CICHF - China Construction Bank: Unfairly Penalized

2023-04-18 16:11:17 ET

Summary

- State-owned CCB continues to be priced at a steep book value discount.

- While Q4 results were mixed, the asset quality and strong capital position remain intact, supporting the high-single-digits percentage yield.

- With the China reopening tailwind gaining traction and the latest set of SOE reforms also set to benefit the bank, the stock isn’t short of re-rating catalysts.

'CCB' or China Construction Bank ( CICHY ), one of China's 'big four' state-owned banks, didn't deliver a particularly strong set of results for the fourth quarter, with revenues and net interest margin ((NIM)) trends missing expectations across the board. Where CCB continues to excel, however, is its asset quality (NPL coverage) and capital position (CET1 ratio), which remain among the strongest in the Chinese banking space. The structural balance sheet advantage is compelling as well - CCB has access to stable funding via a 'sticky' deposits franchise and, like the other state-owned banks, benefits from strong relationships with non-financial state-owned enterprises (SOEs) in China. While SOE banks like CCB aren't the most capital efficient, they are the most resilient and, thus, offer investors a reliable dividend stream through the cycles (currently at an ~8% yield). In a risk-off environment for global banks following the failures in the US/Europe, out-of-favor Chinese banks stand to benefit. With CCB still largely under-owned and trading at a deep discount to book (vs. low teens percentage ROE generation in 2022), the stock looks poised for a re-rating.

Better Opex Cushions the NIM Blow in Q4

CCB ended the year on a disappointing note, with Q4 NIM contracting sequentially to 1.9% on an unfavorable deposit mix shift (i.e., higher time deposit contribution at ~51% of total deposits). This more than offset higher asset yields on the back of a rebalancing of new loan allocations toward higher-yielding personal loans. Fee income also came in weaker YoY on broad-based weakness across bank card and advisory, as well as settlement and clearing fees. Compounding the poor NIM result was a negative non-interest income contribution from trading losses (vs. a trading gain in the prior quarter) amid below-par bond market performance for the quarter.

{kind=link}

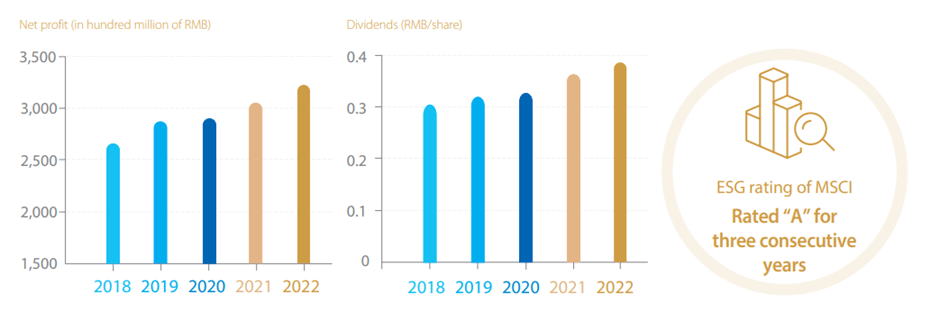

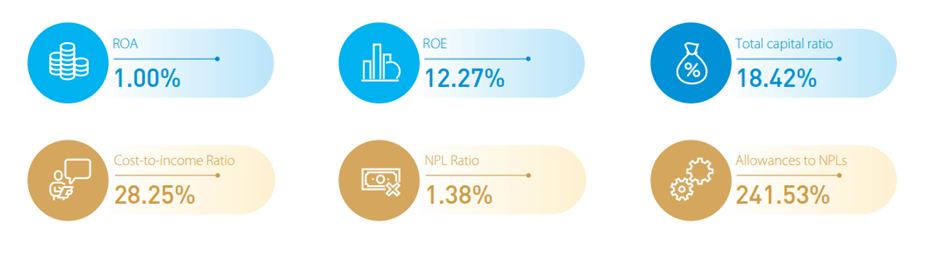

In contrast, operating expenses came in stronger than expected at +1% YoY for the full year. Despite staff costs growth running in the high-single-digits percentage, a mid-single-digits percentage decline in 'other operating expenses' due to cost efficiencies allowed for lower overall costs. While net profit was higher as well, the headline figure did benefit from lower depreciation charges and a deferral of tech-related investments to the later years. Still, ROE closed out the year at a strong ~11% for Q4, and the >30% payout ratio (flat YoY) ensures ample financial flexibility.

Capital Position Remains Best-in-Class

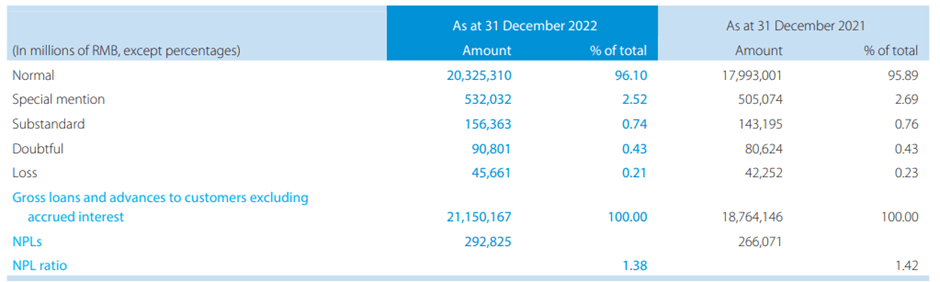

Where CCB really shines is its pristine asset quality and strong capital ratios. The NPL ratio, for instance, was down sequentially to 1.4% as at end-2022, with the coverage levels also strong at 241.5%. Similarly, the bank's special mention loans (or the 'SML') balance also benefited from improved corporate asset quality ratios, particularly in the manufacturing, mining, and utility sectors. Unsurprisingly, NPLs in real estate and construction remain high, though the fiscal support outlined at this year's NPC should boost these sectors in the coming months. Retail NPLs were also up, mainly due to mortgages, though with leading segments like personal/credit card NPLs now largely flat, CCB could be on track for near-term asset quality tailwinds here as well.

{kind=link}

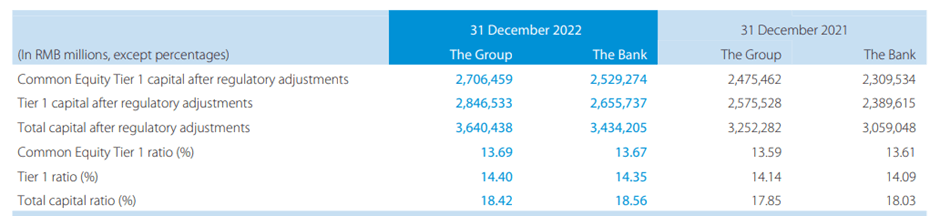

Perhaps most importantly, given the backdrop of bank failures in the US/EU, CCB's tier-1 capital ratio remained robust at ~14% in 2022. The headline result was particularly impressive in the context of headwinds from increased risk-weighted asset (RWA) density relative to the other Chinese banks. A key reason for CCB's resilient capital position is its ties with non-financial SOEs as a state bank, which allows for better asset quality. CCB management also deserves credit for diversifying its underlying loan exposures across sectors, keeping volatility low through the cycles.

{kind=link}

Latest SOE Reforms to Benefit CCB

The full-year results came on the heels of positive SOE reform announcements emphasizing increased efficiency and innovation while also balancing national security needs. Of note, the SOEs will be tied to additional performance targets for 2023, spanning earnings quality, ROE, and cash flow conversion (i.e., operating cash flow to revenue ratio). With the latest regulatory reform driving centralized financial oversight as well, expect highly-regulated SOE banks like CCB to benefit as shadow banking and other marginal institutions operating within the regulatory 'grey area' are reduced. With CCB already on track to generate best-in-class ROEs and an upturn in profitability post-reopening, I wouldn't be surprised to see a reform-driven re-rating of the stock. In the meantime, CCB shareholders get paid a well-covered ~8% dividend yield to wait.

{kind=link}

Unfairly Penalized

Following a poor 2021/2022, CCB has seen its stock come back into favor this year amid renewed optimism about the post-COVID reopening and SOE reforms. As the Q4 report showed, however, a P&L inflection hasn't quite materialized, with revenues and NIMs falling short of consensus estimates. Yet, CCB maintains one of the strongest capital positions among its banking peers, along with a stable funding source (via a highly 'sticky' deposits franchise). With ROEs proving resilient through the ongoing rate cut cycle in China and NPLs also well-covered, CCB screens very attractively at the current ~8% dividend yield. And amid the banking sector pressures in the West, major Chinese banks could benefit from 'safe haven' inflows over the coming months, paving the way for a significant re-rating from the current book value discount.

For further details see:

China Construction Bank: Unfairly Penalized