ECF - CHY: Looking Expensive Consider Alternatives For The Time Being

Summary

- CHY has had a tough time being highly leveraged and growth investments being out of favor.

- The fund relies heavily on capital gains to fund the distribution, and that could be a catalyst for a premium drop if it's adjusted lower.

- There are some alternatives that one could consider for the near-term until CHY's picture looks better.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 22nd, 2023.

The Calamos team offers a lineup of generally strong convertible funds. It's been much tougher in the last year as they've fallen out of favor, with growth stocks taking a hit. However, that hasn't stopped the Calamos Convertible and High Income Fund ( CHY ) from surging to an almost 10% premium recently. That puts it where investors should consider selling.

Since our last update , the fund has provided some relatively strong returns. However, the best results came in on a total share price return basis due to the fund's premium surging higher. As we can see, most of this came in just the last few weeks.

Ycharts

CHY Basics

- 1-Year Z-score: 1.76

- Premium: 9.33%

- Distribution Yield: 9.90%

- Expense Ratio: 1.34%

- Leverage: 39.06%

- Managed Assets: $1.307 billion

- Structure: Perpetual

CHY " seeks total return through a combination of capital appreciation and current income." They attempt to achieve this through "investing in a combination of convertibles and high yield bonds." They highlight that it "provides an alternative to funds that invest exclusively in investment-grade fixed-income instruments, and it seeks to be less sensitive to interest rates by investing in lower duration asset classes."

The fund carries a high amount of leverage, which adds to the fund's volatility. In the last year, that certainly meant much lower relative results than it otherwise would have. It also means that when including the fund's leverage expenses, it comes to 2.45%.

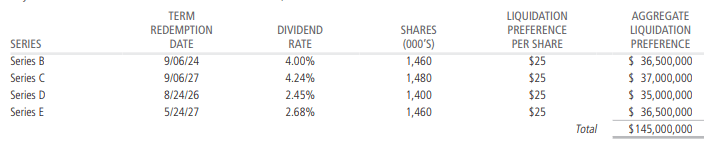

However, while some funds are subject to exploding leverage costs at this time, Calamos has some of the fund's debt at fixed rates. This is primarily through their Mandatory Redeemable Preferred Shares.

The portion that is through a credit facility was listed at $365 million. On that portion, the interest rate is OBFR plus 0.80%. At the end of their fiscal year , that worked out to 3.86%. For some context, in the previous semi-annual report , the average interest rate was listed as 0.61%.

At that time, it was still beating out the cost of some of the preferred leverage the fund utilizes. However, with interest rates continuing to rise, we are at the point where the fixed-rate preferred is more preferential. As a point, OBFR was listed at 4.32% today . Including the 0.80% spread, we are now topping over 5%. Unfortunately, that 5% is the largest part of their leverage being utilized.

{kind=link}

CHY Preferred Leverage (Calamos)

In the last fiscal year, they deleveraged in the form of reducing some of their outstanding loans. They had $435.4 million outstanding at the end of fiscal 2021, and now it comes in at $365.4 million. Due to the high utilization of leverage and the volatile year, it's quite possible that this could have been some forced deleveraging.

Performance - Premium Helps Benefit This Fund

With higher costs, the fund's performance can suffer. Add to that, a weak performance for growth investments - the primary issuer of convertible debt - and you are met with a fund that has performed quite poorly in the last year. Below is comparing the fund to iShares Convertible Bond ETF ( ICVT ) and iShares iBoxx High Yield Corporate Bond ETF ( HYG ). These are non-leveraged ETFs; I included HYG because CHY has a meaningful weighting to high-yield bonds as well.

Ycharts

In the last year, CHY's total share price returns have topped these two ETFs' results. However, that simply came from the premium that popped up recently. On a total NAV return basis, the results were quite poor. Thanks to the leverage the fund employs, the results were worse than they otherwise would be.

Over a longer period of time, results have been better for CHY, where it easily topped the results seen from HYG.

Ycharts

The fund often enjoys trading at a fairly low discount through most periods. However, to put the latest premium into perspective, below we can see the decade average discount comes to 2.26%.

Ycharts

With CHY trading at such premiums, there are some alternatives that an investor could consider based on better valuation. Some of the alternatives could include Bancroft Fund ( BCV ) or Ellsworth Growth and Income Fund ( ECF ). The iShares Convertible Bond ETF ( ICVT ) could also be a consideration. As an ETF, it doesn't have to deal with the same types of discounts/premiums that CEFs contend with.

Over the short term, the results of these three convertible-focused CEFs have been quite similar on a total NAV return basis.

Ycharts

Even on a longer-term basis, these funds have put up similar results. In fact, BCV and ECF have outperformed on a total NAV return basis. Again, thanks to the premium push lately from CHY, it has topped them.

Ycharts

So all else being equal, it makes much more sense to divest CHY, at least temporarily, for one of these other funds.

Distribution - Lack Of Gains

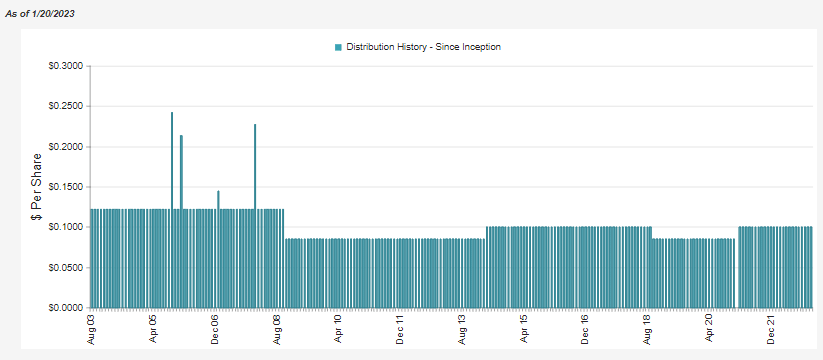

Calamos does a good job of keeping their funds paying fairly steady distributions. They aren't announcing changes every quarter but will adjust when necessary.

{kind=link}

CHY Distribution History (CEFConnect)

Unless we start to see some material rebound, we could be due for another lower adjustment, however. This is because the fund relies significantly on capital gains to fund the distribution. The yield on convertible debt is 0% in some cases.

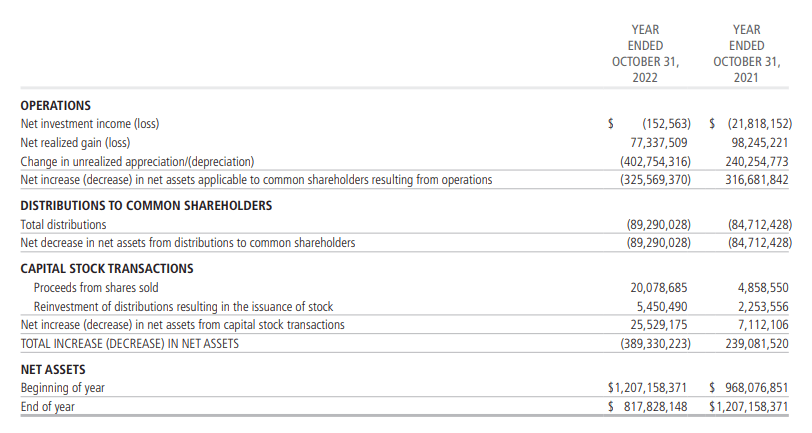

Here is a look at the last annual report. They showed a negative NII figure. That means that the fund didn't have any income left over after expenses.

{kind=link}

CHY Annual Report (Calamos)

To be fair, that doesn't tell us the whole story in this scenario because amortization reduced the fund's total investment income.

{kind=link}

CHY Total Investment Income (Calamos)

That significantly reduced what income was left. However, even if we added that ~$12.7 million back in, the distribution coverage was still clearly lacking, with coverage coming in at around 14%.

Thus, why the other ~$76.6 million would need to be funded through capital gains, which they were able to generate for the year. At the same time, though, the fund had over $400 million in unrealized depreciation. That's why I believe that a cut could be the next logical adjustment for the fund unless we start getting a meaningful rebound in the markets.

A distribution cut alone doesn't make a fund a sell or a buy. With the fund at such a large premium, a cut could immediately send the fund lower, as we've seen historically.

For tax purposes, this fund generally characterizes the distributions as ordinary income. In 2021, as an example, the fund's entire distribution was identified as ordinary income. That was even despite the fund producing -$21.8 million in NII.

That could mean it would be best for a tax-sheltered account. However, long-term capital gains were classified as the majority of the distribution in the last year.

{kind=link}

CHY Distribution Tax Character (Calamos)

CHY's Portfolio

The portfolio turnover rate last came to 36%, and the prior fiscal year showed 44%. This means that the fund isn't overly aggressive in buying and selling but isn't stagnant, either.

The duration of the portfolio comes to 2.6 years. That means that, in theory, for every 1% increase in interest rates that the fund's portfolio could fall 2.6%. Convertible bonds aren't overly interest rate sensitive, as highlighted by this figure. This becomes more true the lower the yield . So when there is a zero coupon bond, it would correlate almost exclusively with the underlying equity price.

A broad overview of the fund shows us that the majority of the fund is invested in convertibles. Then we have another roughly 25% in high-yield corporate bonds. The remainder of the assets is invested in relatively insignificant weightings of everything else.

This hasn't changed drastically in the last quarter, nor has it changed for the couple of years I've been following the fund. So it makes it quite predictable what the composition of the fund generally is.

CHY Asset Allocation (Calamos)

The sector weightings show us that the fund is heaviest in tech securities. This is quite natural as tech makes up a fairly sizeable amount of what could be considered growth. However, it isn't exclusively tilted towards tech and, for the most part, could be considered rather diversified. This also hasn't changed significantly in the latest quarter or the last couple of years.

CHY Sector Weightings (Calamos)

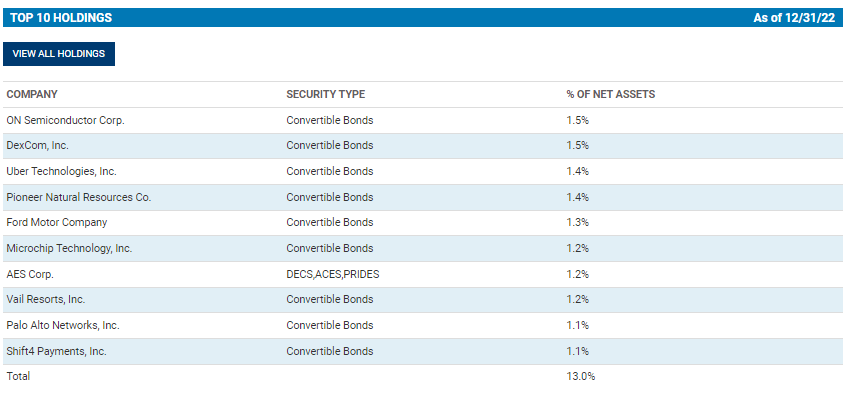

This sort of diversification carries over to the individual positions in the fund as well. The top ten make up only around 13% of the portfolio.

{kind=link}

CHY Top Ten Holdings (Calamos)

One of the key changes here is that Tesla ( TSLA ) is no longer a top holding. It had been a staple for the last couple of years. Most updates would have it in the top ten, if not the number one position. Of course, that necessarily isn't a good thing because TSLA was the poster child for overvalued growth plays.

The $2,120,000 principal amount of 2% TSLA convertible is still in CHY's portfolio. It was simply due to the drop in the price of TSLA that saw the value go from nearly $30 million to $23.3 million in the six-month period between the semi-annual and annual reports.

Ycharts

There has been some recovery since, which would certainly benefit CHY and its shareholders. Then a silver lining could also be that they sold some of their TSLA position sometime since the end of fiscal 2021 . At that time, they held in principal $4,790,000 for a value of nearly $86 million. So they realized some of those gains, which helped contribute to this year's significant realized gains.

Conclusion

CHY is an attractive convertible and high-yield bond fund. They have a low correlation with interest rates which was important for 2022. However, they have a high correlation with growth investments, and those were a horror show throughout the last year.

At the same time, the fund's premium has recently been pushed to significant levels. That indicates that it could be time to cut CHY loose and revisit it in the future. BCV, ECF or ICVT could be short to medium-term alternatives until CHY becomes a better value.

For further details see:

CHY: Looking Expensive, Consider Alternatives For The Time Being