CINT - CI&T: Implementing AI And Machine Learning To Achieve Staggering Growth

2023-10-10 08:47:43 ET

Summary

- CINT’s revenue has grown at a CAGR of 32%, while EBITDA has exceeded this at 59%. CINT is successfully executing an aggressive go-to-market strategy.

- Growth has been achieved through a mixture of M&A and increased scale through reinvestment in its core operations. There is a long runway for this as CINT expands overseas.

- CINT’s margins have not improved to the extent desired, although we attribute this to a focus on growth. We see appreciation through scale and synergies in the coming years.

- AI, machine learning, and other technological developments will drive strong growth in the coming years. CINT is innovating well and has positioned itself as a leading provider.

- CINT’s valuation reflects several heightened risks associated with the business but leaves a substantial upside in our view. We see an upside in excess of 30%.

Investment thesis

Our current investment thesis is:

- CINT's organic growth approach is compelling in our view. It has created an approach to delivery that is highly regarded by its clients, underpinned by the willingness to provide an end-to-end solution and be judged on quantifiable outcomes. This is not a business that provides ideas or generic services but is a long-term partner to leading multinationals and smaller, growing companies. With a net retention of over 120%, it is clear that the company can win, retain, and upsell its clients effectively over time.

- We see growth coming from technological advancements, such as AI and data analytics, as well as continued M&A. Its expansion globally appears to be the correct strategy, although we await to see the outcome in the years to come to judge whether this will be accretive. Nevertheless, CINT's Management has shown an unwavering commitment to the development of its services (despite also doing M&A), which gives us comfort the business will always be at the forefront of technology.

Company description

CI&T (CINT) is a leading global digital solutions specialist. With a focus on driving digital transformation for businesses, CI&T offers strategic consulting, creative services, data intelligence, and technology solutions to help clients evolve and thrive in the digital age.

Share price

CI&T's share price performance has been disappointing since it was listed on the NYSE. The timing of its listing has not helped, with the wider market also struggling during this period, with its recent resurgence driven by a handful of technology companies. This said, the weakness is also a reflection of broader financial weakness, as macro conditions pressure the business.

Financial analysis

{kind=link}

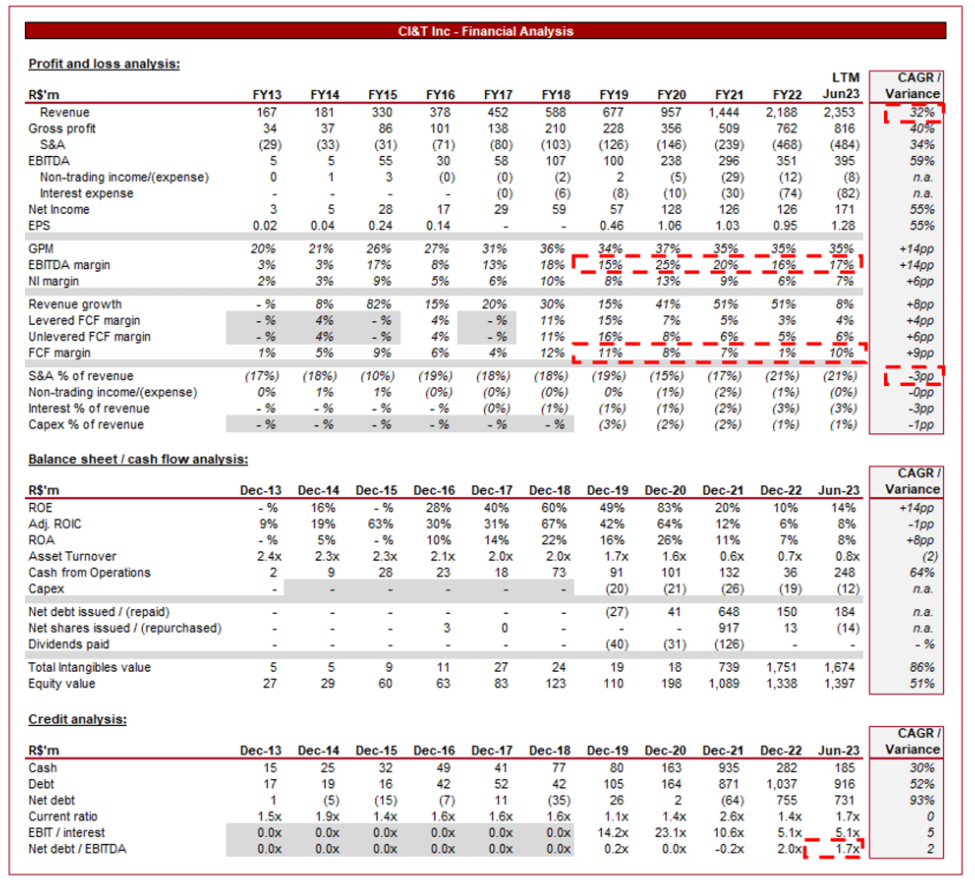

Presented above are CINT's financial results.

Revenue & Commercial Factors

CINT's revenue has grown by an impressive CAGR of 32% during the last decade, while EBITDA has outperformed this at 59%. This growth trajectory has been broadly consistent in its strength, although CINT has fallen below 15% in the LTM period.

Business Model

CINT offers a wide range of services to help businesses adapt and transition to the digital age. This includes digital strategy consulting, user experience design, data analytics, and the development of digital platforms and applications. It works with clients to identify areas for improvement, design tailored digital solutions and implement these solutions effectively.

CINT adopts agile and lean methodologies in their work. This approach emphasizes iterative development, close collaboration with clients (rather than being an outside voice), and a focus on delivering value to end-users quickly. CINT provides end-to-end solutions, from conceptualization and design to development, deployment, and ongoing support. This comprehensive approach ensures that clients have a single point of contact for all their digital needs, streamlining communication and project management. Further, this places the onus on CINT to deliver on its ideas for improvement, a key differentiation from many of its peers that either provide ideas or generic solutions (such as Cloud adoption). CINT has worked with many of the leading multinational companies, such as Nestle (NSRGY) and Coca-Cola (KO).

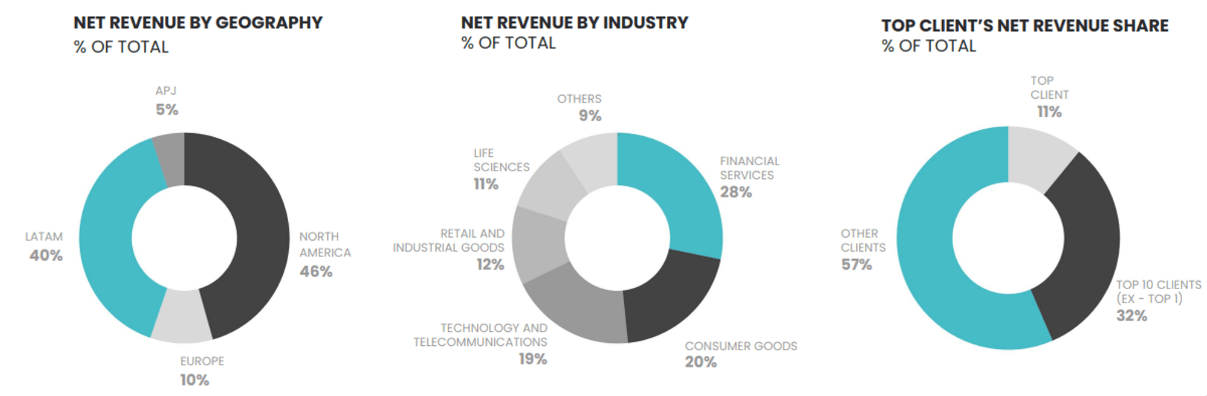

The company primarily operates in the Americas, with 40% of its revenue from LatAm and 46% from North America. Management's objective is to expand its geographical presence, with investment in Europe and other regions.

CINT has developed its approach to be universally applicable, allowing it to target a range of industries and clients. Its focus on modernization has allowed it to target industries such as Financial Services and Consumer Goods, where the benefits of Tech are high but implementation is low.

{kind=link}

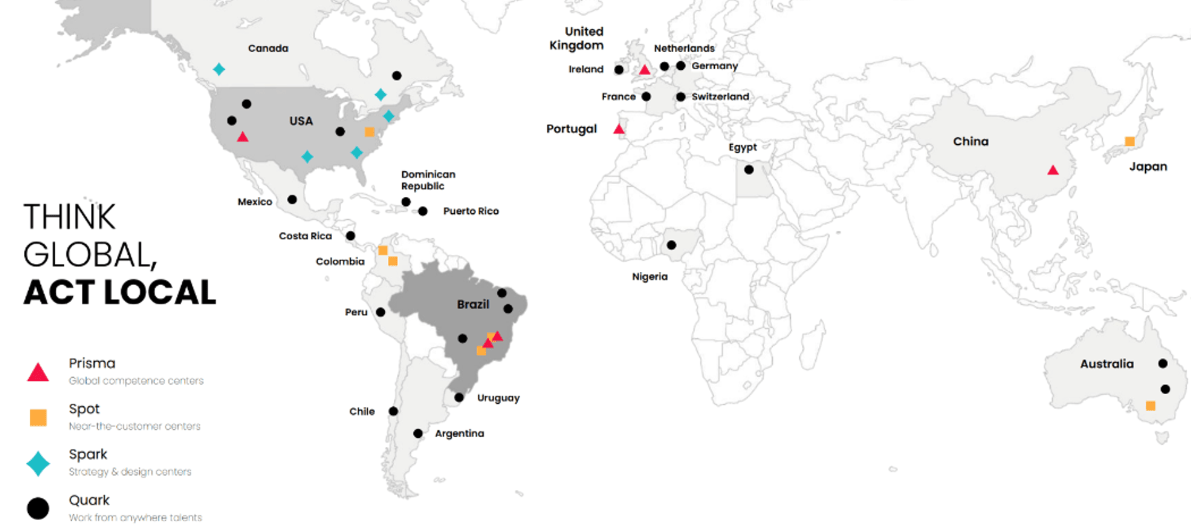

CINT has recently accelerated its global expansion strategy, with acquisitions in various geographies to expand its presence. Many of these businesses are being rebadged as "CI&T Global" or "[Company Name]: Part of the CI&T Family". Conceptually, we like this strategy. To grow to the next level, and develop its credibility to target higher-ticket clients, CINT needs to have a global presence. Operating globally allows the business to service a significantly larger number of clients but also supports its clients in specific geographies. This said, the strategy has been incredibly aggressive, creating risks associated with successful integration and sufficient focus given to each business.

What comforts us is how CINT is structuring its acquisitions, ensuring an alignment of incentives. If we take the Somo acquisition as an example (UK-based digital product agency), 25% of the base purchase price is paid in the form of shares in CINT. Further, there is an earn-out of 20% of the base purchase price linked to future performance.

{kind=link}

Competitive Positioning

We believe CINT is well-placed within the transformational segment. We consider the following factors to be key competitive advantages:

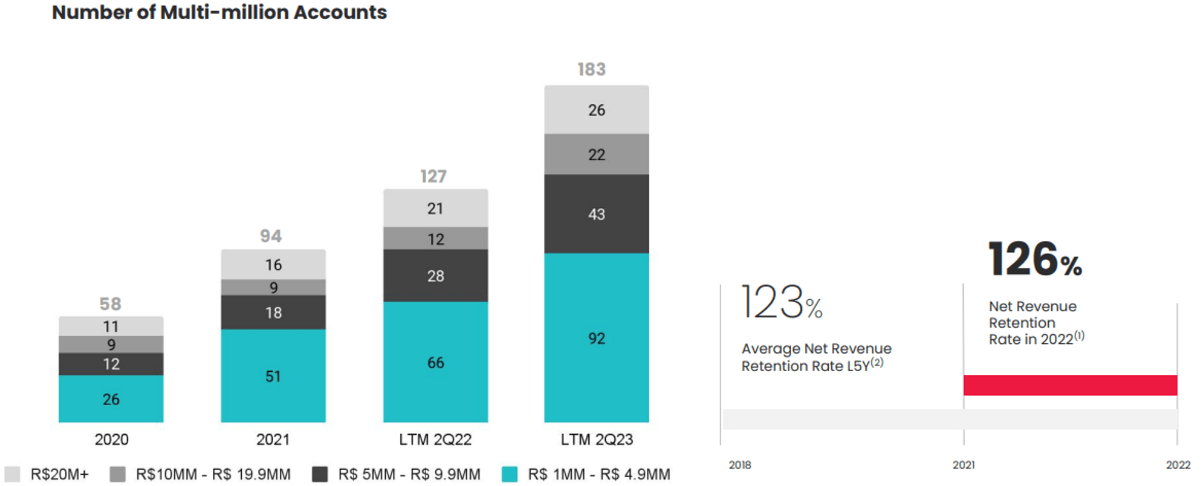

- Client-Centric Approach - CINT prioritizes building long-term relationships with clients. Its deep understanding of client industries and challenges allows it to offer personalized solutions that are purposefully scalable. CINT is not seeking to provide one-and-done integration services. A good metric to assess the success of this is retention. CINT's current retention is above its 5Y average, despite the market slowdown, and is at an incredibly strong level (125%). This suggests CINT is extremely successful with retaining and up/cross-selling clients.

{kind=link}

- Global Reach - CINT now has a strong presence, serving clients across different continents. Its ability to work in diverse markets and understand varying cultural nuances has broadened its potential client base.

- Expertise in Emerging Technologies - CINT's focus on innovation and its expertise in emerging technologies gives it a competitive edge. Management has instilled a culture of constantly seeking the "next big thing", with a focus on how it can generate genuine value. CINT is a leading player in incorporating AI (recent launch of CI&T/FLOW), machine learning, and other cutting-edge technologies, attracting clients looking to stay ahead in their respective industries. Management is seeing good progress in its development thus far.

{kind=link}

- Partnerships with Leading Technology Providers - CINT has improved its credibility and integration capabilities by partnering with major technology providers, such as Google Cloud (GOOG), to deliver integrated solutions. These partnerships enhance the quality of its services and streamline the process for clients.

- Investment in Talent - CINT invests in hiring and retaining top talent. Its teams consist of skilled professionals who have experience at leading technology firms, many of which have come directly from competitors. As a labor-intensive business, headcount management is critical. CINT currently has a leadership attrition of 2.6% and a broader attrition of 10.5%, which is a respectable level in the current environment. We attribute this to culture and working conditions.

{kind=link}

- Recurring Revenue through Support and Maintenance - CI&T often provides ongoing support and maintenance services to clients after the initial solution deployment. This creates a stream of recurring revenue, enhancing overall profitability and reducing revenue volatility. Moreover, excellent post-launch support fosters client trust.

Transformations Consulting Industry

The Digital Transformation Consulting industry is forecast to grow at a CAGR of 13% into 2028 , driven by digitalization at the operating level, as Management teams understand the value proposition technology can offer at varying levels. There is a growing desire to incrementally reduce costs and enhance commercial capability through increased digitalization. We are living in a data generation where genuine differentiation can be achieved through better use of data, even in historically "mature"/"boring" industries. Naturally, this has contributed to significant competition among consulting firms to be at the forefront of providing these services to businesses. CI&T competes with companies such as the Big 4 accounting firms, EPAM Systems (EPAM), Endava (DAVA), IBM (IBM), Cognizant (CTSH), and Accenture (ACN).

The runway for growth is long in our view, as there will always be new technologies that supersede prior ones. Cloud has driven growth in the last decade, with AI and Machine Learning positioned perfectly to take its place in the coming years. We believe CINT's culture and development thus far place it as a leading option for businesses.

Margins

{kind=link}

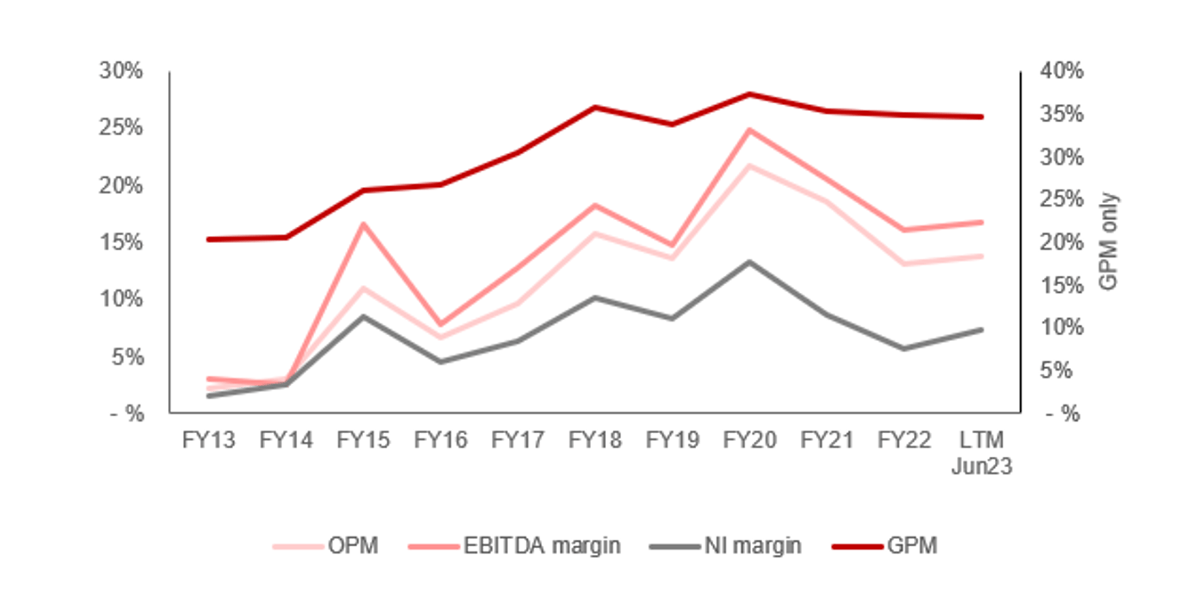

CINT's margins have progressively improved during the historical period, although they have declined in the LTM. The margin improvement is a reflection of several complementary factors. The business has grown in scale, contributing to operating cost leverage and greater efficiency. Further, CINT has expanded its services offering to higher-margin solutions, supported by an improvement in its brand and capabilities. Finally, with scale and greater brand notoriety (from the delivery of successful projects), the business can demand higher rates from new clients.

Quarterly results

CINT's recent performance has been strong, although there are signs of a potential slowdown ahead. In its last four quarters, the company has seen revenue growth of +48.7%, +33.9%, +24.0%, and +8.9%. In conjunction with this, margins have slightly slipped, although are broadly in line with the levels achieved since late 2021.

CINT's resilience is a credit to the company's aggressive growth strategy, with a significant increase in M&A activity. The business is in a consolidation phase, contributing to it maintaining its upward trajectory. This said, the recent quarter may be a closer reflection of its organic trajectory, falling well below its recent performance. The current macroeconomic environment is one of uncertainty and caution, as inflation and interest rates contribute to reduced demand and conservative operational activities. CINT will inevitably be impacted negatively by this, with reduced spending on consulting services as a means of protecting margins.

Assuming M&A activity begins to slow and thus CINT's organic trajectory is more heavily weighted to growth, we suspect the business will struggle to maintain a DD trajectory into FY24. We suspect expansionary policy will begin in mid-to-late 2024 in the West, with strong growth returning at this point. Importantly, we do not believe CINT's business model has degraded in any way but attribute this wholly to market conditions. We do think transformational services will see a spike once market conditions improve, as businesses race to generate operational improvement in a more complex environment, utilizing popular tech such as AI.

Balance sheet & Cash Flows

CINT is reasonably financed, with a ND/EBITDA ratio of 1.7x. This is despite the recent wave of global acquisitions, with CINT spending over R$1.4b. The current level in conjunction with the company's aggressive growth should mean further debt can be raised if required.

CINT's profitability and FCF are broadly aligned, with attractive conversion to cash and minimal Capex commitments. Thus far, cash has been allocated to acquisitions, restricting the ability to distribute to shareholders. We are supportive of this strategy as the company is still in its growth phase, although we suspect returns can be quite attractive once capital allocation begins to be balanced.

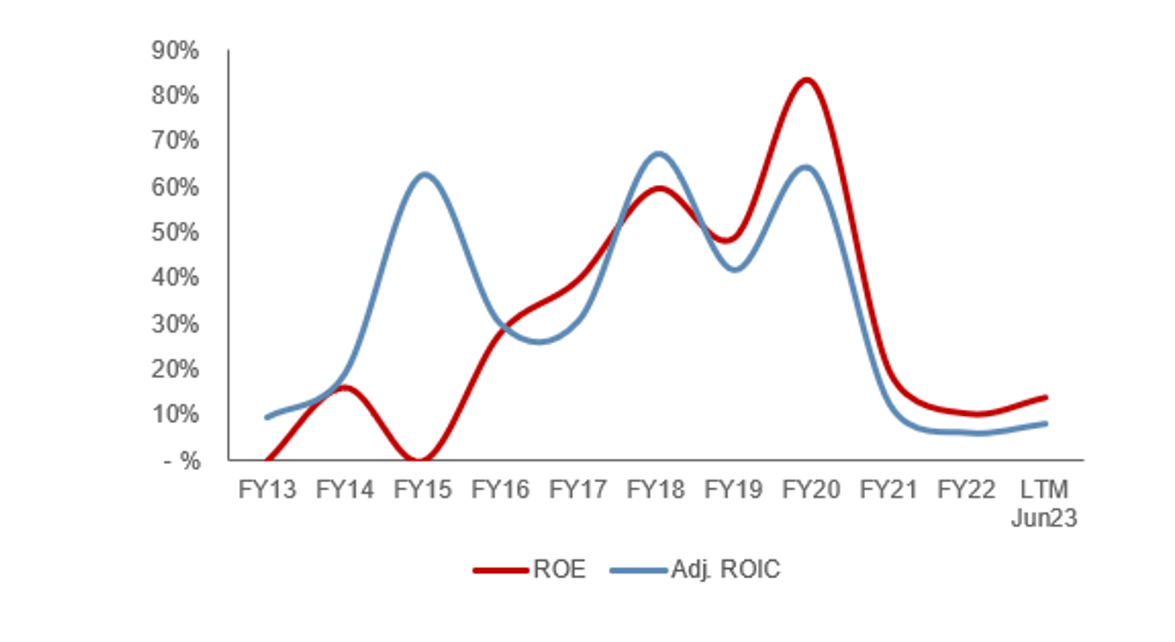

ROE has fluctuated following the substantial uplift in goodwill following its various acquisitions. This will initially depress the ROE ratio until Management has effectively incorporated the newly acquired entities and achieved synergistic benefits. Assuming a ROE of 14% is close to the "bottom" of its normalized level going forward, we see this as very attractive.

{kind=link}

Outlook

{kind=link}

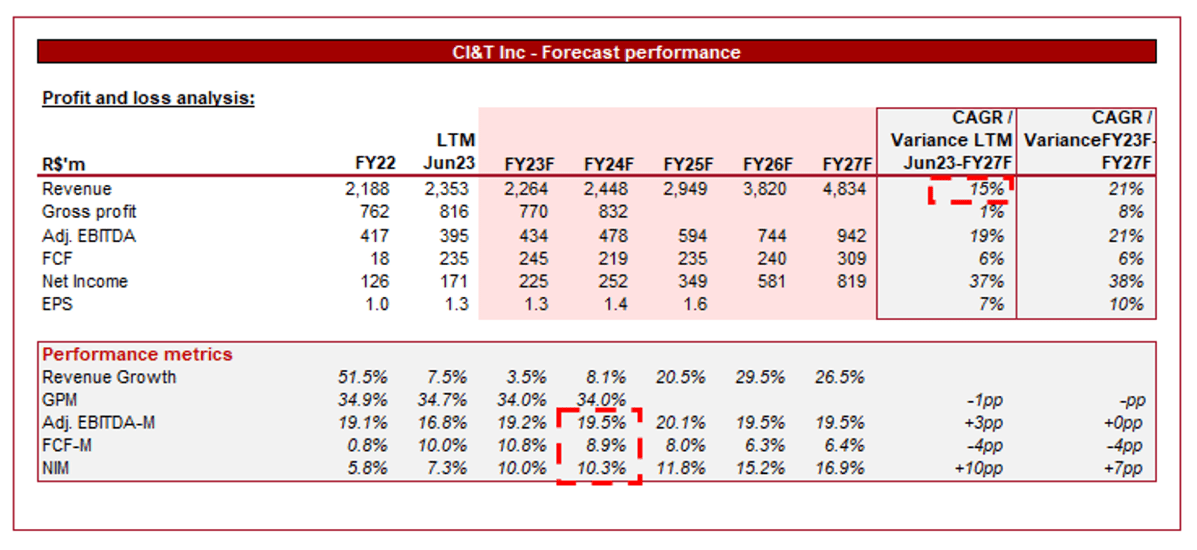

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting strong growth in the coming years, although at a lower level than what has been achieved historically. In conjunction with this, margins are expected to stabilize at its FY22 level.

We believe these assumptions are broadly reasonable, although would consider this a poor performance should it unfold. Following over R$1.4b in spending, we would expect growth between FY22 and FY25F to be higher than mid-single-digits, particularly due to AI tailwinds.

Secondly, following these acquisitions and industry tailwinds, we believe CINT should be achieving an improvement in margins through operating cost leverage, synergies, and higher rate cards.

Our target for the business by FY27F would be a CAGR of 18-22% based on the pipeline of acquisitions, as well as an EBITDA-M of 24%.

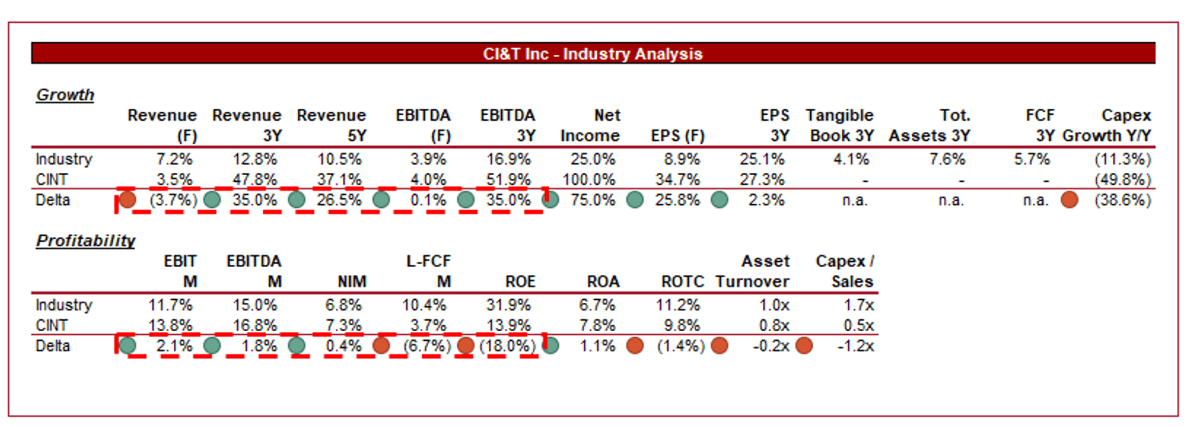

Industry analysis

IT Consulting and Other Services Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of CINT's growth and profitability to the average of its industry, as defined by Seeking Alpha (21 companies).

CINT performs well relative to its peers, especially when contextualized by its growth trajectory. Revenue growth materially outperforms its peers across various time periods, as does profitability. We attribute this to its aggressive go-to-market strategy and eagerness to expand globally, while also having an inherently strong domestic business.

Furthermore, the company's margins are equally strong, although lacking in FCF and ROE. The margin achievement is especially good given CINT is still in its growth phase, with what we believe to be room for margin appreciation through optimization. This suggests CINT is a highly attractive proposition relative to a broad group of mature peers.

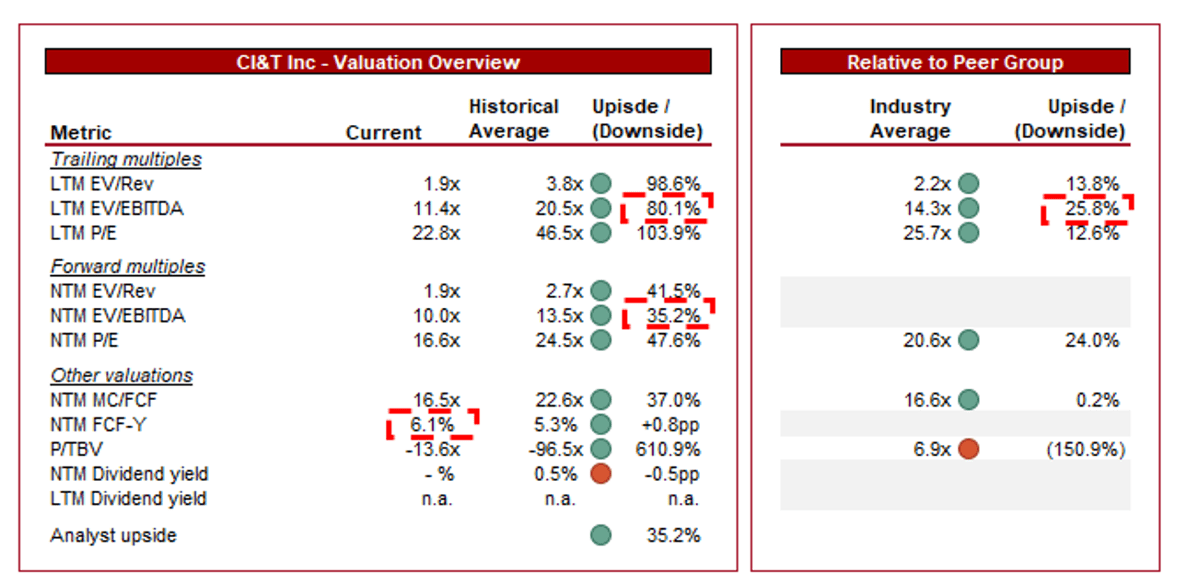

Valuation

{kind=link}

CINT is currently trading at 11x LTM EBITDA and 10x NTM EBITDA. This is a steep discount to its (short) historical average, illustrating the substantial decline in share price.

In order to benchmark CINT's valuation, we will assess the company's valuation relative to its peers. CINT is currently trading at a 26% LTM EBITDA discount to its peers, while comparably trading at a 24% NTM P/E discount. We struggle to reconcile this discount, primarily due to its strong combination of margins and growth. Even when taking a step back and assessing its commercial position, CINT is well regarded in the market and diversifies its capabilities through acquisitions.

We believe CINT has the scope to trade at a premium to its peer, particularly in the medium term, with a conservative level of 10-15%. This implies upside of over 30% at its current share price, aligning with analysts' price target which suggests 35%.

Key risks with our thesis

The risks to our current thesis are:

- FX - As a Brazilian business, the company faces FX risk associated with the conversion of its earnings to USD. With CINT expanding globally, we do see this risk diminishing but remains a concern.

- " Hitting a wall" growing globally - The transformational segment of consulting has seen incredible growth across the West, which is a region CINT is expanding into. There is a risk that the business will not be able to achieve its growth targets in these markets due to higher competition. The willingness of key personnel within these teams to remain post-transaction is critical to success.

- "Brazil is the country of the future... and always will be" (CDG) - 40% of the company's revenue is from LatAm, Brazil being a major part of this. Growing within this region (and nation) requires economic development, much of which has been over-promised and under-delivered for many decades. This broader view of LatAm and Brazil has inevitably led to share price pressure among the LatAm region (which we have seen across other industries).

- Economic slowdown - Delays in economic recovery could contribute to a slowdown in its expansion momentum, particularly in the AI and machine learning segment which is seeing impressive hype currently. More broadly, any slowdown in demand returning will mean greater downward share price pressure.

Final thoughts

CINT is a fantastic company in our view. It is operating within a segment that is benefiting from long-term tailwinds, with AI positioned to be the next big growth area. Businesses will increasingly seek the value associated with incorporating AI given its wide-reaching capabilities. Almost every business in the world can benefit to varying degrees. Beyond this, however, CINT's culture of seeking the next big thing will ensure it always has a well-regarded service offering.

From an operational perspective, we believe the company is run extremely well and is positioned to support its clients over an extended period. This has not compromised its financial performance, however, with leading margins and strong capital returns.

Being based in Brazil, facing near-term macroeconomic headwinds, and an aggressive M&A strategy does increase risks associated with capital appreciation, but we believe this is adequately priced into the stock.

For further details see:

CI&T: Implementing AI And Machine Learning To Achieve Staggering Growth