CHS - Chico's FAS: Attractive Valuation But No Catalysts To Grow

Summary

- The dynamics of consumer spending on clothing continues to be under pressure.

- Chico's FAS announced a reduction in guidance in view of macro headwinds.

- The company is trading below fair growth, however, I do not see any catalysts for the growth of the stock in the coming quarters.

Introduction

Chico's FAS (CHS) shares have risen 4% YTD. Despite the fact that the company is cheaply priced according to multiples, and the DCF model indicates that there is fundamental upside potential for CHS stock, I believe that now is not the best time to go long. In my personal opinion, rising inflation and a decline in real incomes will continue to affect the company's revenue dynamics in 2023, while the effect of traffic recovery in the chain's stores may have already been exhausted. Thus, I expect pressure on the company's operating and financial performance in 2023.

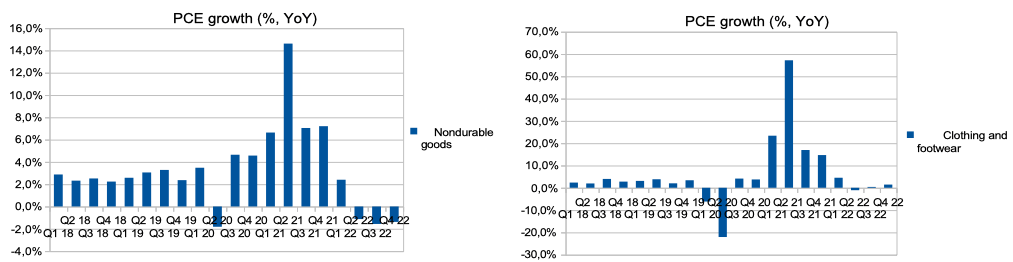

The survey of current trends

Rising inflation and declining real disposable income continue to weigh on consumer spending. Thus, total consumer spending on "Nondurable goods" is in the negative zone during 2-4 quarters of 2022. Clothing and footwear spending is one of the Nondurable Goods segments where consumer spending looks a bit better, but the pressure is still there. I believe that in 2023 we will see how lower consumer spending in the discretionary segment will put pressure on the company's revenue dynamics, as the effect of store openings and traffic recovery will be exhausted. On the charts below, you can see the details of consumer spending.

{kind=link}

Projections

I made my own assumptions about the future cash flows of the business in order to evaluate the company. You can see the main assumptions of my forecasts below:

Revenue growth: in my model, I conservatively assume revenue growth of 5% by the end of 2023 due to rising inflation and a decrease in real income, then I predict stable revenue growth of about 7% per year until 2026.

Gross margin: I predict slight pressure in 2023 due to a weakening consumer, so I assume that the gross margin in 2023 will decrease to 39%, then I predict a recovery to 41% by 2026.

SGA: I believe that by the end of 2023 we will see a slight increase in spending on SGA (% of revenue) to 33.5% due to reduced economies of scale, then I predict a gradual decrease to 32.5% by 2026.

You can see the results of my predictions in the chart below.

Yearly projections:

Forecast (Personal calculations)

Valuation

I prefer to use the DCF approach to value a company. First, the company operates in a stable market where the use of DCF is most preferred. Secondly, using the DCF model allows me to make assumptions about the future growth rates and operating profitability of the business. Also, when forecasting, I can rely on management comments and guidance.

The main inputs in my model are:

WACC: 12.8%

Terminal growth rate: 3%

DCF model (Personal calculations)

Multiples

In addition, I calculated the current and future P/S and P/E multiples for the company based on my sales and net income forecasts. You can see the results of my predictions in the chart below.

Multiples (Personal calculations)

Risks

Competition: increased competition could lead to lower market share, lower revenue growth and lower operating margins due to higher marketing costs, competition for labor and failure to raise prices for key products.

Margin: decreasing economies of scale due to reduced store traffic and lower average check, as well as rising operating costs, could put pressure on the business's operating margin going forward.

Macro: high inflation, declining real disposable income and declining consumer confidence could lead to lower consumer spending in the discretionary segment, which could have a negative impact on business revenue dynamics in the future.

Drivers

Revenue growth: new store openings, traffic and average check growth, and effective marketing could support the company's revenue dynamics in the coming quarters.

Macro: decrease in inflation, reduction of the key rate, recovery of real incomes and consumer confidence of the population may contribute to the growth of the company's revenue in the future. In addition, increased economies of scale could support operating margins.

Conclusion

Despite the fact that I like the company and its business model, in my personal opinion, now is not the best time to go long. I believe that in the first half of 2023 we will see continued pressure on consumer spending, which will continue to put pressure on business revenue dynamics. In addition, a decrease in revenue may cause a decrease in economies of scale, as a result of which operating margins may deteriorate. Based on my DCF model and multiples valuation of the company, I see fundamental upside as the company continues to trade below fair levels, however I see no growth catalysts in the next few quarters. I will gladly change my forecast when consumer behaviour begins to normalize and real incomes of the population begin to grow.

For further details see:

Chico's FAS: Attractive Valuation But No Catalysts To Grow