CI - Cigna: Buy This Value Gem Before It Bounces Back

2023-06-12 08:30:00 ET

Summary

- Cigna is a global health insurer with strong revenue growth potential from its pharmacy benefits manager and insurance segments.

- The company has a solid capital allocation strategy, including business reinvestment, dividends, and share buybacks, which are highly accretive at its current discounted valuation.

- Cigna's stock could deliver potential double-digit annual total returns over the next couple of years, making it an attractive option for value and growth investors.

Asset-light, cash rich companies can make great portfolio diversifiers, especially for their income and total return prospects. With the market seemingly chasing high growth names, a number of insurance companies are now again trading in value territory.

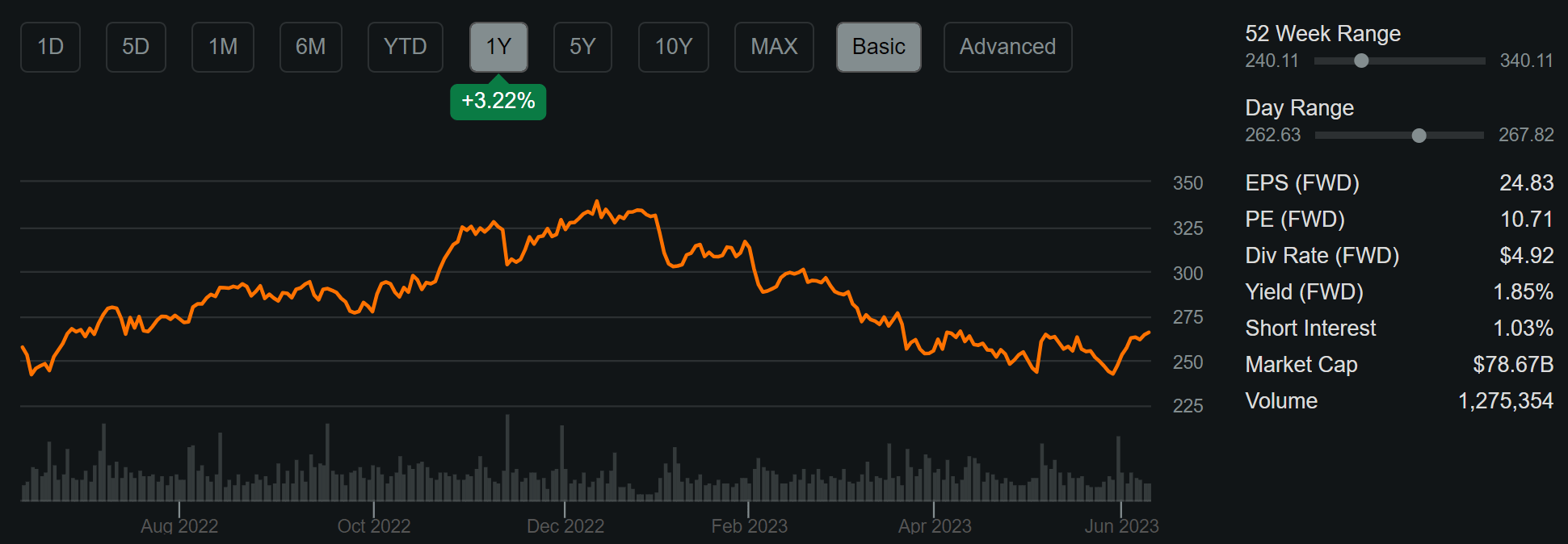

This brings me to Cigna ( CI ), which I last covered here back in July of last year. The stock since had a decent run to $340 before falling back to the $265 price at which I recommended it last year. In this article, I provide an update and discuss why the stock is a bargain for total returns investors at present.

{kind=link}

Why CI?

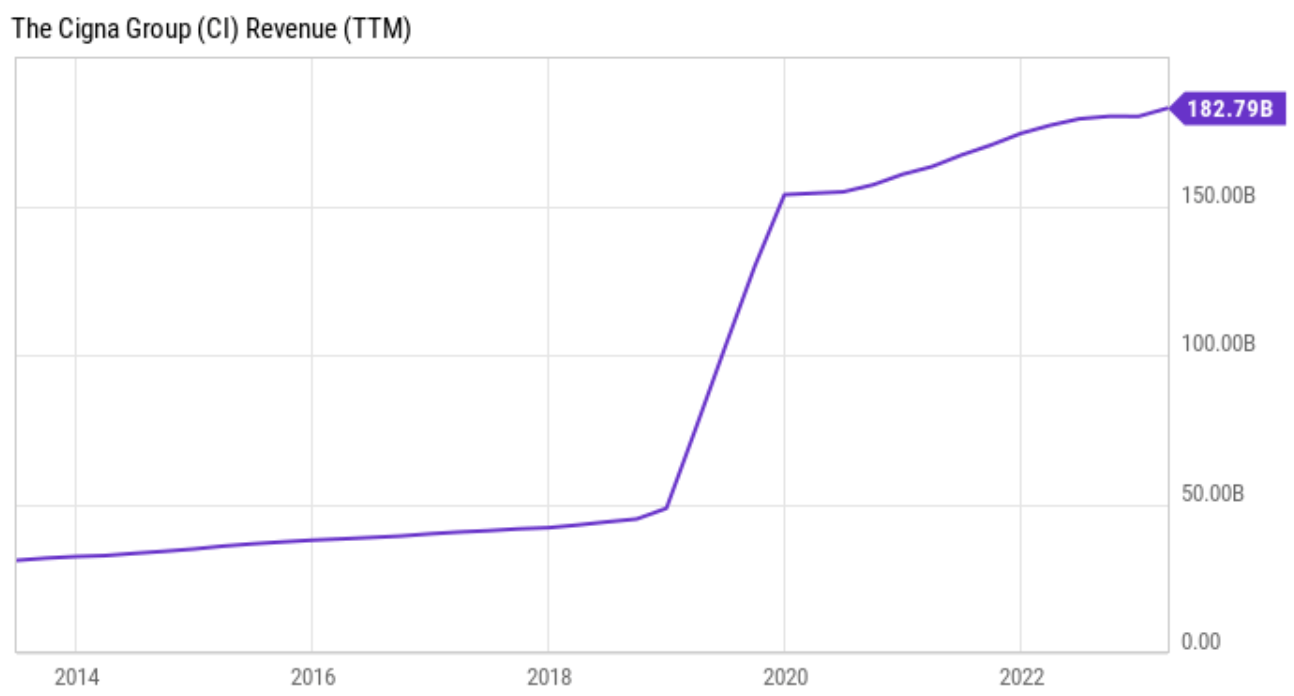

Cigna is an S&P 500 ( SPY ) company and is one of the largest global health insurers on the market. At present, it has over 165 million customer relationships and operates in 30+ countries around the world. Over the trailing 12 months, CI generated $183 billion in total revenue. As shown below, has grown its revenue over the past 10 years, including in the recent years post its acquisition of Express Scripts.

{kind=link}

CI benefits from a strong labor market, and this is reflected by total revenues growing by 6% YoY during the first quarter. This was driven in part by strong 8% revenue growth by Evernorth Health Services, which is CI’s pharmacy benefits manager that was once Express Scripts.

A key reason for the PBM’s growth is the increase in biosimilars on the market, such as those for the previously number one drug, Humira, from AbbVie ( ABBV ). Biosimilars come at lower price points than the original drug, and are therefore cheaper for PBMs such as Evernorth to source.

Also encouraging, CI’s medical memberships grew by a robust 10% YoY and the medical cost ratio also improved, which means that medical payouts as a percentage of premiums collected declined.

Looking ahead, CI has a number of avenues for growth, as its Medicare Advantage business is achieving above market growth. CI could see meaningful upside in this business segment even with market rate growth, considering the fast growing age 65+ cohort, which is the highest growing age group in America.

Moreover, the increasing number of specialty drugs such as weight-loss drug Ozempic from Eli Lilly ( LLY ) and potential for Alzheimer’s disease market to reach $14 billion globally bodes well for Evernorth going forward, as specialty drugs account for 40% of this unit’s revenue. Management also noted that Evernorth Care represents one of its most significant long-term growth opportunities given the increasing demand for virtual and behavioral health services.

Meanwhile, management has fairly clear strategy for capital allocation over the medium term. This includes maintaining a debt to capital ratio of 40%, which should support its strong A- credit rating.

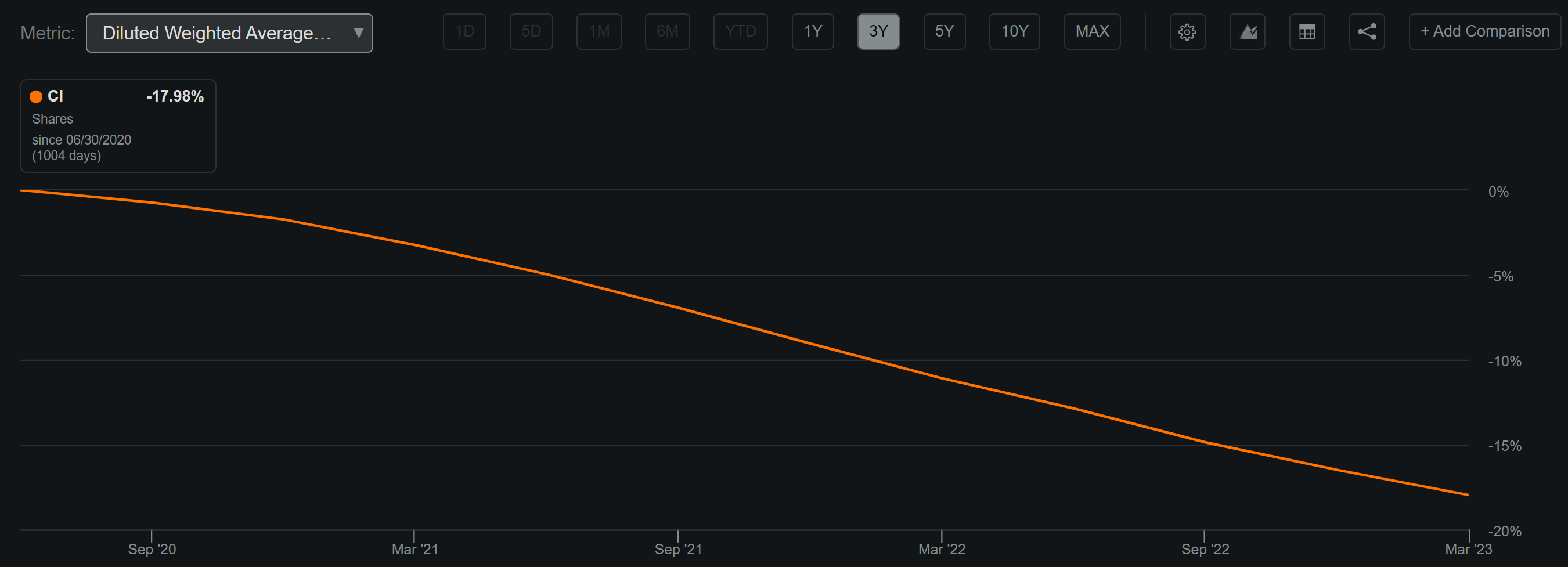

Management also expects to spend 20% of its operating cash flow to fund growth, and the remaining 80% is to be used on the dividend, debt repayments, and share repurchases and strategic M&A. As shown below, CI has repurchased a staggering 18% of its outstanding float over the past 3 years alone, since its Express Scripts acquisition.

{kind=link}

While CI yields just 1.9% at present, the dividend is very well covered by a 20% payout ratio. Management has also demonstrated its willingness to meaningfully increase the dividend in recent years, and this is reflected by the 10% dividend bump earlier this year.

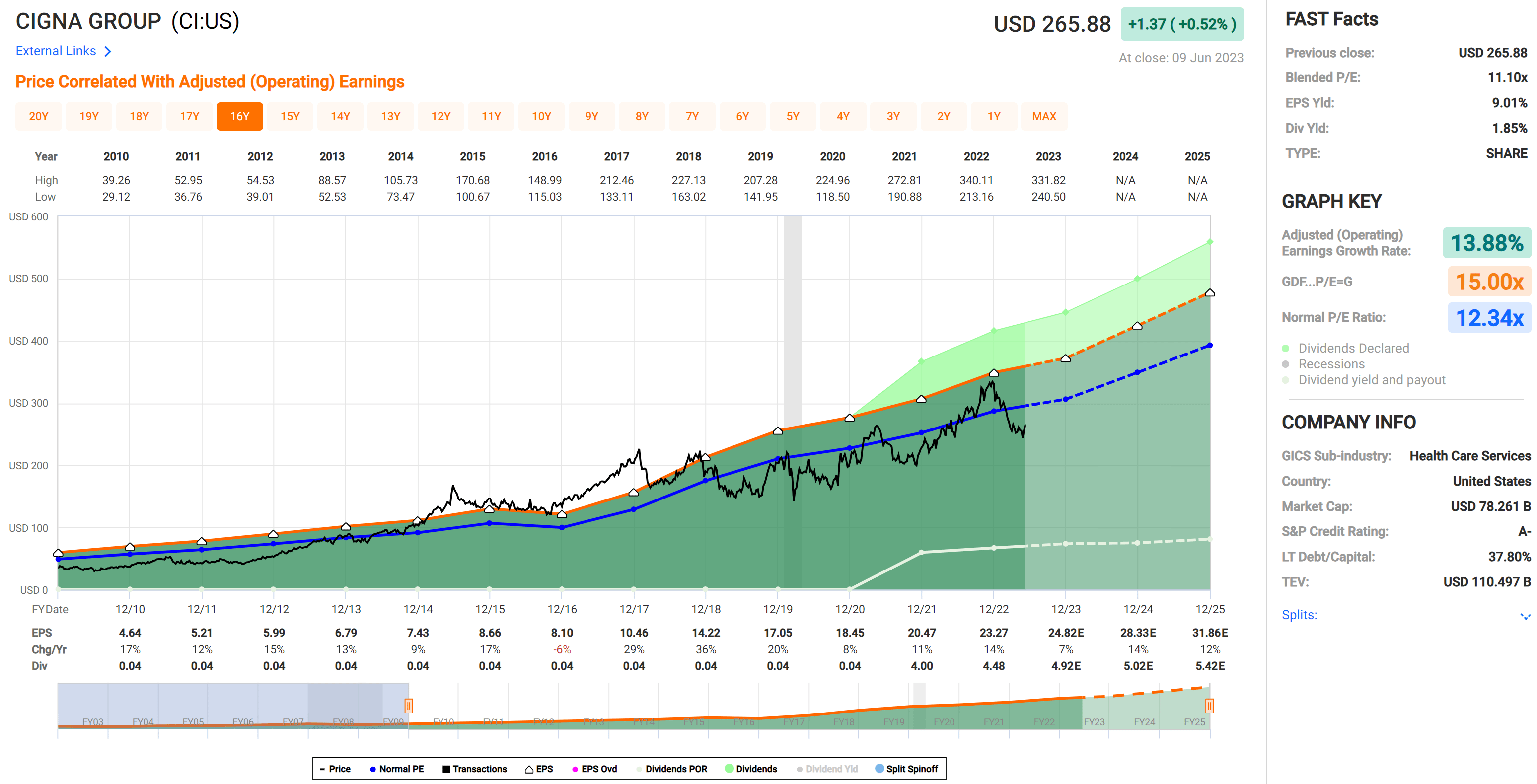

Lastly, I view CI as being a good value stock at the current price of $265.88 with a forward PE of just 10.7. This means that management is producing a 9.3% earnings yield for each dollar spent on share buybacks. CI’s current valuation also sits comfortably below its normal PE of 12.3, as shown below.

{kind=link}

This valuation appears to be far too cheap for a company that could reasonably grow its annual earnings in the ~10% in the medium term for the aforementioned reasons. This is below the 9% to 14% range that analysts expect in the 2024 to 2026 timeframe. Considering CI’s relative undervaluation to historical norms and its forward growth outlook, the stock could handily deliver potential double-digit annual total returns over the next couple of years, and analysts have an average price target of $329 .

Investor Takeaway

Cigna appears to be a great long-term total return pick in today’s market, especially for its relative undervaluation compared to historical norms. Not only does Cigna generate solid revenue growth potential from both its PBM and insurance segments, but it also has strong capital allocation policies that includes both business reinvestment, dividends, and share buybacks, which are highly accretive at the current discounted level. As such, investors looking for both value and growth ought to give CI a hard look at the present price.

For further details see:

Cigna: Buy This Value Gem Before It Bounces Back