LAC:CC - Chile's Lithium Nationalization Decision Validates My Risk-Averse Investment Strategy Approach

2023-04-26 22:00:09 ET

Summary

- Given the constant sources of instability that keep coming this decade, my early decision to diversify, by among other things roughly quadrupling the number of stocks in my portfolio is vindicated.

- The Chilean Government's decision to nationalize its massive lithium industry is the latest example of factors that go beyond financial analysis that can affect one's investments.

- I started building a position in lithium mining stocks this month, based on fundamentals with three stocks that now collectively make up about 5% of my portfolio.

- There is a good chance that all three investment choices will work out in the long term, even though they are currently being impacted, because of my frugal entry point.

- Within the current environment, the potential for geopolitical, political, social, economic, financial, and monetary risks greatly impacting any particular stock available for trade is limitless and risk should be priced into assets accordingly.

Investment thesis

As we approach the halfway point of this decade, it is becoming increasingly clear that from day one, it was always going to be an eventful one and it will probably continue to be interesting for the foreseeable future. For investors, it has been a rollercoaster ride, starting right at the beginning of the decade with the COVID pandemic, and there has been no letup since then. There are geopolitical frictions and shifts in global alignments, fiscal and monetary issues, and the first hints of a potential banking crisis. Most recently, lithium mining stocks were hit hard by Chile's announcement that it intends to nationalize its massive lithium industry. It happened just as I started building a position in lithium mining stocks this month, which are well off of their highs. Luckily I have been keeping a very disciplined policy of avoiding building a position in any stock that exceeds 3% of my overall stock portfolio, thus I am currently looking at around 5% of my overall portfolio exposure to the lithium mining sector, with not all three stocks being impacted by the Chile situation. My general reluctance to invest in companies experiencing all-time highs also helps.

The new risk management strategy I employed a few years back is meant precisely for such occurrences because I expect such events to keep coming with perhaps increasing frequency. Some events will have a broad impact on one's portfolio such as monetary policy changes, while this move by Chile is more of a sector-specific issue. As I wrote on many occasions in the past few years, the challenge for investors this decade will be to just preserve real wealth. In other words, try to beat inflation. The task is all the more challenging, given that the investment scene is increasingly proving to be loaded with landmines that threaten to take a chunk out of one's portfolio every time a landmine goes off. In this respect, damage control meant to keep those chunks small is the best that one can do, because no one can ever know where those mines may be hiding and which one might go off next.

The decade so far has been very volatile, and there is no reason to expect an improvement going forward

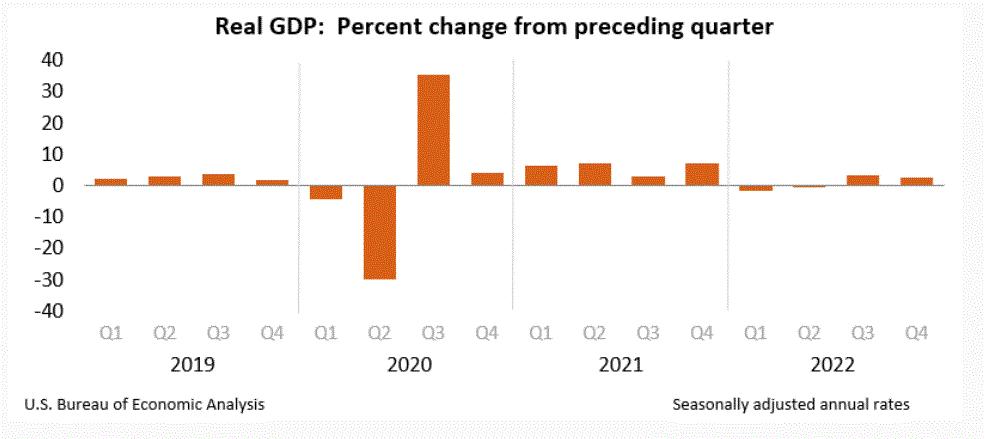

As some light at the end of the COVID crisis tunnel started to shine through in 2021, hope emerged for a prosperous time ahead for the global economy, and naturally, a recovery-fueled investment opportunity that held great promise for the rest of the decade. Average economic cycles lasted about a decade in the past, measured from the beginning of one crisis, to the start of the next one. About 4/5 of the cycle tends to consist of the recovery period. Clearly, this post-COVID recovery is not that kind of recovery. Many major economies experienced negative quarters of growth last year, some of them even experienced official recession conditions, as measured by two consecutive quarters of economic contraction.

U.S. Bureau Of Economic Analysis

{kind=link}

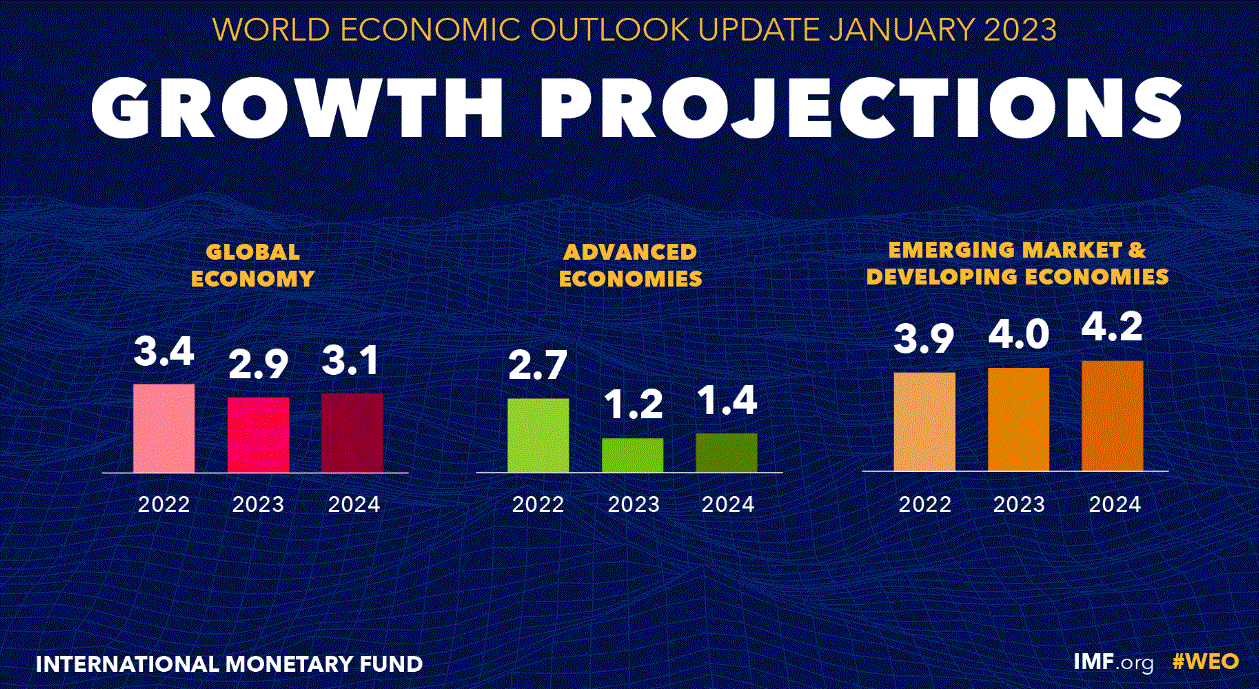

Most forecasts for global economic growth for the rest of this first half of the decade do not present an upbeat picture.

{kind=link}

The one factor of note in this IMF forecast is the fact that for this year and next, the developed economies are seeing their growth cut in half compared with last year's already underwhelming performance, while the emerging economies are actually seeing a very slight acceleration in growth. Ordinarily, this would not be such a major issue. Just a decade ago, China's economy was about 1/3 the size of the US economy, as well as that of the EU. Today, it is larger than the EU economy, and it is closing in on the US in terms of nominal size. India will probably overtake the EU by 2040, to become the world's third-largest economy.

Some historians pointed to Germany's unification and rise as an economic power in the 19th century as being at the root of WWI. A major shift in Europe's balance of power, disrupting a centuries-old status quo inevitably led to frictions that could not be solved. Perhaps, we are arguably also at that point now, where a major shift in the global economic balance of power to Asia is inevitably causing friction. We should all hope that it will not lead to a global war between major nuclear-armed powers. It might be expected however that we will see more proxy wars, as well as economic warfare on a low scale, or at times even high-intensity confrontations which will be very damaging to all sides.

We should recognize that there is always a path to lessening friction, in which case perhaps the second half of the decade will see us return to higher global economic growth rates, which in turn can improve the investment environment. Having said that, even in such a best-case scenario, we still seem to have a major commodities shortage issue.

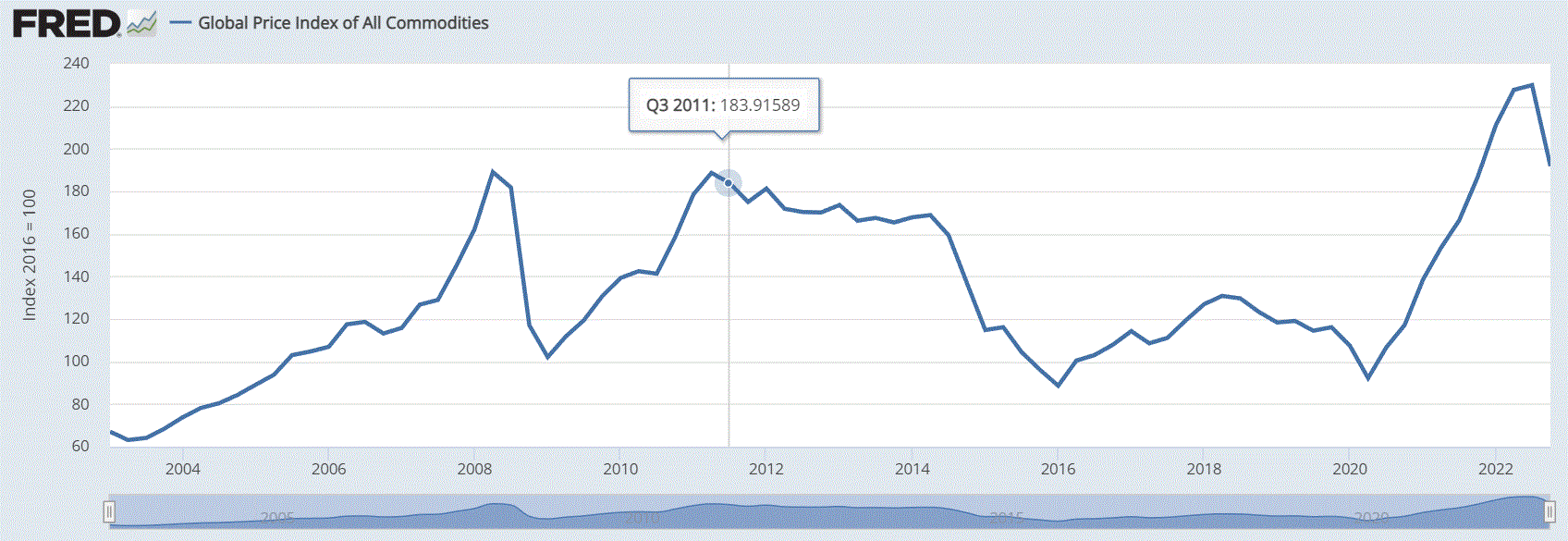

Federal Reserve Bank of St. Louis

{kind=link}

As we can see, despite the weak global economic expansion period we are going through, global commodities prices were still collectively at a record high as of the end of last year. We might see a bit of a reprieve in terms of global commodities prices this year, mostly because global economic growth has seen some deceleration. I believe that in the absence of further deterioration in global economic growth, towards the end of this year, or perhaps sometime next year we might be potentially looking at new record high commodities prices.

My 3% or less of the total portfolio rule is starting to prove its worth within the context of the Chilean decision to nationalize the lithium industry

I went from having on average about 7 to 8 company stocks in my portfolio at any given time just a few years ago, to now having about 25-30. Most of my positions in individual stocks make up 3% or less of the total portfolio. At times, it tends to be tempting to break with my own strategy. However, as the news broke of the Chilean plan to nationalize its lithium industry, where the biggest lithium miners, Albemarle ( ALB ) and SQM ( SQM ) have major operations, I was reminded of its value. Aside from the two miners mentioned above I also bought some Lithium Americas ( LAC ) stock, which was not as heavily affected.

As the market reacted, before we can gain an appreciation of the impact that the Chilean decision might have on lithium miners, causing a roughly 15% decline on average in Albemarle & SQM stock price in one day, the value of avoiding overexposure to any particular company became apparent. Lithium Americas was not impacted particularly hard, since it does not have direct exposure to Chile. The net effect of the plunge in Albemarle and SQM stocks on my overall portfolio was thus about -.5% on the day. If their stock prices would hypothetically go to zero, it would hurt my returns for the year, but not to an extent that it becomes a dramatic hit on its own.

A healthy cash buffer to counter any broad market downturn

In the event that we see a trigger that will hit the entire market, like for instance Russia deciding to withhold perhaps a quarter of its crude and products exports from the global markets in retaliation for our economic pressures on it, having some cash on hand is one way to turn a significant, broad downturn into a positive. I currently hold about 25% of my investment portfolio in cash. It helps to have cash on hand in order to invest in stocks and industries that may face a temporary setback, which provides a good entry point into certain stocks.

Within the context of a high-inflation environment, holding cash seems like a poor choice, since its value erodes at an accelerated pace. However, once it is deployed in well-timed investments, hopefully with the majority of those investments performing according to expectations, it is a far better net return on one's portfolio, compared with having the cash deployed with very limited reserves available to take advantage of potential buying opportunities as they arise.

There is one potential upside to the increased market volatility that we are seeing, and that is a rise in opportunities to take advantage of significant market downturns as we saw with lithium miners in the past months. It is possible that the news coming out of Chile may have been the trigger for the likes of Albemarle and SQM to form a bottom in their stock price. This is likely to be the case if the slide in the lithium spot price will stabilize soon. In that case, investors who bought at or near those lows or lows that are yet to come soon, are likely to reap the benefits of a potentially perfectly timed entry point.

It remains to be seen whether or not this will be an ideal example that will prove my point or not about the need to always have a significant cash position on hand to be able to take advantage of potentially advantageous entry points as they suddenly and often unexpectedly present themselves. Even if the answer is no, the 3% rule for my portfolio means that the stakes for being wrong on one or two such attempts at finding a favorable entry point will not drag down the overall performance of one's portfolio, as long as the other attempts turn out to be solid. Maintaining a healthy cushion of cash is key to being able to take advantage of multiple opportunities that might arise given the increasingly volatile market environment.

Investment implications

The most important takeaway from examining the way this decade has gone so far is that it is not a business-as-usual decade. This is a decade of change. Perhaps it is a decade that is coping with change that occurred over the past few decades. The massive change in the global economic balance, with a clear and massive shift to Asia over a relatively short period of time is perhaps the most disruptive event to take place in human history, in a very long time.

{kind=link}

The change is still ongoing and arguably accelerating. The end result will be a worsening of the global geopolitical landscape, which is helping to saturate the investment field with minefields.

Add to it the myriad of other problems, social, economic, fiscal, and institutional as well as growing evidence that we are faced with severe pressures on resource availability to meet our growing needs and we have the situation we see before us. We live in interesting times and the net outcome for investors is less than appealing.

Dow Jones Index (Seeking Alpha)

In the almost three and a half years since the turn of this decade, the Dow Jones is up about 19%. Compounded inflation since the turn of the decade is about 16%. In other words, so far this decade, a well-balanced portfolio that did as well as the Dow, just managed to beat inflation so far this decade, not much more. Unfortunately, many investors do not even do as well as these averages tend to.

One can argue that the lack of inflation-adjusted gains in stocks is a reflection of the massive disruption that the COVID crisis has caused to the global economy. I personally see plenty of factors ahead that suggest the rest of the decade will be at best as good as the first three and a half years of this decade. There are plenty of reasons to expect things to get far worse, as I pointed out. What is more, sectoral or company-specific hits to one's portfolio are likely to be amplified in frequency as well as in the size of the impact. For this reason, having a portfolio that keeps exposure to any one particular company limited is now arguably the best investment risk contingency plan out there.

The Chile situation in regard to the lithium industry is just the latest example of the increasingly volatile world we live in, which could impact any investment at any point. I am personally keeping away from investing in companies making new all-time highs. The higher they are, the further they can fall. Going back to the SQM & Albemarle situation, their respective stock prices were already down about 1/3 this month from their previous all-time highs. As I write this, the Chilean news brought them down another 10% or so from my entry point. Given that the Chile announcement is not immediately impactful, and it is less dramatic than the headlines would suggest, I believe that I have a good shot at still walking away with a decent gain, on the back of a reversal of lithium prices back higher, somewhere between this year and 2025.

I am far less certain about these stocks reaching and surpassing their previous all-time highs by the middle of this decade. There is even a decent chance that they will never surpass those all-time highs again. Similar situations are likely to arise with growing frequency and there are few investment options out there that we can expect to be potentially safe going forward. There are no more safe haven stocks, sectors, and increasingly not even countries or regions. The investment environment is drastically changed from what we became accustomed to in the modern post-WW2 era. The post-WW2 global order is breaking down and between now and when a new one will emerge if it will at all, things will be volatile for investors. I may not have all the answers to how one should approach things within the current context, but I do believe that some of the basic strategic changes I made to my approach will go a long way in reducing risk and improving the overall performance of my portfolio in the long term.

For further details see:

Chile's Lithium Nationalization Decision Validates My Risk-Averse Investment Strategy Approach