GPS - Children's Place: Updating The Thesis

2023-10-26 08:37:27 ET

Summary

- Children's Place is a specialty retailer of children's clothing with $1.6B in revenues, focusing on millennial moms.

- PLCE has faced challenges due to the pandemic and inflated costs, but these headwinds have now abated.

- The company has optimized its store base, reduced costs, and expects significant improvements in margins and debt/EV balance.

Compelling investment opportunities should be easy to explain. Last December, I publicized my thesis for owning Children's Place ( PLCE ), which has largely transpired without the stock responding. Am I crazy, or is the market wrong? I recently got the chance to pitch the idea at the MicroCapClub annual summit, so I wanted to take this opportunity to update the thesis for my Seeking Alpha readers. Unlike some retailers that have struggled adapting to the post-Covid retail environment, I believe PLCE's fate largely rests in its own hands, with significant levers to pull for self-help.

Who?

Children's Place is a specialty retailer of children's clothing with $1.6B of TTM revenues. PLCE has 600 physical stores, but 50% of their sales are driven through their own website and via Amazon. PLCE also owns the Gymboree brand (which they bought out of bankruptcy in 2019), and recently launched new brands PJ Place and Sugar & Jade.

What?

{kind=link}

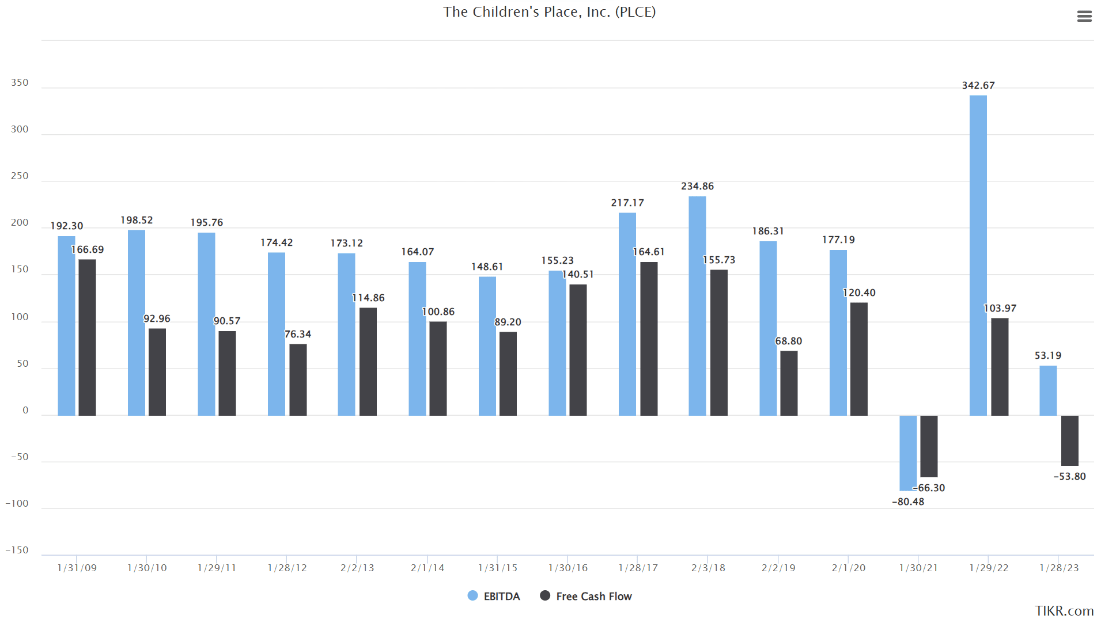

PLCE historically generated significant operating earnings and cash flow, before being walloped by the pandemic and inflated costs from cotton and freight in FY22. Investors must decide if the business is permanently impaired after these two bad years, or if it is functionally the same business trading at a fraction of the historical valuation? This is particularly relevant since the company historically plowed excess cash flow into buybacks, which would quickly be accretive if the business still generates $100m/year on a normalized basis.

How?

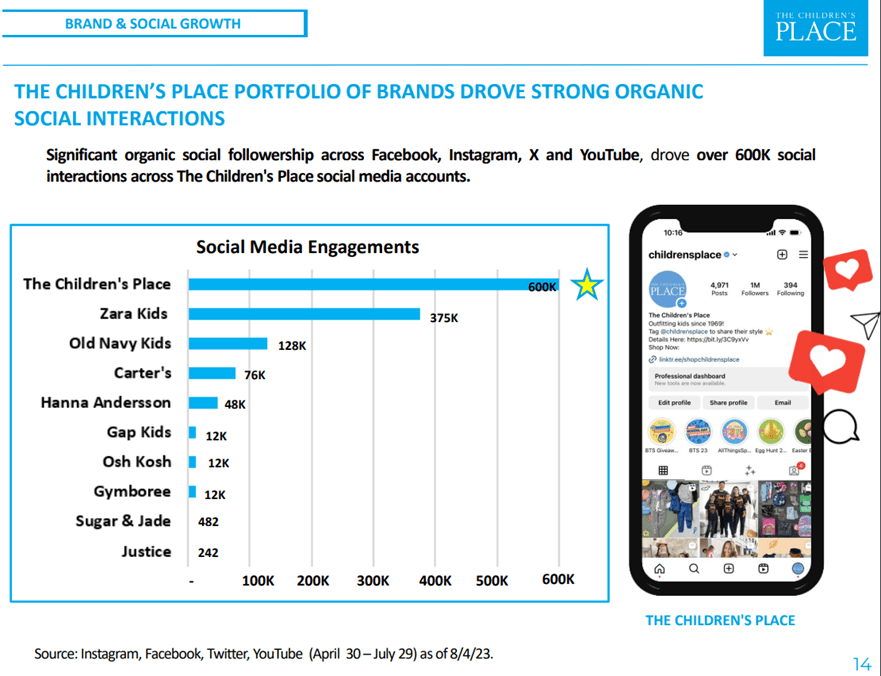

PLCE is focused on one core customer: millennial moms. Unlike peer Carter's ( CRI ), they do not view their stores as a primary customer acquisition channel, but focus heavily on social media to drive the business:

{kind=link}

This is further evidenced by recent campaigns featuring boy band members from prior decades and other ads with Mandy Moore and the Jonas Brothers . The resulting engagement shows PLCE stacks up very well versus peers like CRI, Old Navy and Gap ( GPS ), especially during PLCE's core back-to-school season:

{kind=link}

Why?

I expect most investors to be kept at bay by declining revenues, shrinking margins, and ballooning debt. These are all good reasons to be concerned, after all. But peeling back the layers leads to a different conclusion:

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| GM % |

| 38.0% |

| 35.3% |

| 35.0% |

| 21.9% |

| 41.5% |

| 30.1% |

| OI % |

| 8.9% |

| 6.1% |

| 5.5% |

| (9.6%) |

| 14.8% |

| 0.1% |

| Headwind |

| Gymboree (>$1B) Liquidation |

| Covid |

| Cotton/Freight (7.3%) |

As you can see, PLCE has had unique, specific headwinds that have now abated. Gymboree is liquidated and now owned by PLCE, while cotton and freight have normalized from pandemic highs, and industry inventories have come down from 2022 highs. Of note, the benefits of normalized cotton and freight have yet to hit PLCE financials (inventory costs run on a ~9-month lag), which is perhaps why the stock has yet to respond.

While all this was happening, PLCE has optimized their store base, reducing count from ~1,000 in 2018 to an expected 500 in 2024. They managed this quickly via short lease durations with an eye toward converting sales from legacy brick and mortar locations to the internet, where their target millennial mother customer resides, and they achieve higher operating margins. The decrease in store base and volatile sales around Covid are obscuring their growing online and Amazon wholesale segment.

They also optimized their corporate cost structure, trimming jobs over the summer that will result in significant SG&A savings in 2024, along with an early exit from their corporate headquarters lease for additional savings beginning in May-24. These cuts reflect a much smaller store base than what they managed previously and will drop straight to further operating margin improvement in the coming year. Instead, what most people are seeing are the one-time costs from these efforts, not the future benefits.

Regarding the debt, PLCE is paying SOFR + 2 for their current credit facility, which they guided to paying down at least $159m by the end of the fiscal year via cash flows and reiterated as recently as 9/14 . The interest rate will decrease if PLCE can achieve $200m EBITDA over 4 consecutive quarters. I expect leverage fears will decrease significantly as PLCE generates cash in the back half of this year and shows better debt/EV balance.

Lastly, I think many are missing another self-help lever PLCE can pull. The company grew e-commerce so rapidly, they hit capacity at their 700k square foot Alabama distribution center and have outsourced about 1/3rd of their fulfillment to a third party. A $40m/18 month expansion project should bring all fulfillment back in house, improving margins and further reducing inventory levels (not having to carry multiple products in each location).

From the Q4-22 call:

This owned DC already operates at significantly lower cost than our third-party fulfillment centers, and once our expansion is complete, we will move more of our fulfillment from third parties to our lower cost owned DC, which is expected to further expand margins.

Valuation

I expect PLCE to finish the year with about $200m of net debt and to guide to at least $5/share of EPS, implying the stock trades at 5x my FY24 estimate. Given the company has historically plowed excess cash into buybacks, I don't think the status quo can be maintained indefinitely, especially if PLCE can shift perceptions around risks from their leverage, margins, and growth. If the stock doesn't move with this setup, I would expect significant buybacks or private equity interest.

Risks

- Cotton and freight become headwinds again ( can be tracked , with cotton prices generally displaying a 9-month lag per Management).

- Recession hits in 2024 and PLCE proves less resilient than they were in 08/09 ( flat SSS ).

- Amazon relationship changes and operating margins no longer hit accretive double-digit range expected by Management (Amazon is pulling back on private label ).

- Pressure from Temu and Shein spending aggressively to acquire US customers impacts marketing costs or sales. (Note - PLCE pricing is competitive with both )

- Shrinking store base impacts online revenues and reduces operating leverage.

Conclusion

I believe people are missing the opportunity at PLCE due to optically high leverage, declining margins, and bloated inventory. The company has already confirmed these pressures are turning into tailwinds, and as the results are solidified in the coming earnings reports, I expect the stock to re-rate substantially. With lower leverage, better margins, and stabilizing sales, PLCE will again be able to return to their bread and butter - buybacks. I believe PLCE represents one of the best values in the market as we enter 2024.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Children's Place: Updating The Thesis