CIHHF - China Merchants Bank: The Recovery Is Taking Shape

2023-04-20 07:10:25 ET

Summary

- China Merchants Bank has weathered the rate cut headwinds well over the last few months.

- As the focus turns to 'quality' growth and enhancing the ROE profile, CMB likely has more room for upside.

- With the charges against its ex-president also finalized, the stock is poised for a re-rating back to its historical book value premium.

‘CMB’ or China Merchants Bank’s ( OTCPK:CIHKY ) status as the best-in-class retail banking franchise in China has taken a hit following the year-long investigation into its former president, Tian Huiyu, over suspected bribery and insider trading violations. Now that the official charges are out, however, it seems clear that any regulatory risks are limited to Mr. Tian in his personal capacity while the firm remains in the clear. From here, the focus should turn back to CMB’s retail-driven fundamentals, which look poised to improve alongside the reopening. With the stock’s premium to China’s ‘big four’ state-owned banks also narrowing despite maintaining an RoE premium in 2022, CMB has ample room to re-rate from the current ~1x P/Book (a discount to the historical ~1.5x P/Book valuation). And with China’s retail sales already accelerating to ~11% in March, expect more earnings upside heading into Q1/Q2.

Better Fundamental Outlook; Strategic Focus Shifts to 'Quality' Growth

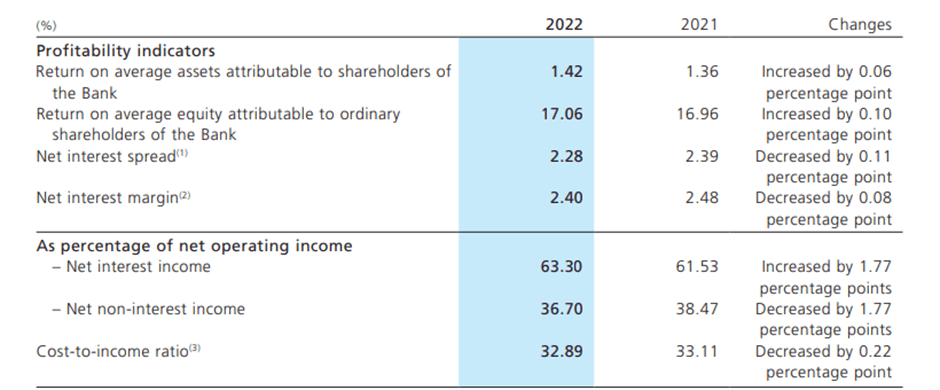

While the rest of the economy will see twin benefits from the reopening tailwind and monetary easing this year, the banking sector faces a different challenge in limiting net interest margin ((NIM)) pressures from an aggressive rate cut cycle. But a stronger economy provides an offset in the form of loan growth, while fiscal support for troubled sectors like property should also mitigate asset quality concerns. Also key will be the extent to which CMB can deliver on a non-interest income recovery; if all the pieces fall into place, the bank should be on track for a mid-teens % YoY bottom line growth. Management also has leeway on areas like provision accumulation, while the accelerating pace of online and overseas consumption (note CMB is the overseas credit card leader in China) bodes well for profit upside in 2023 as well.

{kind=link}

China Merchants Bank

That said, the tone of management’s annual report commentary indicates a focus on ROE expansion over growth. In particular, the dual strategic focus on optimizing the higher-risk, more capital-intensive business for “quality” while pushing for growth in the capital-light, lower-risk business lines hints at the tradeoff CMB is making in light of policymakers’ emphasis on national/social service over corporate profits at this year’s NPC meeting . Given the risk of lending models being standardized across Chinese banks post-reform, expect a greater commitment to the wealth/asset management side, which bodes well for fee income growth and ROEs going forward.

Shareholder Return Intact Amid New Capital Rules

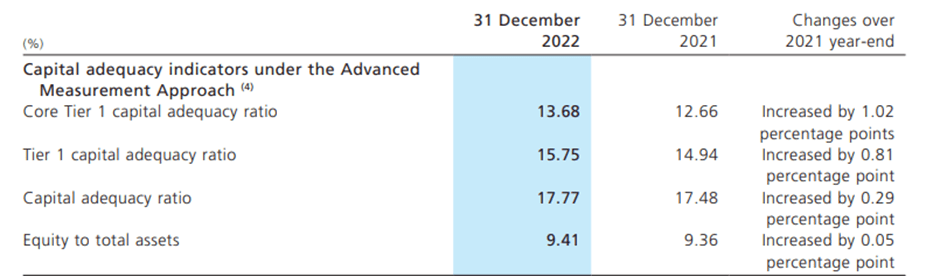

There will be some impact from adopting China’s new commercial banking capital rules , but the positives and negatives balance out. On the one hand, CMB (like the other state banks) already adopts an advanced internal rating-based approach to capital calculation, so changes to ‘loss given default’ and ‘exposure at default’ are unlikely to impact capital ratios. And given CMB’s focus on retail over riskier loan categories like property, which will incur higher capital charges, it could benefit more than its peers. Over the long term, CMB’s shift toward “quality” over growing its capital-intensive business lines fits nicely within the updated regulatory framework, so any near-term headwinds should reverse over time.

{kind=link}

China Merchants Bank

In the meantime, the bank’s strong ~14% CET1 ratio provides more than adequate buffer for the existing shareholder return policy. For context, CMB’s payout lies at the upper end of the Chinese banking universe, coming in at >30% yet again in 2022. Management’s guidance that the current level of dividend payout will be maintained further highlights that the capital return is well-covered. Investors hoping for upside to the capital return could be disappointed, though. CMB has made clear its excess capital deployment priorities are to build a sufficient earnings buffer against potential downturns and to reinvest in the core business, given the high teens % ROE generation.

{kind=link}

China Merchants Bank

Clearing the Governance Overhang

Per a statement recently published on the Chinese Procuratorate’s website (i.e., the national agency responsible for legal prosecution), former CMB president Tian Huiyu has been charged with bribery and insider trading during his time at the company. Specifically, Mr. Tian leveraged his positions at several major banks, including China Cinda ( OTCPK:CCGDF ), Bank of Shanghai, China Construction Bank ( OTCPK:CICHY ), and CMB, for bribes in return for loan approvals, among other business activities. Additionally, Mr. Tian has also been found guilty of insider trading himself and in cooperation with other individuals.

Given the investigations into Mr. Tian had been ongoing since April last year, when CMB’s stock price first de-rated, the confirmation of these charges had been a long time coming. The extent of his involvement wasn’t clear, however, nor was the bank’s potential liability until the latest publication. Given Mr. Tian’s charges are isolated to the individual, with no other current or former CMB employees involved, the latest announcement should see the overhang on CMB’s valuation eventually lifted. As the CMB risk premium fades and investor focus returns to the strong fundamentals (recall the bank sustained high-teens % RoEs in 2022), CMB has ample room to re-rate from the current ~1x P/Book in the coming months.

The Recovery is Taking Shape

CMB has suffered from a persistent valuation overhang over the last year amid an ongoing investigation against its former president on bribery and insider trading counts. With the official statement absolving the bank from any legal liabilities, though, investor sentiment on the bank should eventually improve. Even if we don't get an immediate re-rating to historical P/Book trading levels, the improving retail data in China presents an added catalyst for CMB’s retail-focused business. As the reopening continues to gain traction over the coming months, expect the narrowed premium vs. China’s major state-owned banks to widen in line with its superior high-teens % RoE. In the meantime, investors get paid a decent ~6% dividend yield to wait.

For further details see:

China Merchants Bank: The Recovery Is Taking Shape