CI - Cigna: A Defensive Stock With Multiple Avenues For Growth

Summary

- As inflationary pressures continue to mount, I see healthcare as a defensive industry, with the 1Y returns for XLV (-0.04%) being superior to SPY (-17.49%).

- With their Evernorth platform, Cigna is accelerating vertical integration, moving beyond the traditional financing model for health insurance and focusing on servicing.

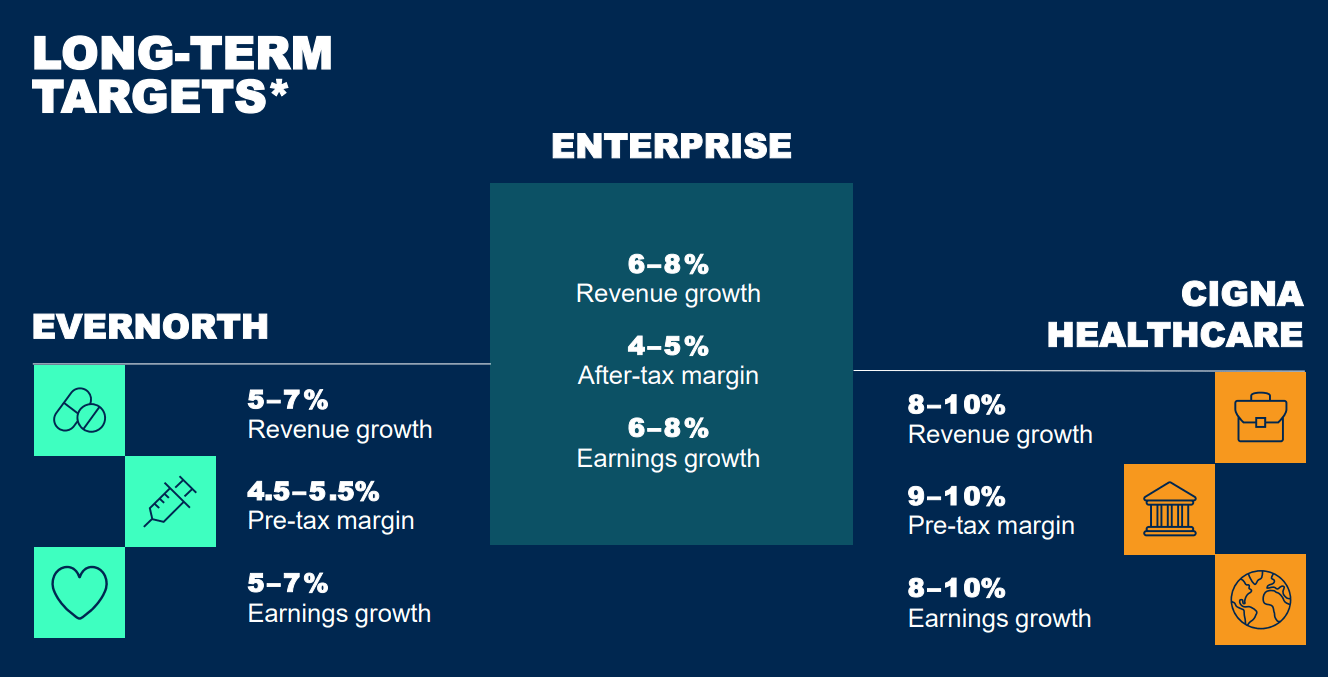

- Evernorth's earnings, which include Pharmacy Benefit Services, Specialty Pharmacy, and Care Services, are expected to grow at 5-7%; this is versus Cigna's Healthcare product, expected to grow at 8-10%.

- To achieve these targets, Cigna plans to deploy $10bn in capex, leveraging broad healthcare trends (digitalization, gene therapy, etc.) via their suite of brands and products.

- That is why I believe Cigna is a long-term buy; they are a forward-looking enterprise with the capabilities required to act upon shifts in the healthcare landscape.

As a healthcare company, I believe Cigna Corporation (CI) sustains a defensive position amidst the volatilities which plague the market, though, more so than that, it has established itself in a superior position to capture broad market growth across different product segments and geographies.

Investment Thesis

My long-term, bullish outlook on Cigna hinges upon the growth of their US Government and International Health segments, the ability for Cigna to capture broad healthcare trends, and accelerating development and deployment of their integrated businesses.

Even in the short term, I believe that Cigna, as a pure healthcare play, will outperform the market in inflationary and recessionary environments as they often do. Addressing these macroeconomic concerns, the company has focused on affordability and accessibility to grow market share.

{kind=link}

Cigna (Blue) vs. SPY (Orange) (tradingview.com)

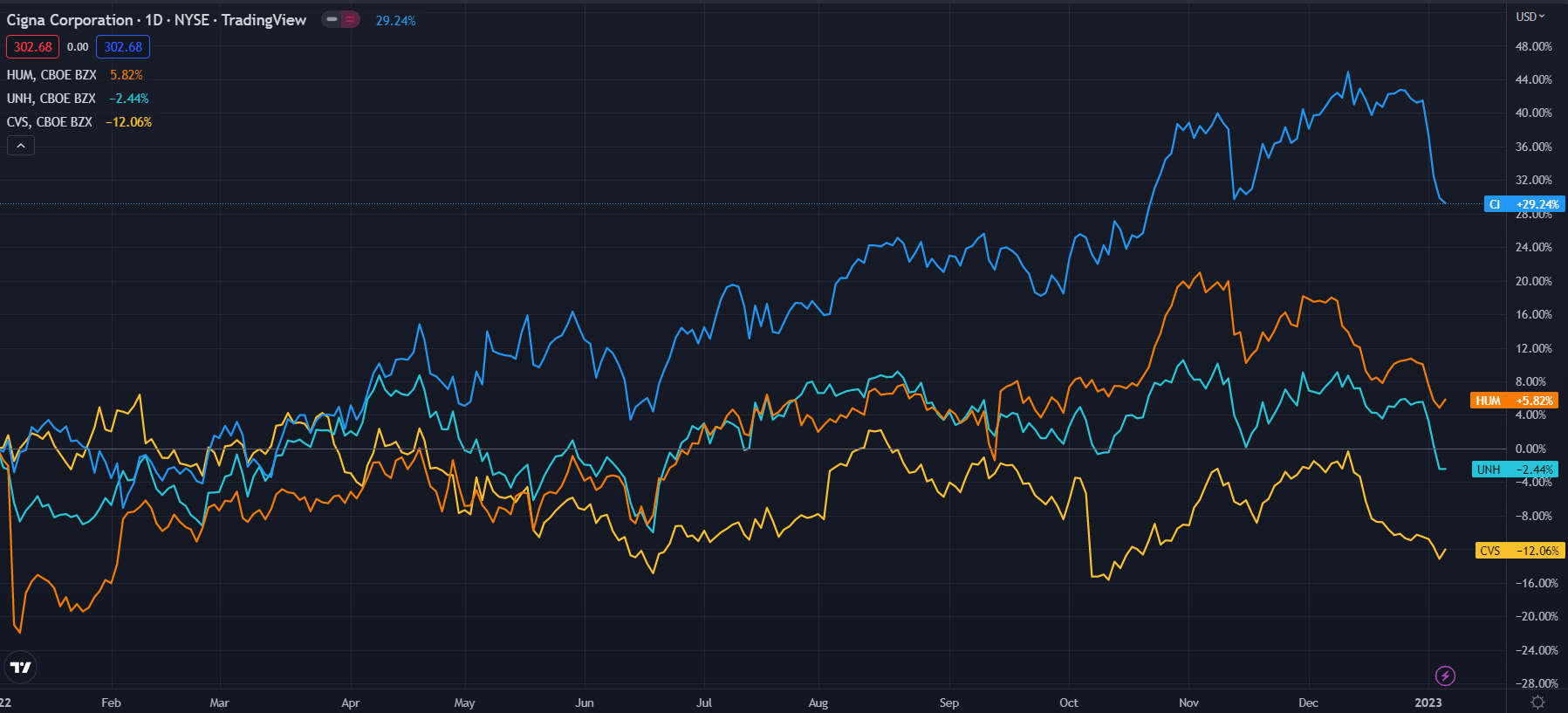

And this strategy has paid off. We can see here how, in spite of the headwinds affecting the wider market, Cigna's stock has performed fairly well.

As such, my analysis suggests that Cigna's long-term focus on streamlining and expanding their core businesses, the accelerated development of their smaller businesses, and their ability to capitalize on healthcare trends sets the company apart from competitors.

Introduction

Cigna is a global health services company and the third-largest American insurance company by market cap. The company sustains more than 190 million consumers, operating in more than 30 countries, with TTM revenues totalling $180.3bn, alongside a TTM net income of $6.62bn.

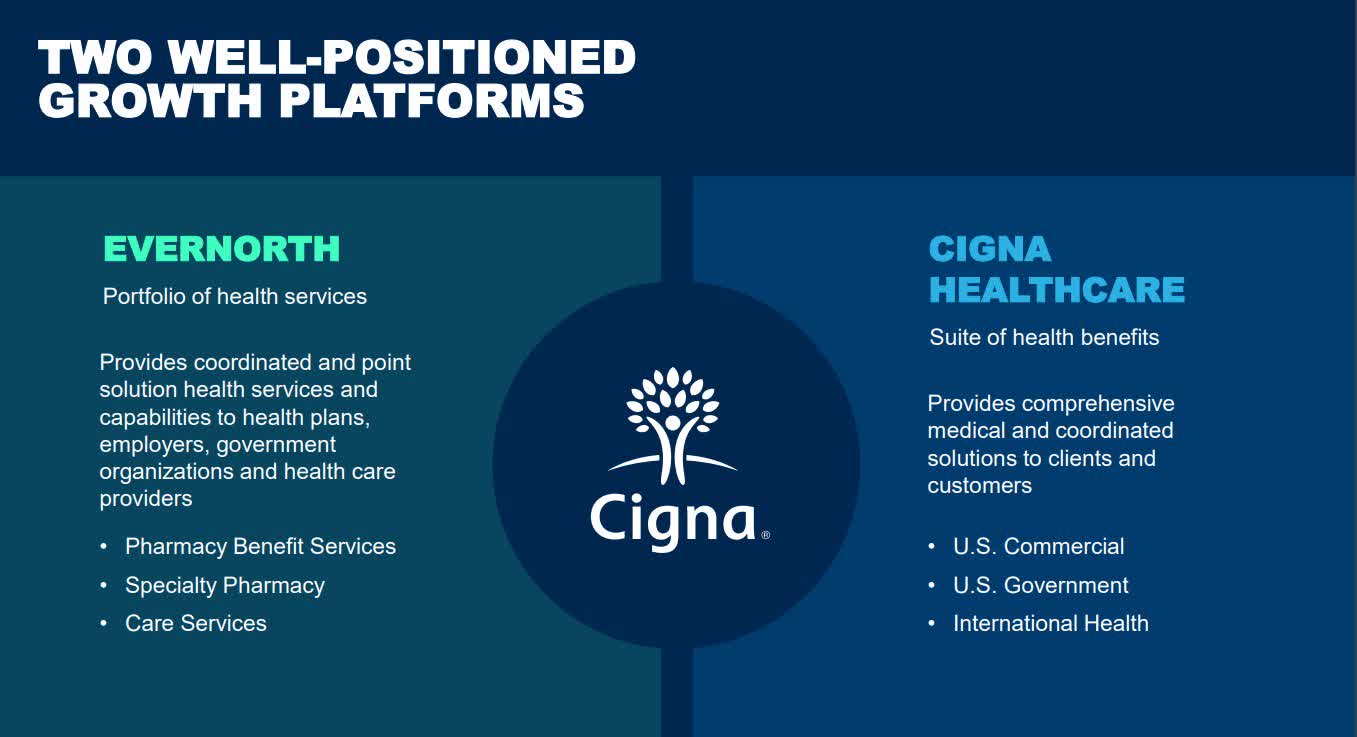

On a fundamental level, the company is comprised of two distinct aspects, Evernorth and Cigna Healthcare, with Cigna segmented into pharmacy revenues (Q3: $32.76bn), premiums (Q3: $9.59bn), and fees/other revenues (Q3: $2.73bn).

{kind=link}

Cigna Investor Presentation

Cigna maintains a significant geographic concentration across the United States, though they have made efforts to expand across the Americas and Europe.

Valuation & Financials

General Overview

Despite coming off an ATH of $340.11, currently, at $302.68, Cigna has appreciated nearly 30% over the past year, versus the XLV healthcare index, which is down 0.04%, and the SPY , down 17.49%.

Evading the consequences of COVID-19, inflation, and the Russian Invasion of Ukraine amongst economic issues, Cigna's business models' resilience is demonstrated through their current price-cash flow ratio of 8.64 and strong solvency, with a debt-assets ratio of 0.23. Annual revenues have additionally grown consistently over the past few years with Q3 pretax income growing 69.55%- yet another surprise for analysts.

For me, none of these results have come as a surprise; though Cigna returns a 1.48% dividend and has most recently announced a $3.5bn share repurchase program, the company is focused on organic growth through high levels of capital expenditure.

Comparable Companies

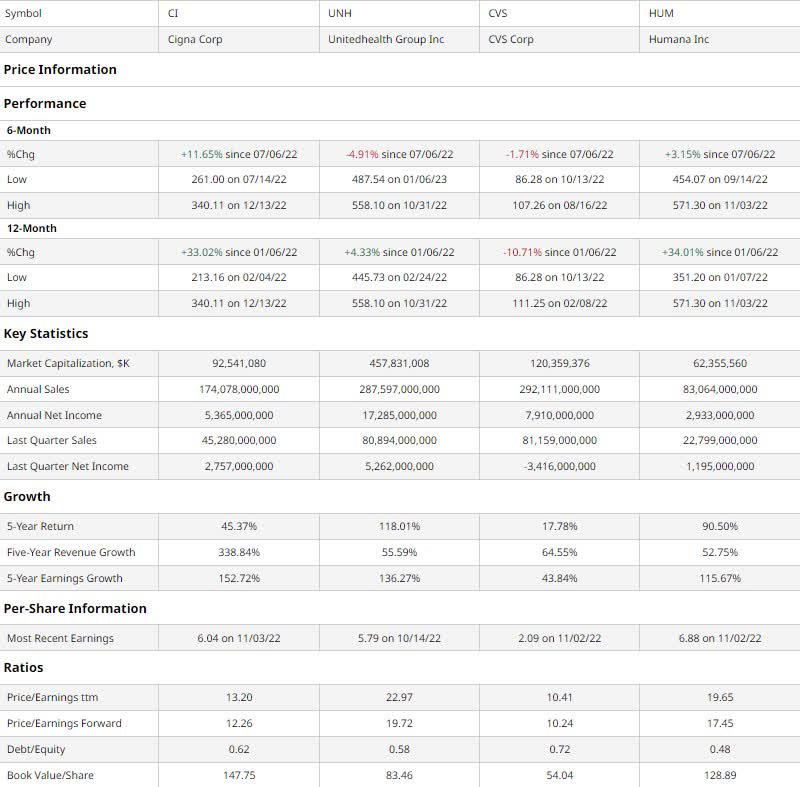

In an era of increasing consolidation , the healthcare market is progressively becoming dominated by larger competitors, with the UnitedHealth Group (NYSE: UNH ) accelerating whole industry vertical integration- particularly with their Optum segment, CVS Health Corp. (NYSE: CVS ) recently purchasing Aetna to expand from pharmacies to health insurance as well, and Humana (NYSE: HUM ), while more concentrated, reinforcing their superior role as a Medicare insurance provider.

{kind=link}

barchart.com

As we can see above, Cigna has weathered macroeconomic turbulence significantly better than its peers, experiencing superior quarterly growth than all and yearly growth than all but Humana, which, due to its relatively smaller size, faces greater volatility.

Though Cigna's acquisition of Express Scripts in 2018 obviously contributed to the exceptional revenue growth- albeit inorganic- it is the margin expansion that Cigna has been able to extract over the past 5 years which is of note. The company has produced significant synergies with subsidiary companies and is continuing to accelerate this process with its vertical integration strategy.

Again, Cigna is second-best amongst Humana when it comes to EPS, though I believe Cigna's share price has not priced in this growth as Humana's has, looking at Cigna's lower TTM and forward P/E.

Additionally, the company has a greater book value per share, indicating high levels of shareholder equity.

{kind=link}

Cigna (Dark Blue) vs. Competitors (tradingview.com)

Therefore, I see Cigna as the best bet amongst US health insurers, as they have proven themselves both with historic growth and greater future potential.

Valuation

According to my DCF calculations, at its base case, Cigna is undervalued by nearly 23%, with its fair value being ~$392.68. The model assumes a discount rate of 9%, over a forecast period of 5 years, and variable net margins hovering at 4% plus or minus a few basis points due to the unpredictable nature of Cigna's business. The DCF was done on an unlevered basis.

Walking through the model, it assumes a discount rate of 9%; Cigna's WACC is approximately 6% , though, in light of greater rate and equity volatility, assuming a discount rate of 6% would be disingenuous, thus the 3% added discount rate.

It additionally supports a >4% net profit margin to calculate accurate cash flows, predicated upon an average between Cigna's mean EBITDA margin and mean net income margin over the past decade, while removing induced volatility of 2020.

Relative Valuation (AlphaSpread)

Similarly, using a relative value analysis through AlphaSpread's tools- employing P/S, P/E, P/B, and Price/Premiums multiples, we can estimate the undervaluation of Cigna by nearly 37%, with its fair value thereby calculated to be 478.50.

Thus, using a mean figure, Cigna should be valued at ~435.59, or 30% above its current price figure.

Corporate Strategy

Core, Vertical Business Expansion

Cigna has developed a laser-focus on their healthcare products in the past few years, with aggressive acquisitions of healthcare businesses such as the pharmacy benefit manager Express Scripts and the sales of life, accident, and supplemental benefits segments of their company to Chubb. Since the healthcare industry, owing to an ageing population, innovations, etc. is growing at a faster pace than other markets, Cigna will be able to capture greater sales.

At the heart of Cigna's vertical integration strategy is the consolidation between Evernorth and Cigna Healthcare, with Evernorth encompassing a suite of healthcare services and Cigna Healthcare involving the offerings of US Commercial, US Government, and International Health businesses. The ability for Cigna to homogenize healthcare financing and products with relatively low debt- as compared to CVS Health, for example- is a key differentiator, as it enables margin expansions while enhancing the capacity for price competition. Moreover, US consumers tend to prefer integrated healthcare offerings due to lower costs .

While augmenting consumer accessibility and corporate profitability, vertical synergies facilitate companies in adapting for future trends, as Cigna, for instance, will retain the ability to shift entire healthcare supply chains toward the problems of the future and ensure continuity of care.

Capitalizing on Overarching Trends

Only thanks to the success of Cigna's efforts in vertical integration do I maintain that the company sustains an edge in capitalizing on emerging healthcare trends. Pharmacy benefit management ((PBM)) has become one of Cigna's largest businesses- and fastest growing; the PBM market is expected to grow at a CAGR of 8.77% versus the wider healthcare market at 7.93% .

{kind=link}

Cigna Investor Presentation

As healthcare services, provided by Evernorth, have eclipsed Cigna's insurance businesses in revenues, so too, has the need for constant, organizational transformation. David Cordani, Cigna CEO, outlines three priorities: the acceleration of pharmacological innovation (specialty pharma, gene therapy, vaccines), the synthesis between mental and physical health, and growing access to care models, particularly across digital channels.

Cigna has invested billions in capturing these trends, with Cigna's telehealth platform, MDLIVE, leading the way. This has aided the creation of products such as low-cost, virtual-first health insurance plans.

Wall Street Consensus

My positive opinion of the stock is echoed by analysts, who forecast an average one-year price increase to $362.82, up from $302.68 today.

{kind=link}

tradingview.com

Even at the minimum projected price of $335.00, there is significant price appreciation (+10.68%), which sidesteps general market sentiment and delivers value to shareholders in a period of high economic turbulence.

Risks

High Competition Market:

The healthcare industry is highly dynamic; significant shifts in industry structure or product developments could affect Cigna's ability to retain or attract consumers. Failure of the company to anticipate and adapt to constant evolution could negatively impact its competitive position. High levels of competitive intensity additionally indicate potential price competition, which may harm margin size.

Multi-faceted business:

Cigna's growing vertical nature and expansive size make it beholden to many stakeholders. If their PBM business loses relationships with key pharmaceutical manufacturers or if insurance pricing benchmarks shift, Cigna's financial performance and attractiveness to consumers could be materially impacted.

Global Risk:

Healthcare as a whole is one of the most highly regulated industries in the world. As Cigna expands its geographic footprint, it also grows its exposure to political, legal, operational, regulatory, and economic risks that may adversely affect multinational operations. For instance, price controls enacted by governments, currency fluctuations, data protection, etc. all increase company vulnerability.

Conclusion

In the short term, I see Cigna as a solid defensive stock, by virtue of the strong performance of healthcare companies during both inflationary and recessionary periods and Cigna's uniquely accommodative position within that market.

In the long term, I conclude that Cigna's chronic relative undervaluation, investments in accelerating vertical integration and streamlining core businesses, and ability to capture growing healthcare markets will be integral to share price appreciation beyond that of peers and the broader market alike.

For further details see:

Cigna: A Defensive Stock With Multiple Avenues For Growth