of 2022, Chevron's net-debt ratio was just over 3% - the lowest net-debt ratio of its peer-group. During the pandemic, Chevron was the only company to show a two-year stress test at $30/bbl Brent that showed it could fund the dividend and capex. The strength of its balance sheet put Chevron in a great position to make the best of a bad situation and acquire Noble during the depth of the down-cycle. As explained earlier, that was a strategic win for the company because, in addition to deepening the company's long and deep Permian runway, Noble's huge gas assets in the Eastern Mediterranean are a relatively low-risk and primary organic growth opportunity going forward.

During the Investor Q&A referenced earlier, Chevron announced it will start buying back shares at a $17.5 billion run-rate in Q2. The over-emphasis on stock buybacks during up-cycles, a common mistake in the energy industry over the past 10-20 years, means that the company is arguably buying back more stock during up-cycles (i.e. a high stock price), rather than during oil price down-cycles when the stock is arguably a much better value for shareholders. My followers know I think any allocation of shareholder capital that over-emphasizes share buybacks over dividends directly to shareholders isn't giving them a fair shake and is another way executives can increase their arguably already massive compensation packages (see Chevron: What A Big Dividend Disappointment ).

As noted in this article, Chevron still refuses to invest in renewable solar and wind electric power generation and is allocating relatively little capital to the non-hydrocarbon space. That being the case, Chevron is exposed to potential shareholder capital destruction if the EV transition accelerates and the company is left with stranded assets (primarily oil) were the price of oil - driven by a significant reduction in global gasoline demand - to decline faster than it anticipates.

Summary and Conclusion

I rate Chevron a HOLD. The current valuation seems fair given the current oil and gas price environment as well as concerns about a potential recession on the horizon that would reduce O&G demand and cause prices to decline. However, investors should watch the macro environment closely. I say that because given still very disciplined spending by U.S. shale operators, combined with OPEC+ holding millions of bbls of capacity off the global market, if a recession doesn't materialize, and if the U.S. economy continues with near record-low unemployment combined with a strong summer driving season, we could easily see oil prices strengthen in the second half of the year. Chevron would be in an excellent position to benefit from that scenario. Meantime, Chevron's $6.04/share annual dividend and 3.6% yield are quite attractive. For investors without adequate exposure to the energy sector, Chevron would be a great company to start with because the dividend growth outlook is excellent.

I'll end with a 10-year total returns chart of Chevron versus peers Exxon and ConocoPhillips and note that while Chevron beat its primary peer (Exxon) by 8% over that time frame, it significantly lagged COP (by ~30%) and - despite the 2022 bear market - was totally left behind by the broad market averages as represented by the Vanguard S&P 500 ETF ( VOO ), the DJIA ETF ( DIA ), and the Nasdaq-100 Trust ( QQQ ):

For further details see:

Chevron: Recent Developments And Preview Of Q1 Report Due Friday