LRCX - Chinese Semi-Caps: The Only Game In Town?

2023-04-11 01:22:56 ET

Summary

- The current geopolitical landscape has pushed the Chinese state sector to invest heavily in semiconductors.

- Local semi-caps stand to benefit from the increased demand for equipment, especially given the export controls imposed on American, Dutch, and Japanese OEMs.

- The development of leading-edge nodes will prove more difficult to achieve in the absence of EUV lithography, thus capping the upside for local equipment manufacturers.

The following is the conclusion of a two-part article on the impact of the current geopolitical environment on Chinese semi-cap OEMs. For more context on their historical development and achievements to date, you can refer to the first part here .

China Semi Industrial Policy Part Deux: This Time it’s Different?

After years of US-China trade disputes and having witnessed the shortfalls of global supply chains during Covid, the Biden administration enacted policies to both re-shore chip production and to hinder China’s development of semi manufacturing. These effectively deny China access to leading-edge chips (<14nm), as well as the software and the equipment that are needed to produce them. The new policies also prohibit U.S. individuals, including Green Card holders, and corporations from facilitating such exports or transferring any relevant technological know-how. This has led to a 27% decline of semiconductor imports in China in the February 2023 YTD period.

Naturally, the Chinese State intervened. Towards the end of 2022, the government earmarked a further $143bn to bolster the domestic semiconductor market over a 5 year period. Several municipal and provincial governments announced similar initiatives, with Guangzhou setting US$29bn aside for investments in tech , including semiconductors. Casting financial incentives aside, there have also been personnel changes. The embattled CICIIF got itself a new boss , and most importantly, the recent National Peoples’ Congress ((NPC)) seemed to favour semi executives , such as the chairmen of Hua Hong and SMIC, over the likes of Tencent’s Pony Ma. The NPC is the national legislature and holds supreme legislative authority in China. Its delegates are chosen every 5 years and include mainly officials from local governments but also representatives from the private sector, indicating which individuals or industrial sectors are favoured by the authorities in Beijing.

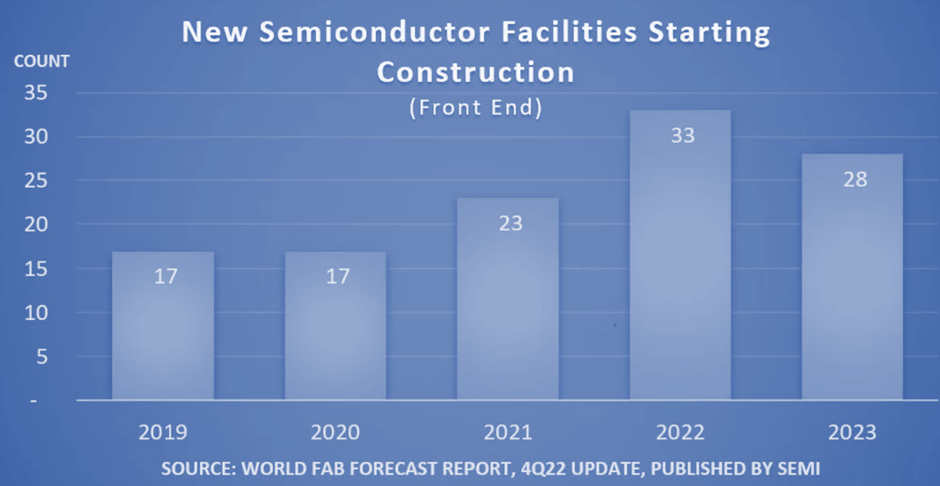

The net effect of these initiatives is expected to benefit the Chinese semiconductor and semi-cap markets. According to SEMI, the chip industry is projected to invest over US$500bn in 84 new fabs with construction start dates in the 2021 to 2023 period. China is set to outpace all other regions with 20 new starts. At this rate, SEMI projects that China will have the largest capacity for 300mm wafer fabrication globally by 2026, with a projected 25% worldwide market share . That presents a huge opportunity for semi-cap OEMs, with Chinese fabs projected to buy US$16.3bn worth of equipment this year alone. That is an opportunity that several American companies will largely have to pass on, with Applied Materials and Lam Research announcing that they will have to forego roughly US$4 – 4.5bn of revenue from China in 2023. That figure translates to about a quarter of total semi-cap demand in China this year and is larger than the combined revenue of China’s two largest toolmakers, AMEC and NAURA, in 2022.

{kind=link}

To be clear, that is not to say that there is a US$4 – 4.5bn upside for Chinese OEMs. There are in fact several factors that may diminish this upside, among them:

- Lam and Applied might be inflating their foregone revenues in China to hide potential losses elsewhere

- It is still unclear how the likes of ASM and other smaller non-US OEMs such as Aixtron will address the Chinese market

- It is not a given that Chinese OEMs will be able to supply some of the more advanced process tools needed in those fabs

Having said that, it is fair to assume that there will be subsidies in place for Chinese fabs to purchase their equipment locally. That, coupled with political pressure, ought to ensure that the lion’s share of the revenue foregone by Applied and Lam is distributed among Chinese OEMs. I would imagine that this trend persists in the medium term, and possibly beyond, and that we will witness a strong upside in the revenue of Chinese semi-caps, especially in process equipment for trailing edge nodes.

Though it might be reasonable to expect that Chinese semi-caps will be able to support, and indeed benefit from, the growth of the local chipmaking industry for more mature nodes, their ability to support the development of more advanced node manufacturing remains questionable.

Tools for Leading Edge Nodes

To produce smaller nodes, TSMC, Samsung and Intel have largely relied on EUV lithography tools produced by ASML. EUV technology uses shorter wavelengths and reflective optics to create smaller features on silicon wafers with fewer processing steps than DUV technology, making it a critical tool for the semiconductor industry to continue shrinking the size of transistors and other features on microchips. ASML’s exports of EUV to China were banned in 2019 and as a result, Chinese chipmakers have not yet been able to produce leading edge at scale, with SMIC and Hua Hong reporting down to 28nm and 55nm node production respectively. To make matters worse for China, the Netherlands have recently agreed to start controlling the export of immersion lithography machines, the best alternative to EUV, and Japan followed suit shortly thereafter .

Hua Hong Revenue Breakdown by Tech (Hua Hong 2021 Annual Report)

{kind=link}

SMIC Revenue Breakdown by Technology (SMIC 2021 Annual Report)

{kind=link}

In spite of this shortfall in lithography, it has been widely reported that SMIC was able to produce 7nm chips for a bitcoin miner using double pattern lithography. Double pattern lithography is a technique where two different patterns are created and overlaid to form a single layer, allowing for the creation of smaller and more complex features on the silicon wafer. Though it may achieve the desired effect, double patterning requires more processing steps than single pattern EUV lithography, thereby increasing manufacturing costs and reducing production throughput.

While it is technically possible to manufacture advanced chips using alternative lithography techniques such as multi-patterning, it is highly unlikely that Chinese fabs will be able to efficiently do so without EUV or immersion technologies. To illustrate, Intel spent tens of billions of dollars in capex over a span of nine years to achieve economic yields on their Intel 7 chips without EUV technology. For the sake of comparison, by being an early adopter of EUV technology, TSMC was able to produce chips with smaller feature sizes and higher transistor densities in a cost-effective manner that made it an attractive partner for clients such as Apple, AMD, and Qualcomm. This gave TSMC a head start in the race to produce high-performance chips for industries such as artificial intelligence and 5G.

The only alternative to imported advanced lithography tools in China, SMEE, is two decades behind ASML, and even though they were able to produce tools that could scan patterns as small as 90nm, their alleged capabilities to produce 14nm scanners are hard to verify. Moreover, according to a Chinese semi executive cited in the Financial Times, “homegrown lithography was examined and verified by academics, not industrial engineers. This equipment is only theoretically usable, and no chip manufacturer has ever dared to activate such a machine in their fabs.” In fact, the top management of the company, which was founded in 2002 by a state power firm executive, had no prior experience in lithography. To build their first machines, they bought second-hand equipment and studied public patents and papers. It is hard to imagine how SMEE might be able to bridge the gap with ASML given their lack of utilisation, but also considering the lack of engineers with experience in lithography tools and of tier-1 suppliers to support their development.

ASML began developing EUV lithography technology in the late 1990s. It took the company over two decades of research and development to bring EUV technology to commercial viability. China is a large country with an abundance of engineering talent, but in the current geopolitical environment it is highly unlikely that they will be able to produce an EUV tool enabling its fabs to build leading edge nodes. This lithography hurdle will have market-wide repercussions in the Chinese semi-cap space, and whilst the majority of local fabrication equipment manufacturers are likely to benefit from an expanded serviceable market in trailing edge nodes, it is unlikely that that market will be expanded to also include sub-14nm chip production in the foreseeable future.

Conclusion

In the current geopolitical landscape, with China effectively being cut-off from vast cross-sections of the global semi supply chain, there is a heightened sense of urgency in reaching self-sufficiency. To that end, the public and private sector will invest heavily to create the largest 300mm wafer capacity worldwide by 2026. Thanks to the export restrictions imposed on American, Dutch, and Japanese semi-cap OEMs, domestic semi-cap OEMs are being presented with a unique opportunity to step in and fill that void. In 2023, they could stand to benefit from up to US$4.5bn worth of incremental sales to the detriment of Lam Research and Applied Materials alone. This trend is expected to continue in the absence of a détente between the US and China, with Chinese semi-caps being among the main beneficiaries from the growth of the local chipmaking industry for mature nodes. However, their ability to support the development of more advanced nodes remains questionable, particularly due to the lack of advanced lithography tools.

Growth in leading edge chipmaking tools will have to come the hard way and over a long-term horizon, through advancements in research, better capital allocation and possibly innovative chipmaking processes that leapfrog the need for EUV lithography altogether.

For further details see:

Chinese Semi-Caps: The Only Game In Town?