CAAS - China Automotive Systems: Invest In This Chinese Stock For Long-Term Gains

2023-04-11 03:35:41 ET

Summary

- China Automotive Systems recently announced Q4 FY22 and FY22 results.

- Despite several challenges, their top and bottom line grew in FY22, which is a positive sign.

- They are undervalued compared to industry standards and have great growth potential.

- I believe it can provide significant returns in the long run; hence I assign a buy rating on CAAS.

China Automotive Systems ( CAAS ) sells automotive systems globally. They provide automotive motors, polymer materials, sensor modules, hydraulic power steering systems, and integral power steering gears. CAAS recently announced its Q4 FY22 and FY22 results. In this report, I will discuss its growth potential and analyze its financial performance. I believe they are undervalued and have excellent growth potential. Hence, I assign a buy rating on CAAS.

Financial Analysis

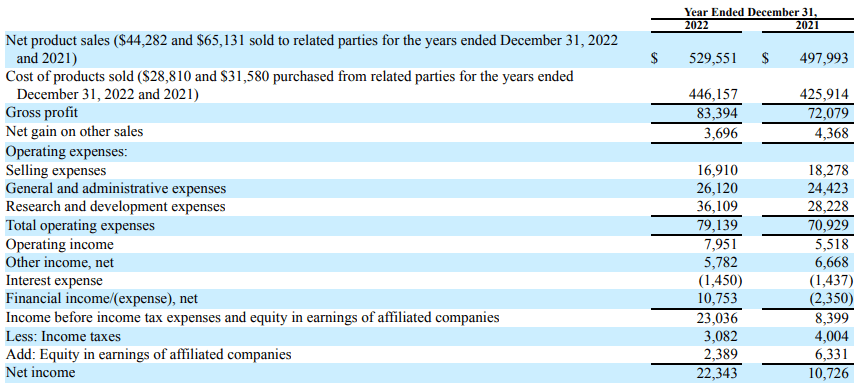

CAAS recently posted its Q4 FY22 and FY22 results . The net sales for FY22 were $529.6 million, a rise of 6.3% compared to FY21. I believe the main reasons behind the rise were:

Higher demand for passenger vehicles in China.

Increased sales of electric power steering.

Increased sales to Cherry Automobile.

The sales of electric power steering were up by 35.6% in FY22 compared to FY21, and their sales to cherry automobiles were up by 54.5% in FY22 compared to FY21. The gross profit margin for FY22 was 15.7% which was 14.4% in FY21. I believe the main reason behind the rise was a change in the product mix. The net income for FY22 was $22.3 million, a rise of 108.3% compared to FY21. I believe the main reason behind the increase was a rise in foreign exchange gains in FY22. Due to the rise in foreign exchange gains, they reported a net financial income of $10.7 million, which increased their net income.

{kind=link}

The net sales for Q4 FY22 were $128.8 million, a decline of 7.2% compared to Q4 FY21. I believe the main reason behind the decline was lower demand for commercial vehicles and passenger automobiles. But I think in the coming quarters we might see a rise in the demand for passenger automobiles and commercial vehicles, the reason I will discuss later in the report, so the net sales in the coming quarters might increase. The gross profit margin for Q4 FY22 was 19.4% which was 14.2% in Q4 FY21. I believe the gross profit margin increased due to a change in product mix. Despite a decline in net sales in Q4 FY22, I believe the financial performance of CAAS in FY22 was excellent. The decline in net sales in Q4 FY22 doesn't bother me much because I believe that they might perform well in FY23. Reasons for it I will discuss this later in the report.

Technical Analysis

{kind=link}

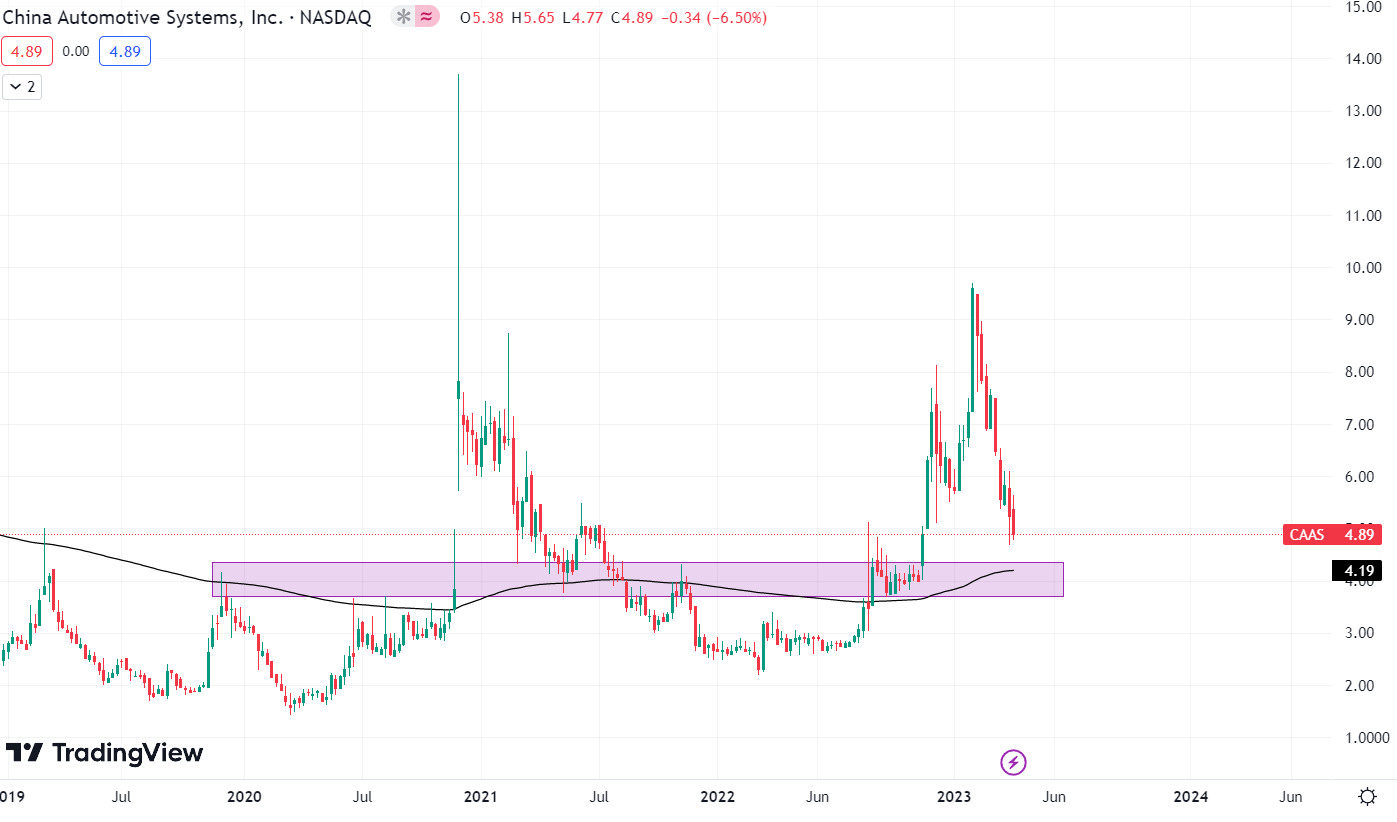

CAAS is trading at the level of $4.8. It is currently above its 200 ema, which indicates that it is in an uptrend. Since January 2023, it has corrected more than 50%, which can be a great investment opportunity. It is approaching the support level and 200 ema at $4.2. In my opinion, one can enter the stock once it reaches the support level because it has the potential to reach $8 from the current levels. Last time it broke the $4 level, it reached around $9.5, showing that buyers are active around the support level.

Should One Invest In CAAS?

{kind=link}

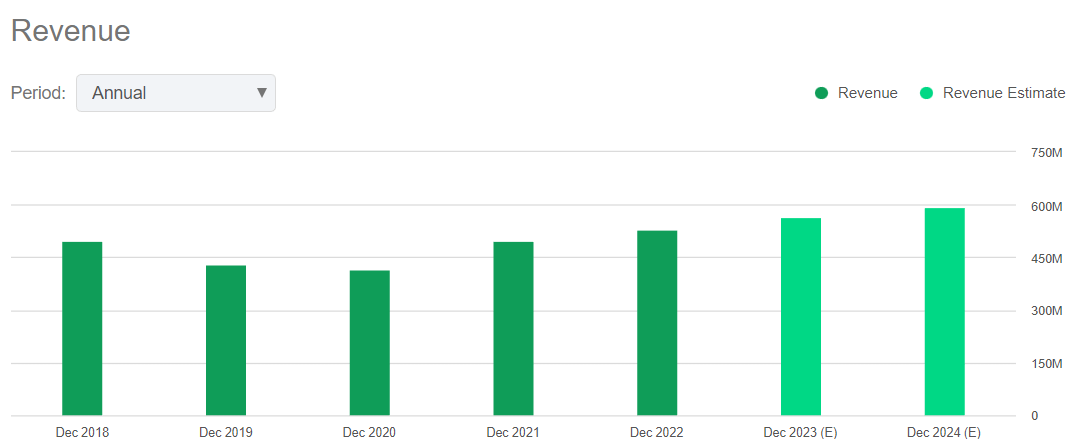

I am very impressed by the financial performance of CAAS in FY22. Despite several headwinds, their top and bottom line grew in FY22 compared to FY21. Covid-19 severely impacted China's economy and the company's business operations in 2022. The covid-19 worsened in the first half of 2022 in China, due to which several cities in China were in lockdown, their sales in China were adversely affected, and China's GDP growth in 2022 was 3% which was 8.4% in 2021. Covid 19 eased in the second half of 2022, but the damage was already done. In addition, they faced supply chain issues and critical computer chip shortages in 2022, which affected their automobile production. Despite all these unfavorable conditions, they posted decent annual results, which impressed me. The revenue estimate for FY23 is around $566.7 million, which is 7% higher than FY22 revenue. I believe they might achieve the revenue targets because the covid situation is now under control in China, and the supply chain issues are easing, which will help the company boost automobile production. The difficulties they experienced in 2022 will most likely not occur in 2023, which could boost their financial performance. In addition, several economists estimate that China's GDP growth in 2023 will be around the range of 5.5%-5.8%, which is a positive sign. There are several positive indicators that could boost their revenue growth in FY23, and I believe CAAS might be a solid investment option for the long term.

Now looking at its valuation. I will use EV / Sales and P/E ratios to judge its valuation. The EV / Sales ratio is calculated by dividing enterprise value by the annual sales, and the P/E ratio of a firm is calculated by dividing a firm's stock price by EPS. CAAS has an EV / Sales (fwd) ratio of 0.13x compared to the sector ratio of 1.08x. CAAS has a P/E (fwd) ratio of 10.19x compared to the sector ratio of 13.70x. After looking at both ratios, I believe they are undervalued. Looking at the company's growth, financial performance, and discounted stock price, I think they're undervalued and can provide significant returns in the long run.

Risk

The Chinese government periodically implements various policies to manage the PRC's economic growth pace. Some of these actions might harm the Company in the short or long run. For example, the Chinese government recently tightened its monetary policy and established a floating exchange rate policy to address excessive inflation and economic imbalances. The Chinese government has also implemented several social initiatives and anti-inflationary measures to lessen the effects of imbalanced growth and social unrest. These have raised expenses for the manufacturing and financial sectors without reducing the effects of excessive inflation and economic imbalances. Even if correctly implemented, the Chinese government's macroeconomic policies could considerably slow down China's economy or lead to severe social upheaval, which would harm the Company's operations and profitability.

Bottom Line

In FY22, they faced several challenges which impacted their business operations. Still, their top and bottom line grew positively, which shows their potential. All the headwinds they faced in 2022 are abating, and the management has provided optimistic revenue guidance for FY23. I believe they have great growth potential and could provide significant returns in the long run. Hence, I assign a buy rating on CAAS.

For further details see:

China Automotive Systems: Invest In This Chinese Stock For Long-Term Gains