ZUMZ - Chico's FAS: A Struggling Fashion Brand That's Turning Around

Summary

- Chico's FAS has had a really rough past few years, with a decrease in location count sending sales lower and hurting bottom line results.

- The company's recovery from the pandemic has been positive, and the management continues to focus on its digital strategy.

- This turnaround in action, combined with how cheap shares are, likely could result in some upside from here.

One of the risks of being a value investor is that you can fall for what is called a 'value trap'. This is a company that looks cheap and that you believe will ultimately appreciate and value, only for it to belong cheap. This is often because of some fundamental issue, but can also be due to other causes. Trying to distinguish between a company that deserves upside and a 'value trap' can be incredibly difficult. One such candidate that deserves our attention right now is a firm called Chico's FAS ( CHS ). In recent years, the financial performance of the company has suffered. But most recently, we have seen a noticeable improvement in its top and bottom lines. Absent this improvement, I believe that the company deserves to be trading on the cheap. But so long as recent trends persist, it could very well buck the definition of a 'value trap'.

A painful few years

According to the management team at Chico's FAS, the company is a Florida-based fashion firm centered around three key brands. The first of these is its hallmark Chico's brand, which focuses on the sale of exclusively designed, private branded clothing for women with moderate to high household income levels. The specific offerings under this brand include several different size categories for clothing, apparel, accessories, and even jewelry. The second brand is referred to as White House Black Market, or WHBM. Through this, the company has positioned itself as a provider of stylish and versatile clothing and accessories, as well as of everyday basics and premium denim, polished casual apparel, relaxed workwear, and more. Like the Chico's brand name, WHBM also focuses on women with moderate to high household income levels. And finally, there is the Soma brand. This largely focuses on private branded lingerie, sleepwear, and loungewear products for women.

{kind=link}

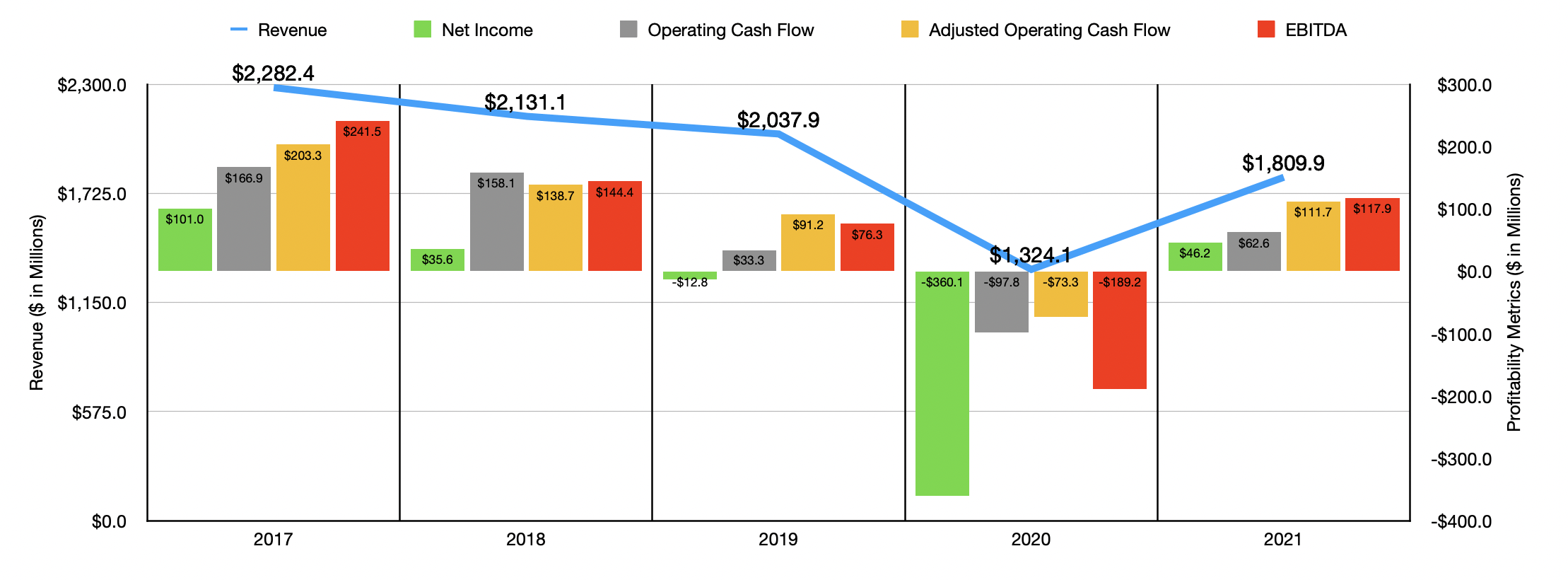

Fundamentally, the picture for Chico's FAS has been rather rocky. From 2017 through 2019, sales of the company inched down year after year, dropping from $2.28 billion to $2.04 billion. Then, in 2020, because of the COVID-19 pandemic, sales plunged to $1.32 billion before rebounding some to $1.81 billion in 2021. The pandemic clearly complicated any sort of analysis of the firm, as has been the case with many other businesses across many other industries. However, it's clear that the firm's troubles began prior to that point. In response to this, in 2020, management decided to focus on transforming the enterprise into a digital-first company. They did this by fast-tracking numerous innovation and digital technology investments throughout not only that year but also 2021. The company also stepped-up marketing efforts to drive traffic and new customers to its brands during this time.

Needless to say, this was a large and bold move by the company. After all, as of the end of its 2021 fiscal year, it operated 1,266 stores across 46 states, Puerto Rico, and the U.S. Virgin Islands. All of this is in addition to the 59 international franchise locations that it sold merchandise through in Mexico and two domestic airport locations. As a note, the pain associated with sales came largely as a result of a decline in store count. For context, at the end of 2017, the company had 1,460 stores in operation. With the decline in revenue and store count also came a worsening of its profitability. Net income went from $101 million in 2017 to a negative $12.8 million in 2019. In 2020, the company posted a loss of $360.1 million. Fortunately, profits rebounded in 2021, with the company earning a net income of $46.2 million. Volatility can also be seen when looking at other profitability metrics. Operating cash flow followed a very similar path. If we adjust for changes in working capital and non-cash lease expense, the picture looks similar. Between 2017 and 2019, adjusted operating cash flow went from $203.3 million to a negative $73.3 million. Then, in 2021, it came in positive to the tune of $111.7 million. Meanwhile, EBITDA went from $241.5 million to negative $189.2 million, before recovering some to $117.9 million, all over this same period of time.

{kind=link}

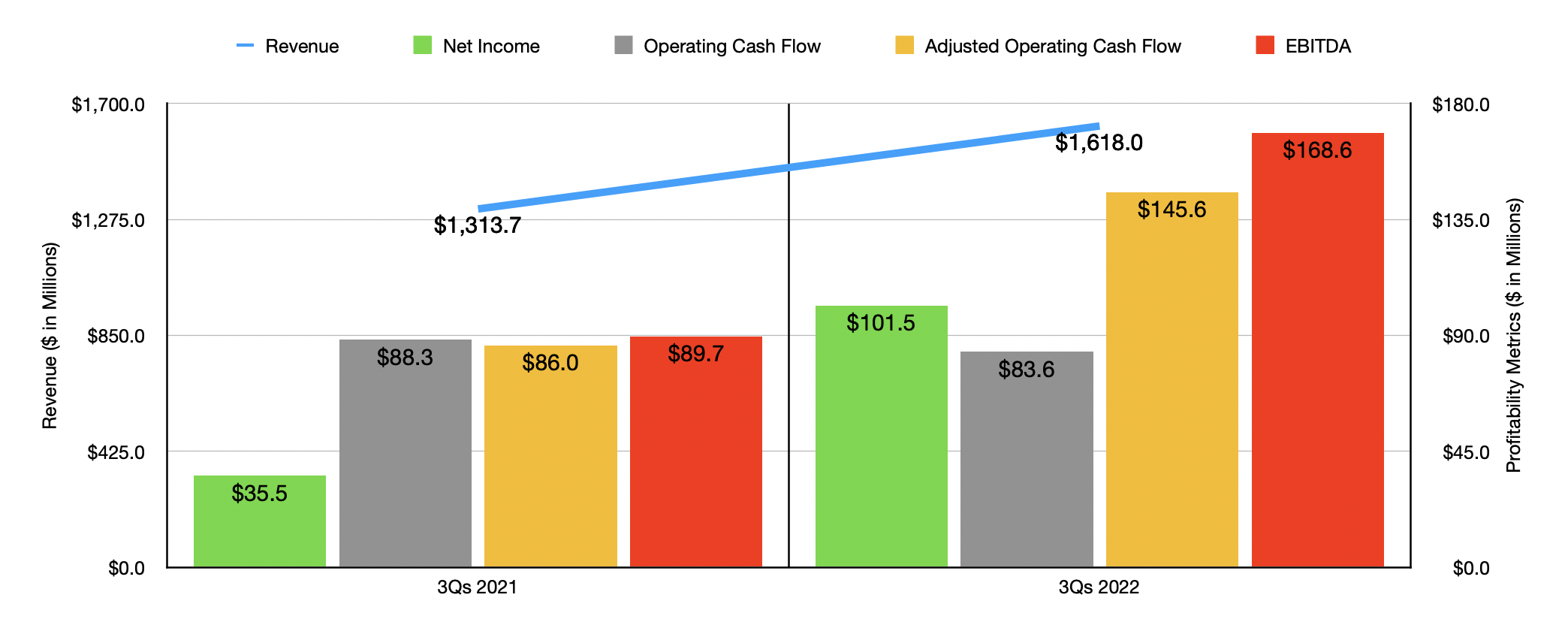

Based solely on the data from 2021, I would not feel comfortable investing in the company. However, we have seen continued improvements since then. For the first nine months of 2022 , sales came in strong at $1.62 billion. That's 23.2% higher than the $1.31 billion reported only one year earlier. The company benefited from strength across two of its three brands. Under the Chico's brand name, sales spiked 33.2%. The WHBM Brand reported a 33.2% increase in revenue as well. The only weakness came from Soma, with revenues dropping 4.9%. Management attributed the sales increase to a 24.7% rise in comparable sales, some of which were offset by 18 permanent net store closures. Management has said that digital sales have been incredibly valuable and have been a tool for growth recently. But they have not revealed any significant details about the contribution to overall revenue and revenue growth from this corner.

The rise in revenue for the company also brought with it significantly better profits. Net income skyrocketed from $35.5 million to $101.5 million. It is true that operating cash flow fell year over year, dropping from $88.3 million to $83.6 million. But if we adjust for changes in working capital, the metric would have risen from $86 million to $145.6 million. Meanwhile, EBITDA for the business also improved, shooting up from $89.7 million to $168.6 million. For 2022 in its entirety, management did say that revenue should be between $2.15 billion and $2.17 billion. Earnings per share, meanwhile, should be between $0.89 and $0.92. At the midpoint, that would translate to roughly $113 million. However, I don't believe that earnings are necessarily the best way to value the firm. Instead, if we annualize results we experienced for the first nine months of the year, we would get an adjusted operating cash flow of $189.1 million and EBITDA of $221.6 million.

{kind=link}

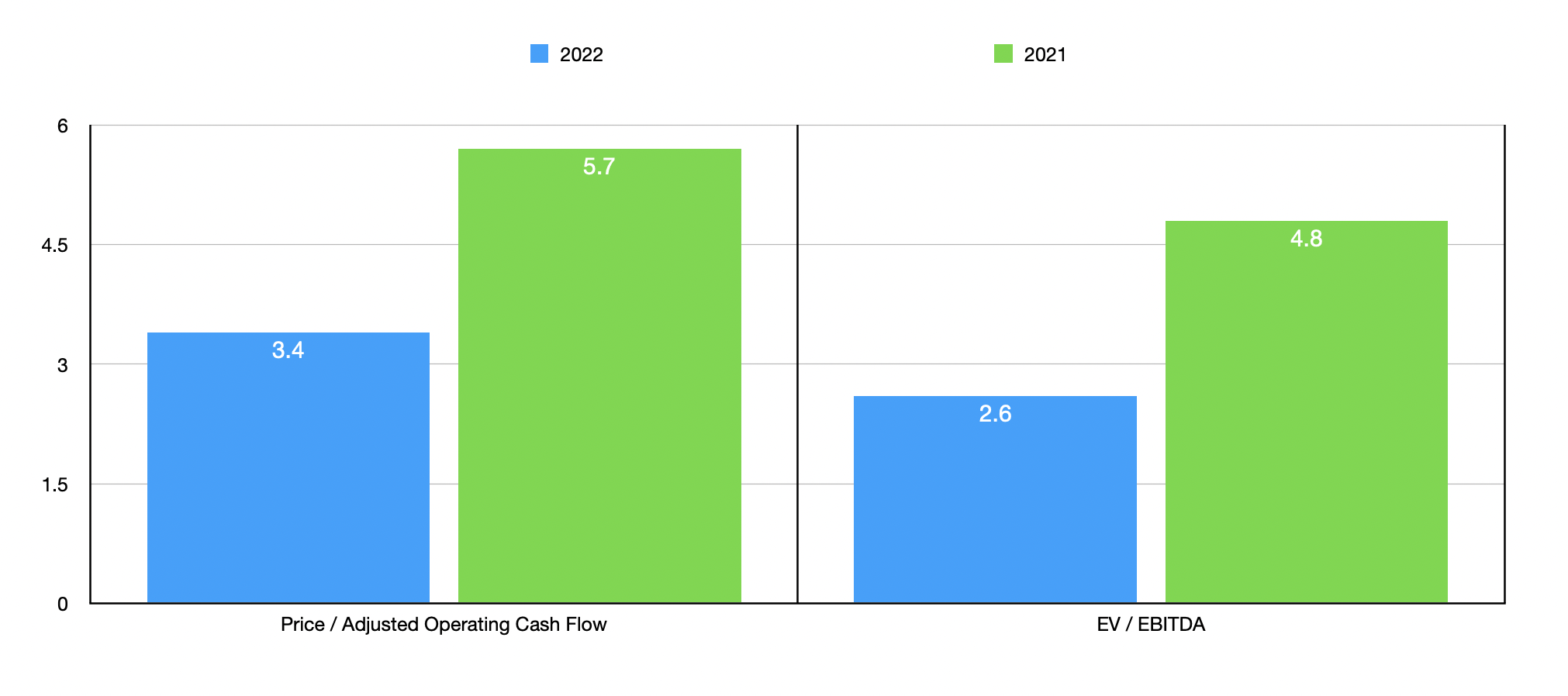

Based on these figures, Chico's FAS is trading at a price to adjusted operating cash flow multiple of 3.4 and at an EV to EBITDA multiple of 2.6. The company is aided on the EV to EBITDA side of things by the fact that it has cash in excess of debt totaling $71.7 million. By comparison, if we were to use the data from the 2021 fiscal year, these multiples would be a bit higher at 5.7 and 4.8, respectively. As part of my analysis, I also compared the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 7.7 to a high of 19. And when it comes to the EV to EBITDA approach, the range was from 3.5 to 4.6. In both of these cases, Chico's FAS was the cheapest of the group.

| Company |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Chico's FAS |

| 3.4 |

| 2.6 |

| Designer Brands ( DBI ) |

| 16.3 |

| 3.5 |

| Genesco ( GCO ) |

| 7.7 |

| 3.7 |

| Shoe Carnival ( SCVL ) |

| 16.3 |

| 4.1 |

| The Children's Place ( PLCE ) |

| 11.9 |

| 4.6 |

| Zumiez ( ZUMZ ) |

| 19.0 |

| 3.9 |

Takeaway

The past several years have been somewhat painful for Chico's FAS. The decline in store count has resulted in falling revenue and struggling profits and cash flows. Fortunately, we are seeing a rather meaningful recovery, with sales, profits, and cash flows all rising nicely. So long as this trend continues, shares do look cheap enough to perhaps warrant some upside. I definitely wouldn't make the case that investors would be wise to hold the stock until it's valued at exactly the same levels as its peers. After all, its track record does justify some discount on this front. But this doesn't mean that the company can't outperform the broader market for the foreseeable future. Because of this, I've decided to rate the business a soft 'buy'.

For further details see:

Chico's FAS: A Struggling Fashion Brand That's Turning Around