PXD - Chord Energy Corporation: Low Valuation And Shareholder-Friendly Management

2023-05-10 14:48:23 ET

Summary

- Chord Energy Corporation saw a better than expected result as shown in the last earnings report as momentum has started to pick up.

- The demand for oil and natural gas will be here for a long time as the transition to an electrified society still requires these commodities.

- Chord has managed to build a strong balance sheet and has good free cash flow yields to help support the dividend and, therefore, I will rate it a buy.

Investment Summary

Chord Energy Corporation ( CHRD ) is a U.S.-based company that specializes in hydrocarbon and hydraulic fracturing exploration. They mainly operate in North Dakota and Montana where they search for oil and natural gas sources. Once they acquire sites, they develop and exploit them to sell their products to a large customer base in the United States.

Chord Energy Corporation has managed to achieve a strong margin across the board but, as shown in the last earnings report , the company can face struggles such as weather which significantly impacted the oil volumes. Despite that, the company still stays true to its shareholder-friendly approach and returned 75% of adjusted free cash flows, and declared a base-plus-variable dividend of $3.22 per share. I think the future is slightly uncertain for the company right now, as it seems to pass on all profits to shareholders, which of course limits capital available to fund expansions. For 2023, the company is investing over $800 million into drilling and completions, and I believe that we will have oil and natural gas with us for a very long time ahead. I will rate Chord a Buy because of the steady trends ahead and the shareholder-friendly management.

The Outlook For Oil And Gas

As I said in the first part of this article, I don't think we will be rid of oil or natural gas anytime soon. There are too many major trends that need to shift in order for that to happen. With India as a quickly emerging market, I think there will be demand there, if not in the U.S. Not in that Chord will set up projects there, but that there will be global continued demand that puts Chord in business as their services continue needing use.

Looking at the U.S, though, it doesn't seem that natural gas is slowing down here, either, a 3% increase from 2022 levels is expected for 2023. This goes against a lot of the thoughts that we are going towards a greener society.

Where I might have some worry going forward is that the oil prices have seen drops from the highs of around 120 in June last year. As stated in a presentation by Chord, they have 1,374 locations that are economic when oil prices go above 80, but thankfully they have another 1,085 locations which remain economic at 60.

Right now I don't expect any strong growth for the coming quarters, as oil seemed to have had its rally. There needs to be another catalyst to push the price up and give Chord a bump in their revenues as in 2022. In Q3 2022 , they had $1.1 billion in revenues and the forecast for 2023 sits at $850 million for the same quarter. I think this is quite reasonable if current prices remain similar. Buying into Chord isn't necessarily done because of a bet on oil prices going up; it's based on that the management can still put out a lot of value to shareholders through a high dividend funded by strong cash flows.

Risks

The main risk I see with Chord is perhaps that oil prices remain at these levels or even lower. The only benefit of owning shares in Chord then would be the dividend. With lower oil prices the estimates for Chord's future revenues also go down of course and that will help justify the low multiple it has right now. The sector doesn't trade above 10x earnings and Chord is below that on a forward basis. Slow growth and a failure to invest in new projects will justify the valuation and the investment won't see the same appreciation in value as perhaps other established companies like Canadian Natural Resources Limited ( CNQ ) or Pioneer Natural Resources Company (PXD).

But I still see the potential in Chord, and they have a strong financial position which I believe can be leveraged efficiently to gain new market share and deliver value to investors.

Financials

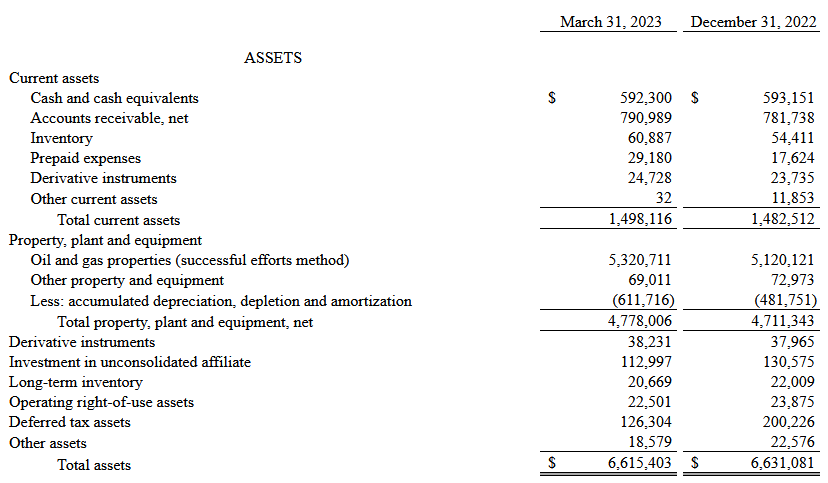

Looking at the balance sheet for Chord, I have already said I think they are in a strong position. A change I see right off the bat is the cash position seeing a slight decrease from $593 million at the end of 2022, now sitting at just under $592 million. Still sitting strong in my opinion, and nice to not see any drastic shifts from QoQ. Assets also saw a major increase between 2021 and 2022, more than doubling as the company's oil and gas properties massively increase by close to $4 billion. Seeing assets still remaining strong makes me confident Chord has a strong position to leverage from once oil prices see another surge.

{kind=link}

{kind=link}

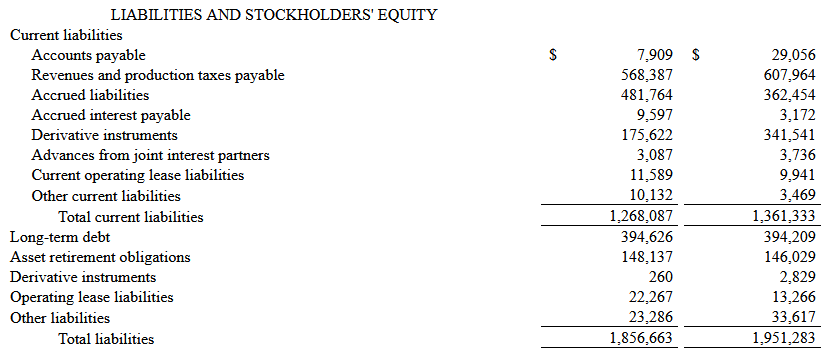

Despite the large growth of assets from 2021 to 2022 on the balance sheet, the long-term debts haven't followed. This puts the company in an incredibly strong position. If the management wishes, they can easily pay off the $394 million in long-term debts without any issues. The net debts are currently negative at around $143 million which I think further highlights the strategic moves the company managed to make in 2022. As we are almost halfway into 2023, I do expect the ROA to take a hit though. The 25% the company has currently won't be sustainable as oil prices remain significantly lower than the year previous. Moving into the coming quarter, investors should also be looking at the cash position of Chord specifically. I want a move upwards and no large increase in the debt. This, I think, will be a major benefit once the market and tide turns in the sector.

Valuation & Wrap Up

Looking at the valuation of Chord, you might be worried to see the forward p/e increasing rather than decreasing. But I think it's fair, seeing as 2022 was a special year for companies who gain from high oil prices. The prices were unsustainable, and I think most people could see that revenues would drop for the coming year or two at least.

{kind=link}

Where I say I see the value in Chord Energy Corporation is the strong balance sheet they have, which they should be able to leverage and bring value to shareholders. The dividend yield sitting at 3.53% is very intriguing, as the company is announcing quite regular raises for it. I do believe the cash flows to be under slight pressure for the year, but even if we remind at the same oil prices of between 70 and 80, Chord estimates they still will have an FCF yield of 14 - 15% and EBITDA coming in around $1.75 billion for 2023.

I think Chord Energy Corporation is a buy based on that my view that oil and natural gas will continue seeing growth and demand for many more years. Chord Energy Corporation sits in a good position to gain from it.

For further details see:

Chord Energy Corporation: Low Valuation And Shareholder-Friendly Management