CINT - CI&T: Redefining Digital Transformation In Brazil And Beyond

2023-07-03 07:18:45 ET

Summary

- CI&T, a Brazilian digital transformation services company, offers an attractive investment opportunity with an estimated intrinsic value of $8.96, despite challenges such as high-interest rates and a slowdown in digital investments.

- The company has a strong track record of client retention and is strategically focused on leveraging acquisition synergies, positioning it for continued success in the digital transformation landscape.

- CINT stock's undervalued status and potential for multiple expansions make it a compelling long-term buy for investors who are willing to navigate the risks and capitalize on the company's strong fundamentals and growth prospects.

Investment Thesis

CI&T ( CINT ), a leading Brazilian digital transformation services company, presents a highly compelling investment opportunity with an estimated intrinsic value of $8.96. Despite facing challenges such as elevated interest rates in Brazil and a slowdown in digital investments, the company's management demonstrates remarkable resilience by projecting revenue growth between 13% and 17% for 2023. With a compound annual growth rate of 48% since 2019, CI&T has outperformed the market consistently. Moreover, the stock offers an enticing valuation as it is currently trading at an EV/EBITDA multiple of approximately 12.36x. I strongly believe that CI&T's strong track record of client retention, coupled with its strategic focus on leveraging acquisition synergies, positions it well for continued success in the dynamic digital transformation landscape. Additionally, the potential for multiple expansion further augments its investment appeal. Considering these factors, I recommend an overweight rating on CI&T, anticipating significant returns over the next 3 to 5 years as the company capitalizes on its strengths and taps into vast opportunities in the technological landscape.

Company Overview and History

CI&T Software S.A., founded in 1995 in Brazil by Cesar Gon (current CEO) and Bruno Guicardi (current North America & Europe President), started as a research and development firm catering to software companies. Over the years, CI&T has transformed into a global digital transformation specialist, working with some of the world's leading brands, such as Johnson & Johnson ( JNJ ), Anheuser-Busch InBev ( BUD ), Nestlé ( NSRGY ), Google ( GOOGL ), Coca-Cola ( KO ), and Audi ( VWAGY ), to help them drive impactful digital transformations in their daily business operations and long-term strategic thinking. The company takes responsibility for developing co-designed strategies that identify business problems and create digital initiative roadmaps for implementing prioritized digital solutions. Leveraging their expertise in digital services and practices in different industry verticals, they help their clients evolve their operating models and organizational culture to adapt quickly to technological advancements such as artificial intelligence, cloud computing, and mobility. While their focus is on expanding their business in North America and Europe, CI&T continues to benefit from their Latin American roots, particularly in Brazil, due to the region's enormous size and high demand for digital transformation services.

Summary of Past Acquisitions

Since 2021, CI&T has embarked on an ambitious acquisition strategy, deploying a majority portion of its IPO capital to expand its technology integration services and enhance its capabilities in supporting digital marketing engagements with new clients. These acquisitions have allowed CI&T to bolster its delivery capacity and extend its reach to international brands. Here are the notable acquisitions made by the company:

Dextra : A prominent Brazilian software development company known for its end-to-end digital product creation and expertise in building secure and scalable software. The acquisition was valued at R$800 million.

Somo Global : A leading independent digital product agency based in the UK that specializes in delivering digital solutions across various industries, including automotive, financial services, utilities, and telecom. The acquisition amounted to £49 million, with an additional earn-out clause of up to £9.8 million.

Box 1824 : A strategic consulting firm headquartered in São Paulo that is renowned for its ability to transform future visions and map out business strategies based on behavioral insights. The total cost of the acquisition was R$34.18 million.

Transpire : An Australian technology consultancy focused on designing and building digital experiences. Transpire's expertise lies in solving complex problems, delivering delightful user experiences, and leveraging technology to improve people's lives. The acquisition amounted to AUD 23.4 million.

NTERSOL : A US-based digital transformation provider specializing in the banking, financial services, and insurance verticals. The transaction, valued at R$664.65 million, included the issuance of 4,000,000 Class A common shares to eligible holders of NTERSOL shares until 2026.

FY 2023 First Quarter Presentation

{kind=link}

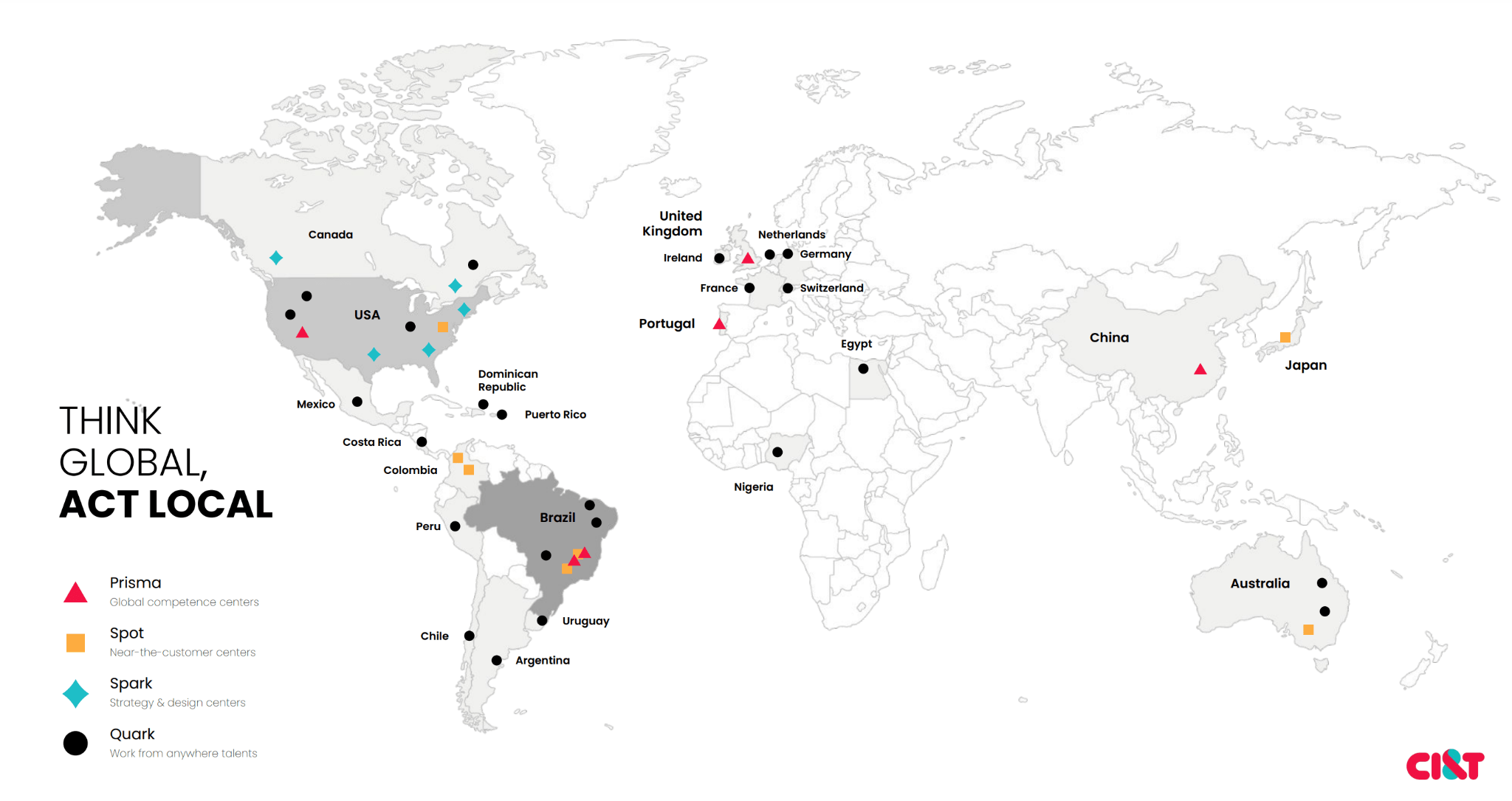

By expanding its global footprint through strategic acquisitions, I believe CI&T is positioning itself to compete vigorously against established digital transformation companies such as EPAM ( EPAM ) and Globant S.A. ( GLOB ). These acquisitions have not only enhanced CI&T's product offerings but also strengthened its capabilities in different geographies, allowing the company to tap into new markets and unlock growth opportunities. In my view, CI&T should be able to maintain its leadership position by capitalizing on the growth opportunities in the digital transformation space and drive continued success in the evolving market landscape.

{kind=link}

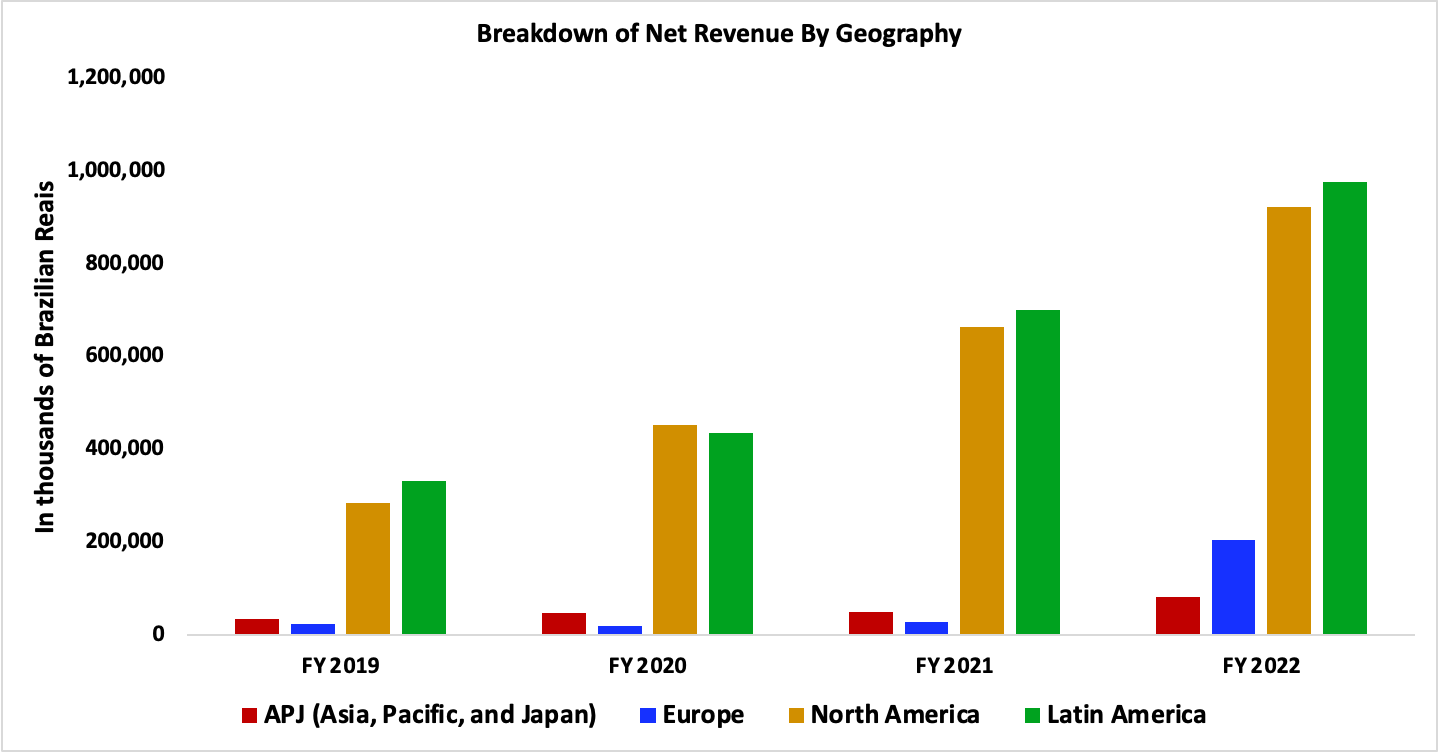

By looking at the chart above, it demonstrates that CI&T's European and Asian footprints have experienced substantial growth, albeit starting from a relatively smaller base compared to North America and LATAM. In my opinion, this growth trajectory is expected to accelerate further with the recent acquisitions of Transpire and Somo, which have provided CI&T with an expanded presence in these geographies. Europe and Asia present compelling opportunities for CI&T due to the increasing recognition of the vital role that digital transformation plays in driving economic growth and competitiveness. As countries in these regions strive to strengthen their international standing, they are increasingly investing in digital technologies and innovation to fuel their development. With its recent acquisitions and expanded capabilities, I believe the company is well-positioned to capture these opportunities and support businesses in geographies that embrace digital transformation to drive innovation and international growth.

Long-Term Industry Trend

{kind=link}

From my perspective, the rapid advancement of technology is disrupting competition across all industries. Digital native companies, which leverage technology in every aspect of their businesses, have gained a competitive edge with their innovative, data-driven, and user-centric approach. In contrast, incumbent enterprises often struggle to balance maintaining legacy infrastructure with adopting next-generation technologies. Institutional constraints, traditional approaches to development, and the difficulty of absorbing technological advancements pose challenges for incumbent enterprises. As a result, I strongly believe that digital transformation has become crucial for incumbent enterprises to meet evolving customer expectations and compete with digital native disruptors. CI&T, as a specialist in digital transformation, can provide valuable assistance to companies navigating this process within their existing structures.

{kind=link}

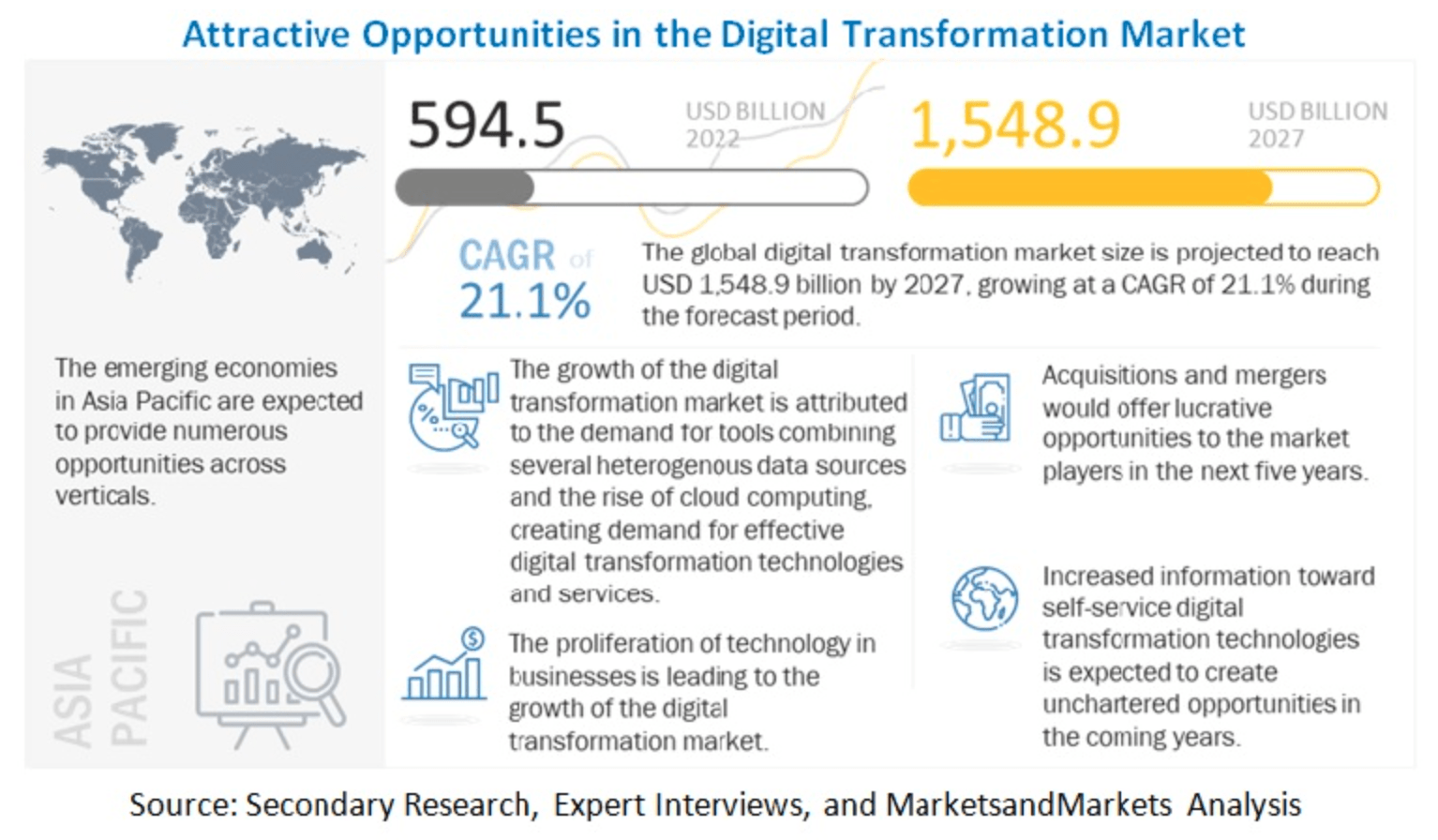

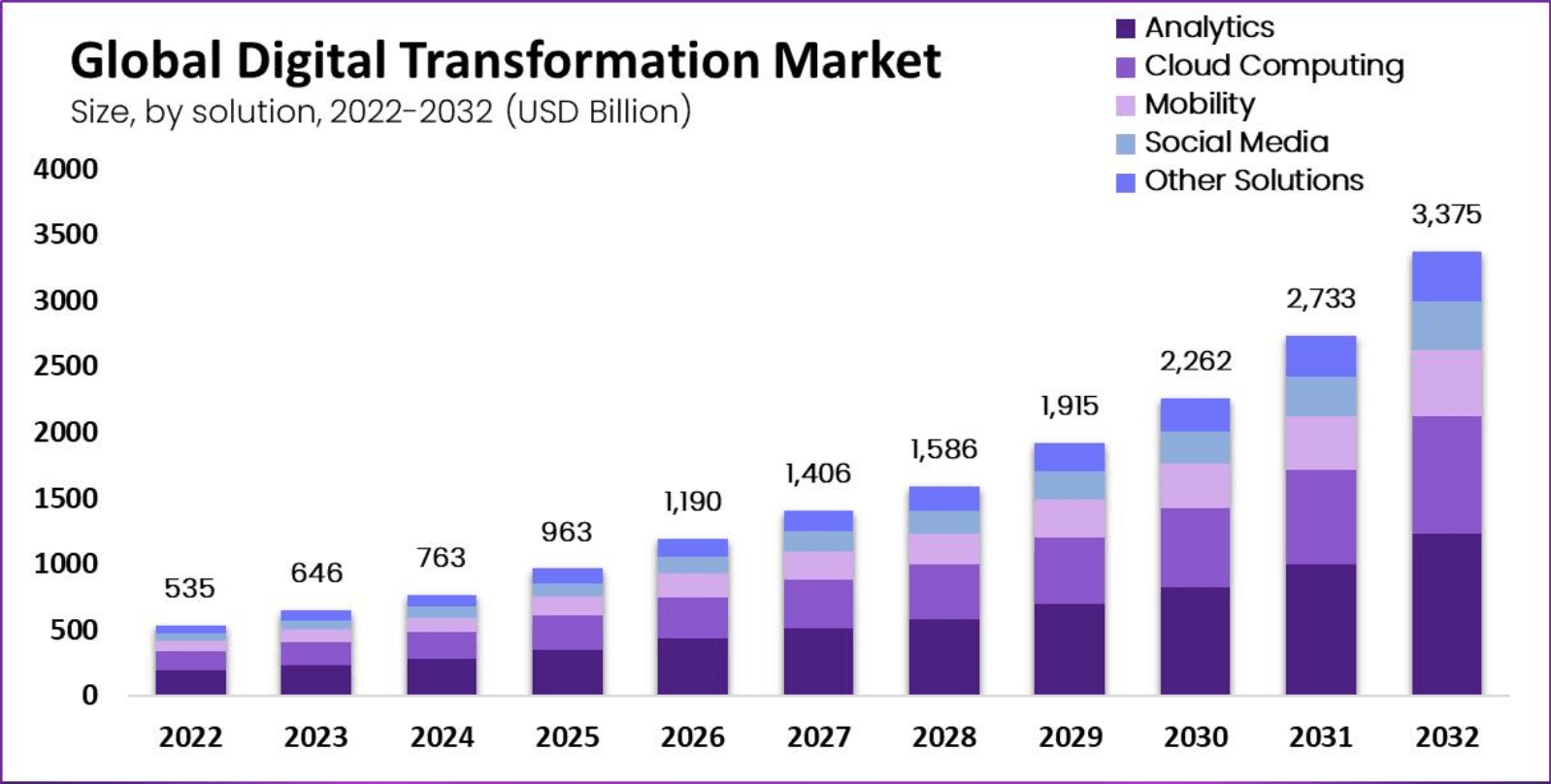

According to reputable sources like MarketsandMarkets , Polaris Market Research , GlobeNewswire and Grand View Research , the digital transformation industry is poised for robust growth, with a projected compound annual growth rate ranging from 20% to 24% between 2022 and 2030. This considerable growth is being driven by the widespread adoption of digital technologies as businesses worldwide undergo substantial digital transitions, shifting their focus from traditional data centers to cloud computing solutions. Organizations across industries are leveraging digital solutions to enhance operational efficiency, improve customer experiences, drive innovation, and gain a competitive advantage in the rapidly evolving global marketplace. As a result, I believe companies such as CI&T will benefit from this ongoing technological advancement by providing businesses with the most advanced digital solutions.

Short-Term Macroeconomic Headwinds

However, digital transformation enterprises are currently facing challenges due to budget constraints and businesses' reluctance to invest in digital transformation amid worsening macroeconomic conditions. This situation has led to downward revisions in revenue outlook by industry peers such as Endava ( DAVA ) and EPAM Systems. On June 5, 2023, EPAM Systems revised its FY 2023 revenue outlook, projecting a decline in the range of $4.650 billion to $4.800 billion, representing a 2% year-over-year decrease. This revision follows a prior adjustment made in Q1 2023 , when the company revised its full-year guidance to a range of $4.950 billion to $5.000 billion, subsequent to initially issuing an outlook of $5.250 billion in Q4 2022. Similarly, Endava has revised their expected fiscal year guidance downwards as they now anticipate their revenue to be between $792.00 million and $794.00 million, compared to the previously projected range of $843.00 million to $852.00 million in Q1 FY 2023. According to their Q3 FY 2023 Earnings Call , this adjustment is attributed to private equity "evaluations of business models and returns, taking into account macroeconomic factors, access to capital, and evolving interest rates across economies."

Despite the challenging economic backdrop, CI&T has demonstrated an outstanding performance, surpassing their initial Q1 revenue outlook . They achieved a revenue of R$610.0 million, reflecting an increase of 24.0% compared to 1Q22. These results have further reinforced their confidence in the full-year outlook , with an expected net revenue growth in the range of 13% to 17% year-over-year. According to their most recent earnings call , CI&T's success can be attributed to their strong client base, with approximately 90% consisting of large traditional brick-and-mortar businesses. In my view, CI&T's management has strategically positioned themselves to benefit from partnering with established businesses since they possess a robust capability to withstand challenging times while actively exploring new initiatives to enhance their operational efficiency.

Key Drivers and Catalysts

FY 2023 First Quarter Presentation

{kind=link}

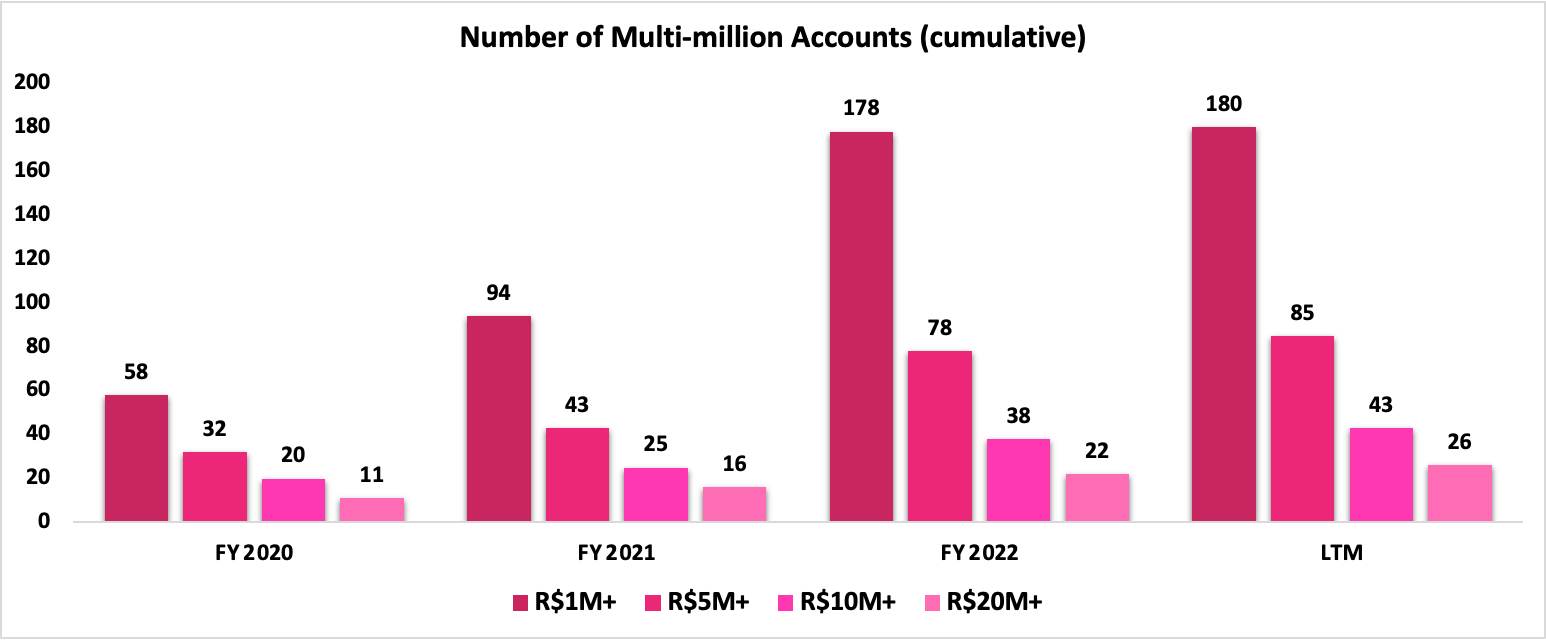

Over the past three years, I believe management has made notable progress in expanding the company's portfolio of multi-million accounts, with its R$1M+ and R$5M+ accounts growing threefold. Moreover, CI&T has demonstrated strong client retention, successfully doubling its R$10M+ and R$20M+ accounts during this period while also achieving an average net revenue retention rate of 123% for the past five years. This achievement highlights the company's ability to attract and retain high-value clients, establishing itself as a trusted partner in their digital transformation journey. The trust and satisfaction of these clients have resulted in increased spending with CI&T as they recognize the value and impact of the company's offerings. As CI&T continues to deliver results and drive efficiency for its clients, I believe it can foster long-term relationships and uncover additional opportunities for growth. With an expanding reputation and a track record of success, CI&T is well-positioned to onboard new clients seeking transformative digital solutions. In my opinion, the stickiness of CI&T's offering, combined with its ability to consistently deliver value, creates a positive feedback loop that fuels growth and positions the company as a trusted partner in clients' digital transformation journeys.

Company's 10-K's Company's 10-K's

{kind=link}

{kind=link}

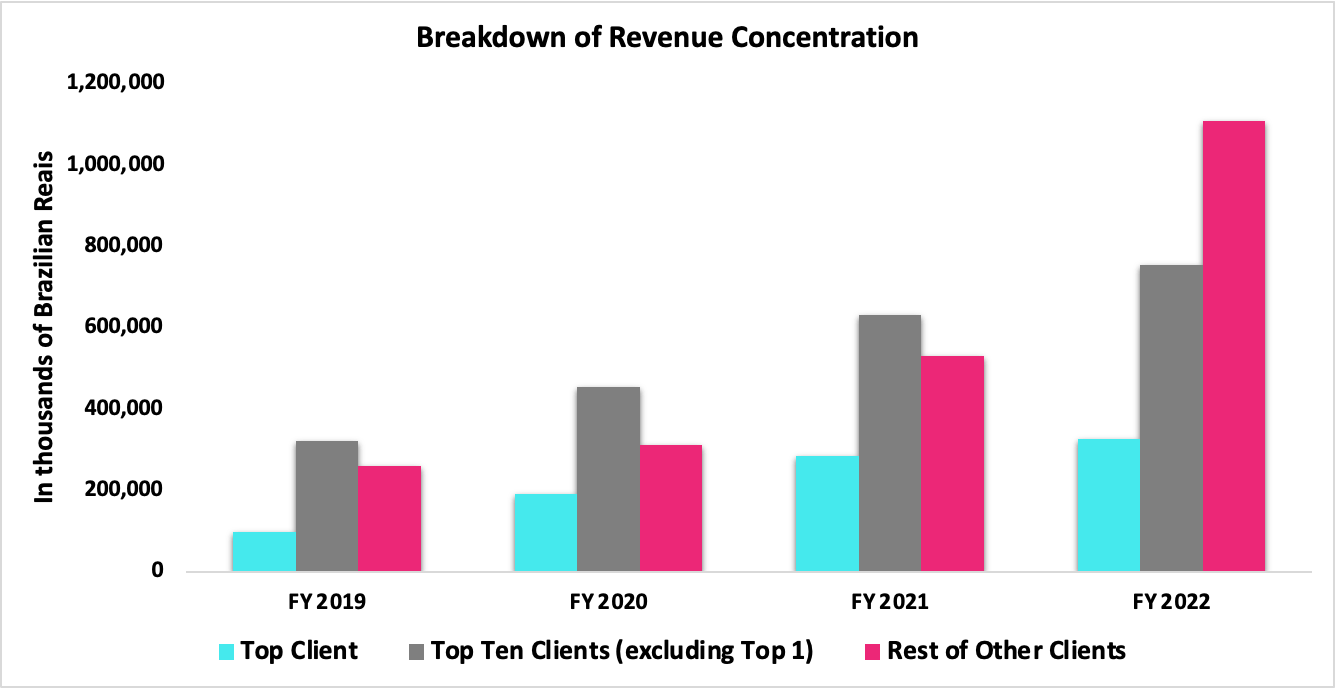

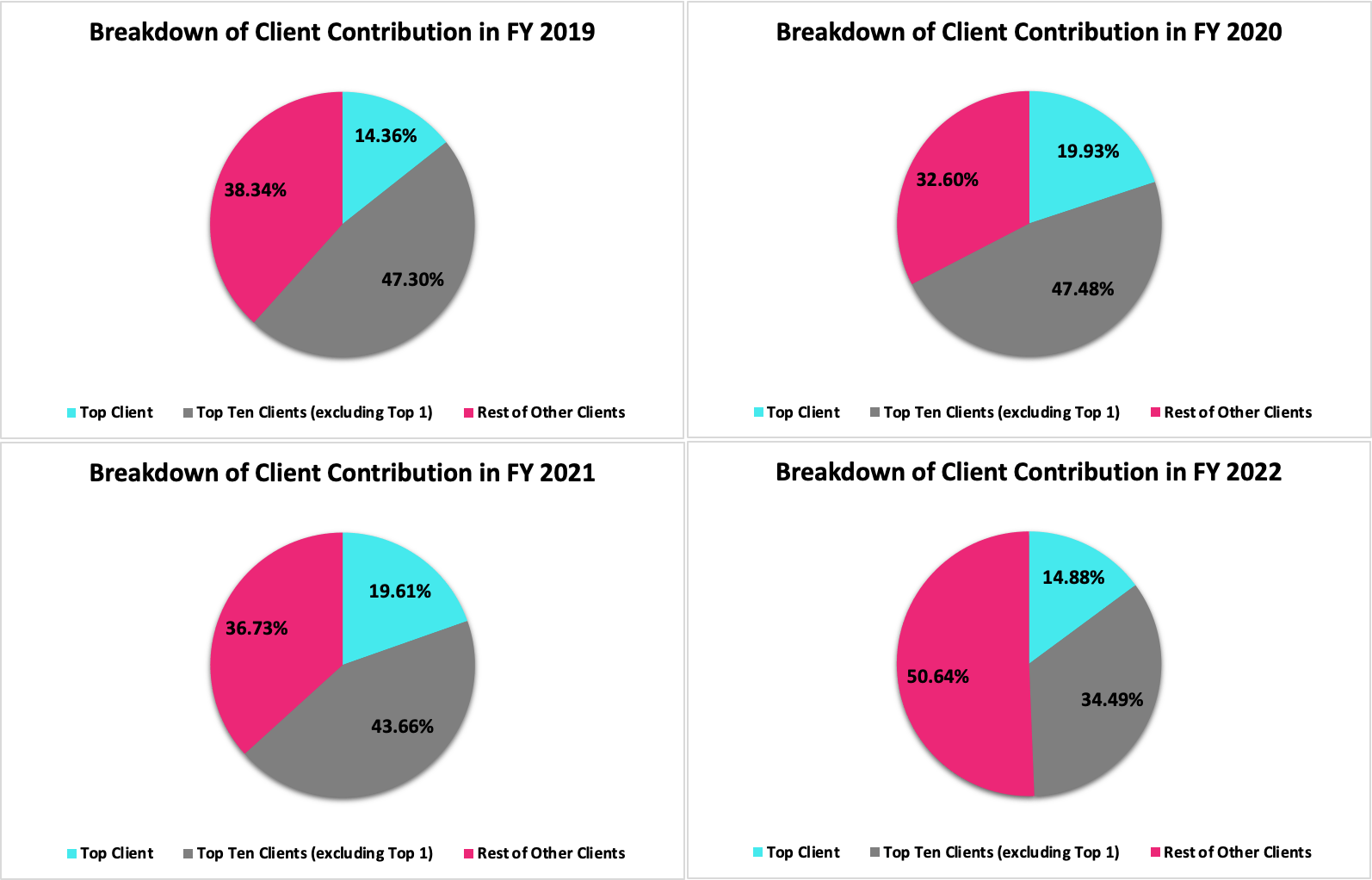

Initially, investors may have been concerned about CI&T's client concentration risk. However, the company's client composition has experienced a shift in 2022, reducing its reliance on the top ten clients for most of its revenue. For the first time in its operating history, CI&T generated slightly more than half of its revenue from clients outside of the top 10. Although the revenue contribution from its largest client has increased in recent years, its overall impact on total revenue has decreased by a sizable amount, mitigating the risk associated with client concentration. In my opinion, this positive trend suggests that CI&T is successfully diversifying its client base and reducing its exposure to client concentration risk, positioning the company for future growth and stability.

{kind=link}

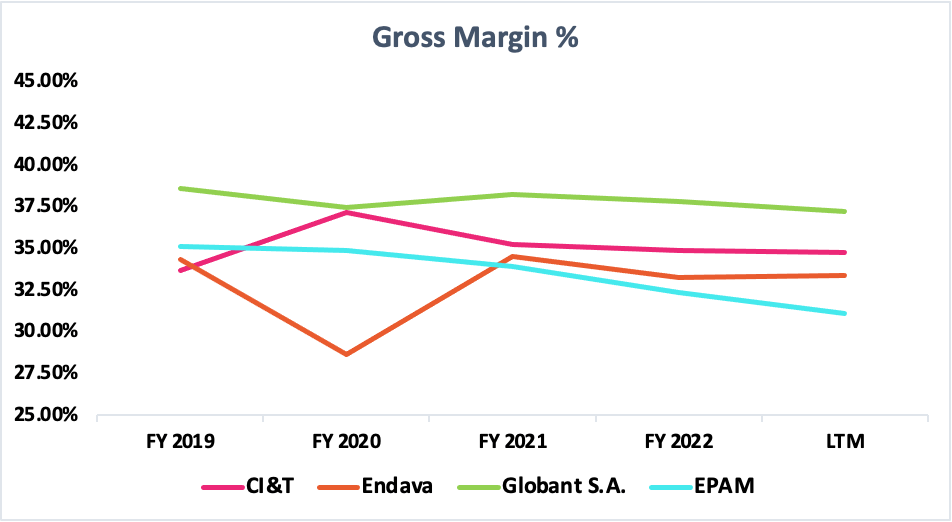

Despite being smaller in size compared to its competitors, CI&T has been maintaining a competitive gross margin in the digital transformation industry. One aspect contributing to CI&T's competitive margin is its ability to keep employee-related costs relatively lower than its counterparts. In my view, this is primarily driven by a combination of factors, including a low employee attrition rate and the concentration of a massive portion of its workforce in Brazil, where labor costs tend to be more cost-effective. According to recent reports shared by Bruno during the company's earnings call, the attrition rate has decreased from 16% in the first quarter of 2022 to a noteworthy 12%. Furthermore, the attrition rate among leadership positions remains below 4%. By maintaining a low attrition rate, I believe the company can leverage the expertise and experience of its employees, ensuring continuity and consistency in delivering high-quality digital transformation services.

{kind=link}

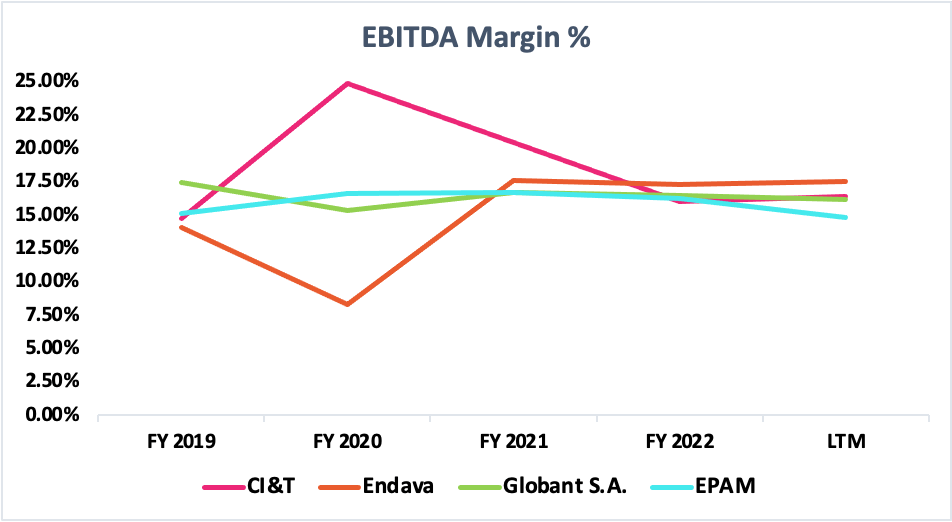

For the past two years, CI&T's acquisitions have led to a noticeable reduction in its EBITDA margin, primarily attributed to higher SG&A costs. Additionally, the company has faced challenges related to wage inflation in Brazil, which further impacted its short-term profitability. However, the company has actively addressed these concerns and implemented strategies to mitigate the impact. By focusing on achieving acquisition synergy and leveraging its operations in Brazil, I believe the company can enhance cost efficiency and improve its overall profitability. The company's decision to pause further acquisitions indicates a shift towards maximizing operational efficiencies and optimizing existing resources. As CI&T continues to execute its operational improvement initiatives, I anticipate a gradual improvement in its EBITDA margin over the next few quarters.

{kind=link}

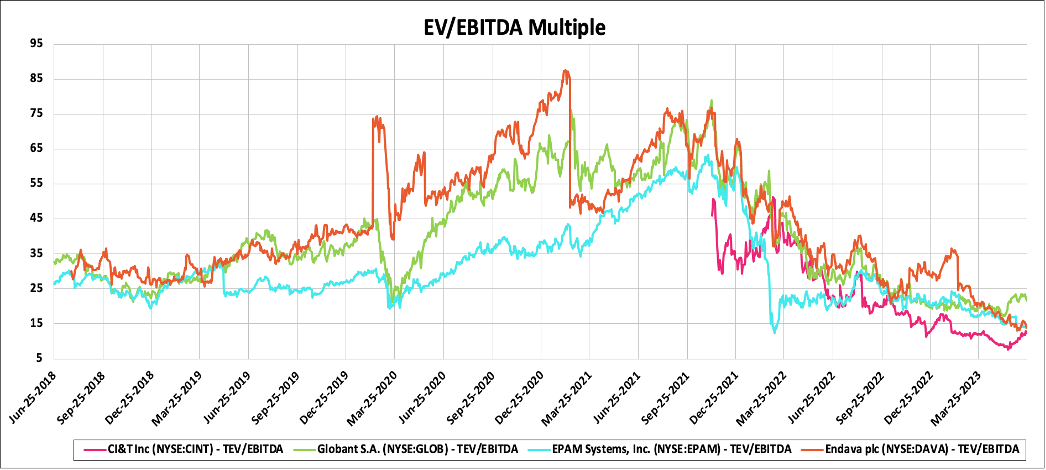

Despite experiencing a huge reduction in its share price since the stock market crash in 2022 and facing a revaluation of equity due to rising interest rates, the company has shown signs of recovery. The stock, which reached its lowest point at $3.34, has rebounded notably in the past month, driven by the company's exceptional earnings report. However, CI&T's current valuation on an EV/EBITDA basis appears relatively lower compared to its peers, such as Endava and EPAM, despite its superior growth potential. According to data from CapitalIQ, CINT is currently trading at a multiple of 12.36x, while its peers trade closer to 14.0x. It is worth noting that Globant stands out with a valuation exceeding 20x. I believe the disparity in valuation can be attributed to the high Brazilian interest rate of 13.75% , which has been maintained since August 2022. However, there are indications that the Brazilian bond market anticipates a decline in interest rates, as evidenced by the more than 300 basis points drop in the 10-year bond yield since its peak in November. Looking ahead, if the Brazilian central bank decides to cut interest rates and investor appetite for Brazilian equity returns strengthens, I anticipate CI&T's valuation to move closer to an EV/EBITDA multiple of 15x.

Capital Structure and Liquidity Analysis

{kind=link}

{kind=link}

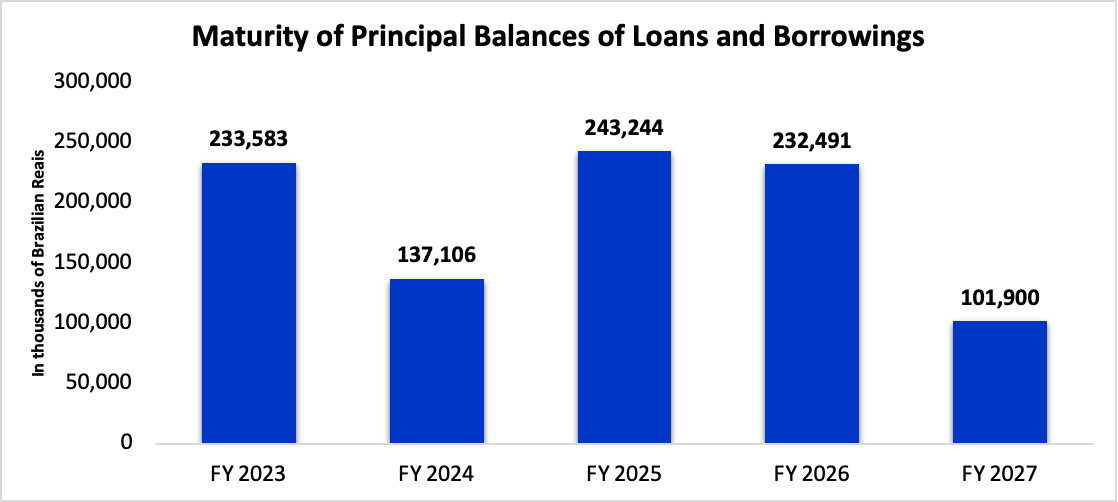

In the last Q1 report, CI&T disclosed upcoming obligations in 2023, including a debt maturity of R$233.58 million, lease liabilities of R$23.9 million, and accounts payable of R$72.4 million resulting from acquisitions. However, the company's liquidity position appears favorable with a balance of R$345.4 million, consisting of R$251.55 million from cash equivalents and R$93.88 million from financial investments. Considering these figures, I think that CI&T has sufficient liquidity to meet its short-term obligations. While the company's current financial condition may not be ideal, it is not in a significant financial crisis. The current ratio stands at 1.5x according to data from CapitalIQ. This indicates that CI&T has a reasonable level of working capital to sustain its operations even in challenging circumstances.

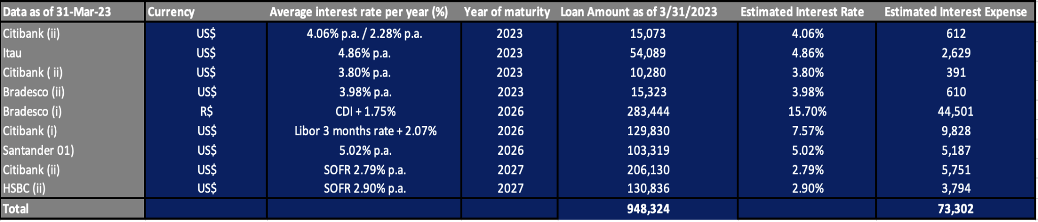

{kind=link}

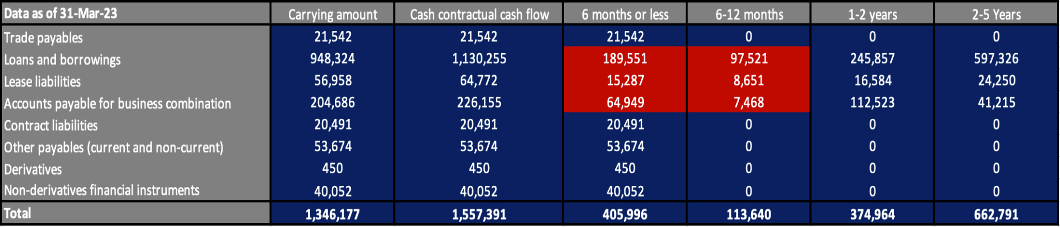

Based on the provided chart, the largest interest expense for CI&T is primarily attributed to its borrowing from Bradesco, which has been impacted by the high interest rates prevalent in Brazil. In contrast, interest expenses related to other debt obligations are fixed. However, despite the elevated interest expense, the forward EBITDA/Interest expense ratio, according to my base case scenario estimate, remains at a comfortable level of 5.6x. Therefore, there is no immediate cause for concern regarding the company's ability to cover its interest obligations. Looking ahead, I anticipate that the Brazilian Central Bank will cut interest rates within the next 6-9 months if inflation continues its downward trend, which can result in lower interest expense associated with the borrowing from Bradesco.

Financial Valuation

{kind=link}

{kind=link}

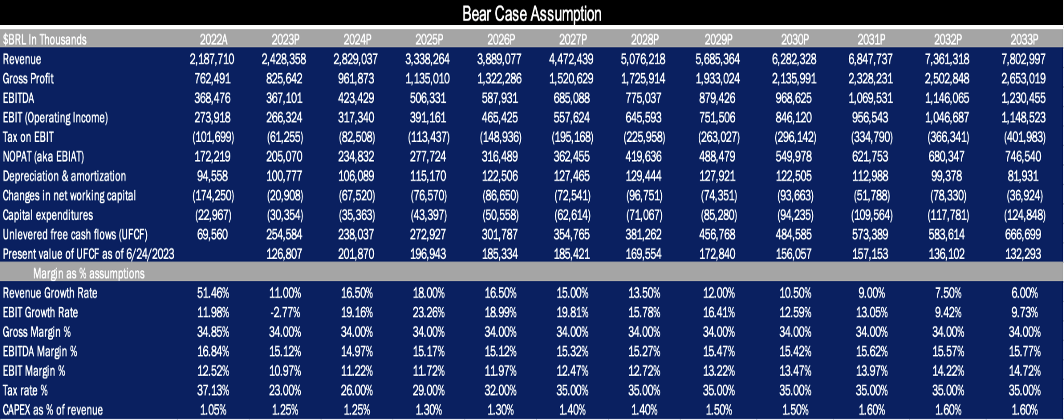

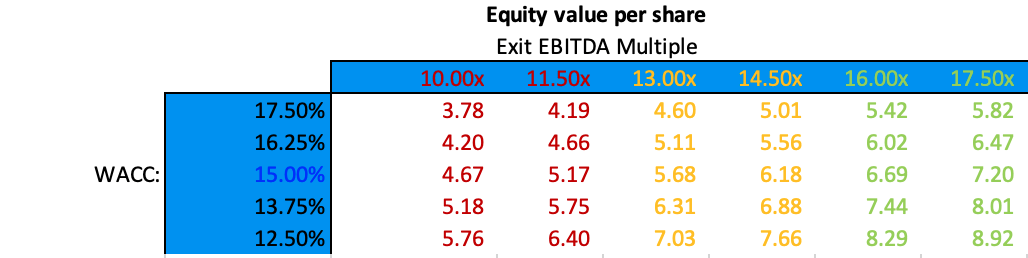

In my bear case scenario, I have formulated conservative assumptions regarding CI&T's revenue growth trajectory. I anticipate a slight deceleration in revenue growth due to a considerable slowdown in macroeconomic activity, particularly towards the end of 2023 when the impact of elevated interest rates fully manifests in the global economy. From 2024 onwards, growth is projected to gradually recover and reach its peak in 2025, subsequently decelerating by 1.50% annually as the company matures while growing a lot lower than the industry's growth rate. To account for potential challenges in the operating environment, I have adjusted the gross margin to be 1% below the historical average of 35%. Additionally, the EBITDA margin is expected to fluctuate between 15% and 16% due to higher selling, general, and administrative expenses, as well as operational inefficiencies. Given the prevailing economic conditions and associated risks, it is prudent to consider a higher discount rate. Currently, the risk-free rate in Brazil stands at 13.75%, indicating a higher premium for risk due to the country's unstable economic conditions. In terms of exchange rates, I have factored in an exchange rate of USD/BRL at 6.5, considering the massive depreciation of the Brazilian Real against the US Dollar over the past decade . Historical trends suggest fluctuations between 4.6 and 5.6 in the past two years. Taking a conservative approach, it is reasonable to expect further depreciation of the Brazilian Real against the US Dollar in the future within our bear case scenario. Assuming a discount rate of 15%, I expect the intrinsic value of CI&T's share to be anywhere between $4.67 and $7.20.

{kind=link}

{kind=link}

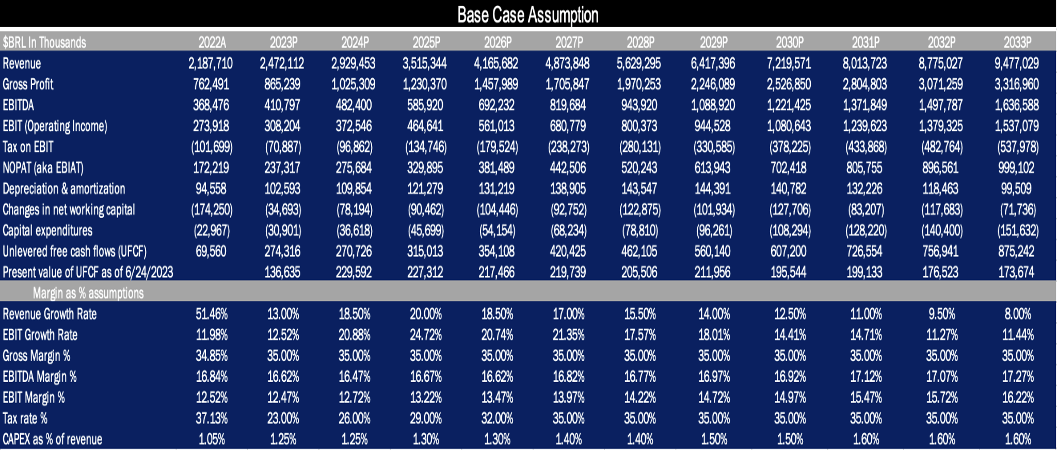

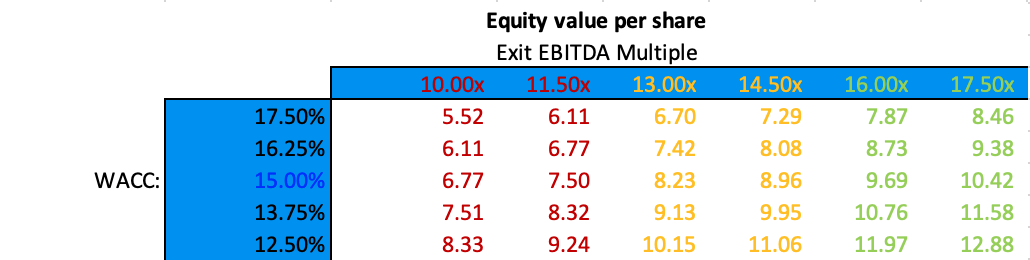

In my base case scenario, I have projected revenue growth for CI&T to be slightly below the industry's growth rate once the economy gains momentum and businesses resume their normal level of technological investment. The gross margin is expected to remain relatively stable, reflecting the company's current performance, while the EBITDA margin is anticipated to show a modest increase over time due to operational leverage, while maintaining a cautious outlook. Regarding taxation, I have factored in the short-term benefits derived from CI&T's acquisitions of companies in jurisdictions with lower tax rates, such as Dextra and NTERSOL. However, I assume the tax rate will eventually return to a more typical level of 35% since the majority of CI&T's business operations are still based in Brazil. Considering the exchange rates, I have utilized an exchange rate of USD/BRL at 6, taking into account the aforementioned factors and the historical trends discussed earlier. With a discount rate of 15% applied to the valuation, I estimate the intrinsic value of CI&T's shares to range between $6.77 and $10.42. This implies limited to no downside risk for investors while still presenting a meaningful upside potential.

{kind=link}

{kind=link}

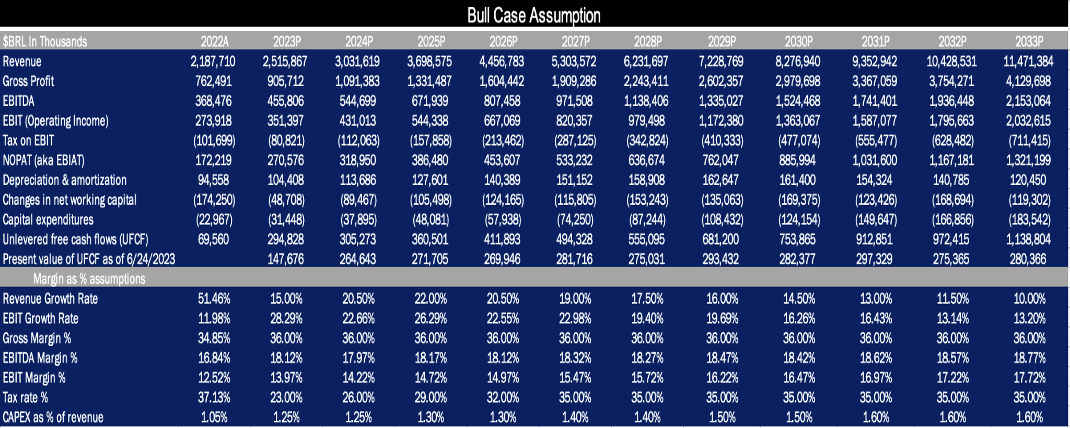

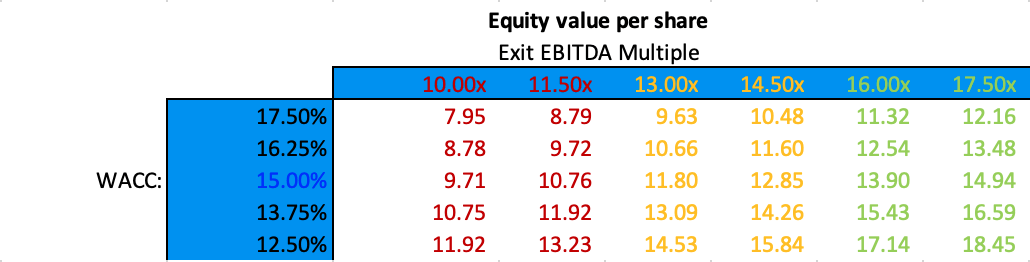

In my best case scenario, I anticipate CI&T's revenue to align more closely with industry expectations, reflecting improved market conditions and the company's ability to capture a larger market share. With favorable factors at play, such as a slowdown in wage inflation in Brazil and a more stable economic environment, CI&T is poised to achieve a top-notch gross margin of 36%. Furthermore, I assume that CI&T's management will effectively control its SG&A costs and capitalize on operational synergies resulting from recent acquisitions. This strategic approach is expected to drive operational leverage, leading to an expanded EBITDA margin of 18.77%, which is much closer to the company's historical performance prior to the multiple acquisitions. Regarding the exchange rate, I have considered the USD/BRL at 5.5, reflecting its proximity to the highest level observed within the past two years. By applying a discount rate of 15% to the valuation, I estimate the intrinsic value of CI&T's shares to range between $9.71 and $14.94 , which indicates a highly satisfactory return potential for investors, coupled with a significant margin of safety.

Main Risks

As the company operates in multiple countries, it is exposed to exchange rate fluctuations, particularly involving the Brazilian Real, which can have an impact when translated into its reporting currency. While the company achieved a 58% revenue growth in 2022 on a constant currency basis, the reported revenue growth shows a lower figure of 51%. In the second quarter of the fiscal year 2022 , the CFO mentioned that a $0.40 fluctuation in the FX rate can result in a 1% impact on EBITDA, either positive or negative, which further highlights the sensitivity of CI&T's financial performance to currency exchange rate movements. Therefore, I believe investors must be careful when considering investments in countries with unstable currencies like Brazil since unfavorable exchange rate movements can lead to reduced revenues when translated into the reporting currency and negatively affect the company's overall financial performance. Nevertheless, I expect the company to continue diversifying its revenue streams by expanding its presence in other geographies and reducing its reliance on a single currency over time.

In addition, CI&T operates in a competitive landscape that includes both digital transformation companies mentioned earlier and established traditional IT providers such as Accenture and Cognizant. These established players have longer operating histories and well-established reputations in the industry, which can pose challenges for CI&T in terms of attracting and retaining clients. Furthermore, I believe that the digital transformation industry is characterized by a relatively high degree of fragmentation and rapid change, which means that new entrants can easily enter the market and intensify competition. The low barriers to entry make it crucial for companies such as CI&T to continuously innovate, differentiate its offerings, and stay ahead of emerging trends to maintain a competitive edge.

Conclusion

In summary, CI&T represents an attractive long-term investment opportunity for investors seeking exposure to the Brazilian market and the rapidly evolving digital transformation industry. Despite the short-term challenges posed by economic headwinds and a slowdown in digital investments, I believe CI&T has demonstrated strong track record of client retention and a strategic focus on operational leverage and acquisition synergies. The company's ability to provide digital solutions that help businesses transform and adapt positions it well in the face of increasing technological change. Moreover, CI&T's undervalued status, with an estimated intrinsic value of $8.96, offers investors a significant margin of safety. While acknowledging the risks associated with the Brazilian market, investors who take a long-term perspective can benefit from CI&T's resilience and potential for multiple expansion. By capitalizing on its strengths and leveraging the opportunities presented by the evolving landscape, I believe the company has the potential to deliver substantial returns over time. Therefore, I recommend CI&T as a compelling long-term buy for investors who are willing to navigate the risks and capitalize on the company's strong fundamentals and growth prospects.

For further details see:

CI&T: Redefining Digital Transformation In Brazil And Beyond