CI - Cigna: A Great Value Pick

2023-04-20 02:08:14 ET

Summary

- Cigna has already dropped over 20% year to date.

- The company's emerging segments have huge market opportunities and should drive growth moving forward.

- The current valuation is significantly discounted compared to both peers and its own historical average.

- I rate the company as a buy.

Investment Thesis

Cigna ( CI ) has been a steady compounder in the past decade with shares up nearly 300%, comfortably outpacing the S&P 500 Index ( SPY ) which was up only 160%. The company got off to a slow start this year with shares down nearly 20% and I believe this offers a great buying opportunity for investors.

While the growth of the company’s core segments is slowing as they mature, emerging segments such as specialty pharmacies are expected to expand rapidly and should drive growth moving forward. Its ongoing share buybacks should also provide solid support for EPS figures. The company's current valuation is significantly discounted compared to peers and should present decent upside potential. I like the risk-to-reward ratio at the current price level therefore I rate CI stock as a buy.

Emerging Growth Opportunities

Cigna is a US-based managed healthcare company that provides PBS (pharmacy benefit services), health insurance, and other health-related services to over 200 million customers across the globe. The growth rates of the company's core segments such as PBS have been moderating, but emerging segments including specialty pharmacies and biosimilars should present huge growth opportunities. The company has a strong presence in the specialty pharmacy space thanks to Accredo, which was acquired under the Express Scripts deal in 2018. The subsidiary provides specialty pharmacy services to patients with complex and chronic health diseases such as Cancer and HIV.

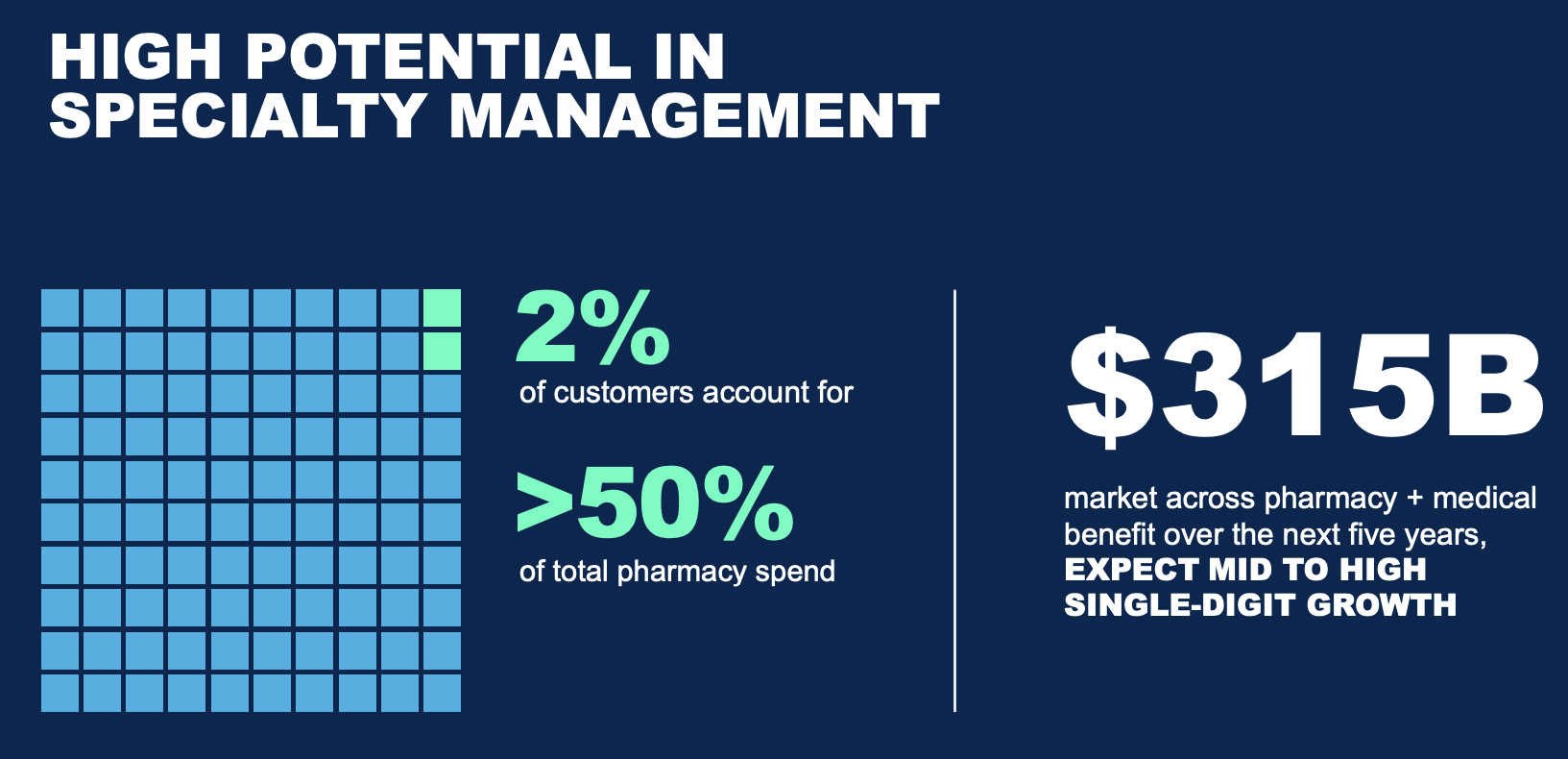

The market size of specialty pharmacies is massive as their costs are significantly higher than generic pharmaceuticals. For instance, their customers only account for 2% of the market, yet they account for over 50% of total pharmacy spend. According to Cigna , the market is estimated to grow from $190 billion in 2023 to $260 billion in 2026, representing a solid CAGR (compounded annual growth rate) of 11%. The growth is driven by the ongoing increase in chronic and complex diseases. The company should be well-positioned to benefit from the ongoing market expansion as Accredo currently has a market share of 25%. They also have access to 75% of limited and exclusive distribution drugs, which presents a much more complete offering compared to competitors.

{kind=link}

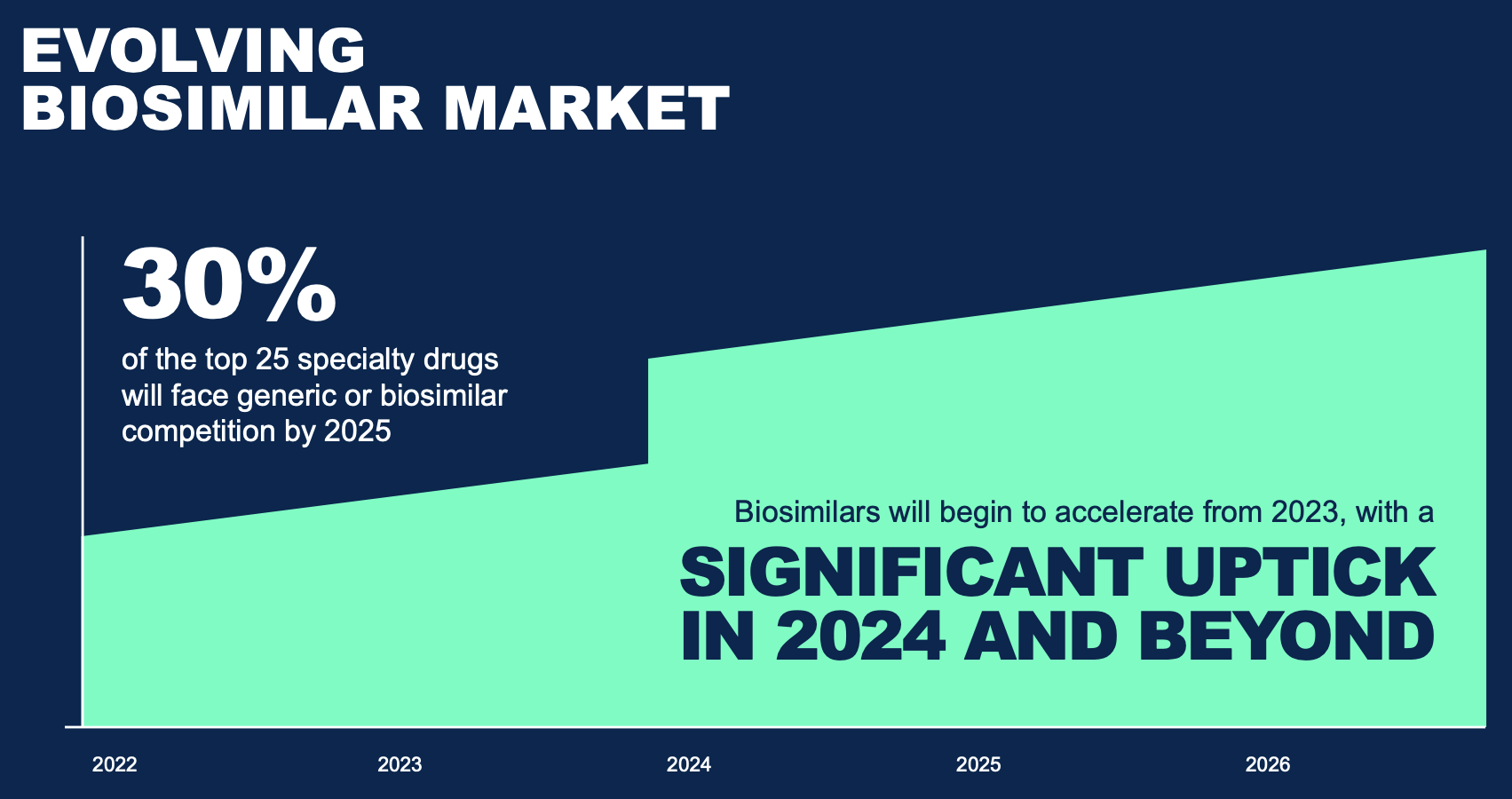

Biosimilars are another compelling growth opportunity. Biosimilars are clinical equivalent but lower costs alternatives for branded biological drugs. According to Markets and Markets , the market size of biosimilars is forecasted to grow from $15.6 billion in 2021 to $44.7 billion in 2026, representing a strong CAGR of 23.5%. The market is growing rapidly due to Biosimilars' much greater affordability, as their prices are usually 15% to 35% lower compared to the original branded drug, according to NCSL . Biosimilars currently account for roughly just 7% of specialty drug spend, and Cigna expects the figure to reach over 25% by 2026. Both specialty pharmacies and biosimilars are huge and fast-growing markets and I believe the two segments will be major growth drivers moving forward.

{kind=link}

Buybacks and Dividends

Another reason why I like Cigna is because of its shareholder-friendly capital allocation. The company has been buying back shares consistently and the number of shares outstanding has declined 21.8% from 380 million to 297 million in the past four years, as shown in the chart below (the huge jump in 2019 is caused by the acquisition of Express Scripts). The ongoing share buybacks are highly accretive to financials and are expected to contribute 400–500 basis points to EPS (earnings per share) growth annually.

After paying down some of the debt from the Express Scripts acquisition, the company significantly boosted its quarterly dividend from $0.01 to $1 in 2021. It has further increased the dividend by double digits in the past two years and the quarterly payout is now $1.23, representing a dividend yield of 1.77%. I believe double-digit increases should be sustainable in the mid-term, as the current payout ratio remains very low at just 19.3%.

Cheap Valuation

As a steady compounder, Cigna’s current valuation looks very attractive in my opinion. The company is trading at a PE ratio of just 12.1x, which is meaningfully lower than other managed healthcare companies including Humana ( HUM ), Elevance Health ( ELV ), and UnitedHealth Group ( UNH ). As shown in the chart below, the group has been trading at a similar valuation historically but the trend has recently diverged. Cigna is now trading at a substantial 45% discount compared to its peer’s average P/E ratio of 22x. The company is also cheap on a historical basis, as the current multiple represents a 15.4% discount compared to its 5-year average P/E ratio of 15.4x. The discount seems unjustified as the company continues to execute and is expected to generate durable double-digit EPS growth.

Investor Takeaway

I believe Cigna is currently attractively priced. The growth of their core segments has slowed but the emerging segments have huge market opportunities and should be able to boost the overall growth rate. According to the management team, this alongside the ongoing buybacks should translate to a long-term EPS growth of 10% to 12%, which is very decent. The current valuation seems way too discounted considering its solid fundamentals and double-digit growth rate and should present meaningful upside as the multiple reverts back to peers' average. Therefore I rate Cigna as a buy.

For further details see:

Cigna: A Great Value Pick