ECF - CHY: Premium Comes Down To A More Reasonable Level

2023-05-15 02:49:26 ET

Summary

- CHY is invested mostly in convertibles but also incorporates a meaningful amount to high-yield bonds, with smaller allocations in other instruments.

- The fund was trading at quite an extended premium earlier in the year, but that bubble has since popped.

- There could be some more downside due to the fund's valuation, but it is certainly looking a lot more tempting these days.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 13th, 2023.

Calamos Convertible & High Income Fund ( CHY ) has come down to a much more attractive valuation than where we were just a short while ago. Similarly, its sister fund, the Calamos Convertible Opportunities & Income Fund ( CHI ) had a similar trajectory in terms of its overvaluation. We recently provided an update on that fund, that while the premium came down , it certainly wasn't a great deal yet.

CHY has come down to only trading at a slight premium, which isn't completely out of line historically. Thus, it could present a better alternative to CHI for some impatient investors that must buy. It could be worth considering if you have the capacity to average down at a later time.

CHI remains at a higher premium relative to its CHY sister, while both funds have delivered similar results over time. Therefore, choosing between the two can easily come down to which is the cheapest from a valuation standpoint. However, while CHY is the better-looking fund at this point, waiting for a discount could still be the best play.

CHY Basics

- 1-Year Z-score: -0.58

- Premium: 2.61%

- Distribution Yield: 11.29%

- Expense Ratio: 1.34%

- Leverage: 37.82%

- Managed Assets: $1.284 billion

- Structure: Perpetual

CHY " seeks total return through a combination of capital appreciation and current income." They attempt to achieve this through "investing in a combination of convertibles and high yield bonds." They highlight that it "provides an alternative to funds that invest exclusively in investment-grade fixed-income instruments, and it seeks to be less sensitive to interest rates by investing in lower duration asset classes."

The fund carries a high amount of leverage, which adds to the fund's volatility. In 2022, that certainly meant much lower relative results than it otherwise would have. In 2023, we've seen a bit of a rebound, but nothing to boast about. This also means that when including the fund's leverage expenses, it comes to 2.45%.

As interest rates have been rising, this has negatively impacted the borrowing costs for CHY. Their credit facility is charged at an interest rate of OBFR plus 0.80%. Fortunately, some of this is offset with the fund's fixed rate preferred.

CHY Preferred Leverage (Calamos)

One thing we noted previously was some deleveraging in the fund. This was once again a factor in the fund as they took down borrowings in the credit facility at fiscal year-end from $365.4 million to $340.4 million as of the data available on April 30th, 2023.

Performance - Attractive Results, Premium Isn't Outrageous

When looking at CEFs, it really isn't about the fund's absolute discount or premium in terms of where it stands today. Historically speaking, funds can tend to mean revert back to longer-term averages. That is to say, a CEF that trades at a deep discount likely continues to trade at a deep discount perpetually. Some funds at elevated premiums tend to trade at premiums.

The caveat for the funds at premiums tends to be that it is as long as they are paying reasonable distributions and that those distributions don't end up getting cut. In those cases, we often see funds at premiums come back down to earth relatively quickly. That's a topic we've touched on previously .

The fund's distribution is a bit questionable for CHY at this time, but the fund doesn't also exhibit an extraordinary overvaluation either. This is because CHY historically trades at a fairly shallow discount. There are exceptions during times of panic, such as in 2016 and Covid, but the fund isn't trading excessively relative to its longer-term average.

Ycharts

The anomaly was when it spiked to a premium earlier this year, which is also what CHI had experienced. CHI continues to trade at a higher premium of over 7% too. This is precisely why my previous coverage of CHY was cautioning on the fund's premium and laid out a couple of "alternatives for the time being." Since that update, the declines have been quite sharp. A good portion of this was the fund's premium going from 9.33% to the latest 2.61% premium. Other factors, such as the banking crisis, were obviously playing a role in pressuring the fund's results too.

CHY's Performance Since Previous Update (Seeking Alpha)

As mentioned in the opening, CHY and CHI trade almost identically, so whichever is the lowest valuation at the time can make a lot of sense. Here's a look at the last decade of performance, looking at both fund's total share price and total NAV returns to highlight this fact.

Ycharts

All that said, the alternatives of Ellsworth Growth And Income Fund ( ECF ), Bancroft Fund ( BCV ) and iShares Convertible Bond ETF ( ICVT ) could still be worth considering.

BCV and ECF trade at substantial discounts, and ICVT, being an ETF, trades mostly at its NAV. Long-term historical results show that you wouldn't be given up potential upside for a swap into these funds either, at least if history is any guide. The usual caveat of history isn't a guarantee of future results is applicable.

Ycharts

ICVT would have actually delivered stronger results during this period too. However, it would have limited the amount of time we could look back for the chart as it was incepted in 2015. Additionally, with a sub-2% yield, the distribution yield of the CEFs is likely to be more appealing for income investors. Of course, with the idea that ICVT pays out only income yield while CEFs pay out distributions of income, capital gains and return of capital.

Also, exploiting the discounts/premiums on CEFs makes a lot of sense too. Finally, including ICVT would give a pure play convertible exposure, while the CEFs include other assets such as equities and high-yield bonds. In CHY's case, high-yield bonds represent a meaningful weighting to the fund.

Since the previous update, when I initially mentioned the alternatives, we can see that CHY was the laggard in terms of total share price returns. BCV only marginally outperformed but showed a reduction in losses regardless. That was even though the fund's total NAV returns were superior by falling less than the other two. This can help highlight why valuations matter, it doesn't always occur so swiftly, but the banking crisis volatility could have been playing a role too.

Ycharts

Distribution - Attractive Yield, But Cautious

We don't have any new financial data to review since our previous update, but a couple of things are worth reiterating. That includes the more recent deleveraging, which has taken place since the fiscal year-end.

The deleveraging we saw in the prior year and the deleveraging we saw more recently since the fiscal year-end hurt the fund's distribution coverage. This is because these are assets that can no longer generate potential returns. However, the borrowing costs also rising leads to hurting coverage too, as well as a lack of capital gains.

So there really are a lot of headwinds facing the distribution for this fund. These are the types of pros and cons that investment managers have to consider before utilizing or reducing leverage.

As we saw previously, the fund will need to cover its distribution largely from capital gains instead of income from the fund.

CHY Annual Report (Calamos)

In fact, due to amortization, the fund hasn't been generating any net investment income for shareholders in recent years.

That [amortization] significantly reduced what income was left. However, even if we added that ~$12.7 million back in, the distribution coverage was still clearly lacking, with coverage coming in at around 14%.

Thus, why the other ~$76.6 million would need to be funded through capital gains, which they were able to generate for the year. At the same time, though, the fund had over $400 million in unrealized depreciation. That's why I believe that a cut could be the next logical adjustment for the fund unless we start getting a meaningful rebound in the markets.

A distribution cut alone doesn't make a fund a sell or a buy. With the fund at such a large premium, a cut could immediately send the fund lower, as we've seen historically.

As we also noted previously, the fund's distribution was elevated. The yield is even higher now, but the fact that its premium has come down sharply should mean a relatively reduced reaction should a cut occur. Calamos doesn't have a history of cutting distributions too frequently, but we know that coverage hasn't been improving with deleveraging occurring. The YTD results for the fund also haven't inspired too much confidence for a significant rebound.

Ycharts

While the S&P 500 and Nasdaq have been showing substantial rallies this year, that's the result primarily of the mega-cap tech names.

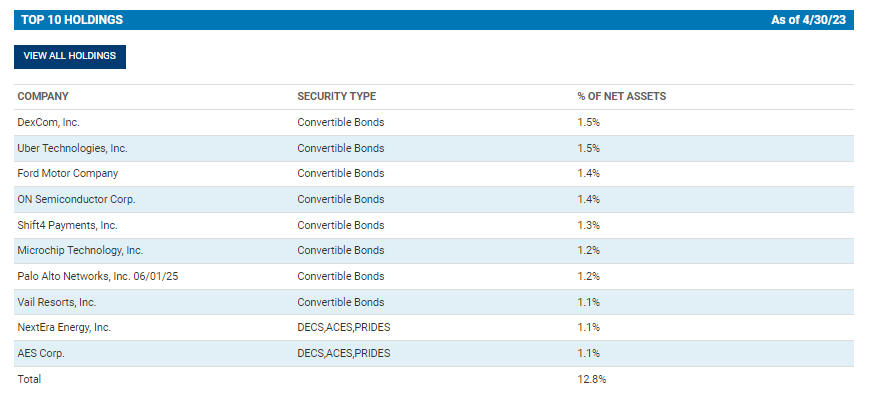

CHY's Portfolio

Speaking of tech, while tech is the largest sector allocation of CHY, it isn't overwhelmingly so. In fact, since our last update, they cut tech's allocation fairly meaningfully from the 23.2% it was at coming to the end of December 2022. Consumer discretionary, communication services and financials received some of the boosts, as they were previously 13.3%, 10.5% and 6.9%, respectively.

CHY Sector Weightings (Calamos)

The increased allocation to financials, in particular, is fairly peculiar considering the banking crisis. Potentially they were picking up some good deals while the sector was down, but this is where trusting management comes in when investing in an actively managed fund.

Their latest quarterly commentary mentioned the banking crisis but didn't necessarily mention if they were looking to take advantage of opportunities there. Instead, they mentioned holding technology, healthcare and consumer discretionary sectors at nearly 50% of their portfolio and why they liked that area of the market.

From an economic sector perspective, our heaviest exposures reside in the information technology, health care and consumer discretionary sectors, which collectively represent approximately 49% of our holdings. Reflecting our strong focus on bottom-up company analysis, we favor companies that are executing well despite macro uncertainties; are considered best-in-class; and are long-term winners benefiting from lasting secular themes such as cybersecurity, automation and productivity enhancements. These long-term themes serve as a beacon in turbulent times, such as now, and help us identify innovative firms whose valuations will most likely be rewarded over time. Many of these are growth firms that have shifted focus from growth-at-all-costs to improving margins, generating free cash flow and increasing profitability. Holding these names should prove advantageous as higher-quality growth becomes scarce as the era of free money ends.

CHY doesn't carry any of the mega-cap tech names that have been getting most of the love through 2023 so far in their top ten. This is really why we are seeing more flattish results on a YTD basis in terms of total NAV return. Most of the market hasn't been experiencing the lift that the handful of tech names have been getting making the 'market' appear as if it's rebounding in 2023.

{kind=link}

Overall, they are quite diversified, with no position making up any significant portion of their portfolio relative to another.

Tesla ( TSLA ) had been a staple in the top ten holdings, but we noted previously they reduced their TSLA stake toward the end of the fiscal year. Their last total holding list available as of the end of March 2023 shows no TSLA position at all. In fact, going back to their latest N-PORT available for the period ending January 2023, TSLA was no longer a position either.

The fund is heavily invested in convertibles (65.99% allocation), but it still carries a meaningful weighting to high-yield corporate bonds (25.69% allocation.) The rest of the portfolio is then spread amongst negligible amounts of other various instruments. Weightings around these allocations were fairly similar in our previous update, even as we see shifts in the underlying sector allocations.

CHY Asset Allocation (Calamos)

Conclusion

CHY has come down to a more reasonable valuation. A more patient investor could still wait for an even better opportunity. A longer-term investor probably wouldn't be too worried about getting the absolute best price, so they could consider a dollar-cost average approach. After all, in the last few years, a discount has been quite elusive. However, history shows it is at least possible for this fund as it tends to get hit in times of panic, just as other CEFs do.

While Calamos doesn't adjust distributions too often, there could be some chance for a reduction which could push the fund to a discount. On the other hand, the fund isn't so grossly overvalued as it was that any cut could see a relatively muted decline.

To sum up, CHY has been looking much better regarding valuation since our last update. That said, I'd still be looking to favor some alternatives, such as ECF or BCV, for now.

For further details see:

CHY: Premium Comes Down To A More Reasonable Level