CI - Cigna: Many Reasons To Invest

2023-05-29 12:07:01 ET

Summary

- Cigna is growing rapidly and earnings per share have increased 13% annually over the past 4 years.

- The long-term outlook is also positive: Cigna is targeting annual EPS growth between 10% and 13%.

- About 20% of cash flow from operations is spent on dividends and about 70% on share repurchases and strategic mergers and acquisitions, further increasing shareholder value.

- About 68% of free cash flow is used to distribute dividends and repurchase shares. Its shareholder return policy is sustainable over the long term.

- Since Cigna expects to grow between 10% and 13% annually, investors can expect annual returns in the mid-teens.

Introduction

One of the insurance companies in my stock portfolio is Cigna ( CI ). Companies with growing (and predictable) sales and profits like Cigna fit well into my portfolio. The premiums paid to insurers are used to purchase bonds, which could increase the float. A good example whose float have become quite large is Warren Buffett's Berkshire Hathaway ( BRK.A )( BRK.B ).

Cigna is a prominent U.S. health insurer that has been in business for many years. In addition to insurance, Cigna offers health services such as pharmacy benefits, pharmacy home delivery and employee assistance programs, data analysis and the like to health plans, employers, government organizations and health care providers.

There are many reasons why an investment in Cigna is attractive. Cigna's growing customer base, for example, as well as rising interest rates and the stock's attractive valuation make it worth buying.

Cigna is also in excellent financial shape. Health insurers talk about medical costs ratio to express the profitability of the insurance business. This ratio calculates the sum of all medical costs and divides it by its premiums. Cigna's medical costs ratio is less than 1, so that means their insurance business is profitable on its own and they have costs well under control. Cigna is a strong buy in my opinion, as there are many reasons to like the company.

Expected Growth Of 10%-13% In Compound EPS

{kind=link}

Pathways To Growth (Cigna 1Q23 Investor Presentation)

One reason to invest in Cigna is its strong earnings growth in recent years. Cigna's diluted earnings per share increased 13.1% annually for the past 4 years, and growth has not stopped here. Many analysts expect the growth trajectory to continue for 2023 and beyond. Cigna expects a strong 2023 with diluted earnings per share of at least $24.70, representing a 6.2% annual increase.

Cigna delivered strong earnings in the first quarter of 2023 with revenue of $46.46 billion and diluted earnings per share of $5.41, which was about 3% higher than analysts had estimated.

The Cigna Group consists of Evernorth Health Services and Cigna Healthcare. Evernorth provides health services to health plans, employers, government organizations and healthcare providers. Specialty Pharmacy, Evernorth Care and Evernorth's Health Benefits Program (Insignia) are growing strongly in revenue and customer growth. Increased affordability has helped customer growth. Specialty Pharmacy accounts for about 40% of Evernorth's total revenue. Cigna has its costs well under control. The medical care ratio represents medical costs as a percentage of premiums. Cigna's medical care ratio was 81.3%, which is great. For the full year 2023, Cigna expects its medical care ratio to be within 81.5% and 82.3%.

For 2023, accelerated growth is expected in its Medicare Advantage business thanks to high-quality affordable health care plans and geographic expansion. Cigna also sees strong growth in its individual and family plans. Cigna therefore believes it will achieve about 10% to 13% compound EPS growth over the long term in the coming years.

{kind=link}

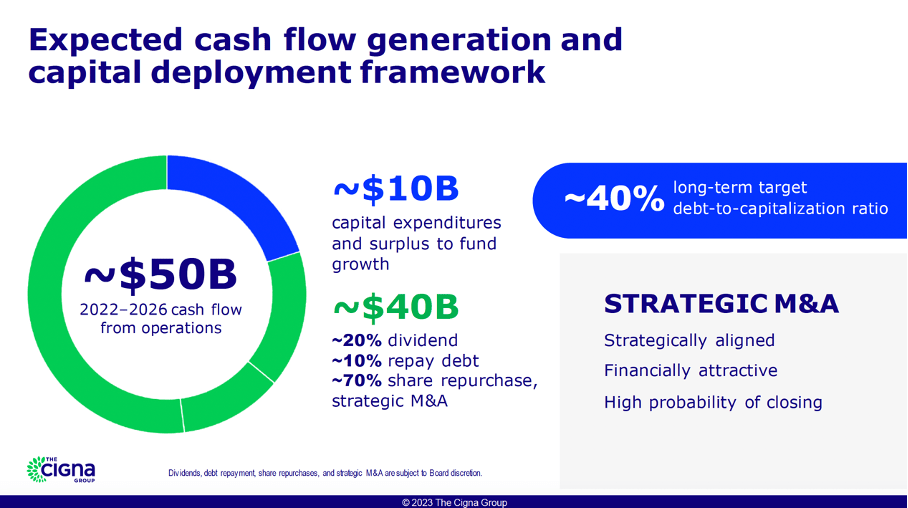

Expected cash flow generation and capital deployment framework (Cigna's 1Q23 Investor Presentation)

Another reason to invest in Cigna is its shareholder-friendly policies. About 20% of cash from operations is spent on dividends and about 70% on share repurchases or strategic mergers and acquisitions, which can further increase long-term shareholder value.

The stable profit stream is beneficial to shareholders because it enables a steadily growing dividend. The dividend is expected to increase 5.4% this year and 5.9% in 2024. Currently, the dividend yield is 2%, which is less than the 3.8% yield on 10-year government bonds. However, dividends are expected to rise annually, while Treasury bond income will remain flat in the coming years. Therefore, income investors should consider Cigna as a good long-term investment.

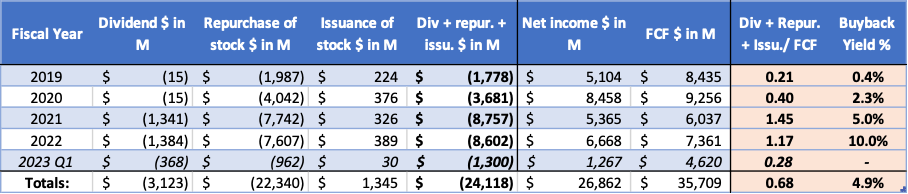

On average, Cigna distributes about 68% of its free cash flow to shareholders by distributing dividends and repurchasing shares. The remaining cash is used to repay debt to achieve a debt-to-capitalization ratio of 40%. Its shareholder return policy is therefore sustainable over the long term. Due to the low share price, the buyback yield is quite high. Investors clearly do not have much confidence in the future of the company. If Cigna decides to repurchase shares on the open market, the high buyback yield may be advantageous because it can drive up the share price.

{kind=link}

Cigna's cash flow highlights (Annual reports and analyst' own calculations)

The Third Reason: Cheap Valuation

The third reason to invest in Cigna is the inexpensive valuation of the stock. The PE ratio is a commonly used valuation metric to understand current and future valuations. I used YCharts to chart the historical PE ratio from 2000 to the present. With a PE ratio of 11.1, we see that the stock is favorably valued compared to its historical valuations. The current market value represents a discount of about 14% to the 3-year median.

Some 23 analysts have revised their earnings estimates upward, expecting earnings per share of $28.35 for 2024 (up 14.2%). The projected PE ratio for 2024 is only 8.6, which represents a sharp undervaluation compared to historical figures. Growth is expected to continue, as Cigna targets EPS growth of 10% to 13% per year. Investors who buy the stock at this price level can expect share price gains in the coming years thanks to the undervaluation and EPS growth. Including dividends, I expect Cigna to offer investors a mid-teens annual return in the coming years.

Risks

Insurance companies like Cigna invest their premiums to grow their float. Float increases through investment income, but the fair value of the investment portfolio has decreased due to sharply increased interest rates. Several banks, such as SVB Financial, had to sell part of their investment portfolio at a reduced value. They had to sell some assets due to the large outflow of deposits. Cigna, like other insurance companies, does not face this risk.

Rising interest rates mean more income for Cigna. Still, net investment income for the first quarter of 2023 was significantly lower than a year ago ($277 million versus $414 million last year). This was due to lower gains on their partnership investments and the unfavorable impact of the Chubb transaction. This year will see further increases in interest rates, followed by a decline in 2024.

Another risk can be found in their private equity and real estate funds. These are categorized under "Other long-term investments" which have a value of $3.9 billion (total long-term investments are $19 billion). In total, they include investments in securities limited partnerships and real estate limited partnerships, direct investments in real estate joint ventures and other custodial activities needed to support various insurance and health services businesses.

Cigna expects continued volatility in the performance of private equity and real estate funds as fair market valuations are adjusted to reflect market and portfolio transactions. However, this risk is not particularly significant, less than 5% ($195 million) of its other long-term investments are exposed to office real estate.

Conclusion

I like investing in insurance companies like Cigna because its revenues and profits are predictable and grow steadily over time. Cigna is an American health insurer that also offers health services through its Evernorth acquisition. There are many reasons why I like investing in Cigna. Cigna is growing rapidly and earnings per share have increased 13% annually over the past 4 years. In 2023, Cigna expects earnings per share to rise 6.2% YoY. The long-term outlook is also positive: Cigna is targeting annual EPS growth between 10% and 13%.

About 20% of cash flow from operations is spent on dividends and about 70% on share repurchases and strategic mergers and acquisitions, further increasing shareholder value. The dividend yield is currently 2% and is expected to rise 5.4% this year. About 68% of free cash flow is used to distribute dividends and repurchase shares. Its shareholder return policy is sustainable over the long term. I like it when Cigna repurchases shares because it increases dividends per share and earnings per share. Also, its share valuation is favorable because it suggests an undervaluation of 14%. Since Cigna expects to grow between 10% and 13% annually, investors can expect annual returns in the mid-teens. We see many reasons to invest in Cigna.

For further details see:

Cigna: Many Reasons To Invest