CAAS - China Automotive Systems: Struggling Despite Performing Well

2023-12-17 09:07:23 ET

Summary

- China Automotive Systems has been performing quite well in tough market conditions, and its balance sheet looks safe.

- It is doing well in Brazil, and I believe it might see solid growth in North America in the coming times.

- Despite all the positives, I think fear is stopping its share price from going up.

- I assign a hold rating on CAAS stock.

I last wrote on China Automotive Systems ( CAAS ) in April. I had a bullish view of it then. But the thesis didn’t go how I thought it would, and the stock price has been down around 32% since then. I am now changing my buy rating to a hold, and I will discuss the reasons in this report.

Financial Analysis

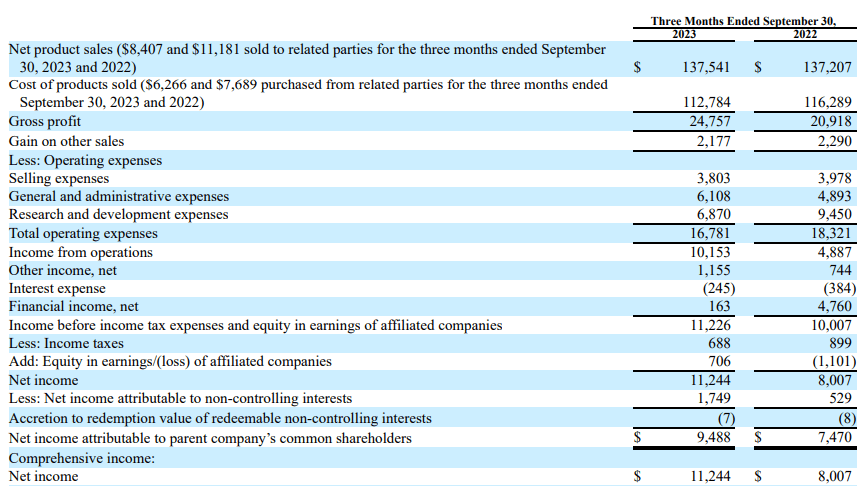

It announced its Q3 FY23 results . The net sales for Q3 FY23 were $137.5 million, a slight increase of 0.2% compared to Q3 FY22. The major reason behind the increase was the strong demand for its electric power steering [EPS] products and steering columns. The EPS sales grew by 2% in Q3 FY23 compared to Q3 FY22. The company performed well in Brazil. Its sales in Brazil grew by 15.7% in Q3 FY23 compared to Q3 FY22. The major reason behind the growth in Brazil was higher sales to Fiat. Its gross margin in Q3 FY23 was 18%, which was 15.2% in Q3 FY22. The increase in margins was due to a decline in unit cost and a change in product mix.

{kind=link}

The net income for Q3 FY23 was $11.2 million, a rise of 40.4% compared to Q3 FY22. The increase was mainly due to lower R&D expenses. Its R&D expense was higher in Q3 FY22 due to the development of its ERCB and IRC products. The increased profitability and margins were positive, and although the revenue growth was stagnant, I believe its revenue growth might be positive in the coming quarters. The reason for the stagnant revenue growth was lower sales in North America. The U.S. economy struggled in the first nine months of 2023. The GDP growth was sluggish, interest rates were quite high, and high inflation affected the U.S. economy, which affected the auto industry. Due to this, the demand in the U.S. was low, which affected the company’s sales. However, there are signs of recovery, which can be a positive for CAAS, and we might see a boost in its sales in the coming quarters. The latest data shows the GDP growth of the U.S. stands at 5.2%, which is higher than many experts predicted, and the easing in inflation has led to a stop in the interest rate hike. These factors are positive for the auto industry, which will benefit CAAS in the coming quarters. Hence, I believe that despite the sluggish growth CAAS is experiencing in North America right now, they might soon see rapid growth. In addition, if we look at its performance in the first nine months of 2023, its sales are higher in these tough times compared to 2022. Its sales in 2023 are 5.1% higher compared to 2022, and its income has also increased significantly. So, by numbers considering the market conditions, CAAS has been performing quite well. Additionally, its balance sheet looks quite safe. It has $108.2 million in cash and just $38.5 million in total debt.

Technical Analysis

{kind=link}

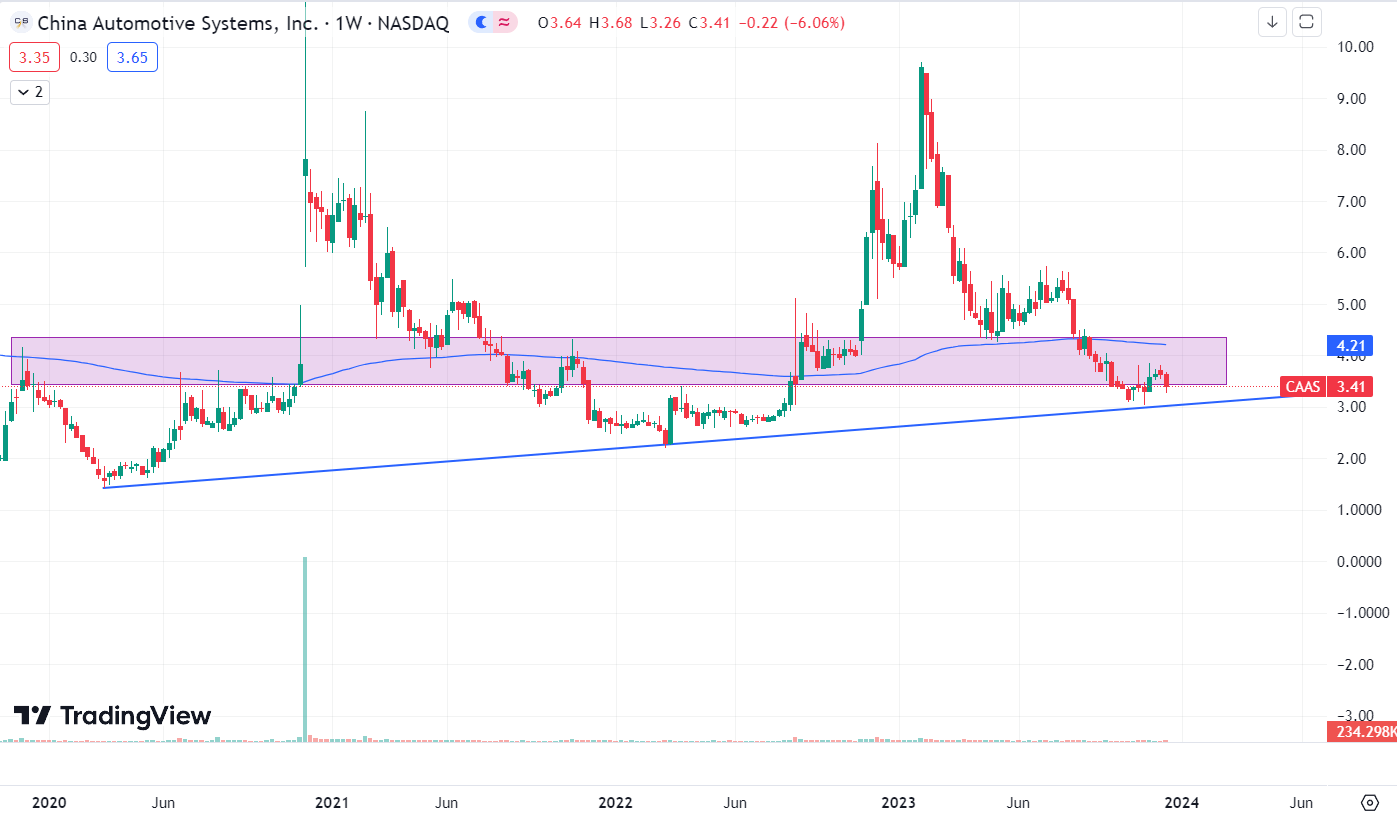

It is trading at $3.4. The chart clearly shows that it is in a downtrend. The share price also broke its 200 ema in August, which shows weakness. However, despite these weaknesses, I see some positives in this price chart. The stock price has reached the support zone of $3.4, which has strongly supported the stock for the last two years. Recently, the stock price gave a breakdown below the $3.4 level, but soon after breaking the level, the stock price rebounded quickly, showing the support zone's significance. In addition, the stock has taken support from the trendline, which it has been following since 2020. So, I believe the downside risk from here is minimal.

Should One Invest In CAAS?

We looked at the financial results. Its financial performance was decent, and my future outlook is positive. I expect them to perform even better in the coming times, and its balance sheet looks safe. But the question remains: even after performing well financially in tough times, why has the stock price been on a downtrend for so long? The simple answer is fear. The majority of CAAS operations are based in China, which I believe is the main problem. The Chinese economy is not doing quite well, and there is a constant fear of sanctions due to uncertainty in the relations between the U.S. and the Chinese government. I don’t see any other reason why CAAS is trading at such a low price; its valuation looks dirt cheap, financially and fundamentally, it looks good, and the future outlook is also positive. Hence, I believe fear is what restricts its share price to go up. CAAS is trading at a P/E [FWD] ratio of 3.42x, which is way lower than the sector median of 17.96x. Hence, despite of all the positives, I am changing my buy rating to a hold.

Risk

The Company's operations are extremely cyclical and depend on its clients' production and sales of automobiles. These factors include consumer spending and preferences, the price and availability of gasoline, and overall economic conditions. Regulatory restrictions, labor relations concerns, and other variables may also have an impact on them. The cost of cars has usually decreased in China during the past two years. Furthermore, there have been variations in China's automotive manufacturing volume year over year, which has led to variations in the demand for the Company's products. As a result, any appreciable downturn in the economy may cause consumers and manufacturers of automobiles to reduce their output and sales, which could have a materially negative impact on its operational performance. Car prices are known to decline, which would also affect the selling price of automotive parts, cutting both profits and revenues.

Bottom Line

In my opinion, CAAS is a solid company that is performing well financially in tough times, and the future outlook for CAAS is positive. It might perform even better in the coming quarters, and its valuation looks dirt cheap. However, despite all the positives, institutions and big investors are afraid to invest in it. Rather than investing in the company, people are betting on the relations between the U.S. and Chinese governments. So, this is the reason I am changing my buy rating to a hold. However, those who like to take risks and think that the Chinese government won't be an obstacle for the company, in the long run, can buy CAAS as I think it is trading at a low valuation, is financially sound, and is in a great accumulation zone.

For further details see:

China Automotive Systems: Struggling Despite Performing Well