CHS - Chico's FAS: An Undervalued And Underappreciated Retail Growth Story

2023-06-29 09:03:53 ET

Summary

- Chico's FAS trades at a discount to apparel retail peers, despite exceptionally strong fundamentals.

- Net cash represents approximately 15% of market capitalization.

- CHS has potential to buyback 15% of its float this fiscal year, given Q1-F23 repurchases and new share repurchase program amount.

- Shares are likely to be re-rated higher as investor sentiment strengthens for consumer discretionary stocks and the company executes a more proactive investor relations strategy.

- There is asymmetric risk/reward for CHS shares, with downside to $4 and upside to $11, over the next 18 months.

Introduction

Chico's FAS (CHS) is a compelling retail apparel stock that trades at a substantial discount to other retailers in the space. There is asymmetric risk/reward, given $1 per share downside risk (roughly 20%) and $4 to $6 per share upside (roughly 100%) potential over the next 12 to 18 months, in our view. Management has successfully transformed the company into a "digital first" retailer and de-risked its balance sheet, such that at the end of Q1-F23 there was $107 million of net cash ($131 million of cash and marketable securities minus $24 million of long-term debt). Shares are likely to significantly appreciate, upon stronger investor confidence in the macroeconomy (i.e. when recession concerns subside) and therefore interest strengthens for risk-on assets, such as consumer discretionary stocks.

This is the fifth article on Chico's FAS that we have written for Seeking Alpha. This time, we are providing a company update by detailing our perspective on recent corporate developments and reiterating our investment thesis. Here are our previous analyses:

November 28, 2022 - Chico's FAS: Shares on Clearance Rack After Another Beat-And-Raise

September 2, 2022 - Chico's FAS: Sell-Off After Beat-And-Raise Presents Buying Opportunity

December 1, 2021 - Chico's FAS: Building Greater Investor Confidence

October 12, 2021 - Chico's FAS: A Chic Turnaround Underway, Potential Substantial Upside

CFO Transition: Oliver In Charge

Approximately one week after reporting Q1-F23 results, CHS announced PJ Guido resigned as chief financial officer to accept a position with another company. As a result, David Oliver, chief accounting officer, was promoted to chief financial officer effective June 24th.

In our view, strength of management is among the most important factors to consider when evaluating a stock. As a result, investors are generally nervous when management changes occur, particularly for either the chief executive officer or chief financial officer.

In this case, we believe investors should not be worried. Guido left Chico's FAS with an exceptionally strong balance sheet (net cash of $107 million, representing $0.87 per share or approximately 15% of its market capitalization). Moreover, Oliver is a company veteran, having joined the retailer more than 10 years ago and serving as interim chief financial officer during the pandemic and until Guido joined CHS in late 2021. We also find the reason for Guido's departure entirely reasonable. Jeff Lick, an analyst at B. Riley Securities who recently launched coverage of CHS, wrote in a research note that Guido commuted weekly from out of state to the company's headquarters in Fort Meyers, Florida, and he simply needed a better work / family-life balance.

We have full confidence in Oliver's ability to be effective and create shareholder value in his expanded role. We also note that Oliver is well-known to investors and therefore applaud the company's board of directors swiftly promoting him rather than embarking on another time intensive (and perhaps costly) executive search process.

Q1-F23 Results: Better Than Expected

After successfully navigating the pandemic, Chico's FAS shares appear to be stalled in a trading range between $4 and $7. While the stock has generated significant share appreciation from the sub-$1 level during the pandemic (late 2020), the stock now appears to trade mostly on retail industry / consumer discretionary sentiment.

For example, on May 31st, one week before CHS reported Q1-F23 results, the stock closed down 12% to $4.54 (after recovering 5% from the intraday low of $4.34). There was no news and only speculation that the retailer's performance in Q1-F23 was weak, given inflation and other macroeconomic concerns.

A week later, CHS announced Q1-F23 earnings, which were significantly better-than-expected. Quarterly EPS was $0.32, 19% better than the $0.27 consensus estimate. Since other retailers during Q1 earnings season provided cautious outlooks for the balance of the year, we think CHS opportunistically lowered its full-year guidance thinking it had a "free pass" to do so. EPS guidance was lowered to $0.70 - $0.82 from $0.79 - $0.91. Management's strategy worked: shares catapulted 11% to $5.41 (from $4.89), as investors focused more on the Q1 earnings performance and discounted the lowered full-year guidance.

During its conference call , management blamed its moderated full-year outlook on low inventories at White House Black Market that are impeding higher sales growth, as well as choppy store traffic trends across the retailer's three concepts at both full-price and outlet stores. However, based on very positive commentary by management on the conference call, we think CHS lowered expectations so they could easily exceed them later in the year.

We remind investors that in January 2023, CHS lowered its Q4-F22 EPS guidance range to ($0.02) - $0.00 from $0.07 - $0.10 before presenting at the ICR Conference. This was approximately three weeks before the end of its quarter (based on the retail calendar). Two months later, CHS reported EPS of $0.06 compared to the $0.00 consensus estimate. As a result, by utilizing this strategy, CHS successfully shifted the narrative from a potential miss by $0.01 or $0.02 to a solid $0.06 beat.

Key Takeaways

In our view, there are significant takeaways from the Q1-F23 report that bode well for the remainder of this year and our long-term investment thesis. (Unless otherwise cited, all of the factual information discussed in this section and highlighted as key takeaways are sourced from the conference call transcript .)

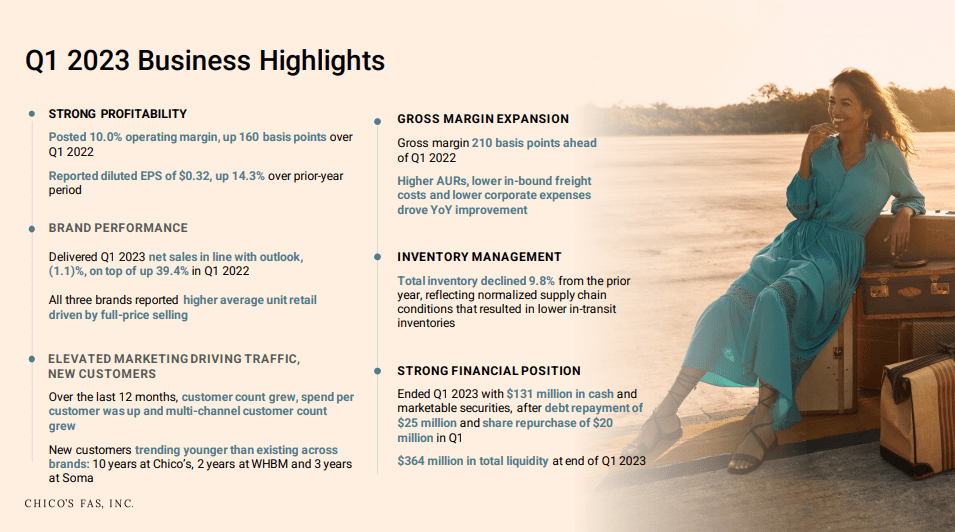

Chico's FAS Q1-23 Business Highlights (Chico's FAS)

{kind=link}

We think management gained more credibility with its Q1-F23 performance by providing more evidence that its strategic vision is bearing fruition: to be customer-led, product-obsessed, digital-first, and operationally excellent. CHS gained market share for all brands, with healthy full-priced selling and growth in both spend per customer and average unit retail. At the Chico's brand, strength in these key performance indicators demonstrated customers' affinity for innovative fashion and complete outfits. At the White House Black Market brand, despite same-store sales being down 8% year over year (while up 57% on a two-year stacked basis), customers reacted so strongly to newness in fabric innovation and fashion that CHS simply ran out of inventory during the quarter. With that said, a clear catalyst for 2H:23 is more alignment on inventory with customer demand.

Perhaps most exciting to us and supportive of our investment thesis is that during the past year, the multi-channel customer count was up 6%, spend per customer grew by 7%, and the total customer count increased by 2%, indicating exceptional long-term potential for each brand. This directly correlates to earnings growth power, since CHS across brands has attracted customers that are truly focused on fashion and newness rather than pricing and value. In our view, this is a critical differentiating factor for CHS and is the core reason for this retailer's resilient outperformance within the industry. CHS caters to an affluent customer whose spending has generally been unaffected by inflation and other macroeconomic concerns. This is why we believe that CHS deserves to be re-rated higher on valuation, rather than languishing with a mid-single digit P/E multiple.

Due to exceptionally effective digital tools driving customer engagement as well as fashion emphasizing quality and newness, CHS is attracting younger new customers across its brands. Compared to existing customers, new customers are 10 years younger at Chico's, two years younger at White House Black Market, and three years younger at Soma.

Moreover, management is emphatic that closing stores has been highly accretive to its profitability. During the past few years, CHS has been optimizing its store fleet. To this end, 7 stores were closed in Q1-F23, resulting in 1,262 boutiques at the end of the quarter. In addition, CHS has negotiated longer-term new and renewed leases with more favorable terms in better locations.

Returning Capital To Shareholders

During Q1-F23, Chico's FAS resumed returning capital to shareholders by resuming activity on its share repurchase program. CHS repurchased $19.8 million in stock, representing $3.25 million shares at an average price of $6.09 per share.

To further underscore its commitment to this initiative, the board of directors authorized a new $100 million share repurchase program , replacing its previous one that had $35.4 million remaining. Therefore, the net incremental authorization is $64.6 million. Given the activity year-to-date, we expect CHS to exhaust this current program by the end of this fiscal year, averaging approximately $33 million per quarter. If we were to assume the average price remains at approximately $6 per share, then CHS would repurchase an additional 16.5 million shares. Combined with the Q1-F23 activity, CHS would repurchase more than 15% of its diluted shares outstanding.

Valuation

For comparative valuation purposes, we suggest analyzing the following retail stocks: Capri Holdings ( CPRI ), Guess ( GES ), J. Jill ( JILL ), and The Buckle ( BKE ). Based on consensus F2023 estimates, CPRI trades at 6.1x, GES at 7.2x, JILL at 9.2x, and BKE at 8.8x, resulting in a 7.8x average multiple. However, CHS currently trades at 6.9x, a discount of nearly a full turn. Even if CHS were to be valued at the group average, the stock would be $6.08, 12% higher than current price. However, with more than 15% of its market cap in net cash and a share repurchase program that is poised to retire 10% of its float, we contend CHS deserves a premium valuation of at least 9x which translates into a $8 stock price based on our $0.90 above-consensus F2023 EPS estimate. However, as we are nearly at the mid-year of 2023, we suggest a 12-month price target would blend EPS estimates for F2023 and F2024. Our EPS estimate for 2024 is $1.05, and therefore the two-year average EPS is $0.98, resulting in a 12-month price target of $9. For our 18-month price target (i.e. year-end 2024), we only utilize our F2024 estimate and increase our valuation to 10x for a more normalized economy, resulting in an $11 price target.

Catalysts

White House Black Market. Given the current inventory flow issues at the White House Black Market concept combined with a fashion miss (i.e. issue with party dresses) in Q4-F22, we think there is significant upside in 2H:F23, provided the right fashion and inventory levels. Management has already fixed the former, and the latter will be corrected for Q3-F23.

Investor relations. Earlier this year, CHS hired Julie MacMedan as Head of Investor Relations . We think this signals a shift in investor relations strategy to be more proactive. In our view, since only two analysts cover CHS, management needs to be more visible with the investment community to better publicize its operational and financial successes. To this end, we highly suggest that management present at more investor conferences, engage with potential investors in more non-deal roadshows, and collaborate with sell-side analysts, whether or not they currently cover CHS, for "fireside chats" to further pitch the CHS story to investors.

Share repurchase program. The new $100 million share repurchase program should serve as a backstop for the shares, as well as be an incremental driver for EPS growth.

Balance sheet. With a mere $25 million in gross long-term debt on its balance sheet at the end of Q1-F23, we fully expect CHS to be debt-free by end of the current quarter. If so, this could improve investor sentiment.

Inflation. Since CHS trades in-line with general market views on the retail industry / macroeconomic trends, we suggest that continued moderating inflation trends would help turn the market more positive on consumer discretionary stocks.

Risks

Macroeconomy. Whether perception or reality, macroeconomic sentiment currently drives consumer discretionary stocks, and CHS is no exception even if its core customers are more "recession-resistant." As a result, higher interest rates, "higher for longer" monetary policy, lower consumer confidence, or stubbornly high inflation could negatively impact CHS shares.

Fashion. As demonstrated in Q4-22, there is some fashion risk, particularly at the White House Black Market brand. A merchandising miss would likely cause CHS to miss sales and earnings forecasts.

Management. In our view, strength of management is among the most important factors to consider when evaluating a stock. Our investment thesis is heavily weighted on Molly Langenstein's phenomenal and transformational leadership as chief executive officer. If she were to depart from CHS, we would re-evaluate our view on the stock.

Conclusion

We think Chico's FAS is among the most attractive retail apparel stocks. The risk/reward is compelling, with realistic downside risk to $4 with upside potential to $11 over the next 18 months. In our view, the CHS turnaround is only mid-cycle, especially when considering the new dynamic customer loyalty program that continues to gain momentum and the anticipated rebounds at White House Black Market and Soma in 2H:F23. Moreover, we believe that in addition to earnings growth driving share price appreciation, shares will be re-rated higher (i.e. P/E multiple expansion) over the next 18 months as investor confidence strengthens in consumer discretionary stocks and the company executes on a new proactive investor relations strategy.

For further details see:

Chico's FAS: An Undervalued And Underappreciated Retail Growth Story