CHD - Church & Dwight: Quality Business Trading At A Premium

2023-06-22 03:47:50 ET

Summary

- Church & Dwight has been a successful compounder in recent years and after facing a challenging 2022, the business is rebounding this year.

- Q1 2023 results were better than expected across the board, beating estimates and raising guidance.

- However, CHD stock appears expensive compared to historical averages, suggesting a cautious approach to entry at the current valuation.

Investment Thesis

Church & Dwight ( CHD ) has been a magnificent compounder over the last decade. And after a rough 2022 dominated by inflation and supply chain issues, the company is getting back on its feet in 2023. The business is performing better than expected: they beat earnings and raise guidance. However, we believe that the stock has already priced the majority of the future growth and looks expensive relative to historical averages.

Business Overview

Church & Dwight develops, manufactures, and markets a broad range of consumer household and personal care products and specialty products focused on animal and food production, chemicals, and cleaners. It was founded in 1846.

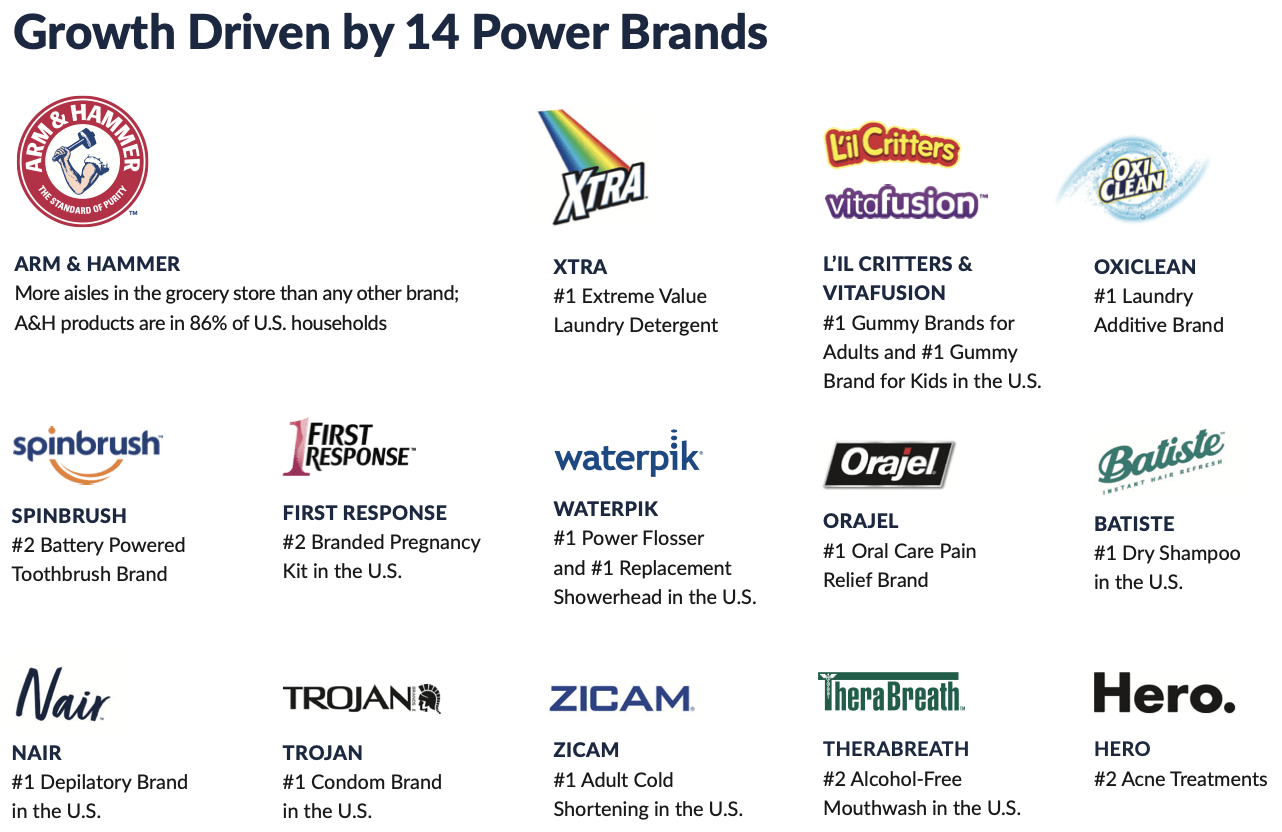

The company's efforts are focused primarily on its 14 "power brands". This list includes ARM AND HAMMER (baking soda, cat litter, laundry detergent, carpet deodorizer, and other baking soda based products), TROJAN (condoms, lubricants and vibrators), and OXICLEAN (stain removers, cleaning solutions, laundry detergent, and bleach alternatives), among others. Church & Dwight sells its products through a broad distribution platform that includes supermarkets, mass merchandisers, wholesale clubs, convenience stores, etc., in the US and internationally.

Church & Dwight 2022 Annual Report

{kind=link}

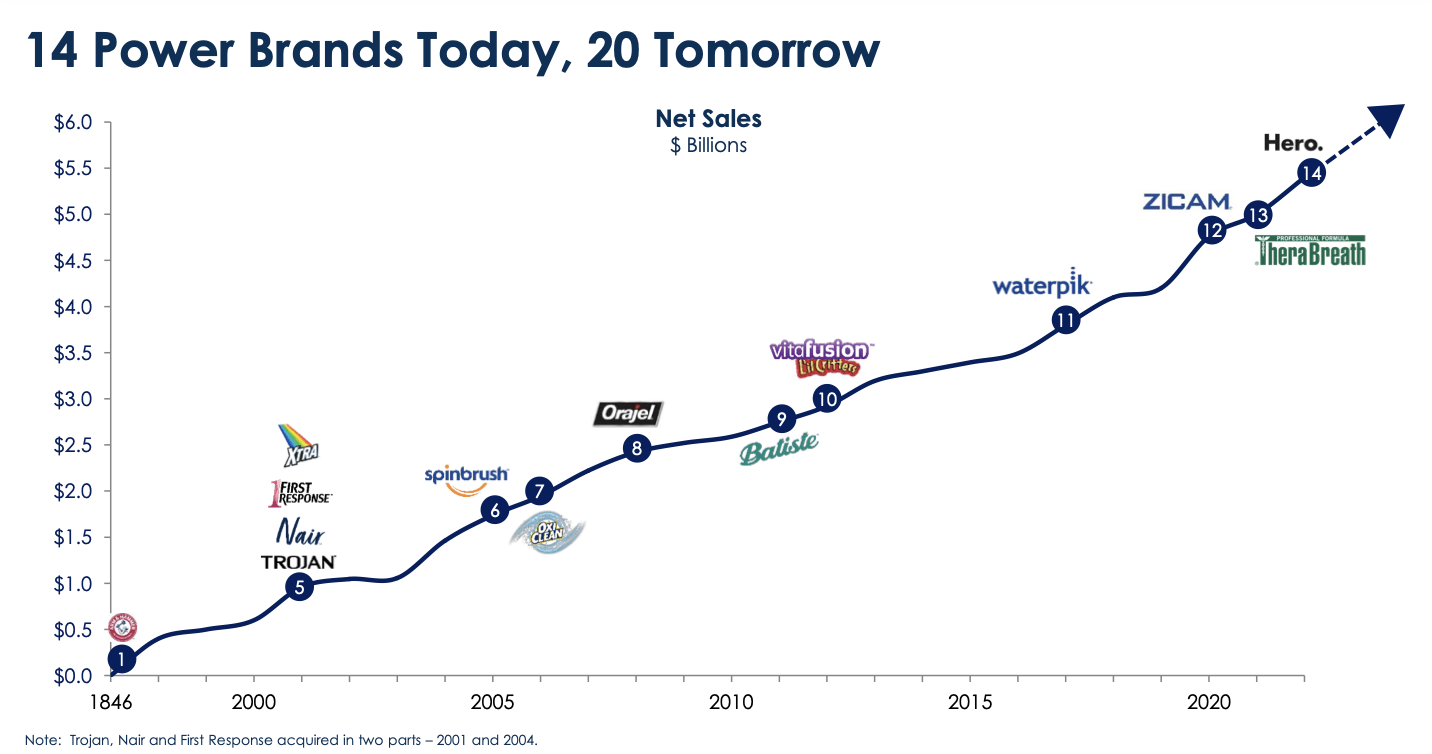

13 out of the 14 "power brands" were acquired since 2001, and they currently represent 85% of revenue and profits. The company has a long history of growth through acquisitions and, as you can see in the graph below, made very clear in stating that it will not stop at 14 power brands.

Church & Dwight Presentation - dbAccess Global Consumer Conference 2023

{kind=link}

As a result, the stock has compounded money at a 13.3% CAGR over the last 10 years, and at 16.9% per year since inception.

Q1 2023 Financial Results

Church & Dwight reported better than expected Q1 2023 financial results on May 31. Net sales grew 10.2% to $1.3 billion, surpassing the company's expectations, while organic sales grew 5.7% YoY due to pricing power and product mix. Notably, the company's domestic brands grew consumption in 12 of 17 categories in which they compete, and 8 out of the 14 "power brands" gained market share.

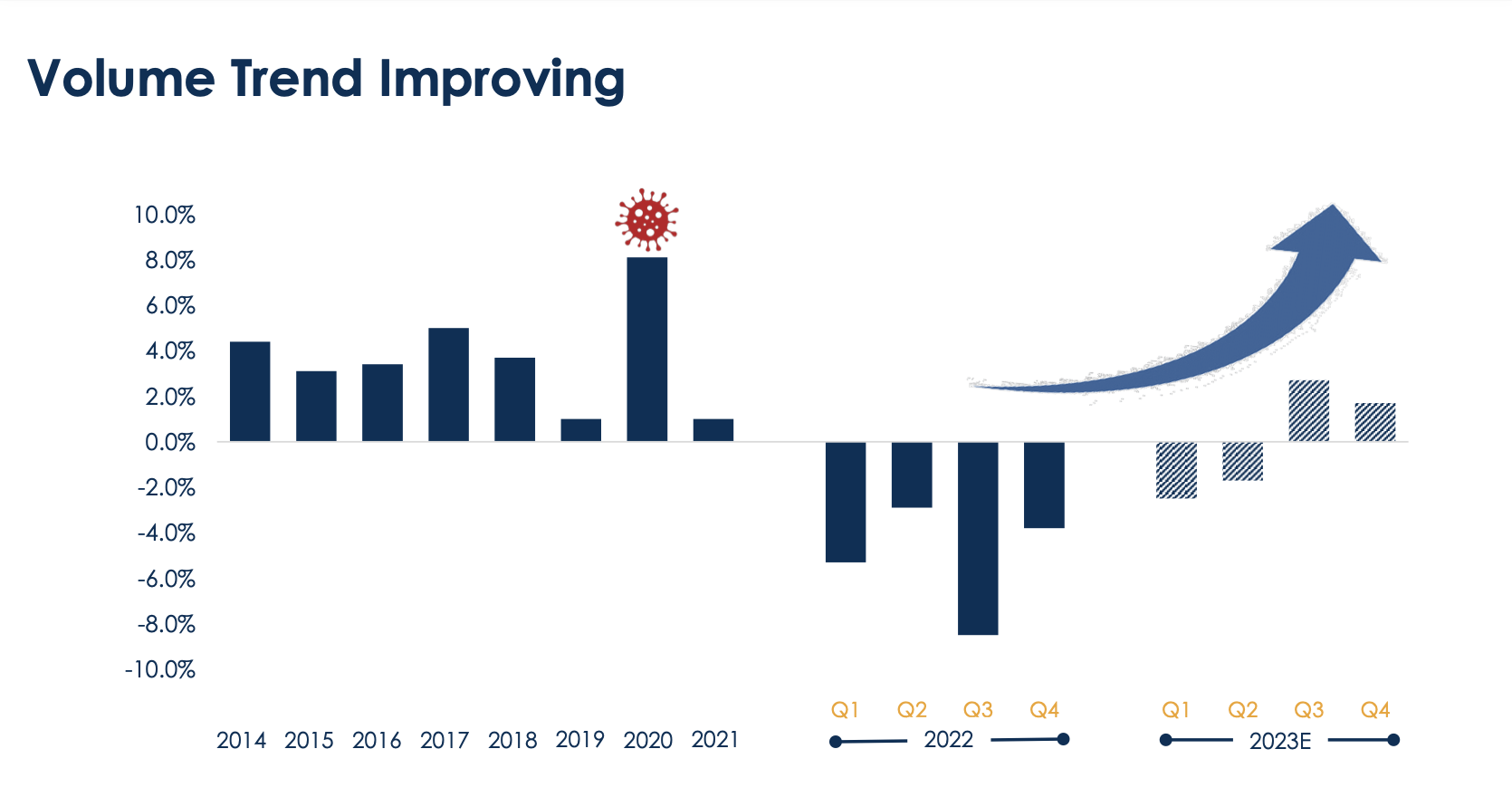

Product volume sold, on the other hand, was flat YoY. Volume is highly relevant because the company cannot rely solely on price increases to grow organic sales. Volume was negative through 2022, but we expect it to return to be positive in the second half of the year given the improving fill rates and the supply chain issues being resolved. To give you an idea, fill rates increased to 93% in Q1 2023 from 72% in Q1 2022.

Church & Dwight Presentation - dbAccess Global Consumer Conference 2023

{kind=link}

Gross margin increased 90 basis points to 43.5% due to improved pricing, productivity, and the impact of the Hero acquisition. The gross margin took a big hit in 2022 due to higher commodities, higher transportation costs, labor increases, and investments. However, all of these problems are practically gone in 2023, and we expect that their pricing and productivity efforts will exceed inflationary pressures, leading to higher gross margins in the coming quarters. Plus, gross margin should also benefit from volume leverage as it turns positive in the second half of the year.

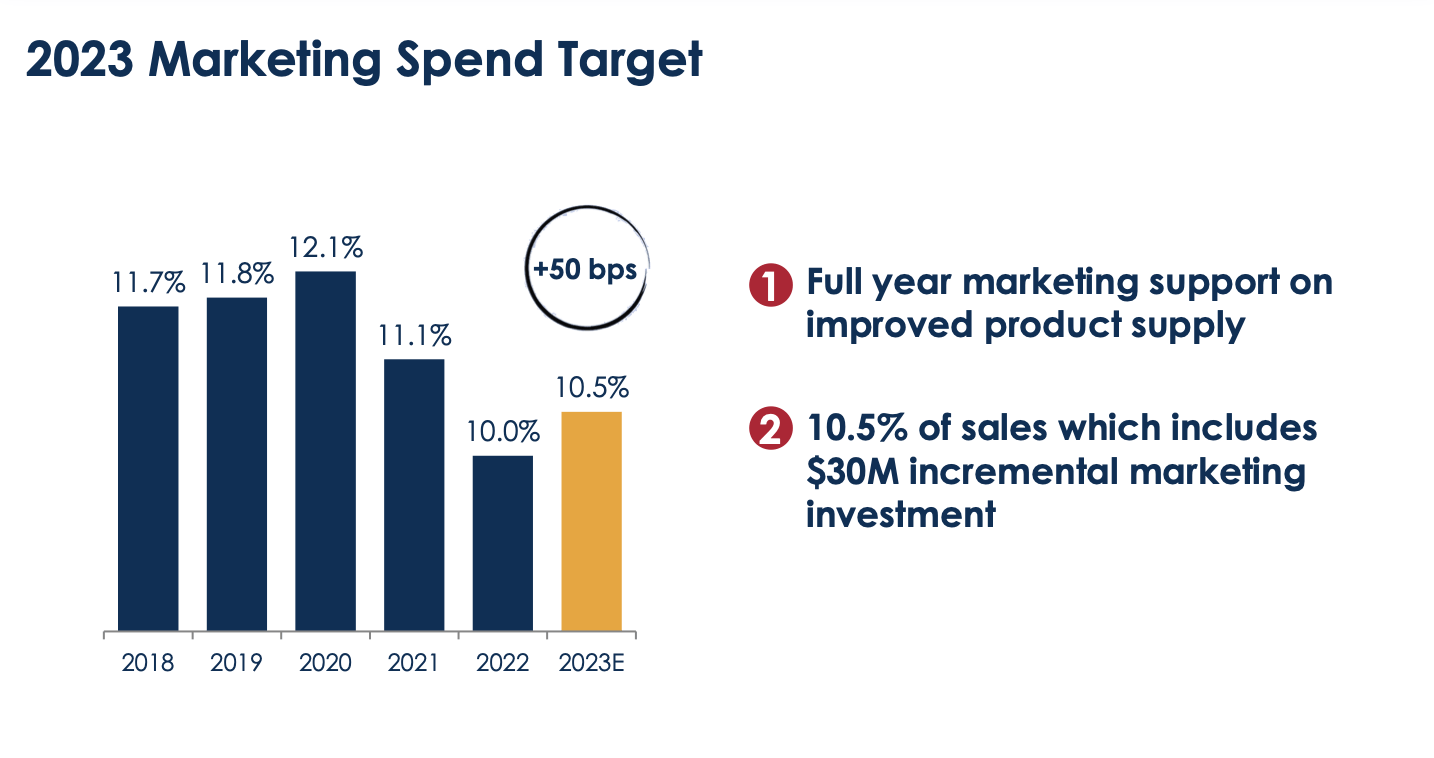

Marketing expenses were $122.3 million, which was $20.4 million higher vs. prior year. Marketing as a percentage of net sales increased 70 basis points to 8.6%. One sign of good cost management was that the company reduced marketing spending in 2022 as supply shortages impacted its ability to meet customer demand, as it is shown in the graph below. But now that supply is normalizing, we assume that marketing expenses will accelerate in the following quarters, and it would not surprise us if they represent more than 10.5% of the revenue, as management expects, in an effort to boost organic sales and increase volume.

Church & Dwight Presentation - dbAccess Global Consumer Conference 2023

{kind=link}

Finally, net income was $203.4 million, or 14.2% of sales. Adjusted EPS grew by 2.4% YoY to $0.85. The company generated $273.1 million in operating cash flow, spent $25 million in CapEx, repaid $255.6 million of debt, and returned $66.3 million to shareholders through dividends.

To be honest, there is very little to dislike about this earnings report. Every major financial indicator is improving, and the company is on track to hit all its 2023 estimates, which is why management raised their full year outlook for sales, EPS, gross margin, and cash flow in the earnings report as well. This explains why the stock has increased 17% YTD, outperforming the SPY.

Balance Sheet

Given that Church & Dwight makes many acquisitions, we should briefly mention the condition of its balance sheet. The company has $202 million in cash, only $18 million in short term debt and $2.4 billion in long term debt. At the end of 2022, 82% of the total debt had a fixed weighted average interest rate of 4.1% and the remaining 18% was constituted of commercial paper issued by the company that had a weighted average interest rate of approximately 4.0% and the term loan due 2024 with a rate of approximately 5.1%. Total debt increased 50% in Q1 2023 versus Q4 2021.

The explanation for this is mainly the HERO acquisition in 2022, which cost $630 million and was financed with debt. HERO is the #1 brand in the acne patch category in the United States and the fastest growing brand in the acne treatment category. This caused the Debt/EBITDA ratio to skyrocket to over 3x, well above historical values.

Although, we are not particularly happy with this situation, we still believe that the company can take on this debt without much problem. It is a good sign that they repaid $255 million of debt last quarter, and we would prefer to see the company deleverage its balance sheet before making new acquisitions. Also, this means that interest expense will hurt the bottom line. In Q1 2023 it increased by 60% versus the prior year.

Biggest Growth Opportunity

Despite being an "old" company, Church & Dwight still has growth opportunities. Apart from acquisitions, we consider the major one international expansion. We believe that there is very little awareness of the brands they have outside the US. I, for example, live outside of the US and never heard of Arm & Hammer before researching the company. This may have to do with the fact that the company has begun to expand internationally only over the past few years (foreign sales are accounted for only from 2017). They have fully operational subsidiaries in six countries (U.K., France, Germany, Canada, Mexico, and Australia) and export our products to over 130 countries through their Global Markets Group (“GMG”).

International sales still represent less than 20% of sales. In Q1 2023, Consumer International net sales were $230.6 million, a 7.5% increase versus the prior year. Organic sales increased 11.6% due to higher volume (6.8%) and higher pricing/mix (4.8%). In the long term, the company targets to grow organic sales 6% per year, much higher than the 2% they target domestically.

Risks

Walmart stands as Church & Dwight's largest client, contributing 24% of their total net sales . The strategic nature of the association with Walmart is highly valuable to Church & Dwight, but we seem highly unlikely that Walmart would cease to carry their products on their shelves. Apart from this, there are no single customers that account for 10% or more of their net sales.

Also, we cannot overlook the fact that competition or damage to the reputation of some of their brands can cause sales to decline. For example, WATERPIK, a power flosser and replacement powerhead brand, has recently experienced a significant decline in customer demand for many of its products, primarily due to lower consumer spending for discretionary products from inflation and a growing number of water flosser consumers switching to more value-branded products. Church & Dwight paid $1 billion for WATERPIK in 2017, and the acquisition has been one of the worst they made yet.

Valuation

Overall, Church & Dwight business is performing better than expected. Earnings expectations are being surpassed and guidance is being raised, which leads to the stock trading higher and sentiment being positive. But despite the good performance of the business, we believe the stock has already priced a lot of future growth. The company trades at 31x Forward P/E, much higher than the last 5-year average of around 26x-27x.

On an EV to FCF basis, the company also seems overpriced relative to the historical measures.

Conclusion

We think that the current valuation is factoring in the majority of future growth and does not represent a good entry point. While we are very optimistic about the business fundamentals and growth prospects, we will wait in the sidelines for a better entry price, ideally under the $75 level.

For further details see:

Church & Dwight: Quality Business Trading At A Premium