KALL - China's Macro Indicators Suggest A Quiet Crisis

2023-08-21 18:16:18 ET

Summary

- China's real estate trends indicate that, despite strong PMI, there's a substantial affordability crisis among its masses.

- Rising joblessness among the youth in now-quashed government data indicates a burgeoning "lost generation" is in the making.

- Market performance of China instruments are largely aided by foreign investors' diversification mandates. Arguments of outsized performance are getting increasingly weaker.

As the past week closed, a number of interesting events came to pass over at the People's Republic of China. The first was China's largest private real-estate developer Country Garden missing a number of bond payments and posting guidance that it will likely post a record loss for the first six months of the year, thus evoking memories of the Evergrande Group crisis which began a little over two years ago and concluded about two days ago when the company filed for bankruptcy protection .

A number of data points for July were also released last week. Industrial output grew 3.7% on a Year-on-Year (YoY) basis, down from 4.4% in June, and missed analysts' expectations of 4.4%. Retail sales rose 2.5% YoY, was down from 3.1% in June and missed analysts' expectations of 4.5%. Overall, the setting of expectations is somewhat less significant for two reasons:

- Past performance largely determines present expectations. China has a history of producing strong growth numbers for decades and the models used forecast expectations accordingly. When metrics slip, the models would recalibrate after a number of iterations.

- Expectations also are used to validate investment targets. China has long been a many an investor's destination of choice for achieving portfolio diversification.

Regardless of expectations, the metrics trend positive. Other indicators decidedly do not trend positive and have been in decline for some time. Ironically, recent concerns over expectations not being met are helping to shed light on fundamental indicators that are far, far more fundamental and important.

Shelters Crumble

Last week, the People's Bank of China (PBOC) lowered its one-year loan prime rate - on which most of China's household and business loans are based - from 3.55% to 3.45%. This was the second cut in three months. However, it was confirmed this week that the five-year loan prime rate - the peg for most mortgages - was left unchanged at 4.2%. This rate was reduced in June but the PBOC is seemingly unwilling to budge on this right now.

The real estate sector should be considered a proxy of citizens' long-term wealth accrual ability. In other words, it's an indirect indicator for affordability concerns. As it turns out, this sector has been glaring red for some time now.

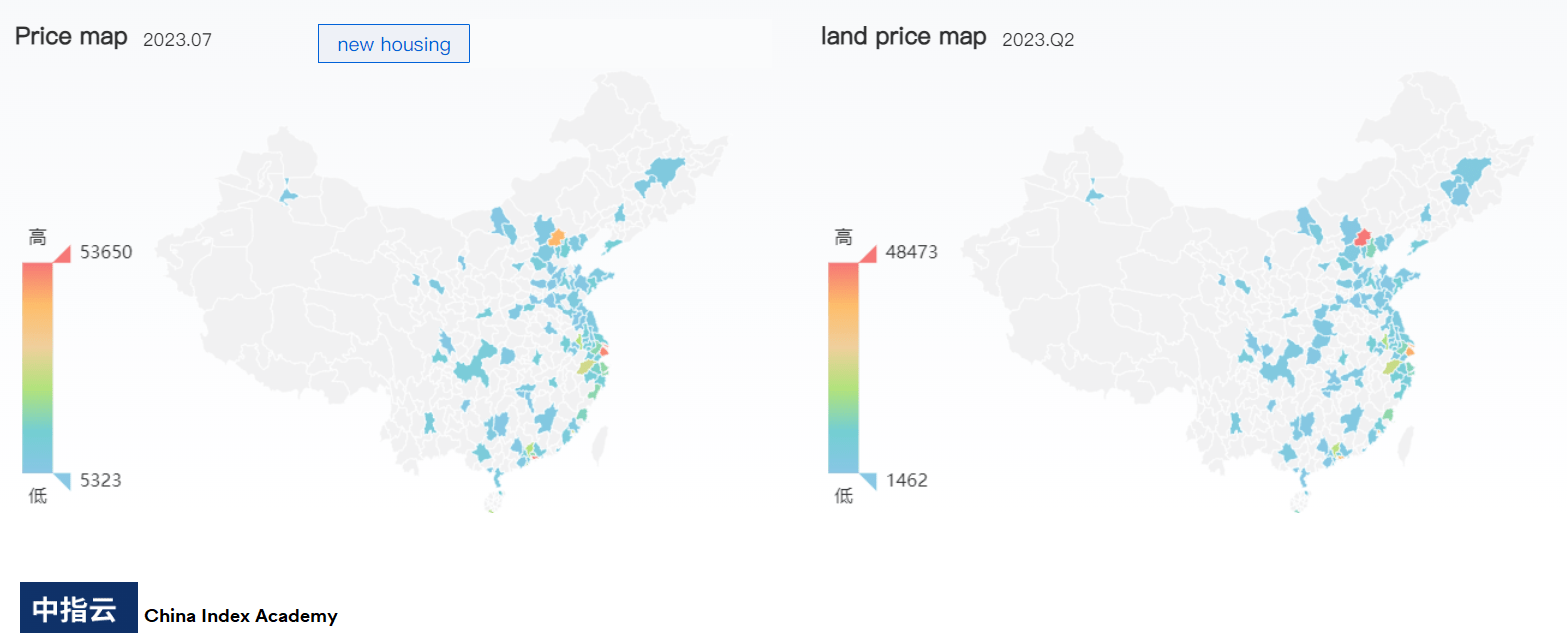

The China Index Academy, a leading Chinese real estate analytics platform (with the unfortunate acronym "CIA" but which could also be referred to by its parent company Fang Holdings or "SouFun"), reported that "new housing" (i.e. built-up properties such as apartments) as well as land prices have cooled off on a YoY basis throughout the People's Republic as of July.

Source: China Index Academy (SouFun)

{kind=link}

Note: SouFun's charts/reports aren't available in English. All text is machine-translated from Putonghua.

The only regions that principally display a weak uptrend in "new housing" prices are (in order) those surrounding Shenzhen, Shanghai and Beijing. The areas that show a principal uptrend in land prices are (in order) those surrounding Beijing, Shanghai and Shenzhen. All three cities are considered "first-tier".

SouFun also reported that the number of foreclosed properties in China rose almost 20% YoY in the first half of 2023. The dominant reason has been the inability of owners to pay mortgages due to a drop-off in incomes. These owners were both corporate entities as well as individuals.

The biggest increase in foreclosures was seen in central China, with foreclosures in Henan province and Sichuan province in the southwest witnessing a 63% and 51% surge respectively. Other significant spots were Guangdong, Jiangsu and Chongqing provinces. Even some large homes in "first-tier" Shenzhen were foreclosed on for a staggering average value of CNY114 million ($15.6 million).

The highest number of homes changing hands during auction proceedings were in the economically-active Yangtze River and Pearl River Deltas whereas western regions such as Qinghai and Ningxia Hui Autonomous Region saw significantly less turnover despite more properties awaiting disposal.

Chinese asset managers note that the dominant factor behind this jump in 2023 was due to the 1- to 2-year process for disposing of non-performing assets normalizing after pandemic control measures were lifted. The seeds for the foreclosures, however, were planted well before.

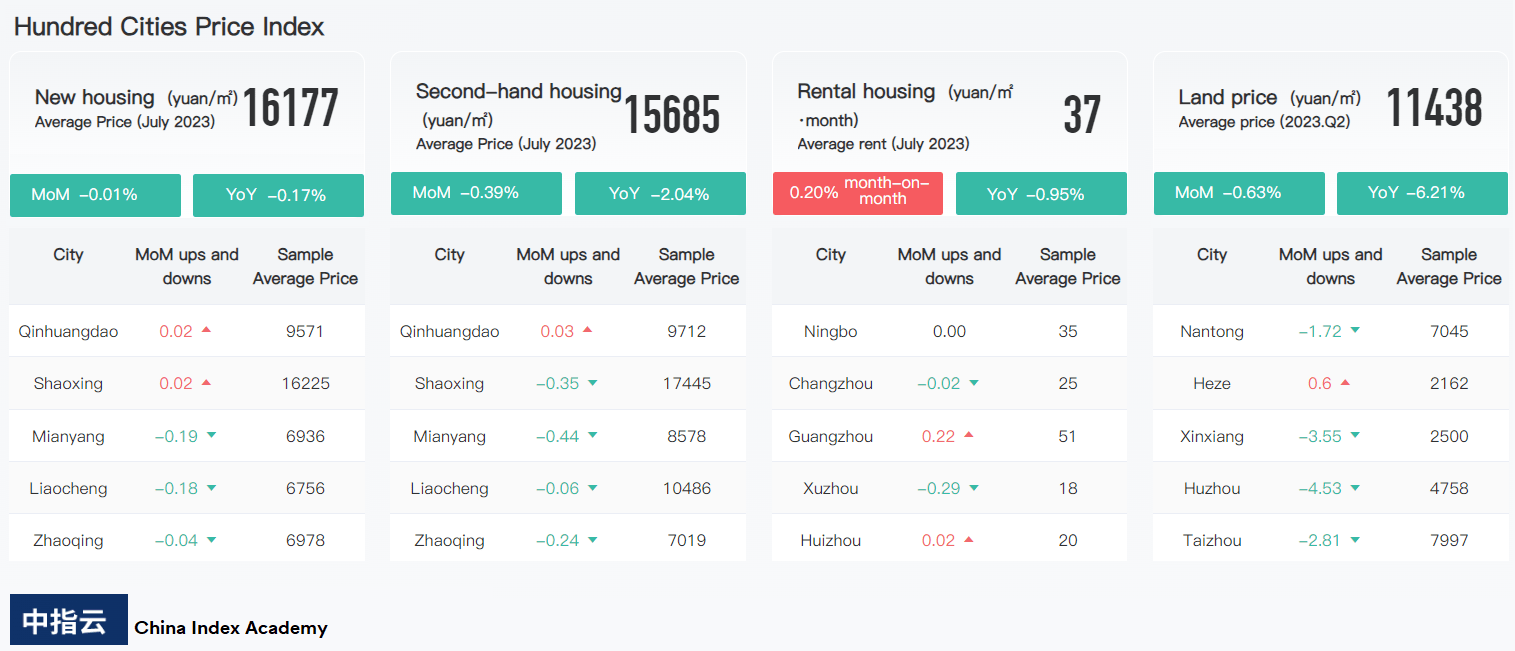

SouFun's "Hundred Cities Price Index" shows that, overall, prices for land and new housing have dropped in both YoY and Month-on-Month (MoM) terms. However, rent on average has been rising in recent months despite a YoY drop.

Source: China Index Academy (SouFun)

{kind=link}

Note: In SouFun's charts, green is negative, red is positive

As housing ownership dwindles, rent rises. Here too, the largest rent increases were evident more so in "first-tier" cities and less so in subsequent tiers.

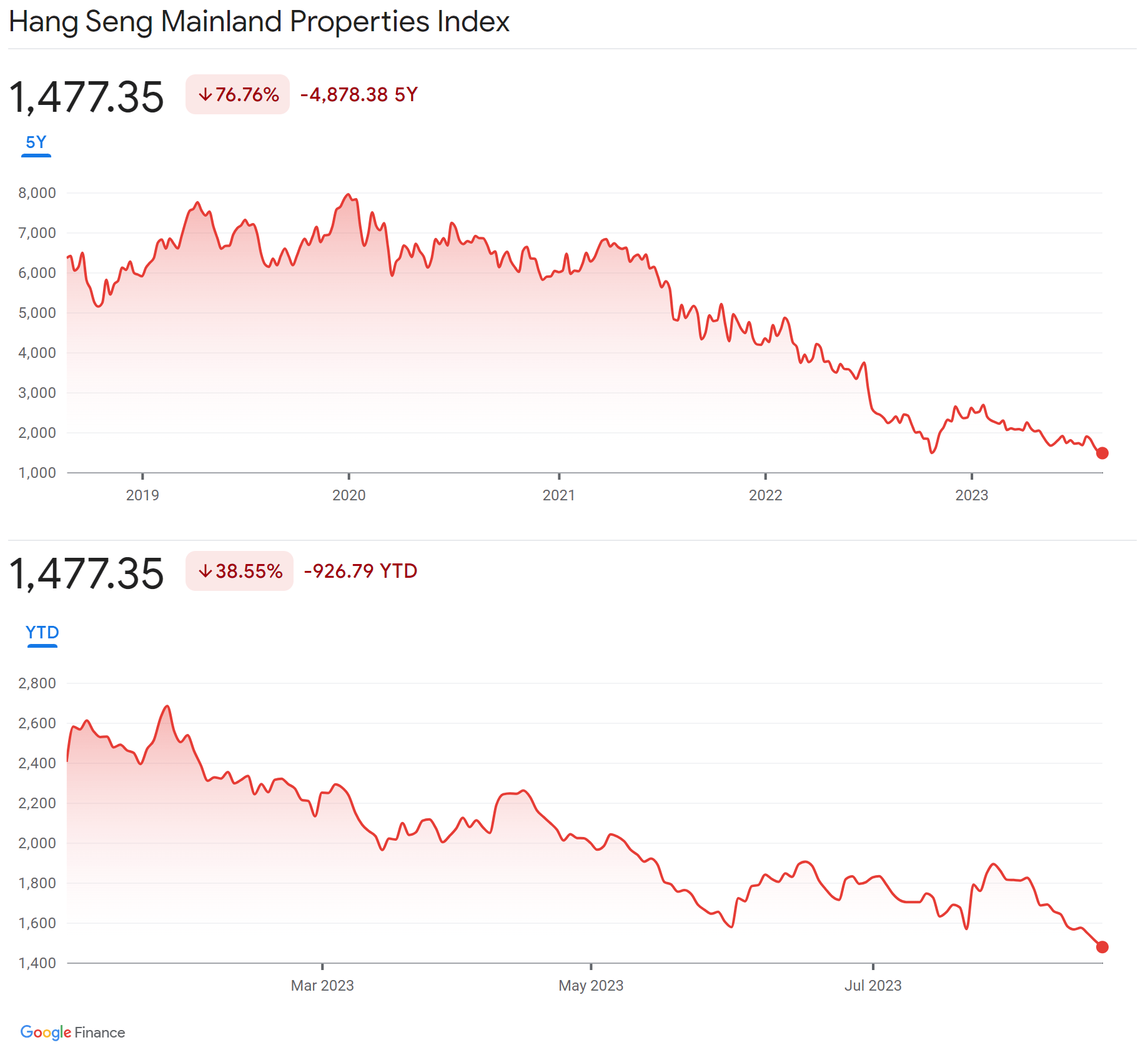

Chinese asset managers' assertions aren't far off the mark. The Hang Sang Mainland Properties Index (Hang Seng ticker: HSPMI) indicates that it has largely been downhill since the peak of January 2020. On a 5-year basis, the HSMPI is down nearly 77%.

{kind=link}

In the Year-to-Date (YTD) alone, the HSMPI has declined by nearly 39%.

While leading bank economists expected a 15 basis point cut due to default risks from festering liquidity woes in the property sector, the Politburo had made it quite clear that present trends are to be somewhat expected. In a July message that strangely caused property firms' stocks to rally , this top body of the Chinese government stated that it is necessary to "adjust and optimize policies in a timely manner". A phrase in the message that stated "housing is for living in, not speculation" was subsequently removed from the transcript.

The "vanishing phrase" should have been regarded as a warning. Instead, it was assumed that Chinese government support for the property sector is a given. The Chinese property sector had long been accorded the status of a "preferred investment asset" under the assumption that demand would always drive prices up. As a result, building activities expanded outwards from "first-tier" cities and across the People's Republic.

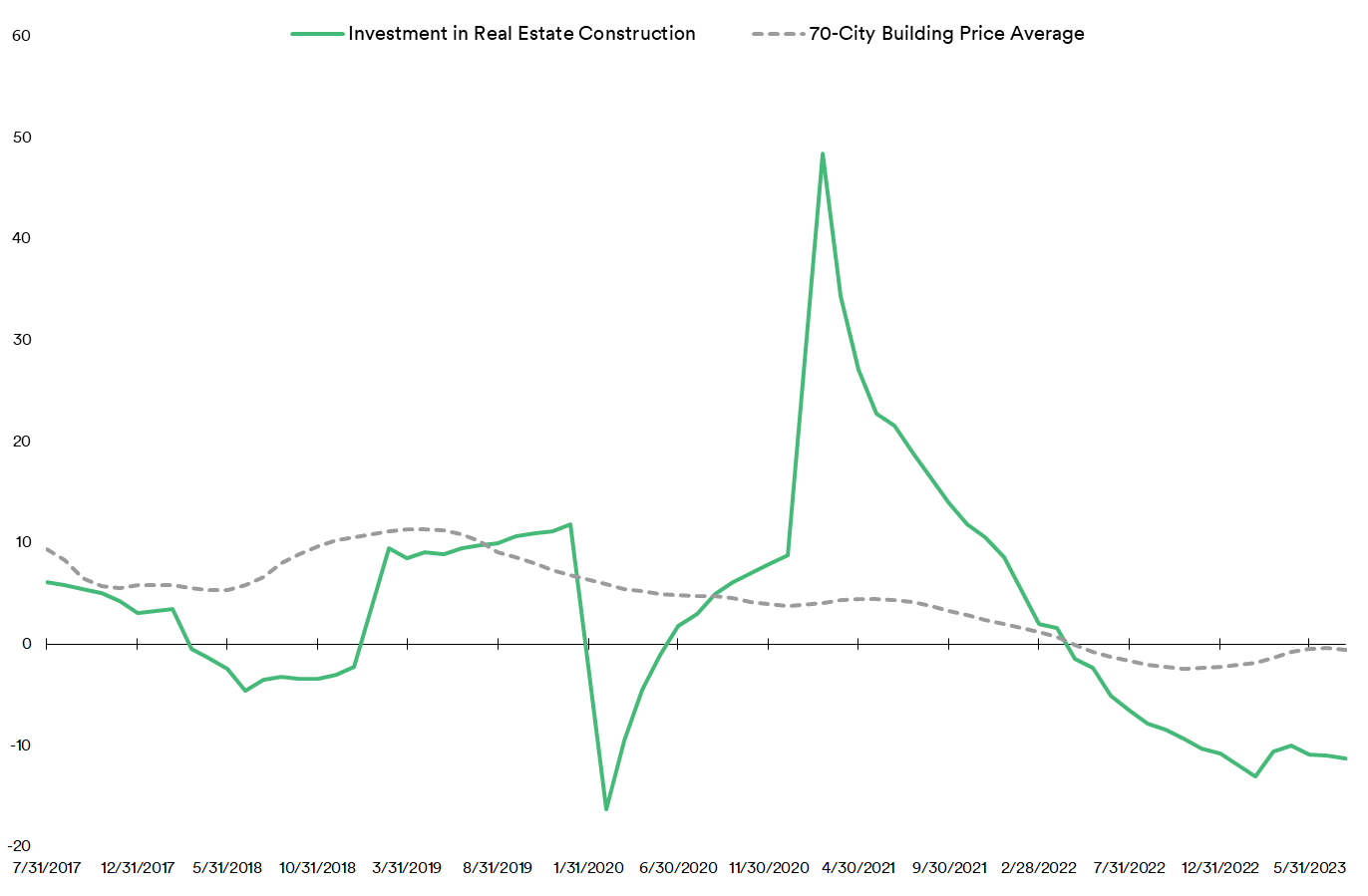

This assumption has long been found to be wanting. Let us consider a second-order trend analysis, i.e. a trend of trends, to demonstrate. An analysis of "China Property Investment in Real Estate Construction YoY" versus "China 70 Cities Newly Built Commercial and Residential Buildings Prices Average YoY" metrics over the past six years indicate how disparate this assumption is from reality.

Source: Created by Sandeep G. Rao using data from Bloomberg

{kind=link}

All through 2020 until Q1 2021, investment in construction was hoisted atop strong trends despite building prices trending downwards since Q1 2019. Investments in construction faced a sharp pullback in Q1 2021 which continues till the present day.

Ordinarily, the prospect of constricted supply should have firmed up building prices. In other words, the trends should have "crossed streams". This didn't happen. Instead, both trends have been running (largely) negative for the past one year, despite an effective moratorium on foreclosures, numerous initiatives to ease ownership of homes, etc.

Some of these measures and events might very well have provided "signals" for the stock market despite these indicators. For instance, the Shanghai Stock Exchange's Property Subindex (SHH: 000006) - comprised of the likes of publicly-listed property developers and accessible mostly to domestic investors and certain qualified international investors - showed very dramatic swings and roundabouts before finally trending in line with these indicators over the past month or so.

Source: Created by Sandeep G. Rao using data from MarketWatch

{kind=link}

The trends in property consumption is aligned with some depressive trends seen along the younger spectrum of China's citizenry.

The Beginnings of a Lost Generation

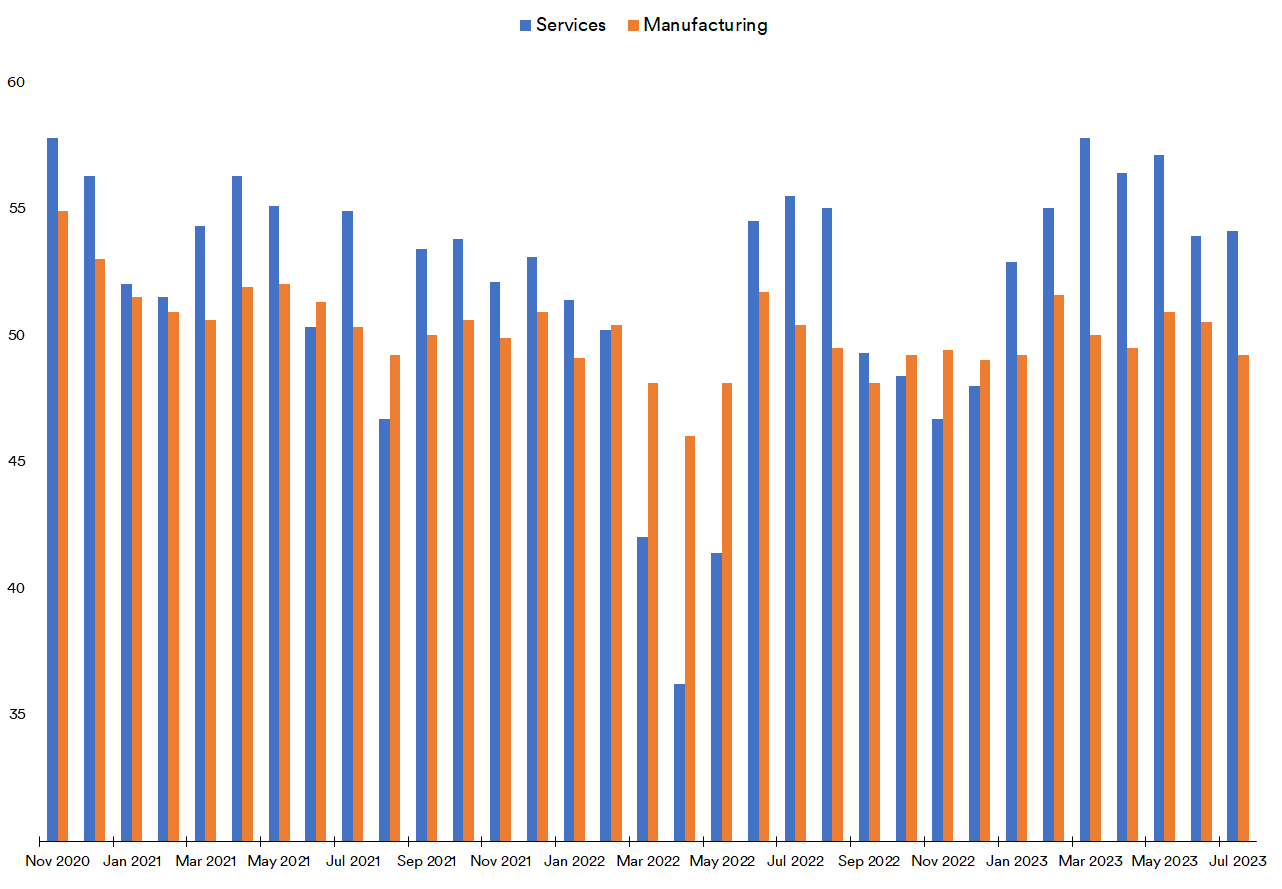

Much like the property sector, another significant pillar of China's economic engine is its massive manufacturing base effectively serving as the "crucible" for most aspects of the Western Hemisphere's consumption (and to varying degrees elsewhere). A comparison of the China Caixin Purchasing Managers Index (PMI) for both Services and Manufacturing shows that China's "foundry" effectively hasn't faltered since June of last year.

Source: Created by Sandeep G. Rao using data from Investing.com

{kind=link}

Ordinarily, this should suggest that the economy is going from strength to strength; the Chinese economic engine is indeed able to meet incoming demand for its produced goods and services from all customers adequately. However, this doesn't necessarily translate to a benefit for all demographics of its citizenry or even those who work in the "crucible".

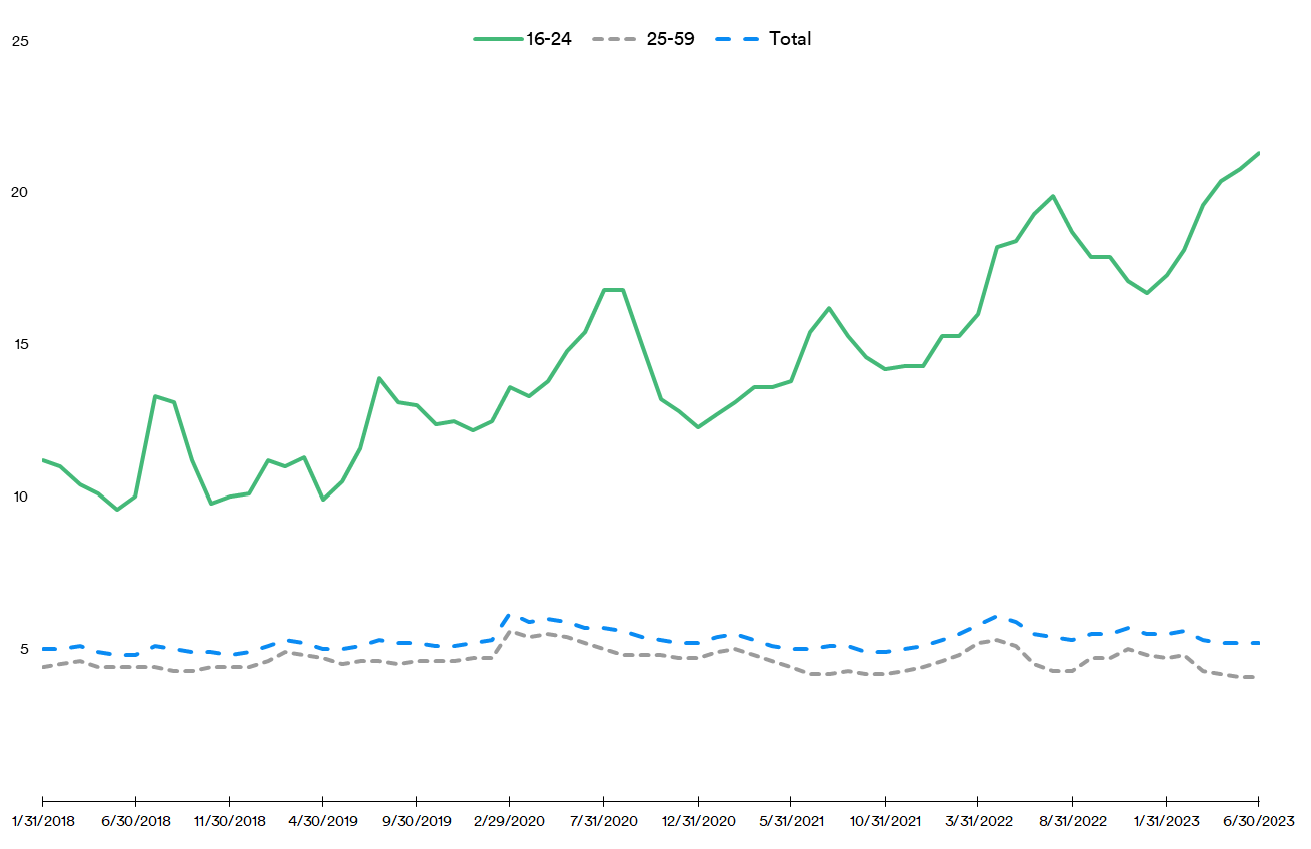

As compiled by China's state-run National Bureau of Statistics, the surveyed jobless rate across urban areas - when broken down by age and compared against the total effective rate - reveals a fascinating and concerning "hidden feature":

Source: Created by Sandeep G. Rao using data from Bloomberg

{kind=link}

The total jobless rate runs mostly parallel relative to the surveyed jobless rate in the 25-59 age range. However, for the 16-24 age range, the jobless rate has skyrocketed to 21.3% . If it were to be assumed that the 25-59 age group is the prime consumer/investor of investable assets such as property, then the trends in property consumption indicate that this group is largely unable to, despite the reported strong PMI. This is an indirect indicator of an affordability crisis.

The jobless rate in the 16-24 age range is a matter of concern. Unlike countries in the Western Hemisphere, a college education isn't culturally considered a necessary path to employment in most of Asia. In fact, many young workers graduate directly from "technical" schools and enter the workforce. As of 2021, the Chinese government stated that 57.3% of its youth are enrolled in higher education programs. Even after factoring that in, unemployment among the 16-24 range runs nearly double that of the total rate.

It's no omission that the jobless rate estimates stop at June. The National Bureau of Statistics, citing a need for refining its calculations, has halted the publication of this metric with no stated date for resumption. Instead, a spokesperson for the organization stated that the employment situation among college graduates in China is "generally stable" and even "slightly higher" than last year. In an article for financial publication Caixin, Peking University's economics professor Zhang Dandan posited that the true unemployment rate could be as high as 46.5% if it includes those who are neither in school nor actively looking for work. This article was withdrawn shortly thereafter.

A recurrent feature of Chinese youth's reluctance has been the low wages relative to the jobs they would be expected to perform. China's political leadership had in recent times come off rather unsympathetic to such concerns by exhorting the youth to lower their expectations and "eat bitterness" (i.e. "toughen up").

There's a very sound strategic reason why China's political leadership and business magnates might not want to address stagnant/"unlivable" wages: raising wages would increase the cost of its goods and services, thus opening up the potential for substitution by a number of other countries with stronger labour laws that are still cheaper than producing in leading Western economies. Unlocking wages thus might disrupt China's "crucible" pillar unless its provides a very high level of value addition as an incentive.

Market Effects

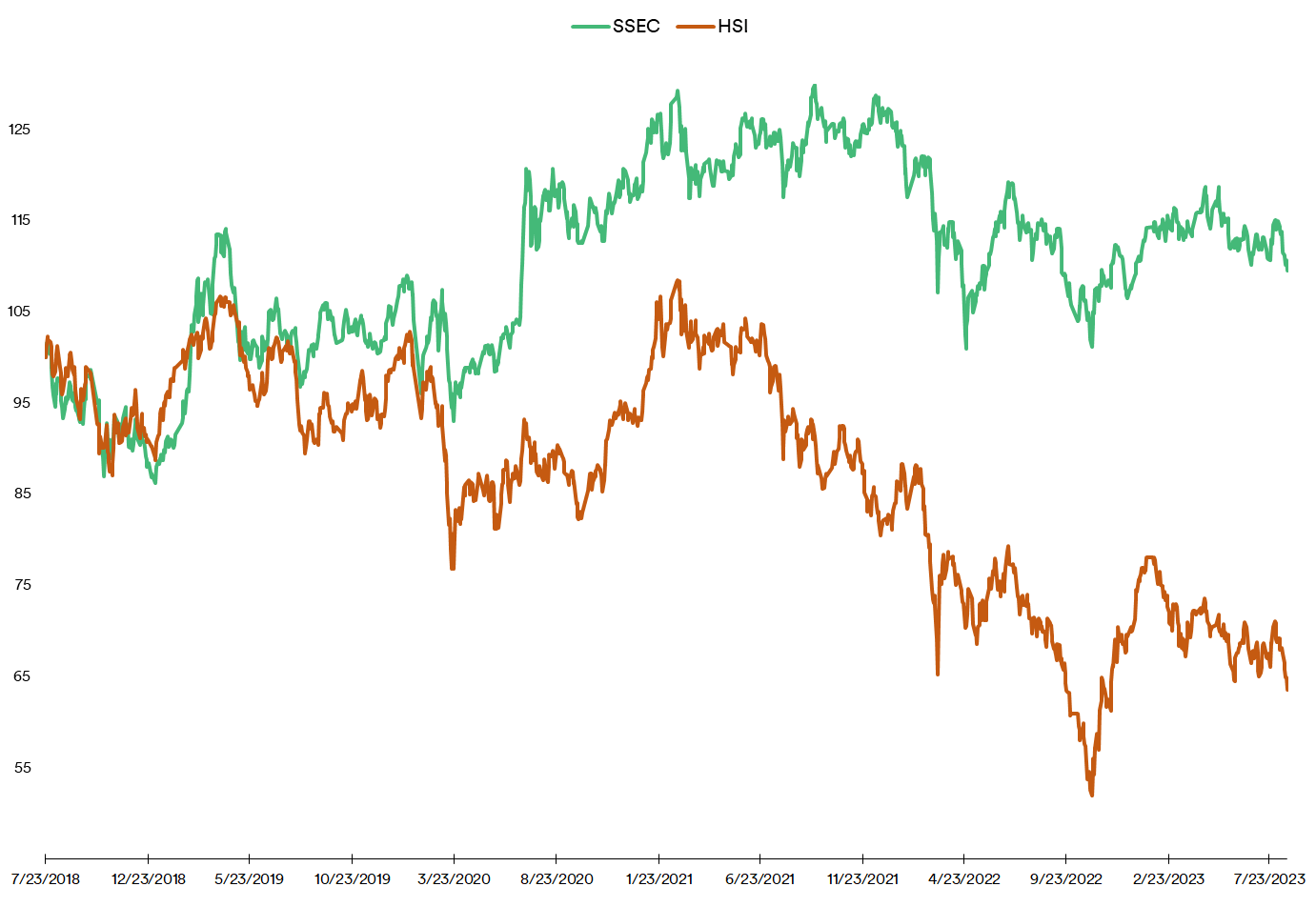

Let's consider two indices. First, the Shanghai Stock Exchange Composite Index (SSEC), which is comprised of both yuan-denominated "A Shares" (open only to domestic and certain qualified foreign institutional investors) and US dollar-denominated "B-Shares" (meant for foreign investors but also open to certain domestic investors). Next is the Hang Seng Index ( HSI ), comprised of the 60 largest companies that trade on the Hong Kong Exchange ((HKEX)) including Alibaba ( BABA ), JD.com ( JD ), Lenovo, Meituan and so forth. The constituents of this index are accessible to foreign investors via the likes of the iShares MSCI Hong Kong ETF ( EWH ), the Franklin FTSE Hong Kong ETF ( FLHK ), the KraneShares Hong Kong Tech ETF ( KTEC ) and so forth.

Over the past 5 years, the SSEC has remained above par in net performance while the HSI - by virtue of the deflation of the tech sector in the wake of regulatory crackdowns, et al, has performed under par . In all other respects, sentiments in both indices show a very high degree of correlation.

Source: Created by Sandeep G. Rao using data from Investing.com

{kind=link}

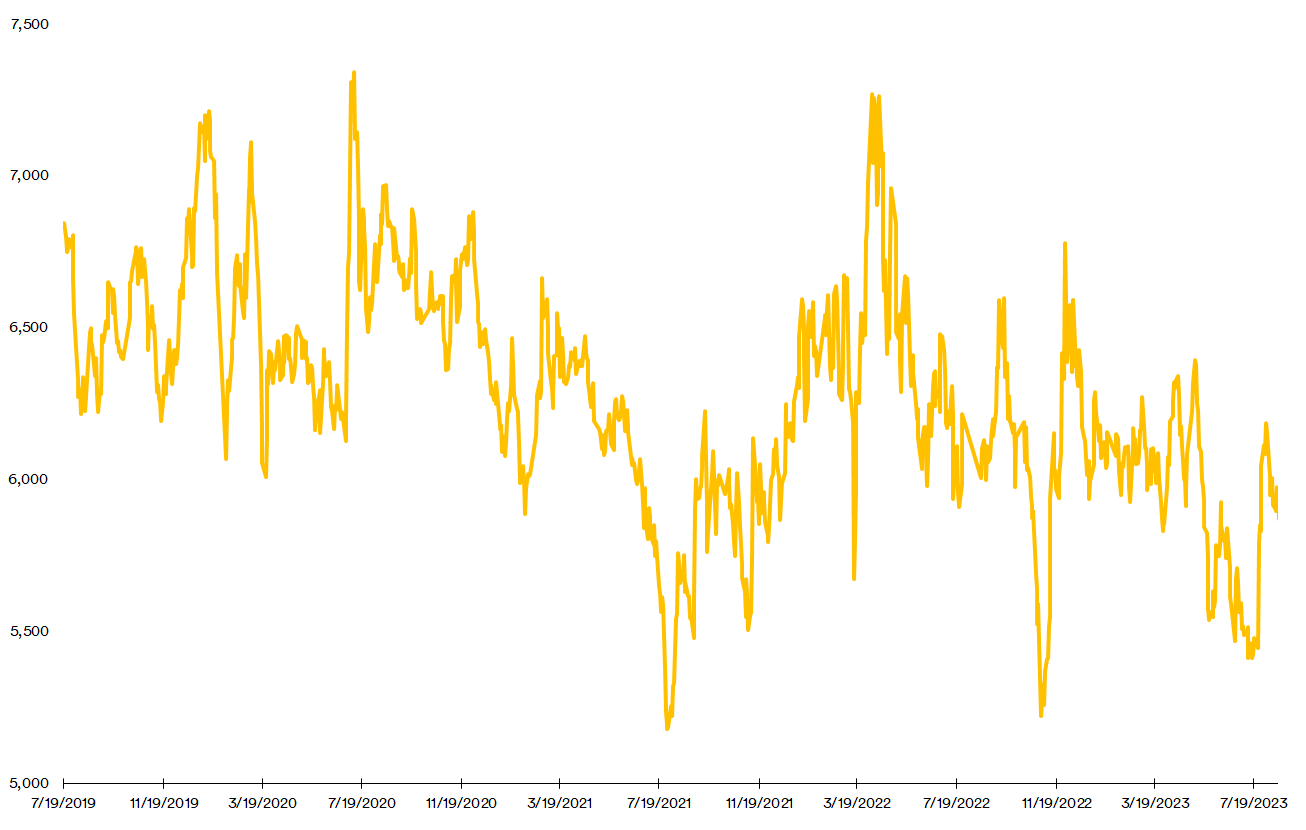

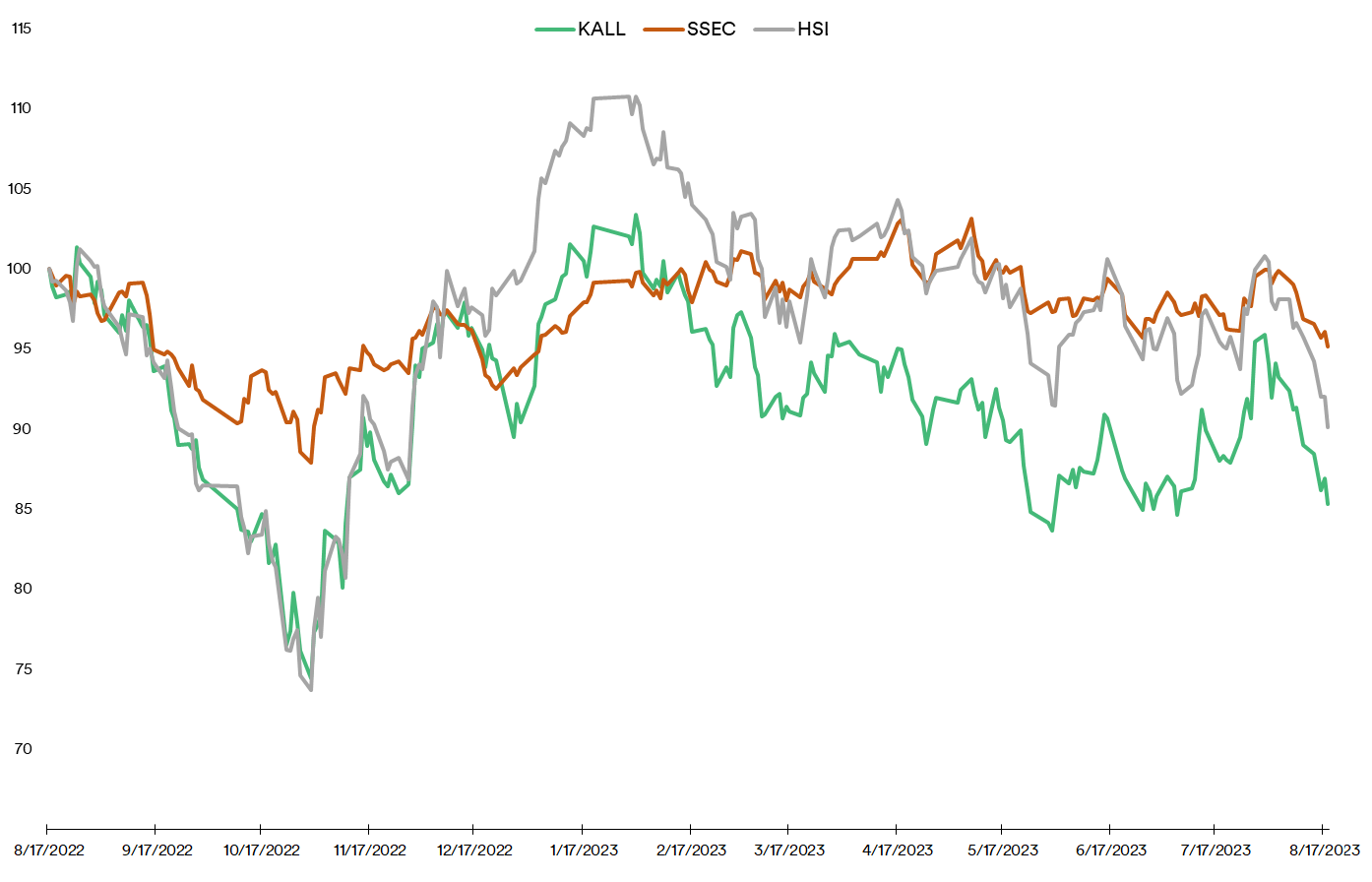

For a 1-year performance comparison, let's consider another more recent instrument that has been gaining popularity: the KraneShares MSCI All China Index ETF ( KALL ). Tracking the MSCI China All Shares Index, this fund offers exposures to A-Shares, B-Shares and Hong Kong-listed "H-Shares".

Source: Created by Sandeep G. Rao using data from Investing.com and Yahoo! Finance

{kind=link}

It is immediately discernible that foreign investor-focused KALL and HSI show strong correlations in trends. Meanwhile, the overall trend seen between HSI and SSEC over the past five years diminishes in the 1-year window, suggesting a tendency towards convergence over the long run. Also evident is that 1-year performance of the SSEC now runs below par - just like with HSI.

Of course, it's important to note that SSEC isn't entirely bereft of foreign investor participation: about 54 constituents are "B-Shares".

It also bears reiterating that institutional investors do not always pick foreign-listed instruments for their performance. The base considerations always include diversification mandates, which Chinese shares have long been a preferred choice for.

What is being weakened is the argument for considering it a "job well done" by simply buying Chinese shares for economic diversification. If the argument is participation in economic growth, the forward outlook for China looks grim as domestic consumption seems poised to be continue being impacted. There's only so much support due from the Chinese government before it stops being an "economy with choices" and turns into a "command economy" with rations allocated to all and sundry. It's unlikely that the Chinese government will revert to the latter any time soon.

My last article indicated that institutional investors have been picking up large quantities of Chinese shares. Given the economic data at hand and inferred indirect indicators, I think it can be assumed that a sustained buy-in would be hitting its peak soon for the simple reason that China's economy is caught between a rock and a hard place that will likely require years of restorative work.

For disciplined investors, diversifying beyond an easy pick via diligent research tends to bear rewards. There are many choices through which diversification can be achieved beyond both China and Developed Market economies. Sustained selections among them will inevitably begin to impact Chinese stock valuations. Caveat emptor .

For further details see:

China's Macro Indicators Suggest A Quiet Crisis