HUM - Cigna: What To Make Of The $10 Billion Buyback Bomb

2023-12-11 16:45:47 ET

Summary

- The Cigna Group and Humana Inc. were in talks for a potential merger, but the deal fell through due to disagreements on financial terms.

- Yesterday, Cigna announced an update to its already generous shareholder return program - an incremental $10 billion buyback authorization.

- In this update, I will take a fresh look at Cigna's cash-generating ability and balance sheet, and assess whether the massive buyback program could jeopardize the company's credit quality.

- Given that Cigna is likely to refinance most or all of its near-term maturities, I will present scenario calculations that model the impact of "higher and longer" interest rates.

- I will put the buyback program in proper perspective and quantify its impact on earnings per share growth and the dividend payout ratio.

Introduction

On November 29, 2023, management of The Cigna Group ( CI ) shocked investors by announcing that it was in talks with Humana Inc. ( HUM ) about a possible merger. According to a Wall Street Journal report , the cash-and-stock deal could be finalized by the end of the year, or in just about a month. But of course, this didn't mean that regulators would approve the deal, considering the likely resulting dominance of the combined Humana and Cigna entity, and the fact that the Anthem-Cigna merger was blocked in 2017 due to antitrust concerns.

Even as a relatively new shareholder of Cigna ( read here why I changed my mind after initial hesitation ), I questioned the merger coming to fruition from the first moment and was therefore not very surprised when it was announced on Sunday, December 10, that the two healthcare giants had abandoned talks because they apparently could not agree on the financial terms of the deal.

Initially I felt that I had nothing meaningful to contribute to the discussion and refrained from writing an update amid the merger speculation. However, now that the merger is off the table and Cigna's management has announced a significantly increased share buyback program, I think it's time to take a fresh look and evaluate the impact of that program - both on shareholder returns and the balance sheet. Keep in mind that Cigna is not exactly a low leverage company given its acquisition of Express Scripts in 2018.

An Updated Look At Cigna's Balance Sheet And The Impact Of The Buyback Program

Before answering the question about the impact of the significantly expanded buyback authorization on shareholder returns, I believe it is essential to take a fresh look at the company's balance sheet. This is important not only due to the fact that Cigna acquired Express Scripts in 2018 for a transaction value of $52.8 billion, but also due to the comparatively high interest rate environment that penalizes highly leveraged companies with significant near-term maturities.

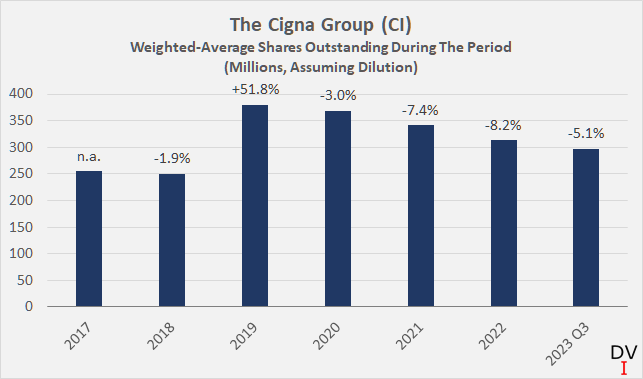

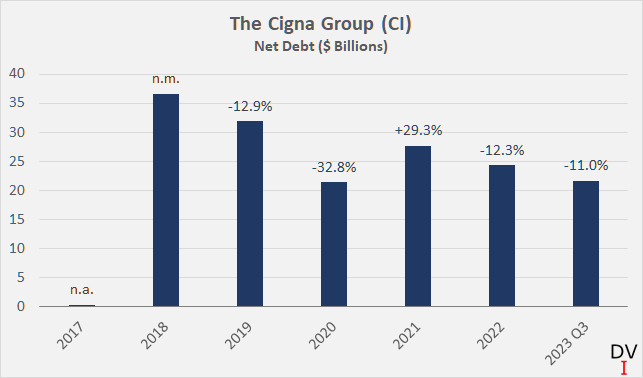

Cigna's acquisition of Express Scripts was structured as a cash/stock deal, increasing Cigna's share count by approximately 50% to 380 million (Figure 1), while the company's net debt increased to over $36 billion (Figure 2).

{kind=link}

Figure 1: The Cigna Group (CI): Weighted-average shares outstanding during the year or quarter (own work, based on company filings)

{kind=link}

Figure 2: The Cigna Group (CI): Net debt at the end of the year or quarter (own work, based on company filings)

Obviously, management has prioritized share buybacks to reduce the impact of dilution. More importantly, however, a significant portion of the free cash flow generated over the years was used to reduce debt.

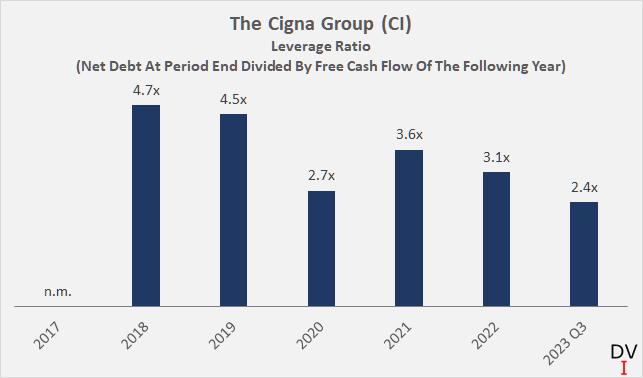

In my view, the high profitability of the merged company and the conservative but shareholder-friendly stance of the management are best underlined by the sharp decline in the leverage ratio, measured by net debt to free cash flow (Figure 3). Since the Express Scripts acquisition, Cigna's leverage ratio has declined faster than net debt in absolute terms, confirming strong free cash flow growth, excellent business integration and the successful realization of merger synergies. In 2023, free cash flow after adjusting for stock-based compensation is expected to be close to $9 billion, which corresponds to a leverage ratio of less than 2.5 - hardly a worrying figure.

{kind=link}

Figure 3: The Cigna Group (CI): Leverage ratio in terms of net debt to free cash flow (own work, based on company filings)

Cigna's solid progress has also been recognized by rating agencies such as Moody's, which upgraded the company's senior unsecured credit rating by one notch to Baa1 in April 2021. According to the agency, the rating:

... reflects [Cigna's] strong market position, relatively low underwriting risk, the strong capital position of its health insurance operating subsidiaries and the leading EBITDA margin among Moody's rated health insurers. It also reflects the company's significantly enhanced diversification and the large increase in unregulated revenues attained through the acquisition of Express Scripts ((ESI)) in December 2018.

Moody's Investors Service, April 14, 2021

Management announced yesterday that it would buy back another $10 billion worth of shares, bringing the current total authorization to $11.3 billion. I expect the company to pay out about $1.45 billion in dividends in 2023, leaving excess free cash flow of about $7.5 billion. There will therefore be no cash flow left for debt repayment and, depending on the timing of the buybacks, it is even possible that Cigna will (temporarily) take on additional debt.

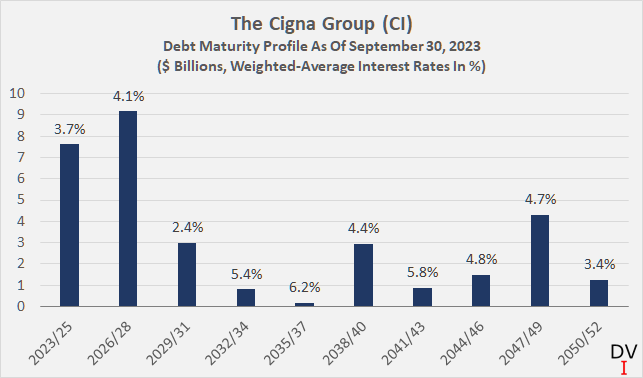

Therefore, despite the positive operational developments and strong fundamentals discussed in my previous articles, it is important to take a look at the maturity profile of Cigna's debt (Figure 4). Short-term maturities are quite pronounced with more than 50% of gross debt maturing between 2023 and 2028. Should interest rates remain elevated for several years, Cigna would have to refinance at comparatively unfavorable interest rates, which would weaken its interest coverage ratio.

{kind=link}

Figure 4: The Cigna Group (CI): Debt maturity profile at the end of Q3 2023, including commercial paper (own work, based on company filings)

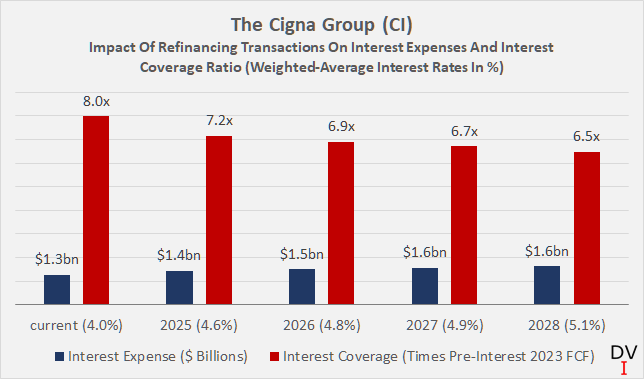

In Figure 5, I have illustrated the impact of refinancing transactions assuming that Cigna refinances all debt due by the respective year at an interest rate of 6.0%. However, even if interest rates remain elevated until 2028, I think it is reasonable to conclude that the negative impact of refinancing transactions on Cigna's interest coverage ratio will remain very manageable. Also keep in mind that I have not included interest income in the calculation in order to remain conservative. Assuming Cigna receives 3.5% p.a. on its current cash balance of $8.5 billion, its interest coverage ratio would improve from 8x to 10x its expected 2023 free cash flow before interest.

So clearly, Cigna not only has the cash flow to maintain such generous returns for shareholders, but also the financial flexibility to pause deleveraging for a few years - even if interest rates actually stay "higher for longer".

{kind=link}

Figure 5: The Cigna Group (CI): Scenario calculations illustrating the impact of debt refinancing under the assumption that interest rates remain elevated for several years (own work, based on company filings and own calculations)

Conclusion – What The Bold Share Buyback Announcement Means For Cigna Shareholders

I think it's fair to say that Cigna's management has done a great job with the bold acquisition of Express Scripts and the subsequent deleveraging and share buybacks. The current leverage is already very manageable and the company is highly cash generative, so it is not surprising that management has significantly expanded its share buyback program - by $10 billion to the current $11.3 billion.

In this context, it is worth emphasizing that Cigna's management usually under-promises to over-deliver, as I have noted in my previous articles. For example, in its latest earnings report , management again raised cash flow guidance, which now stands at over $10.5 billion for cash flow from operations - $1.5 billion more than three months earlier .

Clearly, there is no doubt that Cigna not only has the cash flow to maintain such generous returns for shareholders, but also the financial flexibility to suspend deleveraging for a few years - even if interest rates do indeed remain "higher for longer". For example, if interest rates remain at the current level until 2028, the company's interest coverage ratio would fall to only 6.5 times its current pre-interest free cash flow - and this is without taking into account significant interest income and assumes zero growth in free cash flow.

In the third quarter of 2023, Cigna had 297 million shares outstanding.

According to yesterday's press release, management expects to complete half of the additional $10 billion repurchase authorization by the end of the first half of 2024. If we assume that Cigna's share price remains at $300 during this period, this would mean that diluted shares outstanding would fall to approximately 280 million. Of course, this does not take into account the dilution from stock-based compensation, but considering that its impact is fairly modest (on average 3.5% of operating cash flow between 2018 and 2022). Assuming that the remainder of the current authorization is also executed at a share price of $300, the number of Cigna shares would fall to less than 260 million.

In other words, Cigna expects to buy back around 13% of its current market capitalization in the near future. This means that earnings per share growth will increase by 9.8 percentage points (annualized rate between 2023 and 2024), assuming Cigna completes the entire program by the end of 2024. The share buybacks will also lower Cigna's dividend payout ratio, which is already very comfortable at 16% of expected 2023 free cash flow. The buyback of 38 million shares would lower the payout ratio by two percentage points, which in turn would further increase the headroom for dividend increases. As I mentioned previously, I think CI is a dividend growth stock in the making.

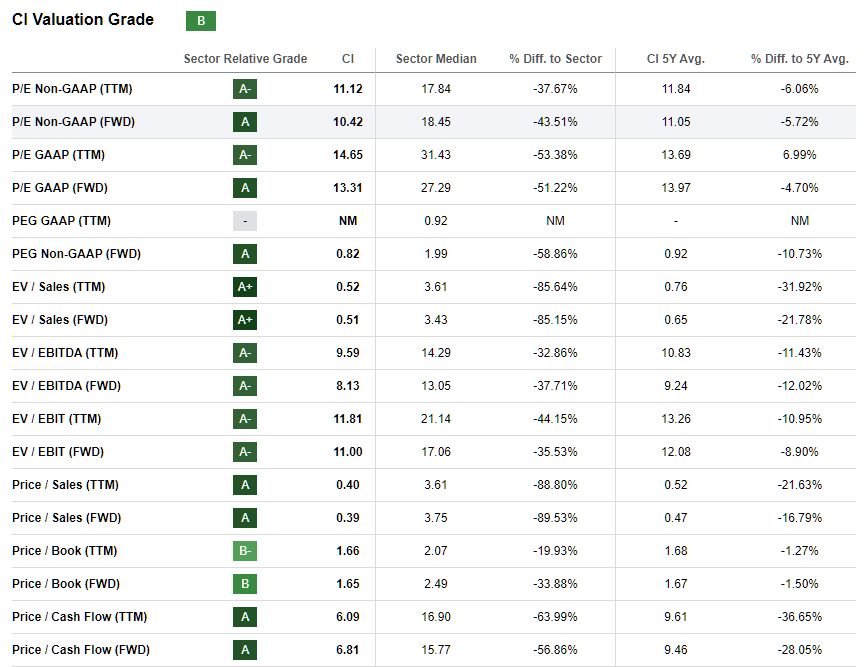

For these reasons, and given the buybacks represent a compelling return on investment (Figure 11 and Table 1), it is no wonder that Cigna stock has come back into focus with investors, but this time in a positive light.

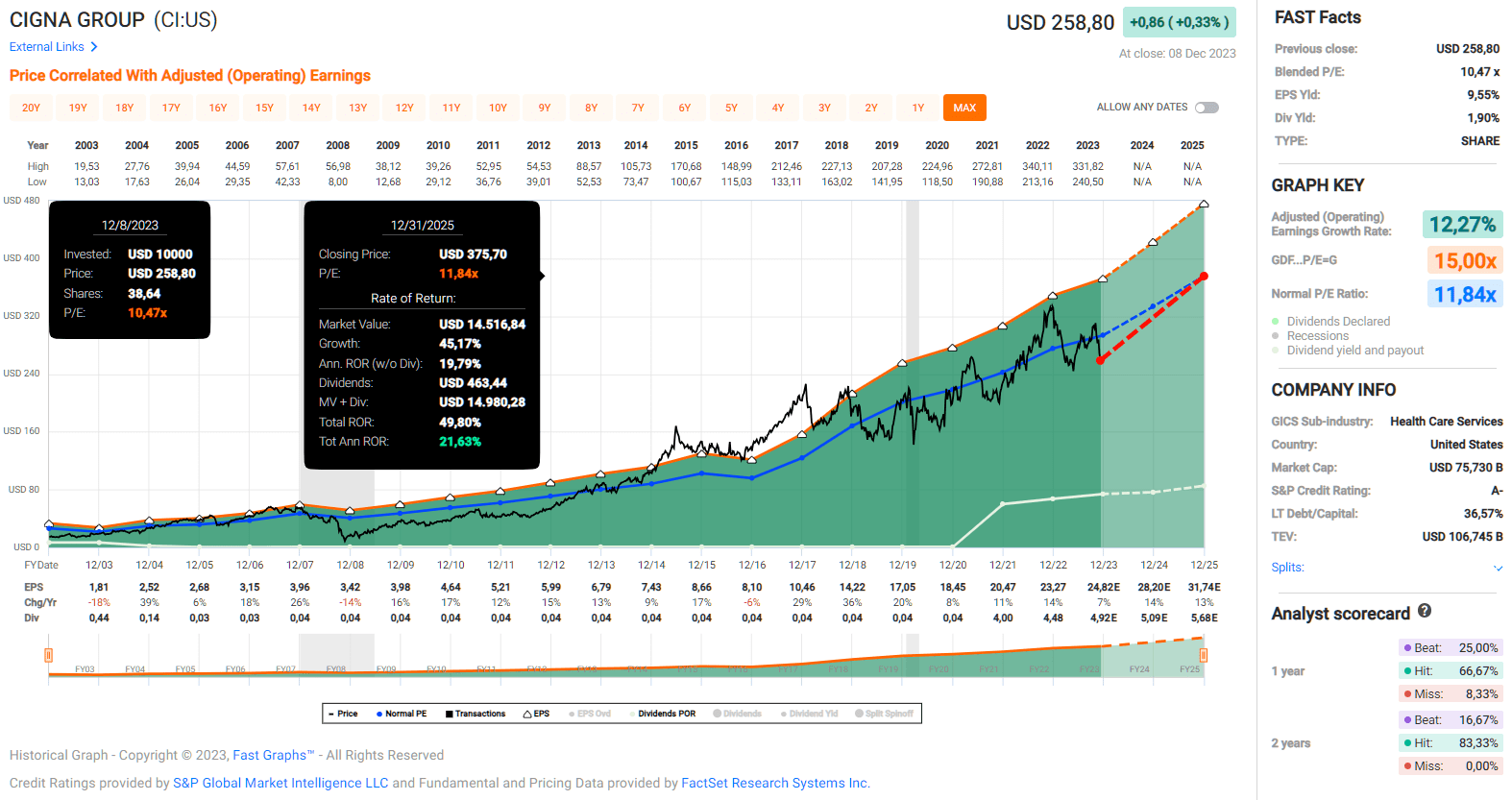

On a side note, given the sharp jump in Cigna's share price today (+16% at the time of writing), the blended price/earnings ratio is of course no longer 10.5, but even at an earnings multiple of just over 12, I think it would be an exaggeration to call the stock expensive.

{kind=link}

Figure 6: The Cigna Group (CI): FAST Graphs chart, based on adjusted (operating) earnings per share; actual return expectations are lower due to today’s jump in share price (FAST Graphs)

{kind=link}

Table 1: The Cigna Group (CI): Valuation grade and underlying metrics (Seeking Alpha)

That said, and as I have already explained in my previous articles, I do not believe that an earnings multiple in the high tens is justified for a stock like Cigna - despite its current strong growth. I consider it to be fairly valued at a P/E ratio of 12 to 13, mainly due to the uncertain regulatory environment and the ever looming - but difficult to implement - healthcare reform.

Cigna currently makes up about 0.6% of my total portfolio value, and I bought most of my position right after the positive first quarter earnings announcement in May (as disclosed in the corresponding article ), but also recently amid the merger-related selloff.

At $300, I rate the stock as a "hold with a tendency to buy" and am not adding to my position at this time - mainly because I don't think it's a particularly good idea to buy or sell a stock immediately after a major news event. Nevertheless, I will monitor CI's stock price over the coming weeks and expect to add on any further weakness.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Cigna: What To Make Of The $10 Billion Buyback Bomb