CMPR - Cimpress: Bullish Amid Ongoing Turnaround And Climbing Profitability

2023-10-31 12:05:51 ET

Summary

- Cimpress plc reported its fiscal Q1 earnings with EPS beating expectations while management hiked the full-year EBITDA guidance.

- Efforts to control spending and generate cost savings have helped to improve margins while supporting a balance sheet deleveraging.

- We see upside for the stock into 2024.

Cimpress plc ( CMPR ) has emerged as an impressive turnaround story with shares more than tripling from the 2022 lows. The company recognized as a leader in customizable marketing products and business merchandise is attempting to navigate a shifting market environment since the pandemic.

The good news is that the latest quarterly report was highlighted by an ongoing earnings rebound and overall improving fundamentals. Management has set a positive outlook for the year ahead.

We like the stock with a sense that the brand portfolio with category leaders like "VistaPrint" and "PrintBrothers" maintains a solid long-term outlook. Despite ongoing macro headwinds, CMPR has more upside as the company continues to drive profitably while reducing debt.

CMPR Earnings Recap

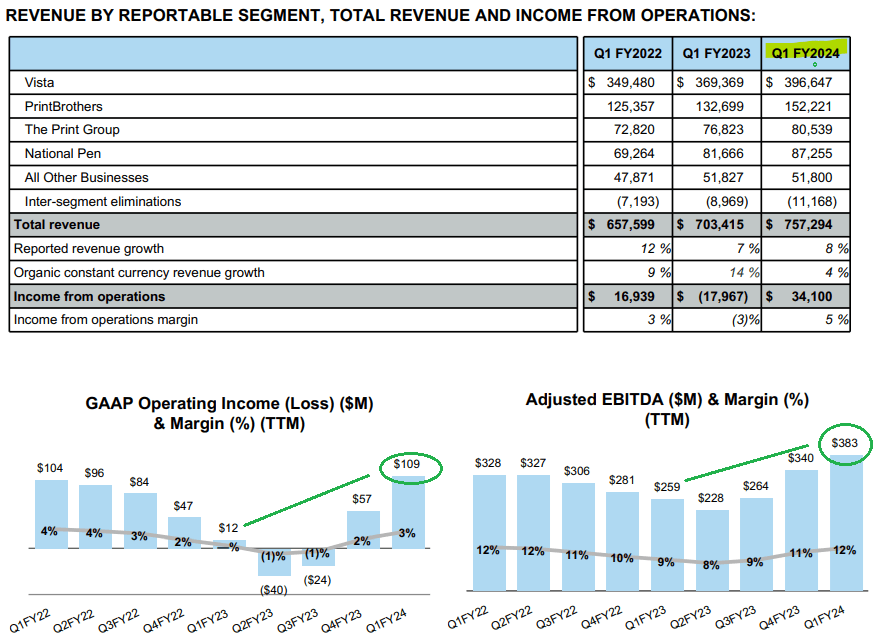

CMPR reports fiscal 2024 Q1 EPS of $0.17 reversing a loss of -$0.97 in the period last year and continuing a trend that has been sequentially stronger over the past two quarters. Consolidated revenue of $757 million, climbed by 8% year over year with gains across the main operating segments.

The story here is the sharply higher operating margin which reached 5%, compared to -3% in Q1 fiscal 2023 and even 3% in Q1 fiscal 2022. Efforts at savings and generating operational efficiencies have paid off.

The results are evident as advertising as a percentage of revenue is down 100 basis points from fiscal 2023 while an expansion of the gross margin explains much of the momentum. The company is also benefiting from lower inflationary cost pressures compared to headline-making supply chain shortages early last year.

Total adjusted EBITDA at $383 million over the trailing twelve months is also the highest since fiscal 2021 from the early stages of the pandemic boom. Similarly, free cash flow this quarter at $11 million reversed a cash bleed of -$52 million in the period last year.

{kind=link}

source: company IR

Operationally, a large part of the earnings strength has been from the Vista segment "Vistaprint" where sales increased by 7% y/y while the operating income was up 53% given the margin impacts.

Management notes that the average order value is up for most groups with repeat customers expanding into new categories of products as a runway going forward. The "PrintBrothers" segment with a large market position in Europe posted revenue up 15%, re-accelerating compared to a slowdown in fiscal 2023.

In terms of guidance, Cimpress is reiterating its full-year revenue growth target of "at least 8%", or at least 6% on an organic constant-currency basis. The bigger update here is that the company is hiking its EBITDA forecast slightly to "at least $425 million" compared to the prior figure closer to $420 million announced last quarter.

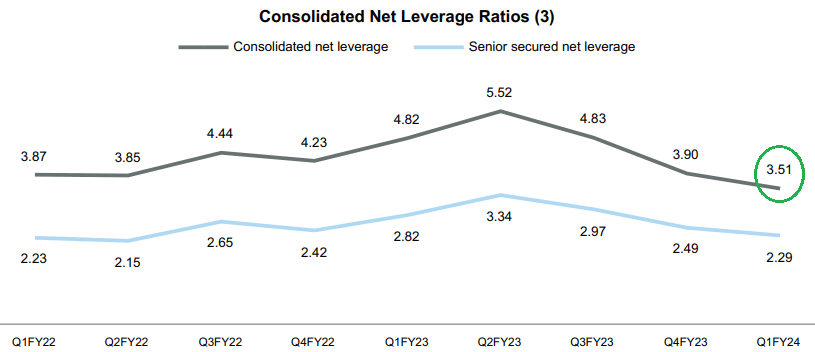

The company also expects to reach a net leverage ratio of 3.25x by year-end compared to 3.5x this quarter. We note that Cimpress' leverage has been declining over the past year and is now at the lowest level since fiscal 2021. While still a touch elevated, we believe this trend is a strong point in the company's investment outlook.

{kind=link}

source: company IR

What's Next For CMPR?

The financial turnaround at Cimpress speaks for itself and highlights the importance of this otherwise unique category of consumer products and business marketing tools.

Even as the global economy continues to transition towards digital commerce, the idea here is that Cimpress' core products between print materials and signage covering things like business cards, flyers, posters, banners, and custom packaging materials remain as relevant as ever.

At the same time, the company made efforts to diversify that exposure by expanding into new online categories including website builders and design services that can complement the overall ecosystem. Our take is that the latest trends reflect good brand recognition and building loyalty with customers.

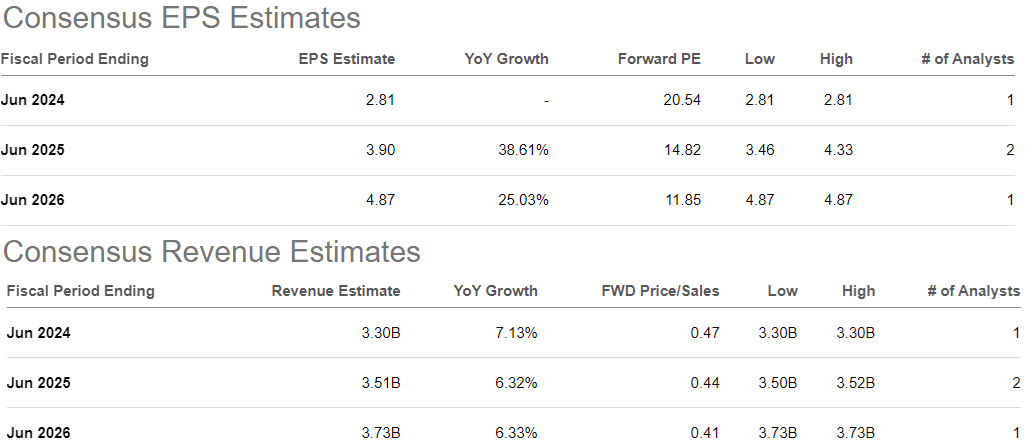

According to consensus, the forecast is for steady growth over the next few years while EPS accelerates higher based on the effort of supporting margins. The market expects 2024 EPS of $2.81, reversing two consecutive years of losses. The expectation for a more sustainable model can support earnings even higher through fiscal 2025 with an EPS estimate of $3.90.

In terms of valuation, we believe CMPR trading at a forward P/E of 21x or 15x into next year is reasonable considering the earnings runway and benefit of the ongoing balance sheet deleveraging as a tailwind for the stock.

{kind=link}

Seeking Alpha

That being said, it is clear the operating environment remains exposed to broad macro conditions. While 2023 has been defined by a resilient U.S. economy, trends like two-decade high-interest rates and even the Middle East conflict add a layer of uncertainty. A broader slowdown in consumer spending and general business conditions would undermine demand for Cimpress products and its earnings outlook.

We can also cite an aspect of intense competition globally from category-specific startups or emerging players attempting to undercut prices. New tools available online including capabilities from generative AI add a layer of uncertainty regarding the company's competitive advantage and market positioning as a risk to consider down the line.

Final Thought

We're bullish on CMPR and expect the company to continue executing its operational and financial strategy. The upside here is that there is room for growth to ultimately outperform expectations and the company could get a boost if macro conditions evolve more favorably.

It's not going to be a straight line up for the stock, and the all-time highs for CMPR are likely out of reach for the foreseeable future, but we ultimately expect shares to be trading higher by this time next year.

For further details see:

Cimpress: Bullish Amid Ongoing Turnaround And Climbing Profitability