F - CHY: Some Good Qualities But Be Cautious

2023-10-16 10:06:45 ET

Summary

- The Calamos Convertible & High Income Fund offers a high level of current income with a 10.69% yield without sacrificing upside potential, making it attractive for retirees.

- The fund has performed well compared to the S&P 500 Index recently and has a portfolio weighted towards convertible bonds.

- The fund employs leverage to boost returns, but its high level of debt and recent decline in net asset value raise concerns.

- The fund managed to cover its distribution in the first half of this fiscal year, but it is uncertain whether it will be able to sustain this over the second half.

- The fund is currently trading at an incredibly high valuation, so it might be best to wait for a better entry point.

The Calamos Convertible & High Income Fund ( CHY ) is a closed-end fund, or CEF, that is designed to provide a high level of current income that can be used to pay bills or finance other expenses. This is increasingly something that many retirees need in the face of the high levels of inflation that many nations have been experiencing over the past few years. The fund’s current 10.69% yield speaks well to its capabilities as a source of income, as that is a much higher yield than many other assets in the market possess.

Unfortunately, many times a double-digit yield may be a sign that the fund is paying out more than it can actually afford based on the performance of the assets in its portfolio. While this is not as big a problem as it used to be, since the market has been offering higher yields on just about everything than it did over the past decade, we still want to analyze the fund’s finances in order to determine how sustainable the current payout is likely to be.

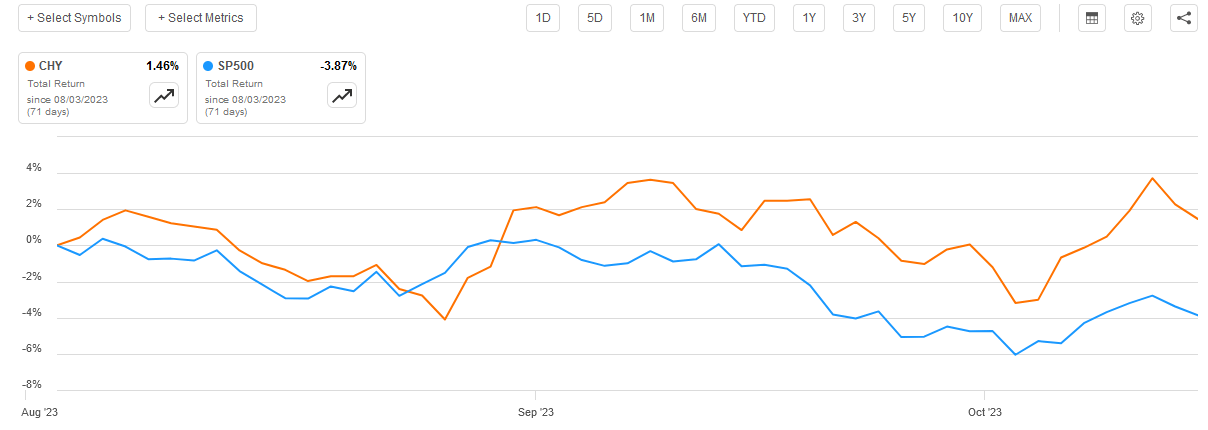

As regular readers may recall, we last discussed this fund in early August. Its performance since that time has been reasonably impressive as investors in the fund have actually realized a positive total return. This is better than the S&P 500 Index ( SP500 ) delivered over the period, as index investors have been handed a loss:

{kind=link}

The fund also managed to deliver a higher total return than the index over the trailing full-year period. This is partly because it benefited somewhat from the market’s increasing acceptance that high interest rates may be with us for a considerable amount of time. As I discussed in a previous article , junk bonds have been one of the few assets that have really benefited from this over the past two months. This fund is more than just junk bonds though, so that will affect its performance compared to a typical junk bond fund.

About The Fund

According to the fund’s website , the Calamos Convertible & High Income Fund has the stated objective of providing its investors with a high level of current income. The fund aims to achieve its objectives by investing in a combination of convertible bonds and junk bonds. As we can see here, the fund’s portfolio is currently more weighted to convertible bonds than it is to junk-rated debt, as 63.74% of the fund’s assets are invested in convertible bonds:

CEF Connect

This makes this one of the few convertible bond funds that is actually more heavily weighted to convertible securities than it is to traditional bonds. That is not a bad thing though, as convertible securities are a very good investment for income-seeking investors, but they can be difficult to access. As I pointed out in my previous article on this fund:

A convertible bond is simply a bond that can converted into equity of the issuing company after certain conditions are met. Thus, it basically provides both the safety and income potential of a bond combined with the upside potential of common stock. These securities are frequently issued by start-ups or similar companies that do not have the cash flow to obtain regular debt financing but may have the potential for substantial returns a few years down the road.

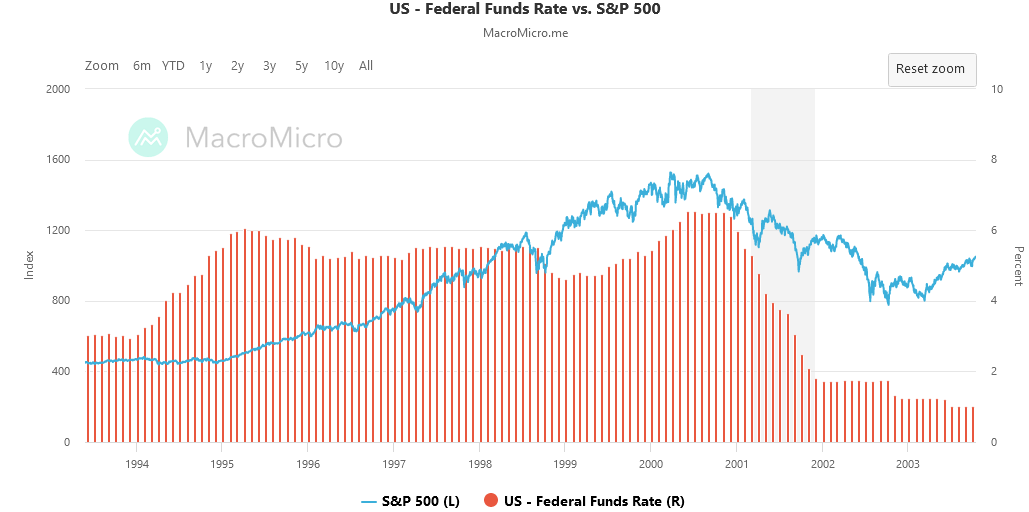

I have always liked these securities for income-focused investing because they provide the yield of fixed-income securities, but the investor does not need to sacrifice the upside potential of common stock to obtain this income. This is a very appealing trade-off, particularly in an inflationary environment since the upside potential of these securities (following the conversion) can help overcome the decline in purchasing power that an ordinary fixed-coupon bond would have. In addition, these securities might hold up better in a rising-rate environment than a fixed-rate bond because the common stock performance of the issuing company has an impact on the performance of its convertibles. Despite common belief right now, common stock does not always decline when interest rates go up. During the late 1990s, for example, common stock and interest rates both went up together.

{kind=link}

In 2022, the energy sector actually went up along with the federal funds rate. I pointed this out in several blog posts and articles that were published here on Seeking Alpha around the beginning of this year. We have, in fact, been seeing the same thing over the past two months as long-term rates (as indicated by the ten-year U.S. Treasury) have gone up, as have energy stocks. The only reason why the broader stock market has fallen as rates have risen over the past two years is because the S&P 500 Index is heavily weighted to long-duration stocks, such as the major technology companies, that boast valuations that cannot be explained given their current financial performance. In short, though, there is not necessarily a correlation between stock prices and interest rates. Different stocks are affected by interest rates differently.

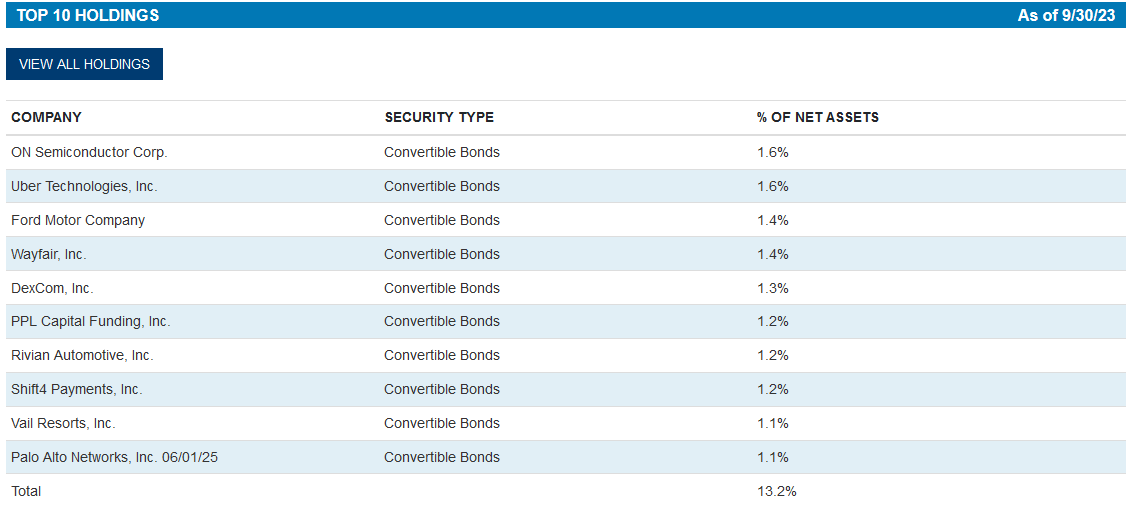

Unfortunately, the Calamos Convertible & High Income Fund is primarily weighted to long-duration assets. We can see this by looking at the largest positions in the fund:

{kind=link}

Many of these stocks are interest rate sensitive due to their valuations being driven mostly by expectations of their profitability twenty or thirty years from now, not what they earn today. The exception to this is possibly Ford ( F ), but interest rates have a significant effect on it as well since consumers usually borrow money to buy cars and the higher interest rates are, the less expensive a car they are able to buy. The fact that consumers are forced to trade down to a cheaper vehicle or postpone their purchase affects Ford’s revenue and net income in a negative way.

In this case, the fact that these are convertible bonds works in our favor as investors. This is because the issuing companies have to make coupon payments on the bonds until the bonds convert to common stock. This, therefore, provides the fund with a source of income even if the stocks themselves are not performing particularly well. This is one reason why these securities can oftentimes be the best of both worlds.

As might be expected from looking at the largest holdings in the fund, the Calamos Convertible & High Income Fund is heavily invested in technology companies. In fact, 19.9% of the fund’s assets are invested in this sector:

Calamos

This is a larger allocation than the fund had to this sector the last time that we discussed it. However, it is still lower than the S&P 500 Index’s 28.34% weighting to the sector. This is not especially surprising considering that convertible securities are frequently issued by start-ups and cash-flow-strained companies that cannot obtain reasonable rates on their debt without offering the potential for substantial returns from the common stock component. These companies are more often found in the technology space than in more capital-intensive industries such as materials, energy, or manufacturing.

With that said, we do see some capital-intensive businesses using convertible securities to raise funds. Rivian ( RIVN ), for example, is among the fund’s largest holdings. Tesla ( TSLA ) has also issued convertible securities in the past. Electric car manufacturers are one of the few capital-intensive industries that was easily able to obtain cheap financing by issuing common stock over most of the past decade or so, but convertible securities can allow them to appeal to investors and funds that desire current income without having to either to pay very high interest rates or dilute their current shareholders to an unacceptable degree. These securities do provide one of the only ways for investors to obtain exposure to this emerging sector and still earn a certain amount of income, so the fact that the fund includes convertible securities from this company might offer a certain amount of appeal.

Leverage

As is the case with most closed-end funds, the Calamos Convertible & High Income Fund employs leverage as a means of boosting its overall returns. I explained how this works in my last article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase convertible securities and high-yield bonds. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

It is important to note though that this strategy is not as effective today with interest rates at 6% as it was two years ago when interest rates were 0%. This is because the higher borrowing costs have greatly reduced the difference between the rate at which the fund borrows and the yield that it can get from the assets in the portfolio.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt since that would expose us to an excessive amount of risk. I do not generally like to see a fund’s assets exceed a third as a percentage of its assets for this reason.

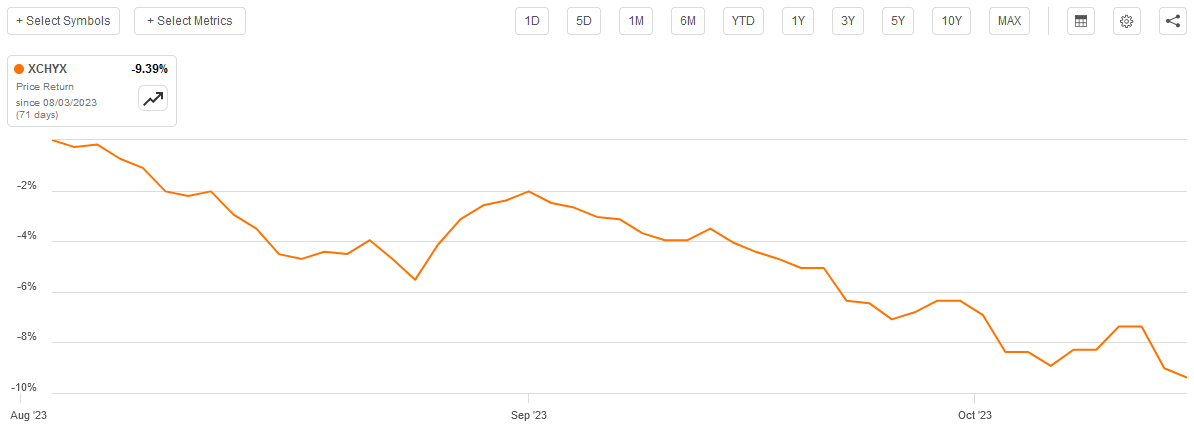

As was the case the last time that we discussed this fund, the Calamos Convertible & High Income Fund currently exceeds this one-third level with respect to its current leverage. As of the time of writing, the fund’s levered assets account for 39.32% of the portfolio, which is higher than the 36.97% ratio that it had the last time that we analyzed it. While it is true that this fund invests mostly in debt securities, which should be somewhat safer than common stocks, this is still a fairly high level of leverage. It is more concerning that its debt appears to be increasing, however, since that indicates that the fund’s overall risk is going up.

Admittedly, some of the leverage increase could very well be caused by the value of the fund’s assets going down. As we can see here, the fund’s net asset value is down 9.39% since August 3, 2023:

{kind=link}

Thus, it does not appear that the leverage increase that we see here is caused by the fund actively borrowing more money but rather by the value of its assets going down. That certainly does not make things better though, and we want to keep an eye on this since the leverage amplifies downside risk so the worse our losses will be if the market keeps moving against this fund. As this fund’s assets appear to have an inverse correlation to interest rates in aggregate, this means that we could be in for some trouble as most expectations right now are that the Federal Reserve will not reduce interest rates for the remainder of the year. In fact, if energy prices keep going up, there may be more increases and the leverage will amplify the losses.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Calamos Convertible & High Income Fund is to provide its investors with a high level of current income. In order to achieve this objective, the fund invests in a portfolio of convertible and junk bonds. For the most part, these securities deliver the majority of their investment returns in the form of direct payments to their owners. Convertible securities also have the upside potential of the common stock component, but for the most part, these securities are all designed for investors who are seeking to earn income. The fund collects the payments that it receives from these securities and applies a layer of leverage to boost the effective yield that it receives. The fund then pays out the money to its own investors, net of the fund’s own expenses. As such, we might expect that this will give the fund a fairly high yield.

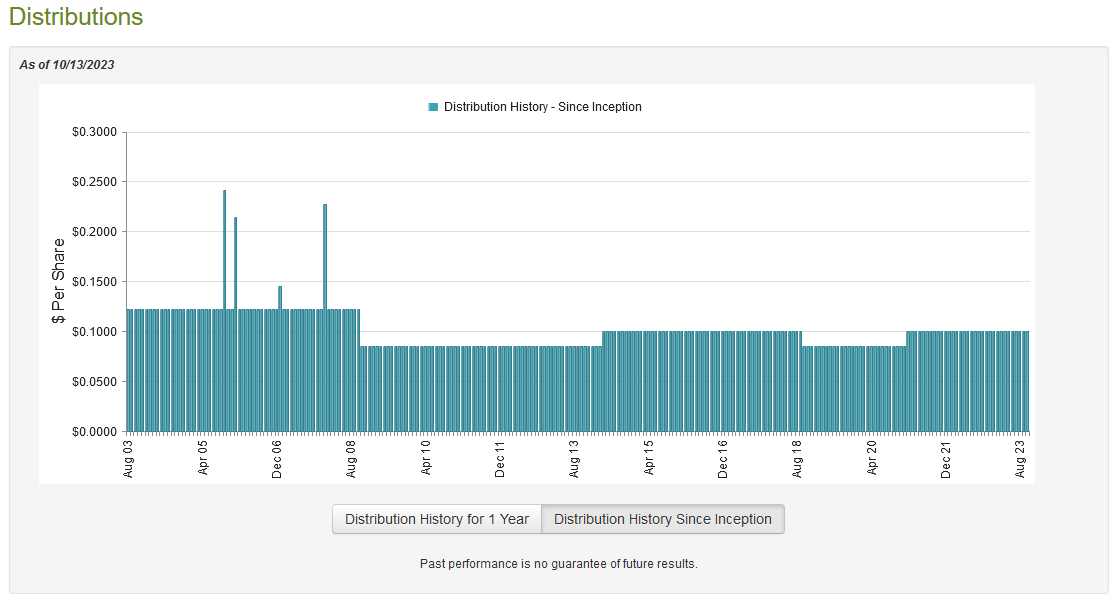

This is certainly the case as the Calamos Convertible & High Income Fund pays a monthly distribution of $0.10 per share ($1.20 per share annually), which gives it a 10.69% yield at the current price. That is certainly a high enough yield to appeal to most income-seeking investors, and indeed it is higher than just about anything else in the market. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years, as it has both raised it and cut it many times over its lifetime:

{kind=link}

This may reduce the fund’s appeal in the eyes of those investors who are seeking to earn a safe and consistent level of income from the assets in their portfolios. However, this fund has been much more reliable than most funds that invest in fixed-income securities as the distribution does not bounce all over the place like it often does with fixed-income funds. As such, this does present some questions as to why this fund is able to be more consistent than many other ones in the market. Thus, we want to investigate how exactly this fund is financing its distribution so that we can see just how well-covered it is. After all, if the fund is paying out more than it earns from its investments then that is very destructive to the capital base and could cause problems at some point.

Fortunately, we do have a relatively recent document that can be consulted for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on April 30, 2023. This was a very interesting time for the market, as the end of 2022 saw the markets crash fairly dramatically but they quickly recovered after the new year as a bubble started forming in artificial intelligence and traders began to expect that the Federal Reserve would pivot and start reducing rates. While this belief proved to be incorrect, the market did not start to decline until well after this period ended. Thus, the fund may have had the opportunity to sell some assets and realize capital gains, as bond traders were bidding up bond prices based on the pivot belief.

During the six-month period, the Calamos Convertible & High Income Fund received $16,723,953 in interest and $3,203,958 in dividends from the assets in its portfolio. However, some of the interest payments were actually considered to be a return of principal and thus are not considered to be investment income for tax purposes. As such, the fund only reported a total investment income of $14,850,520 during the period. Its expenses actually exceeded this amount, and the fund reported a net investment loss of $1,500,710 during the period. This is certainly going to be concerning, as the fund obviously did not have sufficient net investment income to afford any distributions, but it paid out $45,482,406 to its investors anyway. We normally like fixed-income funds to completely finance their distributions out of net investment income, so this is obviously problematic.

However, the fund does have other ways to obtain the money that it needs to cover its distributions to the shareholders. For example, it might have been able to obtain some capital gains by selling bonds once their prices started rising after the start of 2023. It may also have had some profits from the conversion of certain convertible securities into common equities, which were then sold off. Fortunately, the fund did enjoy some success here, as it reported net realized gains of $54,719,793 but these were partially offset by $31,303,100 net unrealized losses. Overall, the fund’s assets went down by $19,732,392 during the period after accounting for all inflows and outflows.

Thus, technically it failed to cover its distribution as its net assets declined during the period. However, we can see that the net realized gains were actually sufficient to cover both the net investment loss and the distributions with money left over. The decline in net assets was caused entirely by unrealized losses, and these might be erased once strength returns to the market. For the most part, this distribution is probably pretty safe as long as the fund can keep its realized gains at a similar level to what it had in the first half of the year. Admittedly, recent market action casts some doubt on its ability to accomplish that, but for the moment things do look okay. We should pay close attention to its next financial report, however.

Valuation

As of October 12, 2023 (the most recent date for which data is currently available), the Calamos Convertible & High Income Fund has a net asset value of $9.88 per share but the shares currently trade for $11.22 each. This gives the fund’s shares a whopping 13.56% premium on net asset value. That is an incredibly large premium that is quite a bit above the 9.73% premium that the fund has averaged over the past month. As such, the current price seems very high, and it would probably be a good idea to wait for it to come down somewhat. I generally do not like to pay a premium for any fund and especially not a double-digit premium.

The fund’s 52-week average is only a 5.47% premium and it has traded as low as a 3.00% discount on net asset value, so it should be possible to obtain a better price by waiting a bit.

Conclusion

In conclusion, the Calamos Convertible & High Income Fund is a rather interesting closed-end fund that could play a role in the portfolio of an income-focused investor. The fund is one of the few ways to easily get exposure to convertible securities, which are fairly nice as a way to get income without sacrificing upside potential, is nice.

Unfortunately, Calamos Convertible & High Income Fund has not been performing very well in recent weeks as rising interest rates have put a great deal of pressure on bond prices, as well as the price of long-duration assets. Surprisingly, the fund did manage to cover its distribution in the first half of the year, but it is not certain if it will be able to repeat this feat during the second half due to this problem. Caution is advised here, particularly since the fund is trading at a very high price.

For further details see:

CHY: Some Good Qualities, But Be Cautious