CHD - Church & Dwight's Superiority In A Dynamic Consumer Landscape

2023-12-28 06:02:13 ET

Summary

- Church & Dwight is a leading consumer packaged goods company. The company has achieved strong growth in the last decade, with strategic development and M&A driving this.

- When compared to its peers, the business performs extremely well, outperforming on both growth and margins. This is a reflection of its operational superiority and shrewd management of its brands.

- CHD is trading at a premium to its historical average and peer group, which is warranted, but to an extent that does not allow for upside.

Investment thesis

Our current investment thesis is:

- CHD is a high-quality business, owing to its strong portfolio of brands, which are successfully developed over time strategically, and supplemented with M&A.

- Growth has been extremely good for a mature business and margins are high. We see a continuation of its current trajectory.

- Economic conditions and FX movements represent key risks but we are not overly concerned in the medium term given the successful development thus far.

- CHD noticeably outperforms other consumer goods businesses but is expensively priced. We would suggest patience.

Company description

Church & Dwight ( CHD ) is a leading consumer packaged goods company that manufactures and markets a wide range of household, personal care, and specialty products.

The company's portfolio includes well-known brands such as Arm & Hammer, Trojan, OxiClean, and Orajel. With a focus on innovation and quality, Church & Dwight aims to meet consumers' evolving needs and enhance their daily lives.

Share price

CHD's share price has performed extremely well relative to the market, returning over 250%. This is a reflection of its continued positive growth trajectory, at a time when many consumer goods ((CG)) businesses have experienced a slowdown.

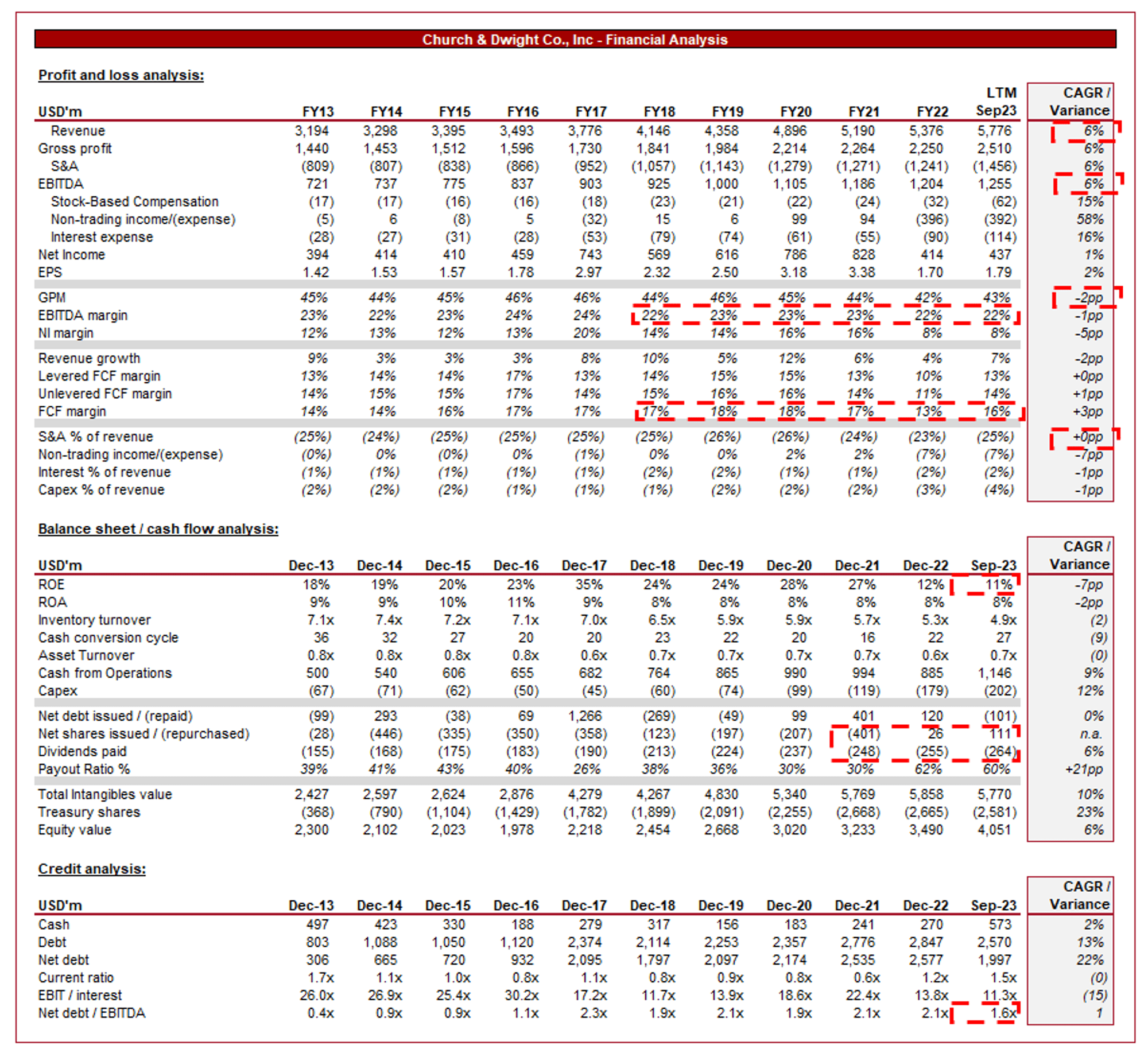

Financial analysis

Church & Dwight Co Financials (Capital IQ)

{kind=link}

Presented above is CHD's financial performance for the last decade.

Revenue & Commercial Factors

CHD has grown its revenue at a healthy 6% CAGR, with no fiscal year below 3%. This is incredible consistency, which is not an easy achievement given the impact of FX and other macro factors that materially distort the results of global CG businesses.

Business Model

CHD operates through three main business segments:

- Consumer Domestic (~77%): This segment offers a diverse range of household and personal care products for the U.S. market, including laundry detergents, oral care, and personal grooming products.

- Consumer International (~17%): Provides similar products to international markets.

- Specialty Products (~6%): Offers specialty chemicals, animal nutrition, and specialty cleaning products.

CHD's products are sold through an extensive distribution network that includes supermarkets, mass merchandisers, wholesale clubs, drugstores, and convenience stores. Additionally, CHD supplies specialty products to industrial customers, livestock producers, and distributors.

The consumer segments (1 & 2) are catered to primarily by CHD's 14 "power brands". These brands operate with high market share within their industries, achieved through brand and product development. This allows the business to price on the higher end, with product quality and marketing allowing for outsized growth.

Operating with a distinct commercial segment is highly beneficial for the business, as it reduces demand volatility and dependency on consumer demand, for what is already a non-seasonal business.

Between these segments and the various product ranges within, CHD has positioned itself well to achieve continued growth in line with global economic development, with scope for outperformance through brand development and product innovation. The business is well entrenched in key consumer markets, with a low risk of downside developments. Given the company's superior market positioning, this is a reasonable expectation in the go-forward period.

Operationally, CHD places a strong emphasis on cost leadership and operational efficiency. By optimizing its supply chain, manufacturing processes, and distribution networks, the company aims to achieve cost savings. This is a key focus for Management as the business is consistently acquiring companies and so requires a strong culture to successfully integrate.

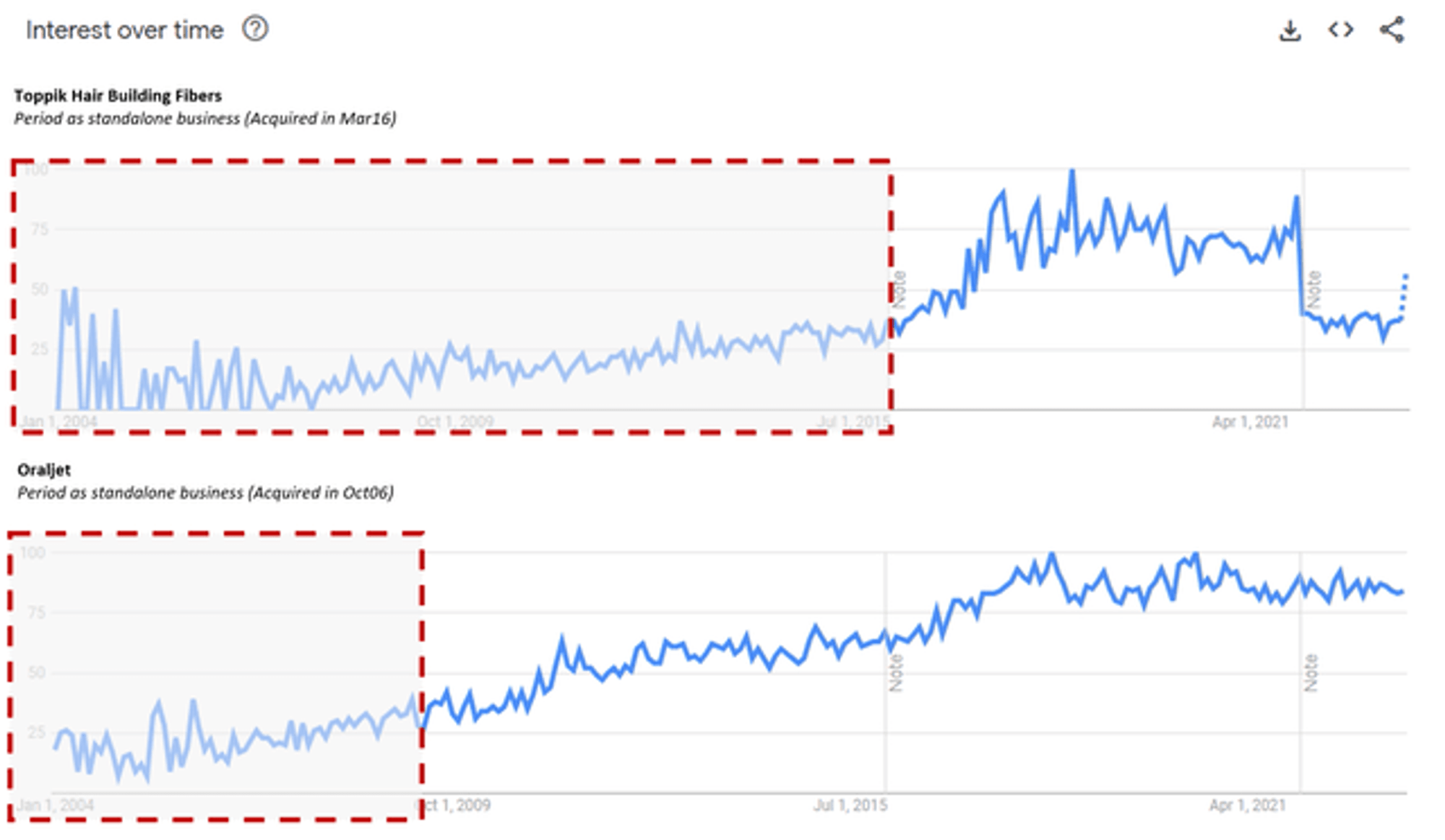

During the last 10 years, CHD has supplemented organic growth with regular acquisitions, with over $4bn spent. CHD has a history of successful acquisitions and partnerships, with the objective of expanding its portfolio and entering new markets. These acquisitions help the company gain immediate access to new customers, distribution channels, and technologies, both enhancing its current businesses and the wider group. CHD's success has come through thorough due diligence, maximizing synergies, as well as achieving growth through its deep expertise.

Although Google Trends is far from a commercially conclusive data source, the post-acquisition trend of the following two examples implies quality value development through its strategic developments.

Toppik and Oraljet (Google Trends)

{kind=link}

Consumer Goods Industry

Consumer goods businesses differentiate themselves through a focus on brands, marketing, innovation, pricing, and the unique properties of their products. CHD faces competition from other CG companies such as Procter & Gamble ( PG ), Kimberly-Clark ( KMB ), Clorox ( CLX ), Reckitt-Benckiser ( RBGPF ), Unilever ( UL ), Haleon ( HLN ), Colgate-Palmolive ( CL ).

Socio-economic conditions and broader marketing have contributed to increased consumer awareness and demand for, personal products used to enhance and improve both healthy and appearance. CHD has positioned itself well to exploit this trend, expanding its exposure. As an example, CHD acquired Flawless, a women's electric hair removal business in 2019.

CHD has been careful with the development of its portfolio, seeking to leverage existing brands and bolt-ons to introduce new variations or extensions, as a means of widening its market share potential. This is a key trend in the consumer industry, as CG companies seek to increase their TAM in order to sustain organic growth.

Tapping into growing consumer markets in developing countries presents opportunities for revenue growth, as economic development and a growing middle class contribute to increased demand for Western products.

Economic & External Consideration

Weaker economic conditions are not necessarily concerning for CG businesses, as their portfolios are positioned to remain resilient due to inelastic demand. Current conditions are not normal, however, due to the extended period of heightened inflation and the elevated rates relative to the last decade. CHD has felt the impact of this, with margins slipping and the need to respond with pricing action.

CHD appears to be on an upward trajectory based on its most recent quarter, however. Growth has increased to double digits (+10.5%), in part due to acquisitions, as well as strong pricing (+2.1%) and volume (+2.7%) gains. While other companies are struggling to maintain positive pricing, CHD is seemingly still successful in doing so without foregoing margins. This is a reflection of its impressive competitive position. This has contributed to a YoY quarterly GPM improvement of 2.7ppts.

Margins

CHD's margins are highly attractive, with an EBITDA-M of 22% and a NIM of 8%. Despite operational improvement, margins have remained flat over the historical period (barring the points discussed above). This suggests the company is likely maxed out of economies of scale, with product mix the only potential value driver going forward.

Balance sheet & Cash Flows

CHD’s distributions have been attractive, when considered in conjunction with an impressive share price performance and M&A (preference for cash utilization). Dividends have grown at a CAGR of +6%, while the company has regularly conducted buybacks.

We are highly supportive of the company’s capital allocation strategy, with ROE consistently above 20% (barring the recent dip due to one-off below-the-line charges). Further, its limited debt usage has allowed interest payments to remain contained, allowing the company the optionality to be greedy in the current market.

Outlook

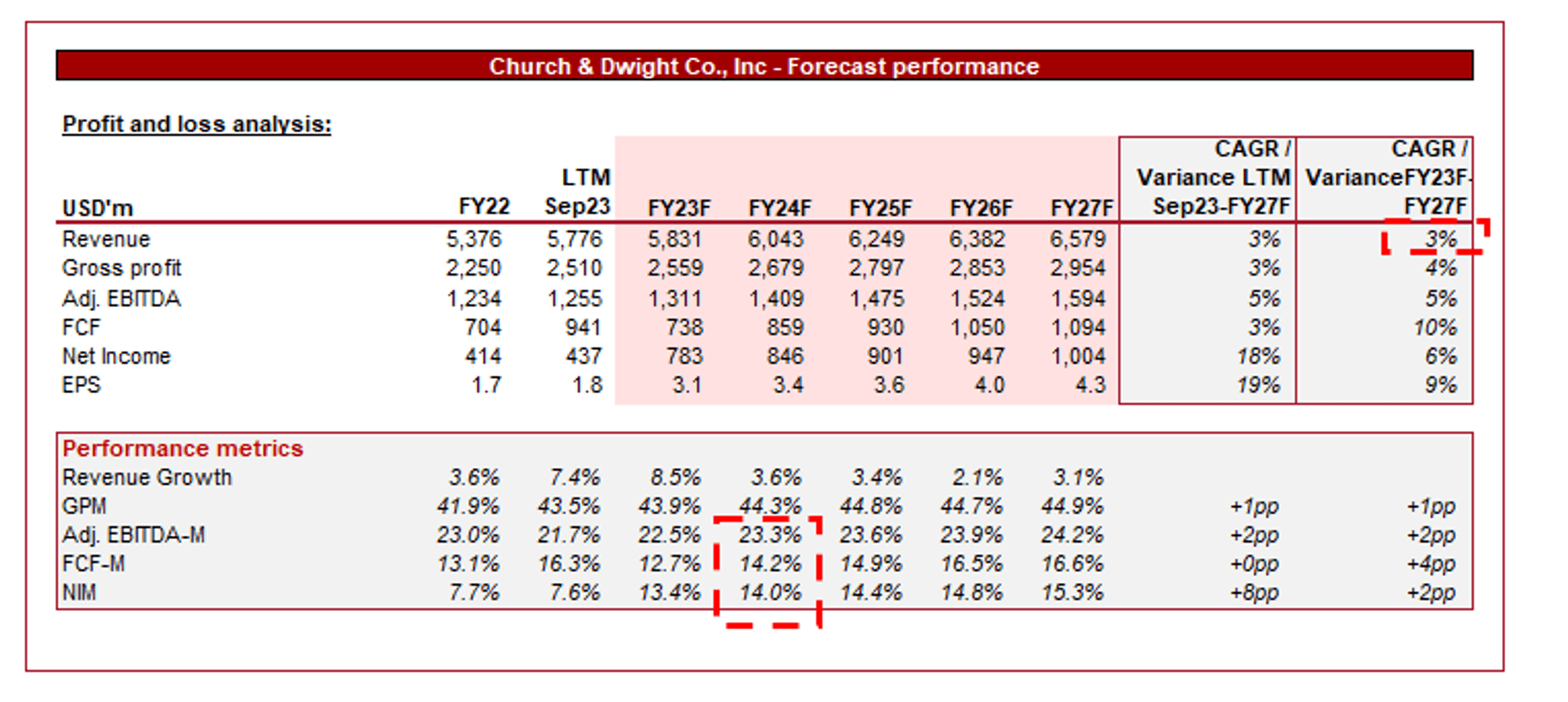

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a forward growth rate of 3%. This is a conservative view of growth in line with the long-term GDP growth rate, as M&A is difficult to price in. We expect CHD to outperform this.

Margins are forecast to improve gradually over the historical period. Given the short-term impact of Covid-19, we expect some immediate improvement over FY23. This said, further improvement is possible but less certain given the lack of clear improvement achieved historically.

Industry analysis

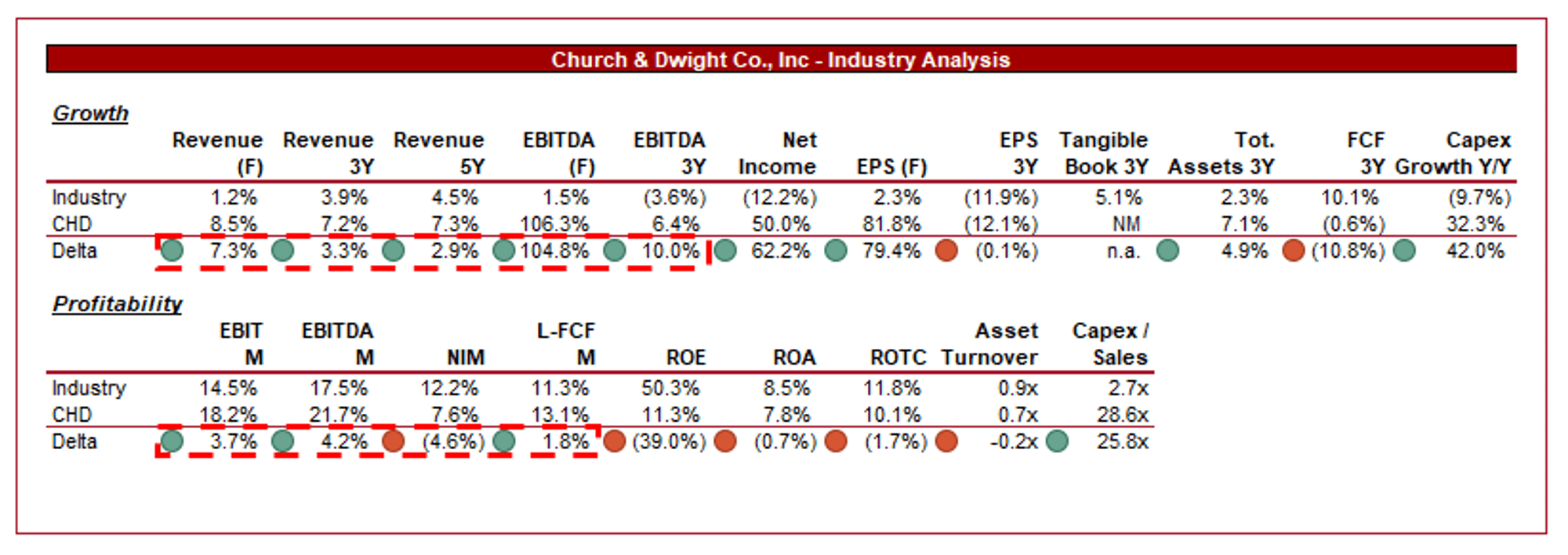

Household Products (Seeking Alpha)

{kind=link}

Presented above is a comparison of CHD's growth and profitability to the average of its industry, as defined by Seeking Alpha (11 companies).

CHD performs extremely well relative to the peer group, with higher growth and superior margins. Given the strong underlying organic growth, this is an impressive performance by CHD, as it would still be above average based on this alone. The company is navigating the macro environment extremely well on a relative basis, best illustrated by its impressive delta on a forward basis. This likely reflects the strength of its commercial profile.

Based on this, we believe CHD should be trading at a premium to its peer group.

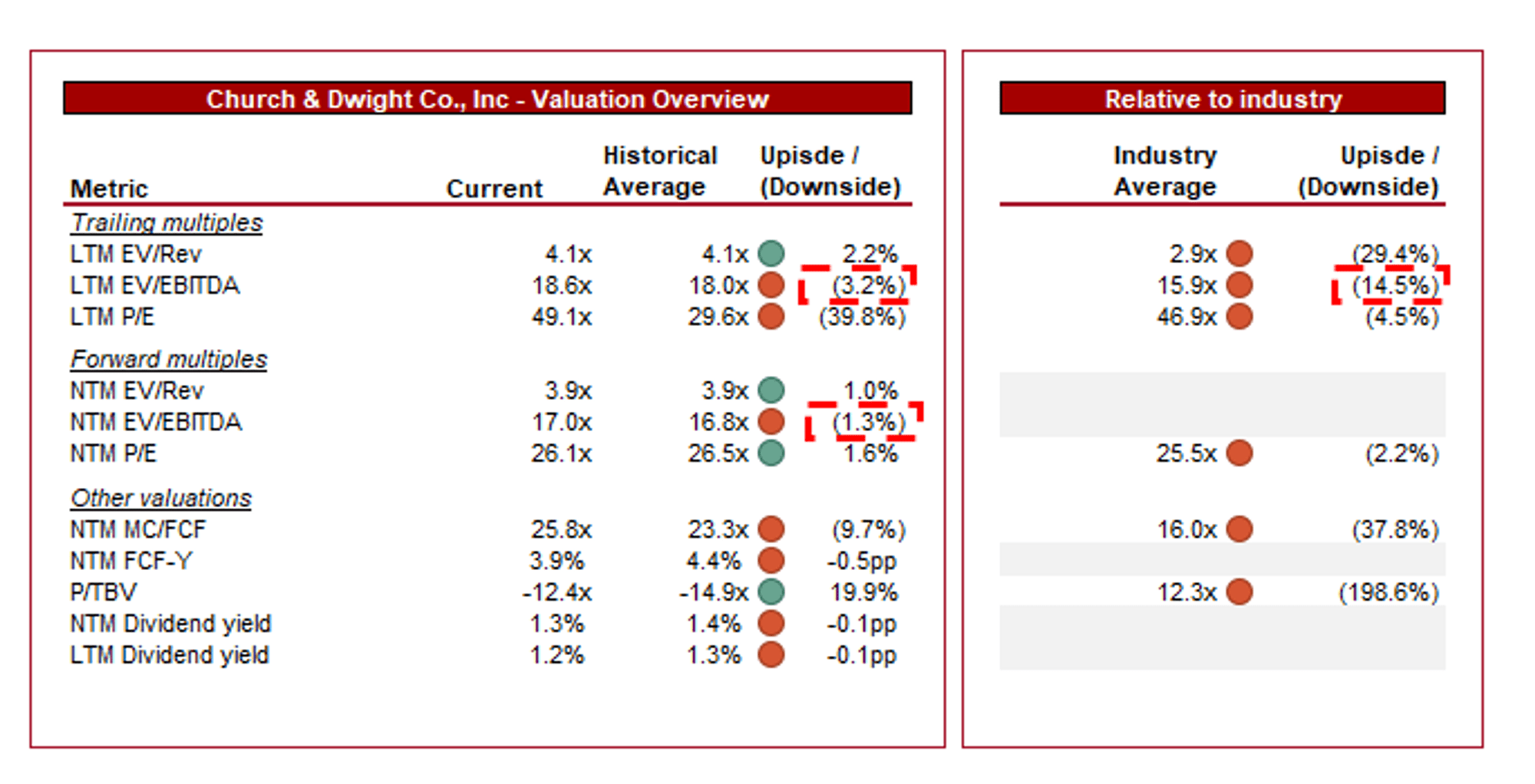

Valuation

{kind=link}

CHD is currently trading at 19x LTM EBITDA and 17x NTM EBITDA. This is a discount to its historical average.

Our view is that CHD should trade at a small premium to its historical average. This is primarily due to its increased scale and portfolio, allowing the business to generate enhanced returns at the same margins.

In addition to this, we believe the business should trade at a premium to its peer group, primarily due to its superior margins but also the wider commercial strength it has exhibited. This is one of the best performing companies in its industry currently, attributable to its business model.

Based on this, CHD is likely trading at a small discount, ~10-15%. This said, we do not think this implies a buy rating yet, primarily due to its below-average FCF yield. Investors have limited reasons for acquiring this company at such as a cash discount, and should be seeking closer to 4.5-5%.

Final thoughts

CHD is an extremely good business, it is no wonder it is a staple in Terry Smith's portfolio. The company owns several strong brands, is strategically successful with development, has a solid approach to M&A, and is operationally efficient. The strength of these factors is reflected in its relative outperformance.

The company is, however, not in a valuation range we would consider attractive. With mature businesses, entry is key and we believe the current price does not imply sufficient upside. We suggest patience until its FCF yield improves.

For further details see:

Church & Dwight's Superiority In A Dynamic Consumer Landscape