CIOXY - Cielo Stock: Discouraging Long-Term Outlook Keeps Me On The Sidelines

2023-07-24 02:57:49 ET

Summary

- Cielo, a major creditor and payment processor in Latin America, faced declining margins in the last five years due to solid competition, the pandemic, and other factors.

- While Cielo demonstrated solid financial performance in the short term, a challenging macroeconomic environment and increasing competition pose obstacles to its long-term growth.

- Despite its discounted valuation and potential short-term gains, uncertainties surrounding Total Payment Volume (TPV) and market share losses suggest a cautious approach for investors in the long run.

Cielo ( OTCPK:CIOXY ) is one of Latin America's largest creditors and payment processors that, for a long time, held a monopoly on credit card machines in Brazil.

In the last five years, factors such as the arrival of solid competition, the pandemic, commoditization of services, low penetration of credit products, and lower cost efficiency have caused the company's margins to fall sharply. Cielo's shares went from $8 per share at the beginning of 2018 to below $1.

Since hitting its lows early last year, Cielo has recovered, canceling loss-making accounts, cutting costs, improving NPS, and increasing its presence in the profitable middle-tier businesses.

Cielo has a positive outlook in the short term, given the resumption of financial volumes, increase in products with embedded advances, credit, and potential divestments in subsidiaries. The discounted valuation may also yield some returns in the short term.

However, despite the more favorable operating environment, I see the macroeconomic condition as a growth impediment for Cielo, along with overwhelming competition and growing turbulence in total traded volume weighing on the investment thesis for the long term.

Cielo's latest financial results

Earlier this year, Cielo demonstrated a solid financial performance in its most recent earnings results, showing growth in revenues, profitability, and EBITDA margin and establishing efficient financial management and a strategy that inspires confidence in the market.

{kind=link}

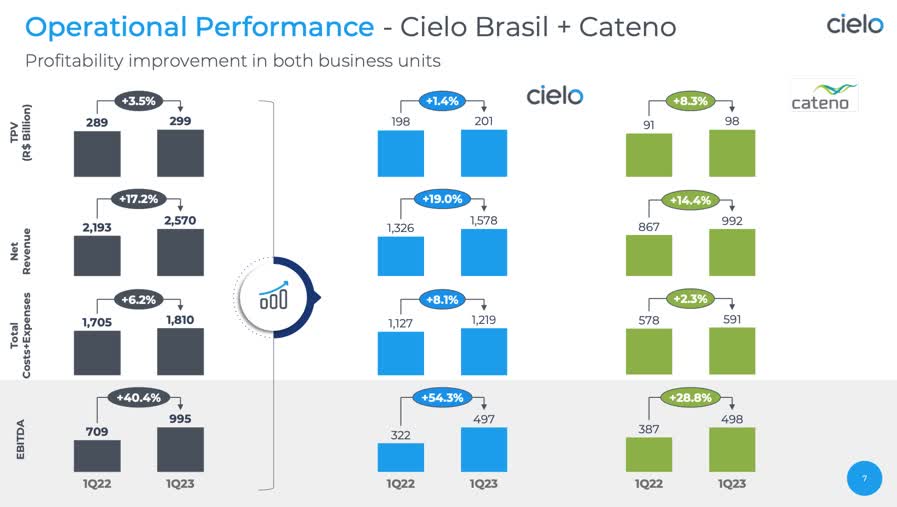

Revenues: The company achieved net operating revenues of R$2.57 billion in Q1 2023, an increase of 17.2% year-on-year. This growth was driven by increased volume and yield at Cielo Brasil and Cateno (its subsidiary).

Profitability: Cielo's recurring net income in the first quarter of 2023 was R$440.8 million, representing a significant growth of 85.1% compared to Q1 2022. Recurring EBITDA in Q1 2023 was R$994.9 million, up 40.4% from 1Q22. This is the highest result for the first quarter since 2018. EBITDA margin also improved, reaching 38.7%, with a gain of 6.4 percentage points compared to Q1 2022.

Cash and cash equivalents: The company closed the quarter with R$2.35 billion in cash and cash equivalents, which represents a decrease of R$1.16 billion compared to the first quarter of 2022, but an increase of R$181 million compared to the previous quarter. In addition, Cielo had R$6.43 billion in loans and financing at the end of the Q1 2023.

Cielo will report its second-quarter results in early August. The company is expected to report EPS of 0.05 and about R$2.91 billion in revenues, where the financial result may come in slightly better than in the first quarter. The revenue from receivables anticipation may show a slight QoQ growth.

In addition, according to the company, the forecast of a drop in the basic interest rate (Selic) should reduce financial expenses in the order of R$150 million for every 1 p.p. reduced.

Better margins but weaker volumes

Despite the positive results during the first quarter of the year, which showcased a significant recovery in Cielo's profit margins, the recent investor meeting shed light on more challenging prospects for Total Payment Volume (TPV).

At the beginning of the year, Cielo expected a TPV growth between 10% and 12% YoY for the industry, below that projected by the Brazilian Association of Credit Card Companies (ABECS) and Services of 14% to 18% YoY.

With this, Cielo has a more conservative view of the future, emphasizing that it does not see a recovery in volume growth in the very short term - some of the factors behind this more conservative expectation of the fall in the Brazilian retail industry.

Weaker consumption is related to banks' restrictions on credit supply, which have reduced limits and card issuance, in addition to the Pix (a Brazilian instant payment system) that replace debit and credit operations, and the macroeconomic deterioration, such as the high household debt . Currently, 80% of Brazilian households have debt, with 30% defaulting. In addition, household debts represent about 33% of the national GDP.

Cielo presented a TPV growth below the industry in the most recent quarter. According to ABECS data, the TPV reported by the market in Q1 2023 was 10.7% YoY, while Cielo's was only 1.4% YoY.

Cielo's Investor Relations

This weaker TPV growth than the market can be seen in the drop in large accounts and SMBs, as it is the company's focus segment at the moment and is where it manages to generate the most profitability - turning on a warning sign for the company's profitability in the long run.

Competition is increasingly suffocating Cielo

I believe Cielo has correctly shifted its focus to profitability rather than market share. Currently, the company holds 24% of the market (down 2% YoY). The decline in market share should continue with Cielo as it suffers in delivering some differentiator to hold its share versus solid competition.

Over the past few years, Cielo's strategy of focusing on small businesses has helped boost its revenues, achieving four consecutive quarters of year-over-year growth. In Q1 2023, Cielo reported a revenue yield of 0.78% increasing 12 bps YoY.

However, as there has been a reduction in Cielo's share in small businesses, this is another warning sign as Mercado Pago - a fintech arm of MercadoLibre ( MELI ) - emerges, which is starting to look at the small business sector (although looking at the bottom of the pyramid of the segment) and the expansion of Rede, belonging to Itaú ( ITUB ) bank - one of the largest in Brazil - in the small business market, where it has as a competitive differential the integration with the bank's acquiring system.

There is also the possibility of Mercado Pago and Rede lowering their prices to gain more market share, which should mean that Cielo may also have to impact its margins not to be left behind in its focus segment.

These are significant challenges for Cielo to face in the long term, where growing its customer base should become increasingly tricky. Consequently, this should impose pressure on optimizing its revenue generation.

Valuations reflect the bearishness

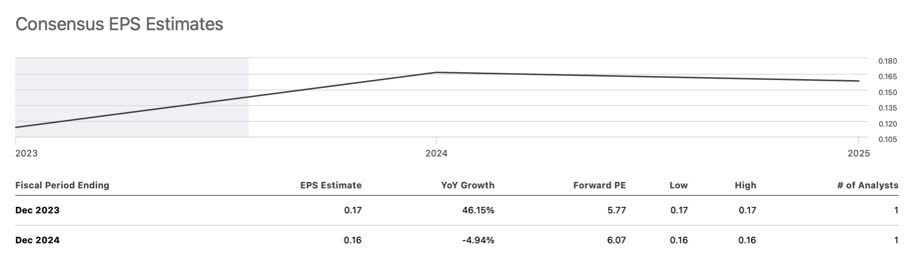

Considering that Cielo currently trades at a price-to-earnings multiple of 5.7 times in 2023, which is approximately 42% below the industry average, it becomes evident that the market has little faith in the company's long-term prospects.

Although there is an estimate of almost 50% EPS growth by the end of this year, reaching $0.17, the consensus for 2024 indicates that EPS is expected to be $0.16, resulting in the company still trading at a forward P/E multiple of 6 times, which remains discounted.

{kind=link}

On the other hand, the discounted valuation may draw the attention of investors and controlling shareholders, potentially leading to Cielo going private and delisting from the public stock exchange. The company's shareholder composition includes two of Brazil's largest banks: Bradesco ( BBD ), holding 30.1% of Cielo's shares, and Banco do Brasil ( OTCPK:BDORY ), holding 28.6% of the company's shares.

With the current stock trading at a discounted price compared to its earnings and the industry average, investors and the controlling shareholders may see an opportunity to acquire more shares or even take the company private. Such a move could give them greater control and benefits from a potential recovery in Cielo's fortunes in the long run.

But, of course, despite being a risk to the bearish thesis, this is still a purely speculative factor.

The bottom line

Cielo is certainly not a bad company, but it has fallen far from the level of success it enjoyed in the not-so-distant past.

The investment thesis for Cielo does not appear to be very exciting, primarily due to the low long-term growth trend in its core business. Additionally, the company faces constant competition in its core segments, and the high-risk Brazilian macroeconomic scenario with increasing defaults and high household indebtedness adds further pressure.

On the other hand, Cielo's strategy of focusing on its core business to increase financial volumes and expand its product portfolio to include features such as anticipation and credit, as well as considering potential divestments in subsidiaries, may help the company improve its discounted valuation in the short term.

However, in the long-term outlook, the company is experiencing a loss of market share and challenging prospects for Total Payment Volume (TPV), raising doubts about whether the profitability-focused strategy will be successful.

Overall, although Cielo may have some potential in the short term due to its strategic initiatives, its uncertainties and challenges call for a cautious approach in the long run.

For further details see:

Cielo Stock: Discouraging Long-Term Outlook Keeps Me On The Sidelines