CIOXY - Cielo's Profitability Persists Yet Volume Woes Loom

2023-09-27 08:44:36 ET

Summary

- Cielo's Q2 results show eighth consecutive quarter of profit growth expansion, with net profit increasing by 10.2% compared to Q1.

- Margins improved due to enhanced take rate of operations and implementation of new interchange rule for prepaid transactions.

- In any case, Cielo's shares have experienced a steep decline since August.

- Concerns arise over declining financial volume traded (TPV) and shrinking customer base, raising doubts about a strong recovery.

In my previous article on Cielo, I highlighted the company's path to recovery after hitting its lows early last year. Cielo implemented measures such as cost reduction, NPS improvement, and an increased presence in mid-tier businesses to achieve this. However, I also noted that macroeconomic headwinds, signaling a slowdown in the Brazilian economy in the year's second half, fierce competition, and growing turbulence in total traded volume cast doubt on the long-term investment thesis.

Cielo (CIOXY) released its second quarter results in early August this year. These mixed results marked the eighth consecutive quarter of profit growth expansion. However, they also revealed fragile volumes, raising doubts about the possibility of a more robust recovery throughout the year, especially as competition in the lucrative mid-tier customer segment intensifies, leading to a price war.

Since the announcement of its Q2 results, the market has been unforgiving with Cielo's shares, which have already dropped by a substantial 28%. This decline can be attributed to a combination of factors, including concerns about the financial volume traded (TPV) and a slowdown in the Brazilian equities bull market in August. This slowdown results from more adverse macroeconomic and microeconomic conditions than those encountered in the first half of 2023.

Net Profit and Margins: The Pretty Side

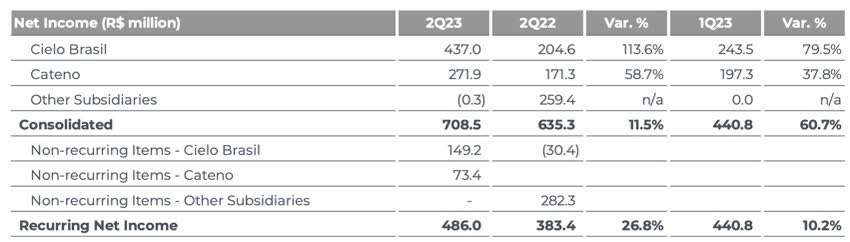

In the second quarter, the Brazilian payment services company Cielo reported relatively favorable and moderately positive results. Notably, Cielo achieved its eighth consecutive quarter of net profit expansion, reaching R$486 million, representing a 10.2% increase compared to the first quarter and a 26% increase compared to the same period last year.

{kind=link}

While Cielo has been emphasizing its commitment to maintaining profitability, it faces pressure from competitors willing to operate with lower or even loss-making margins, according to statements from company executives.

Estanislau Bassols, Cielo's Executive Director and CEO, stated during the company's earnings call :

"In the first half of the year, we implemented price adjustments, considering macroeconomic factors, costs, and the added value of our products. We believe these adjustments demonstrate a high level of rationality, and we remain committed to this approach."

Cielo achieved a Return on Equity ((ROE)) of 17%, representing a 1.1 percentage point increase compared to the first quarter and a 2.2 percentage point increase compared to the previous year's second quarter. The net profit also benefited from an extraordinary service tax ((ISS)) impact of R$223 million.

Notably, Cielo exhibited significant margin improvement, driven by an enhanced take rate of operations, which reached 1.16%. This reflects a 0.06 percentage point increase compared to the first quarter and a 0.24 percentage point increase year-over-year. This improvement is partly attributed to product repricing and implementing the new interchange rule for prepaid transactions, which became effective in the second quarter of 2023.

The growth in net income can also be attributed to Cielo's Q2 revenues. The company reported net revenue of R$2.6 billion, reflecting a 2.8% increase quarter-over-quarter and a 4.0% increase year-over-year. This growth was driven by a 13 basis point increase in revenue yield at Cielo Brasil, reaching 0.83%, its highest level since the first quarter of 2019. Additionally, higher volume and yield at Cateno contributed to this growth. The revenue comparison became more recurring from this quarter onward since Merchant-e Solutions was excluded from consolidation in the first quarter of 2022.

Total expenses in the quarter experienced a significant decrease, reaching R$1.4 billion, a 20.3% decrease quarter-over-quarter and a 9.7% decrease year-over-year. This reduction was primarily driven by an extraordinary reversal of the Services Tax ((ISS)), which will be elaborated on in a separate section. Considering total normalized expenses, excluding the remarkable event, the amount was R$1.38 billion, reflecting a 3.8% increase quarter-over-quarter and a 3.3% increase year-over-year.

Now, let's take a closer look at the results categorized by business units:

{kind=link}

Cielo Brasil

The segment reported net revenue of R$1.6 billion, representing a 3.6% increase quarter-over-quarter and a 4.3% increase year-over-year. This growth was influenced by the rise in revenue yield of 0.12 percentage points to 0.83%.

The new prepaid interchange rule and a slight price increase at the end of the first quarter 2023 contributed to this improvement. A combination of product mix and price increases boosted yield by 0.08 percentage points, while the new interchange rule and reduced taxes contributed an additional 0.04 percentage points.

Regarding expenses, total expenses (excluding extraordinary items) amounted to R$780.7 million, reflecting a 5.1% increase quarter-over-quarter and an 11.2% increase year-over-year. This increase was primarily driven by the hiring of the commercial team and a labor agreement that occurred at the end of 2022.

Cateno

The joint venture formed by Banco do Brasil ( OTCPK:BDORY ) and Cielo, responsible for Cielo's credit and debit card management business) reported net revenues of R$1.0 billion. This represents a 1.5% increase quarter-over-quarter and a 3.6% increase year-over-year, driven by improved yield due to a more favorable mix and volume expansion. Considering revenues from term products, Cielo achieved a take rate of 1.16%, reflecting a 0.06 percentage point increase quarter-over-quarter and a 0.24 percentage point increase year-over-year. This is the highest level since the first quarter of 2019.

Total expenses (excluding extraordinary items) amounted to R$603.3 million, reflecting a 2.0% increase quarter-over-quarter and a 5.5% decrease year-over-year. The increase was impacted by the growth in personnel expenses and expenses related to operational improvement projects.

Cielo's financial result (excluding prepayment) was negatively affected, amounting to R$682 million, reflecting a 2.3% decrease quarter-over-quarter and a 20.1% increase year-over-year. This negative pressure is primarily attributed to the high Brazilian interest rate (Selic), which currently stands at 12.75%, impacting the financial expense line.

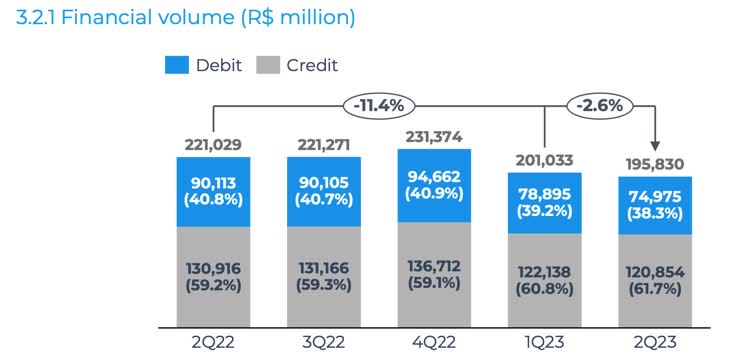

Financial Volume and Client Base: The Ugly Side

While the company made progress on both the top and bottom lines, there are concerning trends in the financial volume traded (TPV) and the client base, which warrant attention.

TPV amounted to R$195.8 billion, which reflects a 2.6% year-over-year decrease and an 11.4% decrease compared to the previous year. This decline is primarily attributed to reduced financial volumes for credit and debit cards, which decreased by 7.7% and 16.8% year-over-year, respectively.

{kind=link}

The shrinking active customer base contributes to this decline, with a total of 958,000 customers, marking a 5.6% year-over-year decrease and a 13.6% decrease compared to the previous year. This drop in the customer base is also reflected in the TPV for the quarter.

Cielo's Active Client Base (thousands) (Cielo's IR)

Cielo has continued to face challenges in the segment it prioritizes the most, the retail and small-business segment, which saw a decline of 1.5% year-over-year and a 12.3% decrease compared to the previous year, resulting in a volume of R$64 billion for the quarter. To address this decline, Cielo plans to hire an additional 400 to 1,000 new commercial agents, building on the 400 sales hunters hired at the beginning of the year, to reverse these losses.

In contrast, the large accounts segment experienced a more pronounced contraction in the quarterly comparison, declining by 2.9%. This is not surprising, as the company decided to give up its subsidized share in this segment.

Despite the significant drop in TPV, there has been an improvement in the mix between credit and debit cards. Credit cards, which yield better results, saw an expansion of 1 percentage point quarter-over-quarter and 2.5 percentage points year-over-year in the mix (credit/debit), reaching 61.7%. Additionally, total transactions did not follow the same downward trend as TPV, with a decrease of 2.1% year-over-year and 8.8% compared to the previous year.

It is also worth noting that Cateno's financial volume experienced relatively weak growth, increasing by 2.1% year-over-year and 2.0% compared to the previous year. However, this performance is better than the contraction seen in Cielo Brasil. Cateno's TPV reached R$100 billion, with a mix of credit and debit cards remaining relatively stable at 59.3% and 40.7%, respectively.

Cielo's IR

Attractive Yield Unchanged For 2023 and 2024

Cielo also announced the payment of R$196.97 million in interest on shareholder equity (JCP). This practice, specific to the Brazilian tax system and corporate finance, revolves around companies paying interest to their shareholders on the equity invested in the company, carrying distinct tax implications in Brazil. Unlike dividends, JCP is accounted for as an "expense" for companies, reducing taxable net income.

The company currently offers a dividend yield of 8.63%, which is 63% higher than its historical average. Cielo is expected to continue to deliver substantial dividends in the upcoming year, potentially achieving a yield exceeding 9% by 2024.

Currently, Cielo is distributing 34% of its profits, roughly 33% below its historical ten-year average payout.

{kind=link}

Brazilian Payment Services Market and Cielo's Valuation

Cielo maintains its position as the market leader in payment services in Brazil, holding a 23.9% market share, according to BTG Pactual. It is followed by Itaú Unibanco's (ITUB) Rede at 23.3%, Santander Brasil's (BSBR) GetNet at 15.1%, StoneCo (STNE) at 11.3%, and PagSeguro (PAGS) at 10.8%. However, the continued dominance of Cielo's market position today raises some concerns.

The second quarter for Cielo was marred by a negative trend in the financial volume transacted (TPV), further emphasizing concerns about client attrition during this period and the persistently challenging macroeconomic environment. According to the company's management, Cielo has faced competition from other players working with unprofitable models in the past, ultimately leading to market share losses, but customers have historically returned.

Despite significant progress in pricing and the adoption of prepayment products, TPV remained fragile, casting doubt on the possibility of a robust recovery this year, especially if competition escalates in the lucrative mid-tier customer segment through a price war. Cateno also reported weak financial volumes, resulting in a slowdown in profit expansion from 34% year-over-year in the first quarter of 2023 to 15.9% year-over-year in the second quarter of 2023.

Despite the pessimistic sentiment reflected in Cielo's market price, its valuation appears attractive. The company is currently trading at an appealing 4.30x P/E ratio for 2023E and 4.53x P/E ratio for 2024E. However, the absence of short-term catalysts and consistently weak volumes raise concerns that competition from other players like StoneCo and PagSeguro could intensify, even though Cielo is trading at a relative discount compared to its main peers.

In Conclusion

In summary, I would like to emphasize that, despite the substantial decline in Cielo's share price, which has further discounted its valuation, the indications of reduced growth in the payment services industry and increased competition, resulting in weak operational performance, suggest that a neutral stance on Cielo might be advisable.

For further details see:

Cielo's Profitability Persists, Yet Volume Woes Loom