CHN - China Fund: Deteriorating Chinese Economic Data Warrants Caution

2023-08-10 13:04:22 ET

Summary

- China appears to be headed for more economic troubles.

- While the China Fund is overweight the more resilient consumer/tech side, the rest of the portfolio remains levered to broader economic shifts.

- With CHN's expense ratio also at a premium to comparable active funds, the NAV discount isn't all that appealing here.

Recent headline inflation data out of China only reinforced the case for weaker economic growth. The silver lining is that a gradual consumption demand recovery appears to be materializing, albeit helped by the summer holiday season. With little evidence of a sustained rebound in mid to long-term consumption, however, all signs point to a more challenging deflationary environment and a slowdown in China's growth momentum going forward.

While the market has pinned its hopes on stimulus (monetary and fiscal), as evidenced by the rally post-Politburo meeting, balance sheet constraints, particularly at the local government level, mean large-scale fiscal stimulus won't be on the cards. And given the size of the leverage issues in property (note Chinese wealth is mostly tied up in real estate), incremental stimulus via targeted policy incentives and more rate cuts likely won't be enough to stop the knock-on economic impacts.

To be fair, the outlook is relatively more benign for the China Fund ( CHN ), given its consumer/tech overweight; yet, the rest of the portfolio remains exposed to the broader economic headwinds. Hence, even at the current high-teens NAV discount and with a performance-linked tender offer policy in place (worth up to 25% of outstanding shares), I am reversing my prior bullish stance on CHN. Instead, I would favor a more selective approach to China from here.

Fund Overview – A Pricey Active China Fund with a Big Consumer/Tech Overweight

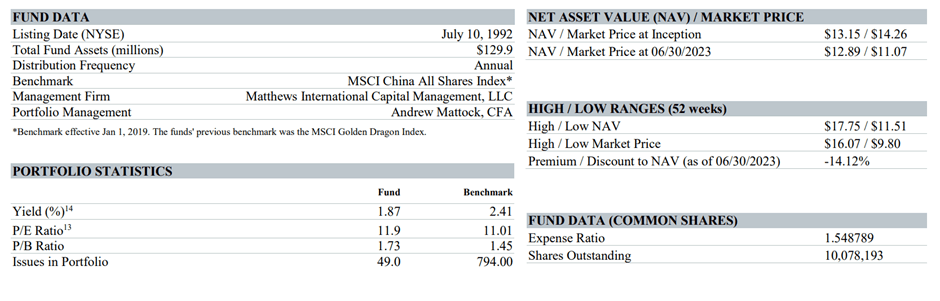

The actively managed Matthews International China Fund benchmarks itself against the MSCI China All Shares Index, a basket of large and mid-cap Chinese equities listed globally. The closed-end fund has seen its net asset base decline over the last quarter, reaching $129.9m (down from $140.4m previously) per its latest factsheet . As a result, the expense ratio is now even higher at 1.5%, above comparable CEFs like the Templeton Dragon Fund ( TDF ), and more than double most passively managed ETF offerings (typically in the 0.7-0.8% range).

{kind=link}

Matthews Asia

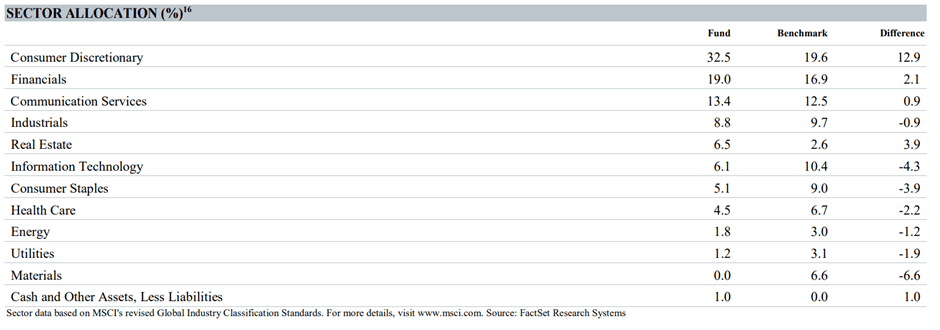

By sector, the fund continues to be heavily overweight Consumer Discretionary at 32.5% (+12.9% vs. the benchmark), followed by Real Estate (+3.9% vs. benchmark) and Financials (+2.1% vs benchmark). Following a relatively strong run this year, the Communication Services allocation is also higher at 13.4% (+0.9% vs benchmark). Sectors like Consumer Staples, Information Technology, and Utilities are some of the fund's notable underweight allocations.

{kind=link}

Matthews Asia

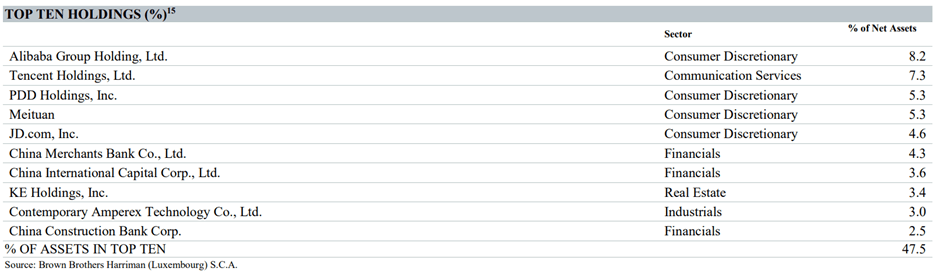

Similarly, CHN's single-stock allocation skews toward China's largest consumer/tech platforms, namely e-commerce giant Alibaba Group ( BABA ) (8.2%), Tencent ( OTCPK:TCEHY ) (7.3%), and PDD Holdings ( PDD ) at 5.3%. The largest non-consumer/tech holding remains China Merchants Bank ( OTCPK:CIHKY ) at 4.3% and China International Capital Corporation at 3.6%. While the ten largest holdings contribute a lower 47.5% of the overall portfolio, CHN remains a concentrated fund.

{kind=link}

Matthews Asia

Near-Term Fund Performance Deteriorates Following Another Tough Quarter

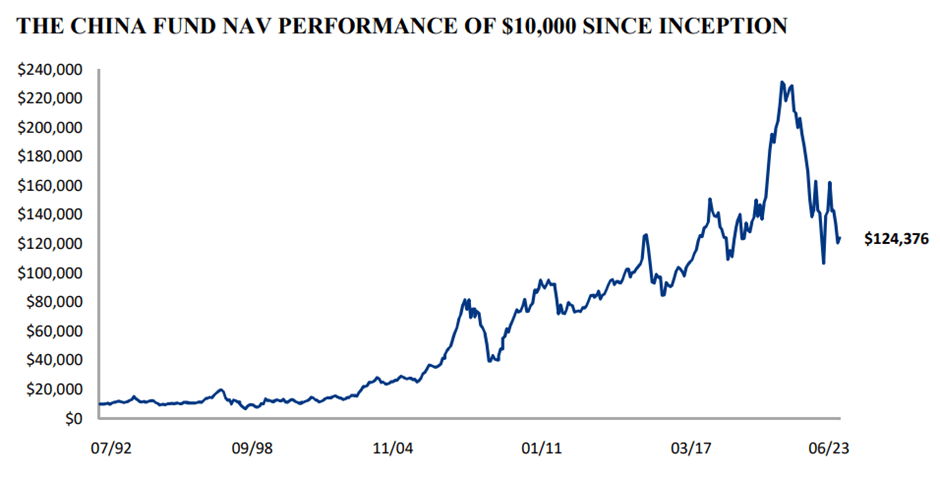

Following another challenging quarter, CHN is now down by -12.7% in NAV terms and a steeper -14.3% in market price terms (a result of the persistent NAV discount). Disappointingly, CHN looks to be headed for the third successive year of drawdowns, with 2021 and 2022 seeing -24.1% and -12.9% declines, respectively. Even relative to its benchmark MSCI China All Shares Index, the fund has underperformed by a considerable margin across one and three-year timelines. The track record over longer timelines remains strong, however - since its 1992 inception, CHN has compounded at a +8.6% pace (+7.8% in market price terms).

{kind=link}

Matthews Asia

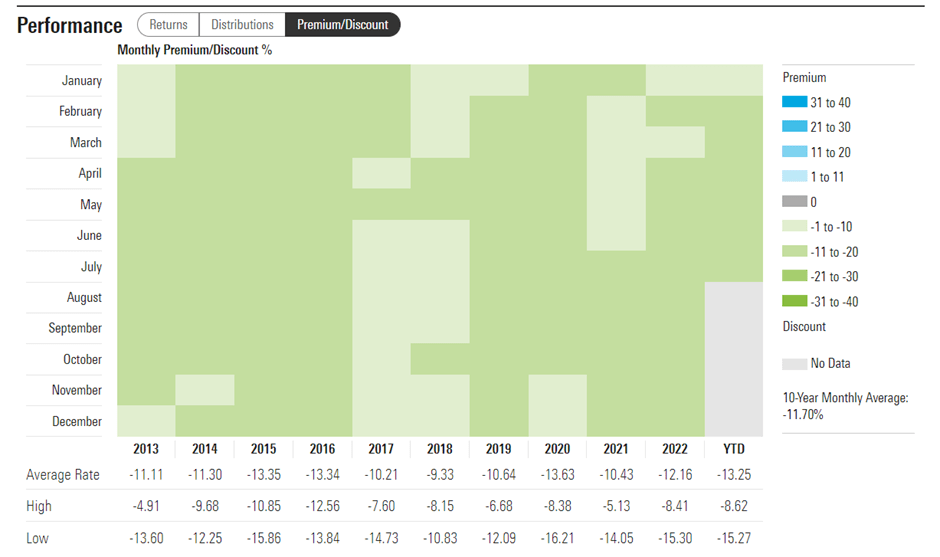

In the meantime, the fund's NAV discount remains wide in the high-teens. Following prolonged underperformance in recent years, investor sentiment has likely played a part, along with lower distributions last year. In response, the Matthews team announced a performance-linked tender offer in January worth up to 25% of outstanding shares. Pending improved performance (absolute and relative) and more active distributions, though, I suspect the CHN discount to NAV won't be closing anytime soon.

{kind=link}

Morningstar

Puts and Takes from Another Deflationary China Print

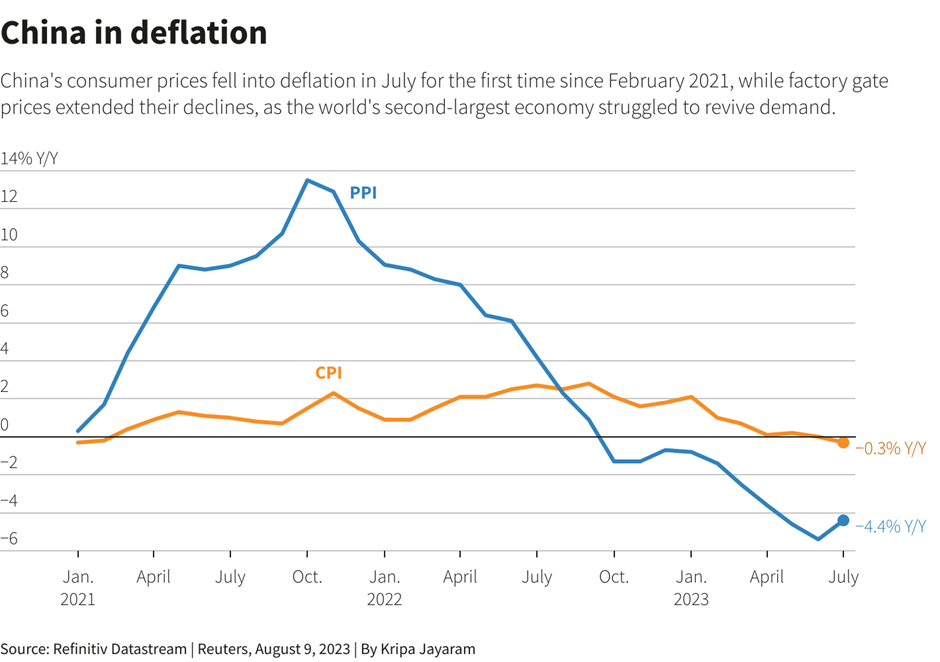

Headline consumer inflation out of China was predictably poor at -0.3% YoY (down from flat YoY in June), marking the first negative YoY reading in two years. Some context is needed, though - the YoY decline was influenced by an unfavorable base effect due to elevated food prices last year. And on a sequential basis, the disinflationary pressures are easing, at least on the consumer side, at -0.2% MoM. Breaking out the non-food components also tells a different story, as non-food inflation was higher YoY, partly on rising oil prices but also on a tourism-related boost from the summer months. The latter will give investors hope that China's pent-up demand theme is gradually playing out post-COVID, though it remains too early to underwrite a meaningful consumption bounce, in my view. On the producer side, there aren't a lot of silver linings, with PPI remaining in deflation at -4.4% YoY; alongside the series of contractionary manufacturing PMI prints in recent months, the outlook on China's non-services economy screens unfavorably.

{kind=link}

Reuters

Looking ahead, the seasonal demand boost from the summer months should continue to support services inflation, while supply-side headwinds (e.g., flooding in North China and El Nino in South/South-East Asia) also pose upside to CPI inflation. Beyond the summer holiday season, however, it remains unclear if consumption growth will sustain, particularly with real estate (a key source of wealth for the Chinese) under pressure and youth unemployment reportedly as high as ~47%. Alongside the weakening momentum in domestic and external manufacturing, all signs point to slowing growth (even vs. the conservative +5% target this year) and potentially more demand-driven deflation ahead. Either way, the underlying price trend appears to be firmly skewed toward deflation, supporting the case for more monetary policy easing by the PBoC (likely via a RRR cut).

Deteriorating Chinese Economic Data Warrants Caution

While better than consensus expectations, China's downbeat producer and consumer inflation data releases this week confirmed a concerning deflationary trend. Beyond the lower YoY commodity prices, domestic demand weakness is key here, and as the summer holiday tailwind fades, China could be set for more declines. In combination with the negative data elsewhere (e.g., contractionary PMIs), the case for more stimulus is clear, with the PBoC likely to kick off more monetary easing in the coming weeks. The fiscal side is an issue, though, given the scale of the leverage issues across Chinese government agencies and property developers. There isn't an easy fix either to structural issues like the elevated youth unemployment rate and unfavorable demographic shifts.

On the one hand, I continue to like the China Fund's skew toward relatively resilient areas like consumer/tech. Yet, the rest of the portfolio remains levered to economically-sensitive sectors like financials, industrials, and real estate, leaving CHN exposed to further downside. Having modestly re-rated on stimulus hopes post-Politburo meeting, I would take some profits here – even with the fund still priced at a wide NAV discount.

For further details see:

China Fund: Deteriorating Chinese Economic Data Warrants Caution