PBJ - Choke Up On The Bat

Summary

- Performance across the major asset classes has been challenged in 2022.

- This difficult performance may continue for the foreseeable future.

- What is the asset allocation investor prioritizing diversification and risk control to do?

Don’t call it a comeback . But it was all going so well just a few weeks ago. Stocks as measured by the S&P 500 were cruising through the summer after a difficult start to the year. Bonds were also getting in on the hot weather rebound after enduring a struggle of their own in 2022. Even gold started to perk up this summer after the Fourth of July holiday. But as the month of August rolled on, the rebound for each of these categories started to tail back off to the downside.

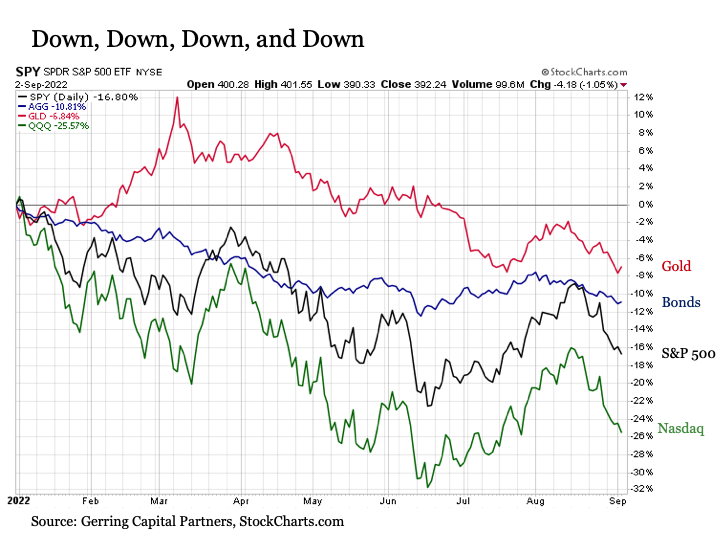

No safe haven in the wild . Performance across the major asset classes has been nothing short of ugly so far in 2022. Consider the following chart of stocks as represented by the S&P 500, bonds as measured by the Bloomberg US Aggregate Bond Index, and the spot price of gold since the start of the year. Each are down and down hard. The S&P 500 is down -17%, and the category that so many investors are piled into in tech is down an even more pronounced -26% as measured by the Nasdaq 100 Index. Bonds, which have a long-established reputation as the great diversifier against a stock market decline, are also down by -11%. And gold, which is regarded as the portfolio diversification insurance policy, gave up its early in the year +12% upside and is now down -7% in its own right in 2022. With seemingly all of the major capital market asset classes struggling in 2022, what is the asset allocation investor prioritizing diversification and risk control to do?

{kind=link}

I wonder . First, investors are well served to adapt their mind set not only for the current environment, but also for what may lie ahead for the next 12 to 18 months if not longer. For while so many became accustomed to #winning when it came to their portfolios since the Great Financial Crisis, the game in which we are playing has definitively changed in 2022. Long gone are the days when the U.S. Federal Reserve would ease monetary policy at the first signs of stock market weakness. In its place is a new Fed sheriff in town that has assumed a honey badger mindset about stock market declines as it carries out tightening monetary policy amid an inflation battle that continues to rage. Put simply, now is not at all the time for investors to swing for the fences and catch falling knives with their portfolio allocations. Instead, now is the time to choke up on the bat and focus on making risk controlled contact by focusing on single and double caliber investment portfolio themes that offer more reliable upside opportunity with relatively less price volatility.

Next, while the allocation across asset classes process is so critically important in the portfolio construction and maintenance process, the specific allocations within asset classes also holds critical importance in capturing upside opportunity and managing against downside risk. This is where targeted active management can add meaningful value to a portfolio strategy over time.

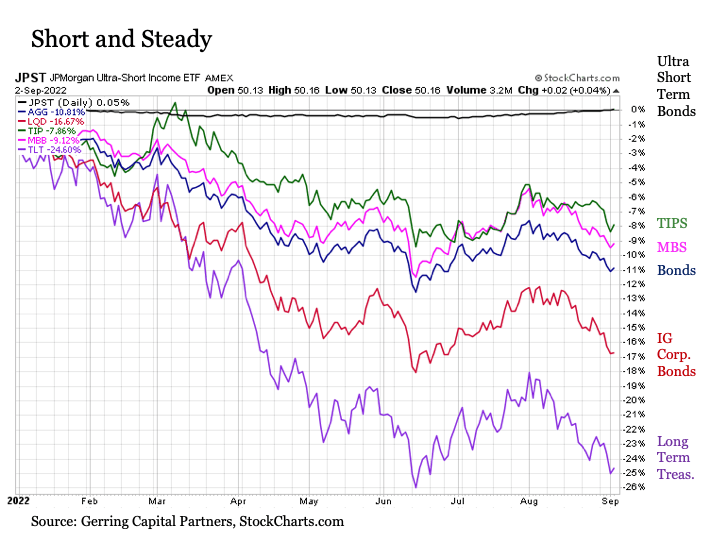

Follow the leaders . Let’s start with the bond market. We’ll focus on the investment grade side of the category, as more speculative high yield bonds are more highly correlated with stocks than investment grade bonds. It should be noted, however, that high yield bonds, convertible bonds, senior loans, and emerging market debt have all been varying degrees of terrible performers this year in their own right.

Bonds . It has undoubtedly been a difficult year for investment grade bonds. Given that inflation is the primary determinant of bond returns, the fact that we have been in a raging albeit recently improving inflation environment throughout 2022 has made for a tough environment for bonds to perform. And performance has been challenging across virtually all of the major investment grade bond categories.

{kind=link}

As would be expected, the long duration side of the bond market has performed worst. For example, long-term U.S. Treasuries are lower by nearly -25% so far this year. I will share that I have held a target weighting to long-term U.S. Treasuries for many years and have continued to maintain it through 2022. Despite its recently poor performance, I remain highly constructive on the prospects for long-term U.S. Treasuries going forward, as I expect inflationary pressures to continue to abate as the economy continues to descend toward recession (assuming, of course, it’s not in it already).

Treasury Inflation Protected Securities, or TIPS, have also struggled this year at down -8% despite the fact that we have been enduring four decade high inflation in 2022. It should be remembered, however, that while TIPS do provide inflation protection, they are also Treasury securities. And the inflation protection identity has been more than offset by the Treasury securities downside. Nonetheless, I have been an almost perpetual target weight owner of TIPS in my broad asset allocation strategy, and I expect to maintain this allocation for the foreseeable future. This is because TIPS offer the best of many worlds. They are bonds backed by the full faith and credit of the U.S. government and serve as a safe haven during periods of capital market volatility. TIPS also provide inflation protection to help protect against pricing pressures like we are enduring today. TIPS are also a great asset allocation portfolio diversifier, as they have a low positive correlation to stocks (+0.25) but also a fairly low positive correlation to the long-term U.S. Treasury market (+0.56) and gold (+0.45). These are just a few reasons to like TIPS for the long run.

Investment grade corporate bonds and mortgage backed securities (MBS) have also fallen steadily and sharply thus far in 2022 at down -17% and -9%, respectively. I’ve been zero weight to investment grade corporate bonds for the last few years now – if it weren’t for the Fed’s extraordinary intervention at the onset of the COVID crisis in 2020, “blue chip” companies like Boeing would have likely been in a heap of trouble (and when I say “heap of trouble”, I mean bankrupt). And I remain troubled by the steady increase in debt-to-total capitalization ratios over the last few decades and the increasing pileup of companies in the BBB credit quality space, some of which are probably more suited from a financial health perspective to crossing the hard line from investment grade to speculative grade and being rated BB or lower if we’re being real. As for MBS, I exited the space back in early March due in part to expectations that the shift toward quantitative tightening (QT) by the U.S. Federal Reserve would further undermine what had already been an unfavorable supply/demand imbalance for the category dating back to last year.

So where for the bond investor to go? While performance has certainly been unexciting from an absolute returns perspective, the ultra short-term segment of the investment grade bond market has been a relative bright spot. As I’ve always said, a +0.01% positive return is always better than a -40% return at any given point in time, and in the case of ultra short-term bonds, a +0.05% positive return so far in 2022 sure beats the -11% return of the broader investment grade bond market. Ultra short-term bonds are by far my largest overweight in my broad asset allocation strategy, and I suspect it is likely to continue to be so through at least mid-November if not the remainder of the year and into next.

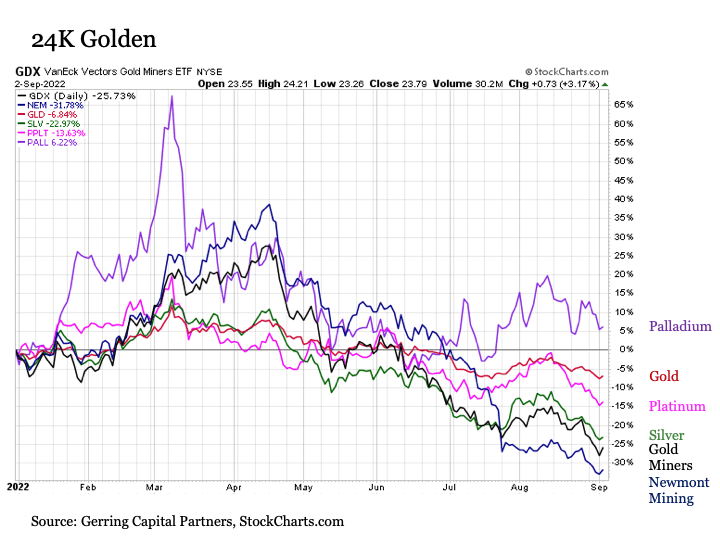

Gold . Precious metals have also had a tough slog so far this year. Palladium stands out as being +6% higher in 202, but of course this overlooks the fact that it is also down a hard -38% since early March after surging more than +65% in the first two months of the year. That’s breathtaking volatility no matter how you cut it.

{kind=link}

Then there’s the rest of the complex. Fellow catalytic converter component platinum is lower by -14%, and this stands out as reasonably good in the crowd. Silver is now down -23% for the year, and the gold miners are off by more than -25%. Even Newmont Mining, which is among my most favored from a financial health and quality perspective among the publicly traded firms, is down by more than -30% despite boasting a lower price standard deviation over time versus the gold miner aggregate.

This leaves us with gold, which remains my favored precious metals allocation for a number of reasons going forward despite the fact that it is lower by -7% for the year to date. First, it has a price volatility that is vastly less than the rest of the group, in some cases by more than half less than certain category peers. Next, gold’s long-term standard deviation is comparable to that of the S&P 500 and is measurably less than the tech heavy Nasdaq 100. Also, gold has generated a compound annual growth rate since the start of the new millennium that has outperformed the U.S. stock market by more than a percentage point, thus giving gold a superior Sharpe ratio at 0.45 versus 0.39 for stocks over this 22+ year time period. Lastly, it is a great portfolio diversifier, as it’s returns are effectively uncorrelated with the S&P 500 and have a low negative correlation with U.S. Treasuries.

For all of these reasons, I maintain a modest overweight to gold in my broad asset allocation strategy and am likely to maintain it given that gold has historically performed best during periods of economic and geopolitical uncertainty.

What about the lackluster performance in the meantime? While gold is widely regarded as an inflation hedge, it does not necessarily perform well during inflationary periods as investors are bracing for the fact that the Fed will tighten monetary policy aggressively, which has a negative effect on gold prices. As inflationary pressures fade and recession risks rise, gold is likely to regain its footing in making its next move higher.

Stocks . As mentioned above, the S&P 500 has been a bummer in 2022, and the tech heavy Nasdaq 100 has been even worse. But the primary problem for stocks is right there in the previous description. We have the two headline stock market benchmarks in the S&P 500 that has a 27% weight to the information technology sector and the Nasdaq that has nearly double as much with a 50% weighting to tech. That’s a lot, a lot, a lot of tech. Then you throw in the tech adjacent sectors of communication services (a number of the largest names in the communication services sector including Alphabet (ne Google) and Meta Platforms (ne Facebook) used to be part of the information technology sector) and these weighting push toward 50% for the S&P 500 and over 80% for the Nasdaq 100.

But here’s the thing. I don’t want any part of any of these three sectors right now. And outside of recent past allocations to Cisco Systems and Verizon Communications, neither of which are the respective sector highflyers, I haven’t wanted much of any part of these sectors for quite a while now. Yet these are the sectors that are effectively driving the discussion on how “stocks” are doing at any given point in time. And all three are languishing at the bottom of the sector performance table for 2022, with tech and consumer discretionary down over -23% year to date and communication services down over -30%.

{kind=link}

Instead, I’ve wanted to favor sectors, industries, and individual stocks where applicable that have attractive growth prospects and, definitely unlike the three sectors mentioned above, also have discounted valuation characteristics. I also like sectors that have price volatility below that of the S&P 500 Index where possible.

Given this focus, let’s start with consumer staples that has a historical price volatility that is roughly one-third less that of the broader S&P 500. Within the sector I particularly like the food industry, and within this industry I’ve particularly liked Kellogg. A +16% year to date return certainly beats a -16% year to date return.

{kind=link}

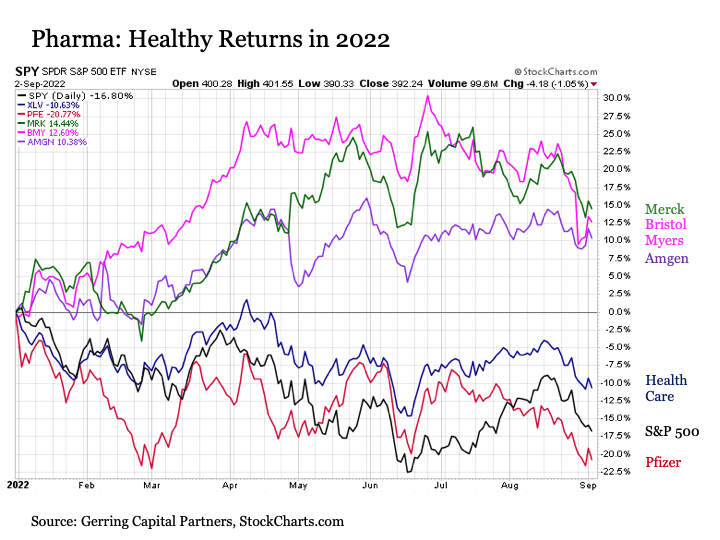

We’ll continue on to health care, which also boasts less price volatility than the broader market. Within health care I favor the pharmaceuticals industry, and within pharma I have particularly favored Pfizer, Merck, Bristol Myers Squibb, and until recently Amgen (from an asset allocation risk control perspective, I need to reduce my heavy overweight to health care as part of larger de-risking). While Pfizer has been a relative underperformer, Merck, Bristol Myers, and Amgen have all posted double-digit positive returns in 2022.

{kind=link}

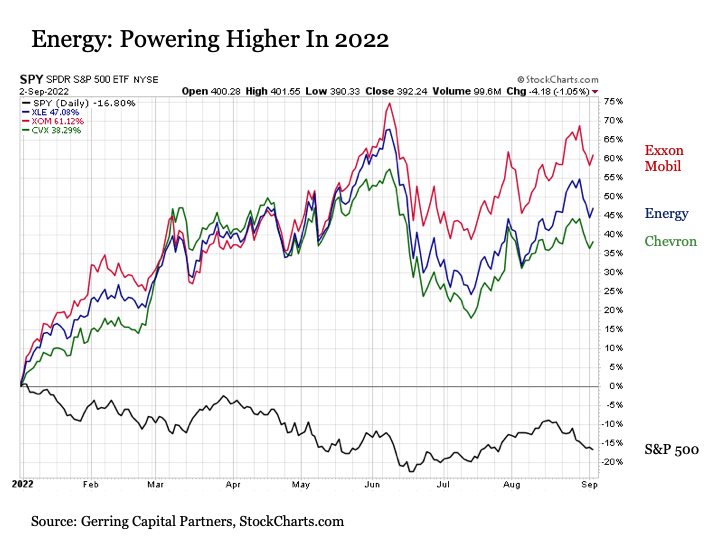

Next up is energy, where the chart below speaks for itself. High oil prices, broader inflation, and the recognition that no matter how much global leaders may want to phase out fossil fuels in favor of green energy, we’re very likely going to need both in a meaningful way for the foreseeable future. Within the energy sector, I continue to favor ExxonMobil and Chevron, both of which have lower price volatility than the broader energy sector as a whole.

{kind=link}

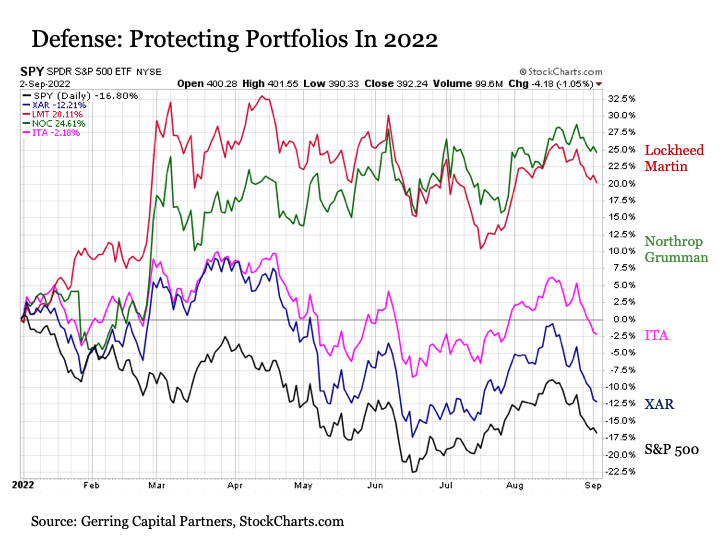

Lastly, with a conflict ongoing between Russia and Ukraine and the potential for more geopolitical confrontations in the years ahead, I’ve favored the defense industry with the industrials sector for some time. Given that aerospace and defense ETFs give me the aerospace exposure that I would like to forgo, I have instead favored targeting individual names such as Lockheed Martin and Northrop Grumman, both of which have meaningfully outperformed the broader market as well as their associated aerospace and defense ETFs by a wide margin.

{kind=link}

These are just a few of the numerous sector, industry, and individual stock opportunities that continue to exist within a broader market that has been struggling throughout much of 2022. Notably, not only have opportunities like these generated positive returns that meaningfully outperformed the broader market, they have done so with measurably lower price volatility in many cases.

Bottom line . The days of easy capital market returns are over. No longer can investors simply pile into the S&P 500 Index or any other asset class leaders and expect the positive returns to come pouring in. Investors in 2022 and going forward will need to work harder and look closer both across and within asset classes to identify particularly attractive total return opportunities. Ideally, this pursuit can also incorporate reducing portfolio risk in the process as well if executed properly.

Capital markets going forward are also likely to require more patience than they have in the past. By their nature, growth securities tend to be more instant gratification when they are working, while value securities require more patience to allow the trading discount to resolve itself over time.

Do your homework, identify targeted opportunities, emphasize risk control, and remain patient and disciplined. Such are the likely keys for not only #NotLosing but #winning in the 12 to 18 months ahead if not longer.

For further details see:

Choke Up On The Bat