CI - Cigna Corporation: Undervalued For Stable Growth

Summary

- Cigna's cost of care trends and goals to further reduce that cost to around the CPI, Cigna stands to gain consumers in the commercial segment.

- Cigna's earnings growth prospects look very promising.

- The general consensus is that Cigna is trading below value.

Investment Thesis

Despite Cigna Corporation's (CI) strong financial base, shares have dropped in the past few months from a high of $340 to the current price of $296.51. I find this drop to be unwarranted given Cigna's incredible profitability and organic growth prospects, and find this to be an excellent entry price for the interested investor. I recommend a BUY in Cigna for the following reasons.

Cross Selling

As a quick aside, Cigna has quite a few pathways to organic growth. First, their 2018 acquisition of Express Scripts opens up Cigna to cross-selling opportunities. The addition of new service offerings should allow Cigna to cross-sell PBM services into its client sets and increase its net dollar expansion rate and earnings. Cigna has also highlighted its eviCore medical benefit management and its Accredo specialty pharmacy (an oncology/rare disease therapy specialization) as additional services on top of its medical insurance and PBM offerings. More information on these divisions and cost control can be found here.

Latest Earnings

I'd like to point out a few notable things about Cigna's latest earnings call.

Cigna ended Q4 2022 with an EPS beat despite a revenue miss, continuing a trend of EPS beats ranging all the way back to Q1 2021. This implies healthy margins, which should only expand given the cross-selling opportunities afforded to Cigna by its diverse service offerings.

Furthermore, Evernorth (a Cigna subsidiary) continued to meet growth expectations , supplemented by Cigna Healthcare's impressive 13% earnings growth and impressive shareholder returns.

Cigna also projects long-term average EPS growth of 10-13%, which, coupled with its 1.63% dividend which Seeking Alpha rates to be very safe and likely to grow, makes Cigna an attractive long-term option.

Buybacks are also a common trend at Cigna. Cigna has bought back at least a hundred million dollars' worth of shares every year since 2011 -- and they aren't stopping now, buying back over $7 billion in 2022. Dilution is unlikely with Cigna.

Guidance for 2023 is very promising, and it is my belief that Cigna will be able to continue to grow at a healthy pace into the future for the reasons below.

Qualitative Factors

Cigna does have a few things that set it apart from its competition.

First, Cigna has a strong brand and an established reputation in the industry. The company has a long history and has jumped all the way up to the 27th largest company in the industry. This limits the risk of new competition since economies of scale and other size advantages give the industry high barriers to entry (though this is true in many industries, so take it with a grain of salt).

Cigna's 10k

Furthermore, Cigna has expanded into alternative care delivery via its acquisition of MDLIVE , a leading provider of telehealth. It also plans to use Evernorth's pharmaceutical strength to take advantage of the growing market for biosimilars (see above, this market is also projected to be in hyper-growth ), in order to keep cost-of-care under control, which should help it grow its commercial consumer base in the face of widespread cost increases.

Lastly, Cigna also has branched into more mental-health-oriented services, such as their partnership with Ginger (an app for on-demand mental health), and expanding their behavioral offerings within Evernorth. Given the salience of mental health and mental health issues in today's society, I see these moves as quite prescient.

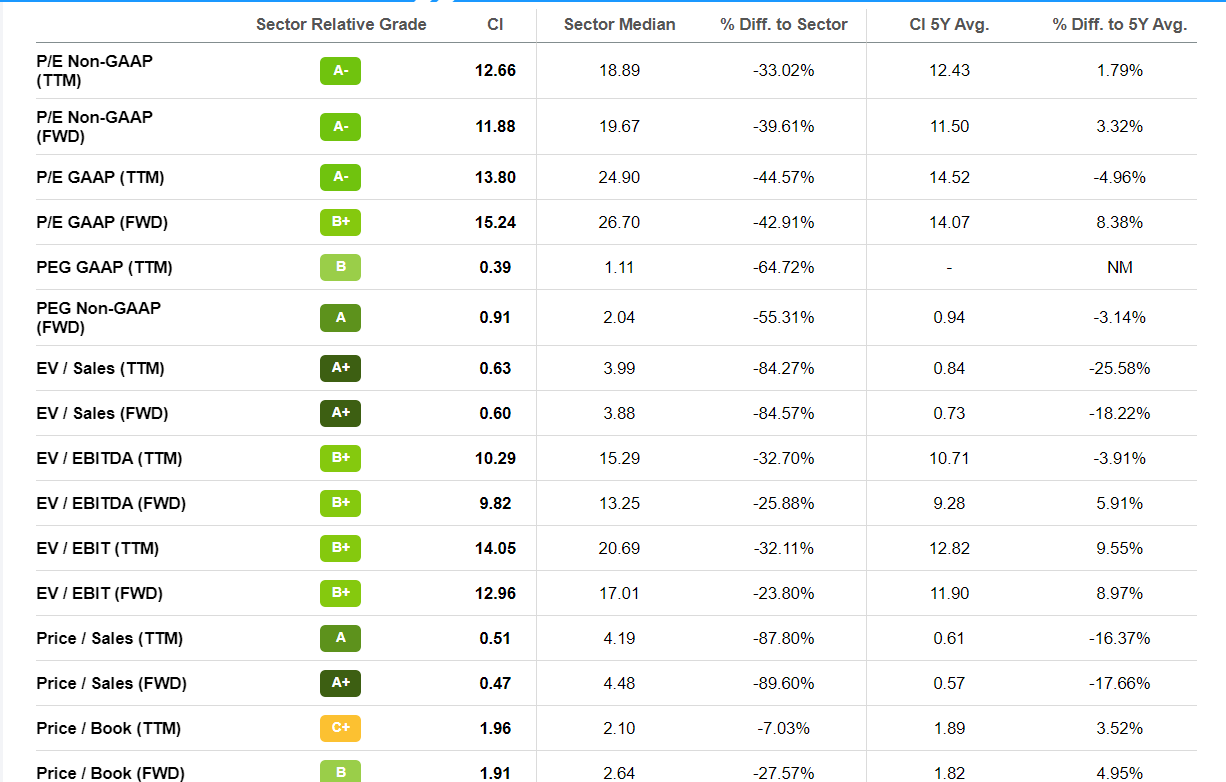

Sector Relative Valuation & DCF

The health insurance industry is a well-populated one, and Cigna faces no shortage of competitors because of that. However, Cigna's valuation makes up for this high level of competition -- all non-GAAP measures point to a very enticing P/E of ~12-13, EV/EBITDA margins which are 25% lower than the sector average, and a forward P/S of .49.

{kind=link}

As you can see, it's a lot of green.

Furthermore, Cigna's P/E is only 60% of its peer average despite a strong 2023 outlook, with its P/B and P/E being less than 50% of the average. According to Simply Wall St, a fair P/E for Cigna would be closer to 30x, given its earnings and growth outlook, risk, and margins. While I wouldn't go nearly that far, I would say Cigna should be trading at the least close to 16-19x.

Furthermore, Simply Wall St's DCF valuation of Cigna places Cigna as trading nearly 48% under value, which, even with an incredibly high margin of safety, still implies that Cigna currently sits at a very good price.

FactSet analyst composites also place a fair price for Cigna at close to $355, with even the lowest estimates sitting near the $310 mark. Given a current price of just under $295, this seems to be a no-brainer given Cigna's recent and projected EPS growth, as well as avenues for expansion and healthy dividend.

Balance Sheet and Misc Financials

Cigna's current financial position is very favorable, with a .86 D/E ratio, a .26 D/A ratio, and a healthy $5.5 billion in cash and nearly $8 billion in FCF to firm. This implies not only financial health in a broad sense, but the sustainability of Cigna's dividends and buybacks (as well as the potential for reinvestment, if needed). Cigna's ROE growth is also nearly 32%, which is quite impressive if even a fraction of that rate is sustainable, and its growth is only hindered by somewhat lackluster revenue growth rates. However, I anticipate Cigna's cross-selling opportunities and avenues into alternative markets like Telehealth, and, in the future, biosimilars, will somewhat remedy that issue.

Risk Factors

While I believe that Cigna is a decent long-term investment opportunity, there are some risks to be aware of. The health insurance industry has been historically highly regulated and therefore is subject to political uncertainty. Any significant changes in government policies or regulations could have an impact on Cigna's profitability. Additionally, competition in the industry is fierce, and if Cigna fails to meet its projected earnings growth, it stands to lose market share. Lastly, healthcare costs continue to rise, and Cigna stands to lose some of its commercial business if it cannot keep the cost of care low.

Bottom Line

Cigna is a strong investment opportunity given its EPS growth, organic growth avenues, and low valuation. Its cross-selling potential, expanded offerings, and commitment to shareholder value are key indicators of a healthy long-term outlook. Nearly all analysts and valuation measures point to a fair price 10-20% higher than its current value. Despite some measure of risk due to the nature of the healthcare sector and somewhat unimpressive revenue/EBIT growth, I find Cigna's current price and aforementioned tailwinds to warrant a BUY.

For further details see:

Cigna Corporation: Undervalued For Stable Growth