ETV - CII And ETV: 2 CEFs Worth Buying When They're Down

2023-11-11 22:25:22 ET

Summary

- The Nasdaq and S&P 500 had recently entered correction territory and that volatility pushed some tech-oriented funds to some attractive discount levels where they remain.

- BlackRock Enhanced Capital and Income (CII) and Eaton Vance Tax-Managed Buy-Write Opportunities Fund (ETV) have put up solid results and provide monthly distributions to investors.

- CII and ETV both have an option writing strategy with tech-heavy portfolios.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Recently, the tech-heavy Nasdaq entered correction territory, and the S&P 500 Index wasn't too far behind, falling more than 10% from their highs. This can create an opportunity for investors to put some cash to work. While the market started a swift recovery from the correction low, the discounts for closed-end funds remain wide. That can create a potential opportunity for investors still looking to put some cash to work.

BlackRock Enhanced Capital and Income ( CII ) and Eaton Vance Tax-Managed Buy-Write Opportunities Fund ( ETV ) both have solid histories of performance helped out by their growth-tilted portfolios with heavy tech sector exposure. They also take a call-writing approach, with CII writing calls on only a portion of their portfolio and writing covered calls. ETV takes a different approach to help it achieve its "tax-managed" approach, and that is through writing calls against indexes.

ETV also targets an overwrite of 100%. A call writing or covered call strategy can give up some potential upside if the market rises rapidly. This could be one of the reasons that ETV has underperformed over the longer term against CII.

Ycharts

However, more recently, over the last year, the funds on a total NAV return basis have been linked closely, coming in virtually identical. On a total share price basis, that's been a completely different story.

Ycharts

Both funds are trading at attractive discounts today, with ETV pushing near a discount that hasn't been seen since around 2012. With the increased volatility, we are starting to CII now turn to a more appealing discount as well.

CII

- 1-Year Z-score: -0.54

- Discount: -3.58%

- Distribution Yield: 6.71%

- Expense Ratio: 0.89%

- Leverage: N/A

- Managed Assets: $784.227 million

- Structure: Perpetual

CII has a simple objective and strategy; it "seeks to provide investors with a combination of current income and capital appreciation" by "investing in a portfolio of equity securities of the U.S. and foreign issuers." They will also "employ a strategy of writing call and put options."

The fund takes no leverage in the form of borrowings, which is seen as a positive, in my opinion, in the current environment of higher interest rates. The covered call writing strategy is also a slightly defensive strategy as it brings in option premiums, which can be beneficial to offset some of the losses seen.

As of the end of September, the fund was overwritten by around 55.5%. That puts the fund on the higher end of the overwritten target of 30 to 40%. That would indicate that the fund is tilting more bearish these days.

With the market entering into a more volatile period recently, it has been taking CII with it. That includes being pushed to a deeper discount than we were just mere weeks ago when the fund was at a premium. The fund is finally getting nearer to its longer-term discount average, and that makes it appealing to consider today. This was after several years post-COVID that saw this fund continually push near-premium territory.

The fund has put up solid results, and that's thanks to its strong focus on growth investments with the tech sector at a weighting of 23% currently. The next highest allocation is to healthcare at under 16%. The fund's focus is the Russell 1000 Index as its benchmark, but they also look at the performance comparison between the MSCI USA Call Overwrite Index to provide a clearer picture of the fund's options writing strategy.

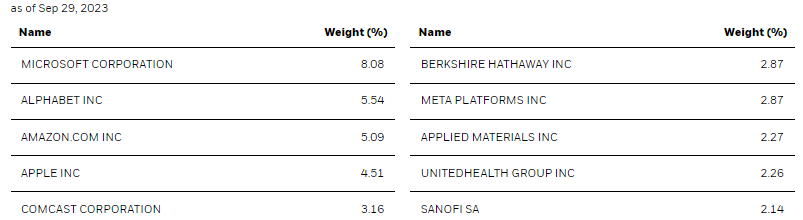

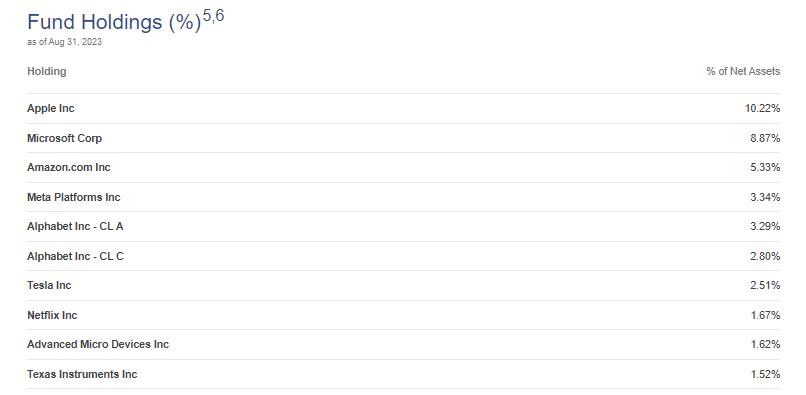

The fund's top ten holds several of the Magnificent Seven names that have driven a large part of the returns in the last decade, but even more particularly, through 2023. We'll see a number of overlapping positions between CII and ETV, which includes Microsoft ( MSFT ), Alphabet ( GOOG )( GOOGL ), Amazon ( AMZN ), Apple ( AAPL ) and Meta Platforms ( META ).

{kind=link}

Given the top ten holdings, it's quite clear that the fund invests primarily in large-cap names, with the average market cap of their holdings coming in at nearly $600 billion. The portfolio is dominated by U.S. exposure as well, with that coming in at ~90% of the fund.

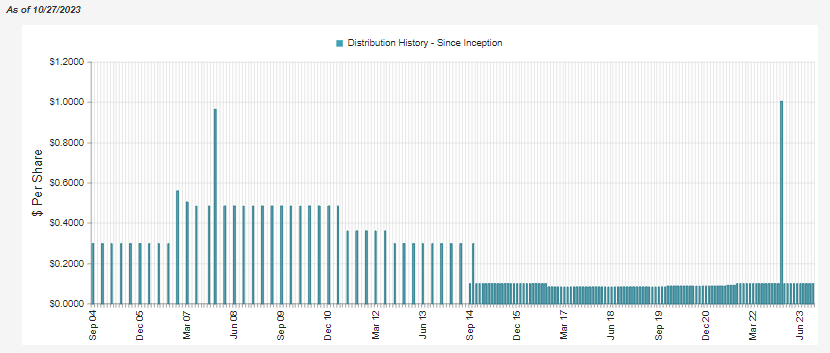

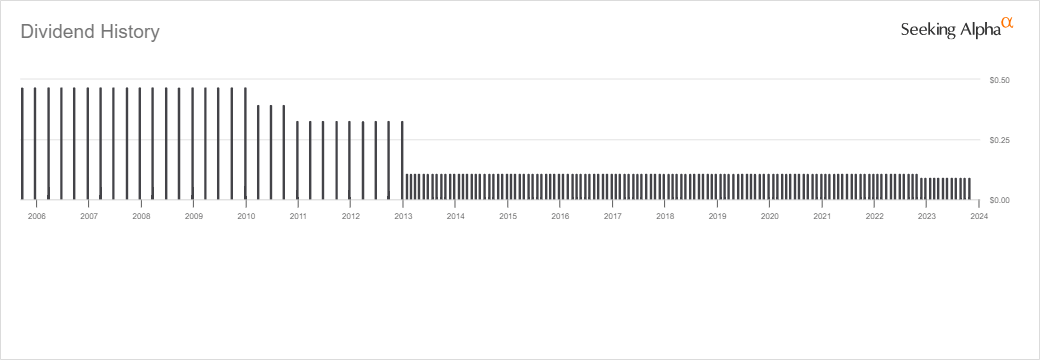

The fund switched from a quarterly distribution schedule to a monthly payout around 2014. After the Great Financial Crisis, the fund did cut its distribution several times, but after a solid bear market, it was able to raise it a couple of times since. At an NAV distribution rate of 6.68%, this latest correction doesn't seem like it would jeopardize the current payout.

{kind=link}

ETV

- 1-Year Z-score: -1.50

- Discount: -7.17%

- Distribution Yield: 9.37%

- Expense Ratio: 1.08%

- Leverage: N/A

- Managed Assets: $1.4 billion

- Structure: Perpetual

ETV's investment objective is to "provide current income and gains, with a secondary objective of capital appreciation." To achieve this, the fund will invest "in a diversified portfolio of common stocks and writes call options on one or more U.S. indices on a substantial portion of the value of its common stock portfolio to seek to generate current earnings from the option premium."

Similarly to CII, ETV doesn't borrow to try to gain an edge and instead writes calls against indexes. For ETV, they benchmark against the S&P 500 and Nasdaq 100 Indexes. However, they also incorporate the CBOE S&P 500 BuyWrite Index and the CBOE Nasdaq 100 BuyWrite Index.

Given the unconstrained nature of the Nasdaq 100 and the impressive bull market run that helped support tech, ETV has clearly fallen short of putting up competitive results against that index. On the other hand, against the BuyWrite Indexes, which are better representative of the fund's strategy, they've been able to blow those comparison results away.

Given these benchmarks, it's no surprise that the fund writes calls against the Nasdaq 100 and S&P 500 Indexes. In implementing the fund's strategy, it's important to have a portfolio that matches what they are writing against since, writing index options, there is theoretically a possibility for unlimited losses. In reality, we know that an index isn't going to rise forever.

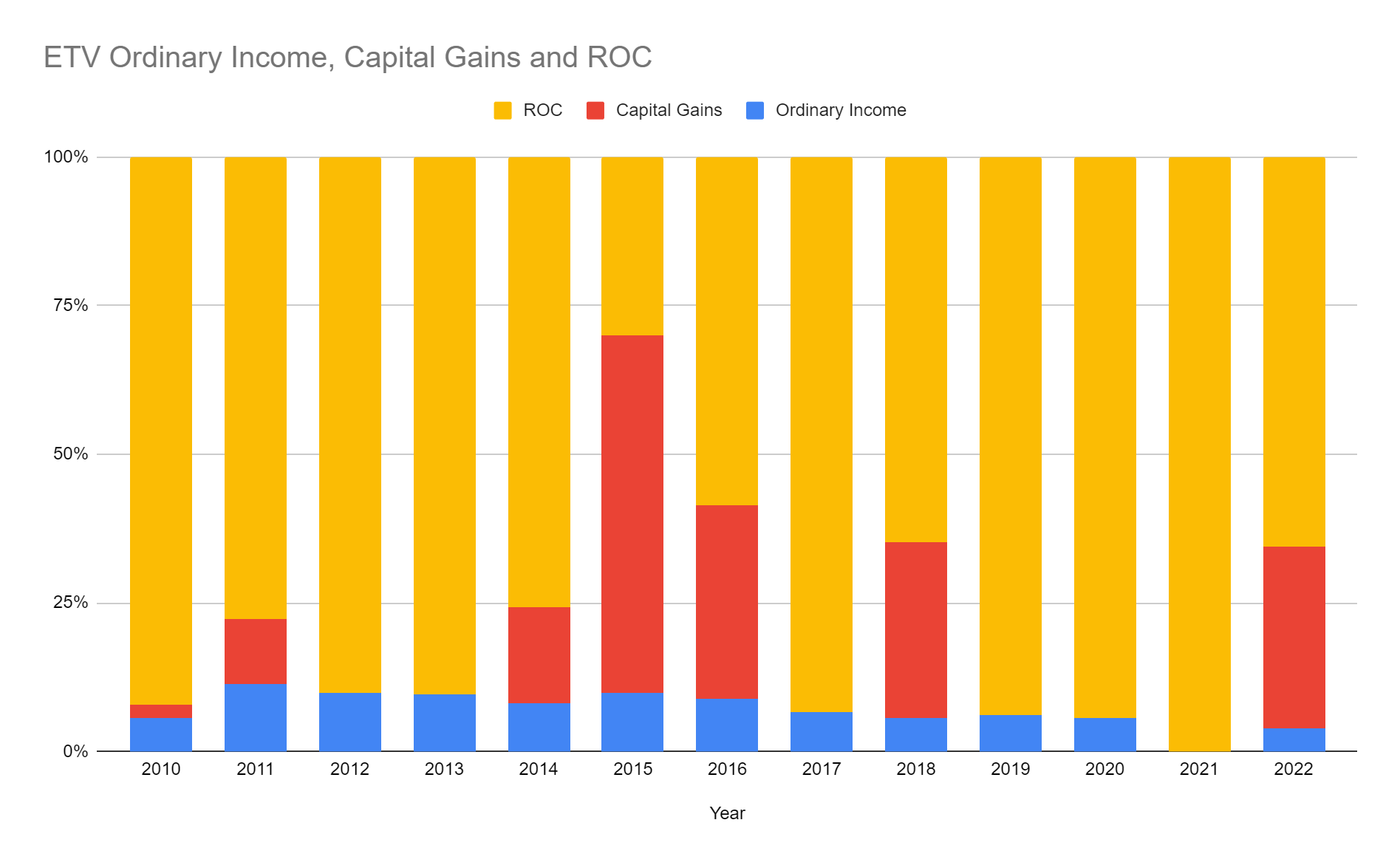

However, by having a portfolio that is primarily composed of that index anyway, as the index rises, producing losses, the underlying portfolio is hedging as those positions are also going to be rising in value. Producing losses is how they offset gains in their portfolio if they realize gains on their underlying portfolio, which they generally don't do too much of anyway. The end result is over the years, the fund has paid tons of return of capital distributions while also producing positive total return results for investors.

ETV Distribution Tax Classification History (Annual Report Filings (Author Compiled Graph))

{kind=link}

This fund had pretty consistently traded at a premium since going to one in 2014. Today, however, the fund has fallen to a deep discount well beyond the fund's historical average level.

The catalyst to cause this discount seemed to be the distribution cut near the end of last year. That just so happened to be when the fund was at a near-all-time high premium as well, which made the whole fall much more dramatic than it otherwise would have been. The fund's distribution had been otherwise incredibly steady since switching from quarterly to monthly around 2013. Similar to CII, the fund was cutting through the GFC.

{kind=link}

ETV currently has the higher distribution yield when compared to CII, and that's thanks in part to the larger discount. However, it also has a 9.34% distribution rate on NAV. When this starts to get too far over 10%, that's generally when EV has historically started timing - which is what happened last year when we went beyond correction territory and into bear market territory.

CII is missing Tesla ( TSLA ) from the Mag 7, but that is represented in ETV's portfolio. However, both funds aren't holding NVIDIA ( NVDA ) in their top ten, which would be the final name of the Mag 7 stocks.

Suffice it to say both portfolios are overloaded with tech. However, ETV takes that to an even higher level, with those names consisting of 36.36% of its portfolio. AAPL alone is over a 10% allocation. CII is a touch more balanced in that regard, with these mega-cap growth names consuming around 26% of the fund's portfolio.

{kind=link}

Conclusion

CII and ETV are more interesting funds these days as we enter into a more volatile period where the market recently entered into correction territory. ETV is sporting one of the deepest discounts in the fund's history, not seen since around 2012. CII isn't quite as much of a screaming deal, but it's still looking more tempting as the fund backs away from the premium level it was trading at just a short while ago.

For further details see:

CII And ETV: 2 CEFs Worth Buying When They're Down