URTH - CHW: Imperfect But Not A Horrible Global Fund

2023-11-01 17:57:06 ET

Summary

- Calamos Global Dynamic Income Fund offers a high current yield of 11.49%, making it attractive for income-seeking investors.

- The CHW closed-end fund's recent market performance has been disappointing, with a decline of 11.07% since the date that we last discussed it.

- The fund's asset allocation is heavily weighted towards common stocks, which may not align with its objective of providing current income.

- The fund has more international diversity than the MSCI World Index, but it still gives investors a substantial amount of exposure to the United States.

- The distribution is a wildcard right now because the fund only managed to cover it during the first half of the year because of unrealized gains that may have been erased.

The Calamos Global Dynamic Income Fund ( CHW ) is a closed-end fund, or CEF, from Calamos Investments, which admittedly is not the most well-known fund house among investors. This does not prevent the CHW fund from being a possible source of income for shareholders, as its 11.49% current yield is among the highest in the industry. Indeed, this is a very respectable yield for a dynamic income fund, which are typically able to alter their composition between different types of securities in order to reduce losses during rising-rate environments and generate capital gains during falling rate environments. This fund takes things a step further than most dynamic income funds though, as it also has the ability to include common stocks and other non-debt instruments in its portfolio.

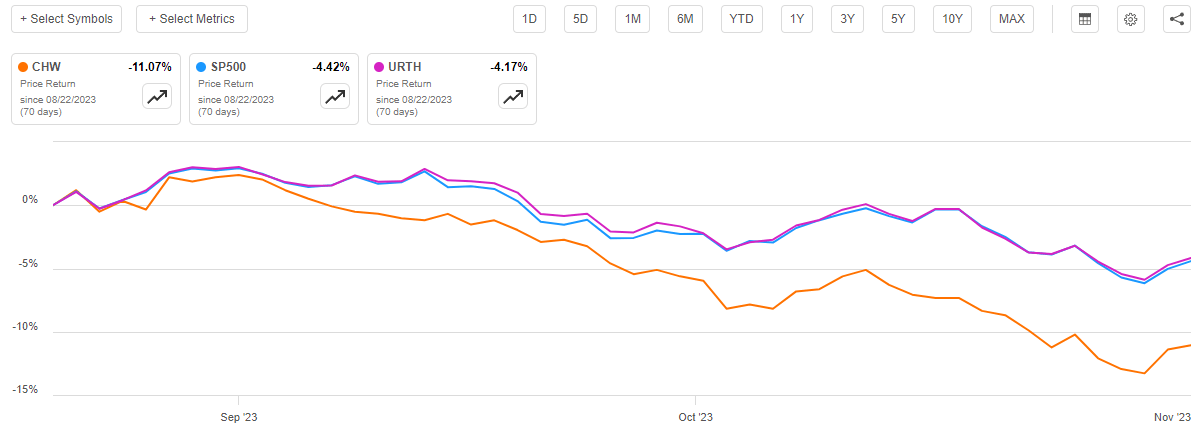

As regular readers may recall, we last discussed this fund in late August 2023. Unfortunately, the fund’s market performance since that time has been very disappointing. As we can see here, the fund’s share price has declined by 11.07%, which is worse than either the S&P 500 Index ( SP500 ) or the MSCI World Index ( URTH ):

{kind=link}

It is also worse than the Vanguard Total World Bond ETF ( BNDW ), which is only down 2.02% over the same period. Thus, the fund’s overall recent performance has certainly left a lot to be desired. Unfortunately, the fact that it has a higher yield than these indices cannot fully close the difference as investors who purchased shares of the fund on the date that my previous article was published are down 9.50% even after considering the distributions paid by the fund.

This is unfortunate as there are some things to like about this fund. In particular, it helps American investors solve one of the biggest problems that they have, which is overexposure to the United States. As I pointed out in a recent article , overexposure to the United States exposes investors to a substantial amount of risks surrounding the economy of a single country. Overexposure to any single nation also makes it more difficult to pursue attractive investment opportunities elsewhere. The Calamos Global Dynamic Income Fund has the ability to invest in assets from all around the world, which allows it to solve both of these problems. However, the poor recent performance is certainly going to put off potential investors so we should engage in a somewhat deeper investigation of this fund and try to determine the causes of this underperformance and how much of a problem they present.

About The Fund

According to the fund’s website , the Calamos Global Dynamic Income Fund has the primary objective of providing its investors with a high level of current income. This is actually a bit surprising considering the strategy that the fund employs. As the website describes,

The Fund seeks to provide a high level of current income with a secondary objective of capital appreciation. The Fund has maximum flexibility to dynamically allocate among equities, convertible bonds, fixed-income securities and alternative investments around the world.

Typically, a fund that has the primary objective of providing current income will focus its investments on bonds or other debt instruments. This is because debt securities are primarily income vehicles due to the simple fact that they have no net capital gains over their lifetimes and all investment returns are in the form of direct payments to the shareholders. Common stocks, on the other hand, are total return vehicles since investors buy them both for income via dividend payments and capital gains that should result as the issuing company grows and prospers.

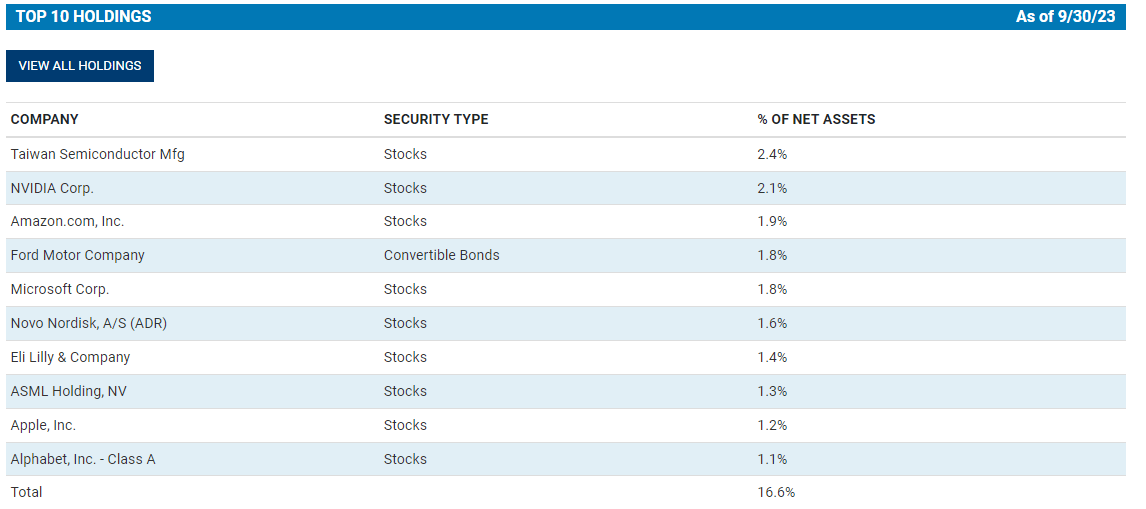

When we consider the differences in return profiles, it is perhaps surprising that the majority of the fund’s assets are invested in common stock. As we can see here, currently 54.17% of the fund’s assets are invested in common stock and the remainder is invested in a combination of convertible securities, traditional bonds, cash, and preferred stock:

CEF Connect

This asset allocation looks much more like a fund that is seeking total return, not current income. After all, the common stocks in the portfolio will provide a combination of income and capital gains, but admittedly not very much income.

We can see this by looking at the dividend yields of the largest stocks in the portfolio. Here are the largest positions held by this fund as of the time of writing:

{kind=link}

Here are the current dividend yields of these stocks:

| Company |

| Current Dividend Yield |

| Taiwan Semiconductor Mfg ( TSM ) |

| 2.09% |

| NVIDIA Corp. ( NVDA ) |

| 0.04% |

| Amazon.com ( AMZN ) |

| 0.00% |

| Microsoft Corp. ( MSFT ) |

| 0.89% |

| Novo Nordisk, A/S ( NVO ) |

| 0.91% |

| Eli Lilly & Co. ( LLY ) |

| 0.82% |

| ASML Holding, NV ( ASML ) |

| 1.05% |

| Apple, Inc. ( AAPL ) |

| 0.56% |

| Alphabet ( GOOGL ) |

| 0.00% |

The Ford ( F ) position is a convertible bond, so its yield is probably relatively decent. We can clearly see though that everything else in the top-ten holdings list has a lower yield than a money market fund right now. In short, if this fund wanted current income, it would be better off just selling all of these stocks and putting the money into two-year U.S. Treasuries. With that said, a few of these stocks have delivered some pretty good gains year-to-date and the fund could sell some of its positions and realize capital gains. That is not current income though, it is current gains. There is a very big difference because current income specifically refers to total investment income and net investment income in a fund’s financial report. Capital gains are not included in investment income.

With that said investors may not really care very much whether the fund is obtaining the money that it pays out to the investors through dividends, interest, or capital gains.

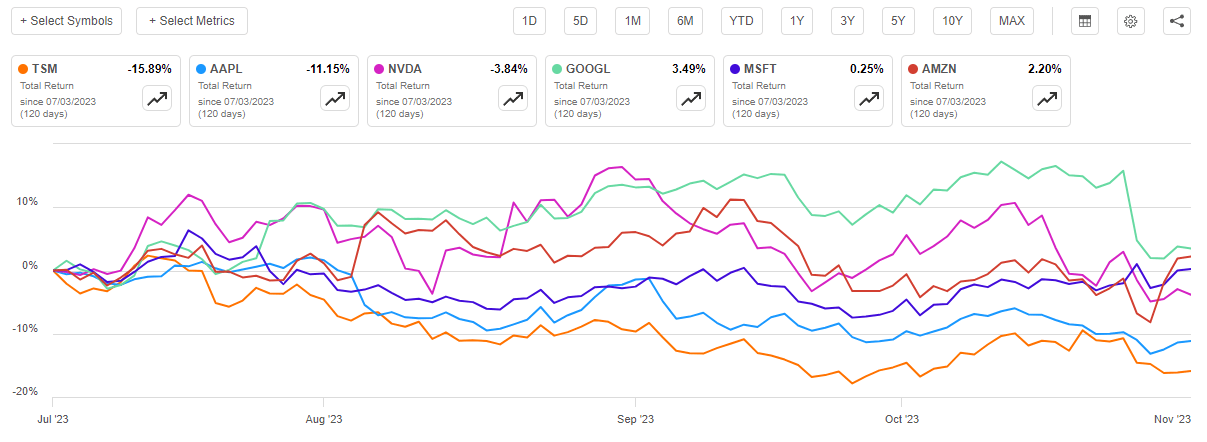

The fund’s largest holdings made a lot of sense during the first half of the year. After all, that was a period of great optimism for the market. Many market participants were widely anticipating that the Federal Reserve would soon pivot with respect to monetary policy and start cutting rates. As a result, they were willing to pay for long-duration assets that would take many years to grow into their valuation. However, the year-over-year inflation numbers started becoming worse starting in mid-July due mostly to energy prices going up. Investors started being less patient and demanding a more rapid return of their money. This caused long-duration stocks, such as many in the technology sector, to either decline or become stagnant. As we can see here, of the major technology stocks listed in the fund’s largest positions, Alphabet has delivered the best performance since the start of July and even it is not particularly impressive:

{kind=link}

To put this in perspective, the U.S. Energy ETF ( IYE ), which tracks a very low-duration sector, is up 4.89% over the same period.

In short, the fund’s current holdings do not make a great deal of sense right now unless interest rates decline. That seems highly unlikely considering that M2 has been relatively static, and the Federal Government is actively competing against the private sector for investor capital. The only real way for inflation to come down is if the Federal Reserve switches to a quantitative easing policy, and it is very hard to see that happening unless the United States enters into a severe recession. This is because anything that gets people borrowing and spending will cause inflation to return. As such, the fund’s holdings may not make a lot of sense in the current environment. Realistically, it should be invested in floating-rate debt securities or other low-duration sectors in order to maximize its returns.

One thing that we can see above is that the fund appears to be heavily invested in the United States. After all, seven of the ten companies shown on the fund’s top-ten holding list above are American firms. However, the fund’s website states that only 53.7% of the fund’s portfolio is invested in American issuers:

Calamos Investments

This is a lower percentage than most global closed-end funds possess, although it is still higher than the actual representation of the United States in the global economy. As of right now, the United States accounts for just under 25% of the global gross domestic product. However, it accounts for 69.88% of the MSCI World Index. Thus, the fund is significantly underweighted to the United States relative to the global market capitalization.

The fact that the United States accounts for such a substantial percentage of the global market capitalization despite only accounting for a much smaller portion of the actual global economic output should immediately set off alarm bells in anyone’s head. After all, this could be a very real sign that there are some risks that the American market in general is substantially overvalued and could have a long way to fall in the event of any economic calamity in the nation. In fact, as of right now, the total market capitalization-to-GDP ratio of the United States is 151.20%. That is well above the long-term average of 100%, although it is not as bad as it was at the start of 2022. However, this does still indicate that the American market is overvalued in general.

Thus, it may be advisable for investors to diversify their assets internationally. This will both help protect their assets against potential future economic problems domestically as well as present the opportunity to take advantage of things that may arise elsewhere in the world. This fund certainly appears to be doing that to a relatively high degree when compared to many other funds and even the global indices. It is not perfect, however, and as such it could still be advisable to purchase an international fund to achieve better global diversification.

Leverage

As is the case with most closed-end funds, the Calamos Global Dynamic Income Fund employs leverage as a method of boosting the effective yield of its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that money to purchase stocks, convertible securities, and bonds from issuers that are located all over the world. As long as the purchased asset delivers a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably higher than retail rates. As such, this scenario will usually be the case. It is important to note though that this strategy is much less effective today with rates at 6% than it was two years ago when rates were basically 0%. This is because the difference between the rate that the fund has to pay on the borrowed money and the return that it can get from the purchased security is much narrower than it once was.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like a fund’s leverage to exceed a third as a percentage of its assets for this reason.

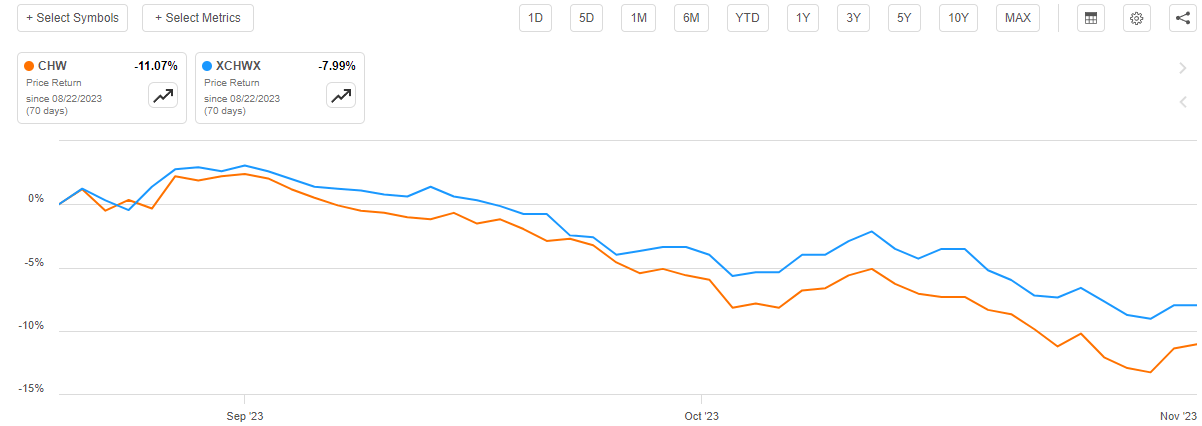

As of the time of writing, the Calamos Global Dynamic Income Fund has levered assets comprising 28.05% of its portfolio. This is quite a bit more than the 26.46% leverage that the fund had the last time that we discussed it, which is a concerning sign. This could indicate that the fund is taking on more debt despite the weakening stock and bond markets. However, we can also see that its net asset value is down 7.99% since the date that we last discussed this fund:

{kind=link}

Thus, static leverage would still result in the fund’s overall leverage ratio going up. This is because the leverage does not go down when assets go down. The fund still owes the same amount of money that it did before, so the leverage represents a higher percentage of the portfolio.

Fortunately, this fund’s leverage still remains at an acceptable level. The risk-reward balance appears to be reasonable here so we should not have too much to worry about.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Calamos Global Dynamic Income Fund is to provide its investors with a very high level of current income. In order to do that, the fund invests in common stocks, preferred stocks, convertible securities, and various other forms of debt securities. In the case of common stocks, the yields are not especially high but many of the other things that this fund can invest in have respectable yields. The fund collects the payments that it receives from all of the debt and hybrid securities in its portfolio and combines it with any capital gains that it manages to realize from the common stock holdings. It then pays out all of this money to its shareholders, net of the fund’s own expenses. This can result in a fairly high yield in certain market conditions.

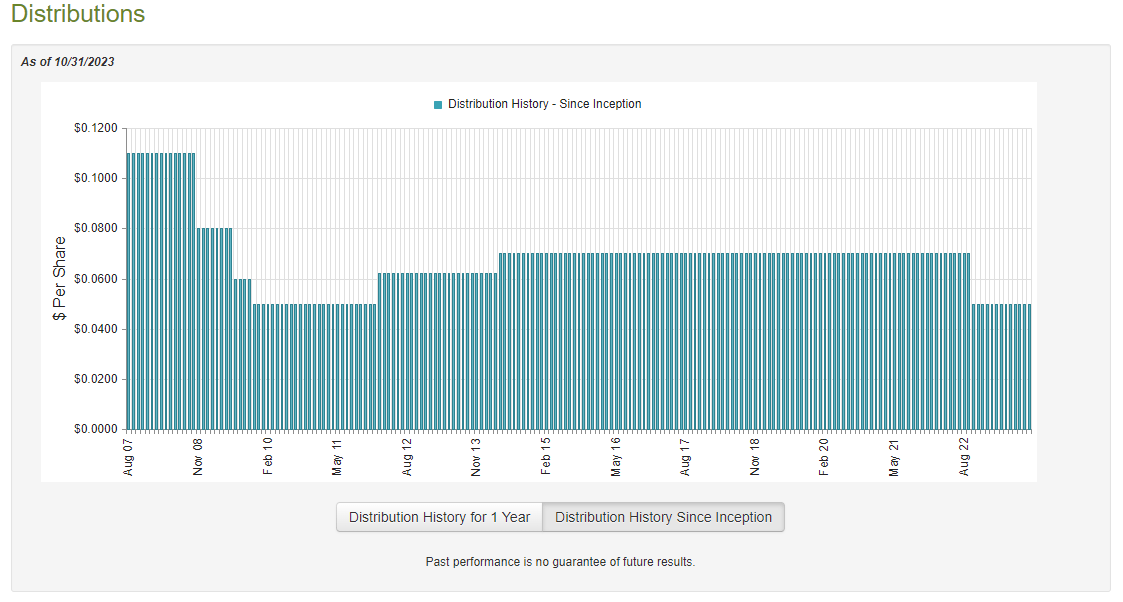

The Calamos Global Dynamic Income Fund currently pays out a monthly distribution of $0.05 per share ($0.60 per share annually), which gives it an 11.49% yield at the current price. This is a much higher yield than just about any index fund, although it is in line with the yield of other leveraged closed-end funds. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years:

{kind=link}

As we can see here, the fund has both raised and cut its distribution several times over the past several years since its inception. Most of the cuts came at a time of stock market weakness, such as the Lehman Brothers collapse, the Great Financial Crisis, and of course the termination of the Federal Reserve’s longstanding easy money policy last year. Thus, the fund’s distribution appears to depend to a certain degree on the overall performance of the American stock market, which makes a lot of sense considering that the fund is weighted most heavily to this particular market. However, it might still prove to be a turn-off for those investors who are seeking a safe and secure source of income to use to pay their bills and finance their lifestyles. After all, we do not really like our ability to support ourselves to be dependent on the performance of the stock market.

It is always a good idea to investigate a fund’s finances before making an investment in it. After all, we do not want to be the victims of a surprise distribution cut since that would reduce our incomes and almost certainly cause the fund’s share price to decline.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on April 30, 2023. As such, it does not include any information about the fund’s financial performance over the past six months. This is unfortunate because it seems likely that the past six months would have delivered a much weaker performance than the period that is reflected in this report. After all, the market during the first half of the year was quite strong and while that undoubtedly presented the fund with the potential to earn some capital gains, if it did not sell its appreciated assets at the right time some of these gains would have been wiped out. In fact, the fact that the fund’s net asset value is down 3.54% since the start of the year suggests that some of its gains from the first half of the year have been wiped out.

During the six-month period that ended on April 30, 2023, the Calamos Global Dynamic Income Fund received $3,669,337 in interest along with $3,523,022 in dividends from the assets in its portfolio. A significant percentage of the interest that the fund received was actually considered to be a return of principal and so is not included in investment income. The fund also had to pay a substantial amount of money in foreign withholding taxes against its income. Thus, it only reported a total investment income of $4,768,806 during the period. That was not sufficient to cover the fund’s expenses and it ended up reporting a net investment loss of $2,351,266 during the period. At first glance, this is almost certainly going to be concerning as the fund clearly did not have sufficient net investment income to pay any distribution, yet it still paid out $19,159,316 to its shareholders.

However, the fund does have other methods through which it can obtain the money that it needs to cover its distribution. For example, it might be able to generate some capital gains by selling appreciated assets into a favorable market. Capital gains are not considered to be investment income for tax or accounting purposes but realized capital gains still clearly represent money coming into the fund. The fund had mixed results in this task during the most recent quarter. The fund reported net realized losses of $3,688,410 but these were more than offset by $53,689,645 net unrealized gains. Overall, the fund’s net assets went up by $28,490,653 during the period after accounting for all inflows and outflows.

Technically, this fund did manage to cover its distribution, but it had to rely on unrealized gains to do it. This could be problematic considering that some of these gains could have very easily been erased by now. As already mentioned, this does appear to be the case considering that its net asset value is down year-to-date. This suggests that the fund may be distributing more than it can really afford. If it did manage to lock in most of its unrealized gains before the market turned then all is well, but there is no guarantee that this is the case. We will unfortunately have to wait until the fund releases its annual report in a month or two before we know for certain where it stands.

Valuation

As of October 31, 2023 (the most recent date for which data is currently available), the Calamos Global Dynamic Income Fund has a net asset value of $5.99 per share but the shares currently trade for $5.26 each. This gives the fund’s shares a 12.19% discount on net asset value at the current price. This is slightly better than the 11.92% discount that the shares have had on average over the past month so overall the price looks quite reasonable. This appears to be a reasonable entry point if you are interested in owning this fund.

Conclusion

In conclusion, the Calamos Global Dynamic Income Fund does not really live up to its name. The name suggests that this is a fixed-income fund, but it is actually a global blended fund that includes both stocks, fixed-income, and hybrid securities from around the world. It does manage to nail down the global component pretty well, as the fund is actually more internationally diversified than the MSCI World Index.

However, a lot of Calamos Global Dynamic Income Fund's holdings consist of long-duration American stocks that are likely to take some bruises if interest rates continue to rise. The fund also might not be able to cover its distribution as net asset value is down year-to-date and the fund relied on unrealized gains to hold its net asset value up during the first half of its fiscal year. The valuation is quite reasonable right now, though, and overall this is a better fund than many of the other options in the market.

For further details see:

CHW: Imperfect, But Not A Horrible Global Fund