CMPR - Cimpress Moves Forward Despite The Balance Sheet Concerns (Rating Upgrade)

2023-08-15 07:03:42 ET

Summary

- Cimpress stabilizes with pricing momentum and lower marketing costs leading to higher operating profits in Q4 2023.

- The company's financial health remains questionable with negative shareholders' equity and high long-term debt.

- CMPR's management expects FY2024 revenues and adjusted EBITDA to increase with cost reduction efforts.

Cimpress Stabilizes Before FY2024

I discussed Cimpress plc's ( CMPR ) strategies in detail in my previous article . Since then, CMPR has rolled back the pricing discount of the last year, which has given it leverage with pricing when input costs decrease. The pricing momentum will likely continue in 2024. On top of it, lower marketing and selling costs led to higher operating profits in Q4 2023 (for the year ended June 30, 2023). The economic indicators have also been resilient against the fear of a recession in the recent past.

But the company’s financial health remains questionable. Its debt-to-equity ratio is not meaningful because its shareholders’ equity is negative. Its long-term debt is relatively high, although, with higher EBITDA, the net leverage should fall by FY2024. Cash flows dwindled in FY2023, which is not conducive to debt reduction efforts. The stock is reasonably valued versus its peers. As its outlook brightens, I suggest investors “hold” the stock for the medium term.

Strategy And Margin Growth

CMPR’s management sees no reason to give pricing concessions in the current environment. Investors may note that in the previous year, it gave pricing discounts because of the lack of demand in the market. It considers the current situation conducive to price optimization. In the future, it may have more leverage with pricing as input costs decrease. So, if the competitors lower their prices, they won’t need to give away market share because they can outlast the competition with higher pricing power. So, the company's margin will likely hold even if revenues fall due to lower prices.

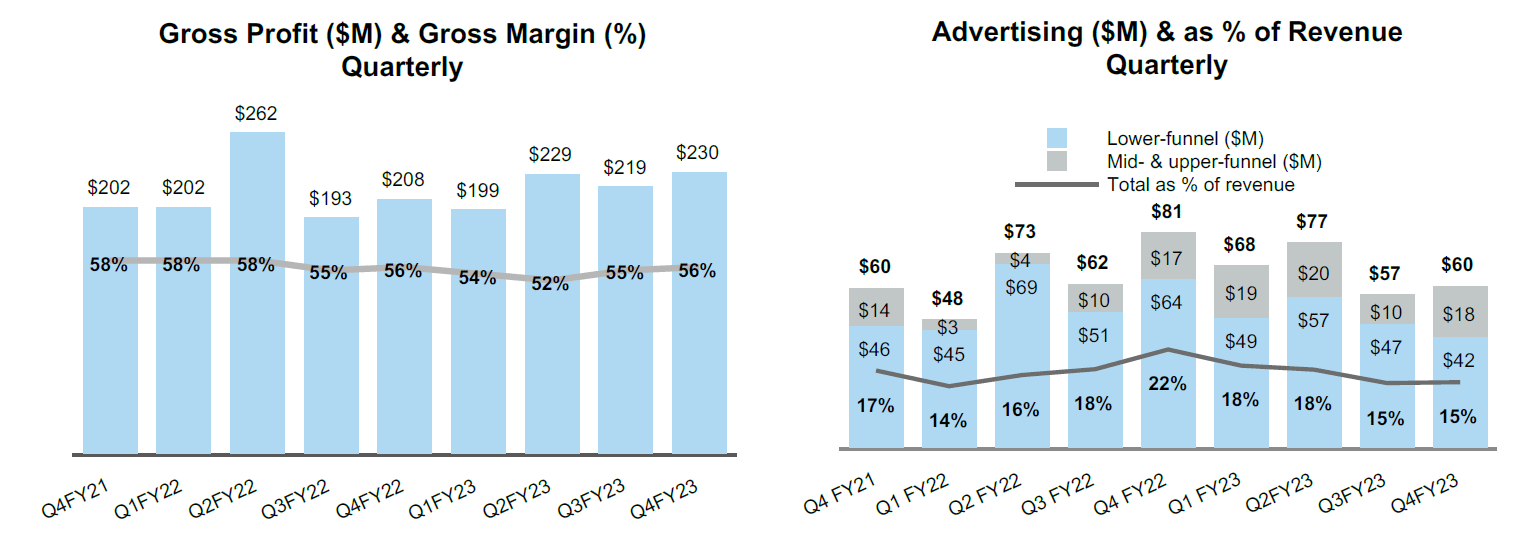

In this context, we may look into Vista’s performance. Better pricing, adding new customers, and increased bookings led to the segment’s 12% organic growth in Q4 2023. The EBITDA profitability expansion in Vista was well-balanced. Gross profit contributed one-third to the expansion, while the rest came from advertising efficiency and lower operating costs. However, the company’s costs typically increase in the year's first half. So, its margin may come under pressure early in 1H 2024.

Cost Reduction And FY2024 Outlook

{kind=link}

CMPR's Q4 2023 Press Release

It has also been focusing on marketing development in a competitive market. It has introduced more personalization to improve customer experience, including design capabilities. These initiatives are expected to drive profitability downstream through physical products. The product development investment can improve order value, retention, and conversion rates. Lower marketing and selling costs led to higher operating profit in Q4. Year-over-year, the company turned to an operating profit in Q4 2023 compared to an operating loss a year earlier.

Given the tailwinds discussed above, CMPR’s management expects FY2024 revenues to increase by 6% compared to FY2023, led primarily by growth in volume. Pricing traction will help the improved result, too. Adjusted EBITDA can increase by ~24% in FY2024. The company estimates that cost reduction, which amounted to $24 million in FY2023, will boost the EBITDA by $76 million incrementally in FY2024. As a result of higher EBITDA, the net leverage should fall below 3.25x by FY2024.

Recent Key Indicators

{kind=link}

tradingeconomics.com

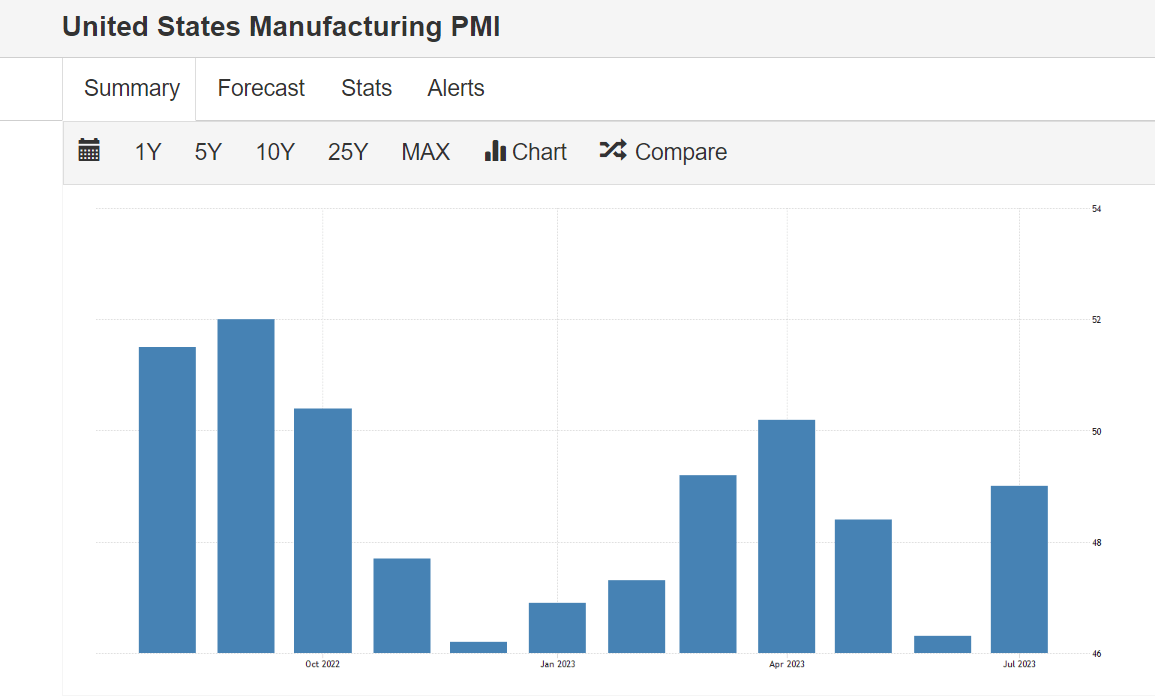

The US PMI failed to reach 50 in July. Any score below 50 suggests an activity contraction. However, July’s score was the best over the past three months. The companies scaled back their input buying due to soft domestic and external demand conditions.

On the other hand, unemployment was low as the US companies seemed to have a more optimistic view of the economy. Selling prices were stable in the manufacturing industry. So, the economic conditions remained mixed, but an improvement over the previous couple of months.

Q4 Segment Drivers And Outlook

{kind=link}

CMPR's filings

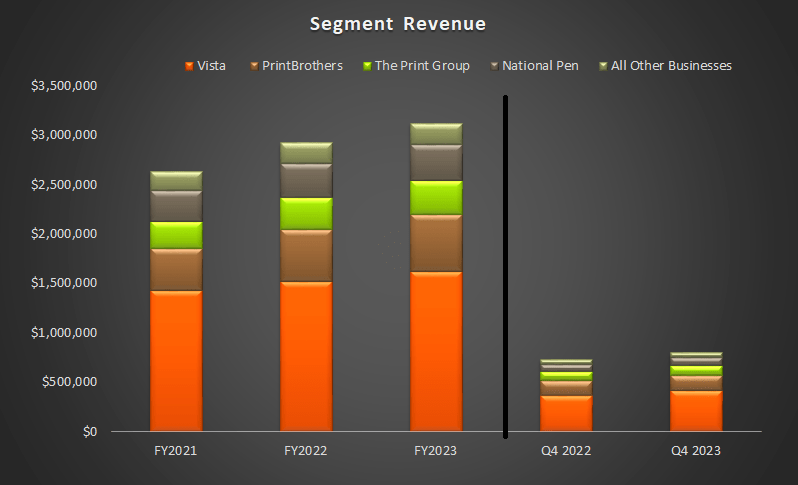

Segment-wise, CMPR’s revenue growth in the Vista segment was 11.4% in Q4 2023 compared to a year ago. The segment saw a 19% adjusted EBITDA margin. The segment accounted for 51% of the company’s consolidated revenues in Q4, so its contribution is essential to its financials. Vista’s contribution to the consolidated EBITDA was the highest in Q4. The gross margin (real terms) expanded by 170 basis points, year-over-year. I expect the pricing benefits, which positively impacted the margin in Q4 2023, will continue to benefit in 1H 2024.

However, the segment will likely face headwinds, too. The promotional products category grew fast in Q4 2023, but will likely slow down in Q1 2024. Pricing, on the other hand, will maintain its positive momentum. Beyond 2024, a favorable product mix will continue positively impacting the segment result.

Among CMPR’s other segments, National Pen grew the most in Q4 2024 compared to a year ago (9.6% up), while the growth in The Print Group was the lowest (4.4%). But the adjusted EBITDA margin for The Print Group was the highest among its segments in Q4 (21.6%). Overall, the company’s consolidated adjusted EBITDA grew by 200% year-over-year in Q4. The improvement includes the benefit of the $100 million of annualized cost reductions. The management believes it will have more cost-reduction opportunities in the coming quarters.

Cash Flows, Debt, And Dividends

In FY2023, CMPR's cash flow from operations decreased by 41%, despite higher revenues. Adverse changes in working capital primarily led to the cash flow decline. Free cash flows (or FCF) also decreased sharply, by 54%, in FY2023 compared to a year ago.

CMPR's debt-to-equity ratio is not meaningful because its shareholders’ equity is negative due to treasury shares (i.e., share repurchases) and accumulated other comprehensive losses. The company uses liquidity, among others, for share repurchases, acquisitions, and debt reduction. In Q4, it allocated $45 million toward repurchasing a part of its debt scheduled to mature in 2026. With the planned cost reductions, it aims to reduce net leverage to below 3.25x by FY204.

What Does The Relative Valuation Tell Us?

{kind=link}

Author Created And Seeking Alpha

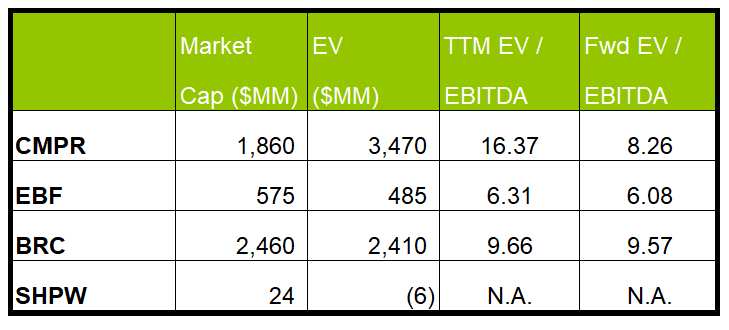

CMPR's forward EV/EBITDA multiple is expected to contract versus the current EV/EBITDA. The rate of contraction is steeper than its peers. This implies that its EBITDA is expected to rise more sharply than its peers next year. This should typically result in a higher EV/EBITDA multiple.

The company's EV/EBITDA multiple (16.4x) exceeds its peers' (EBF, BRC, and SHPW) average. However, the current multiple is also higher than its past five-year average. So, the stock is marginally overvalued compared to its peers.

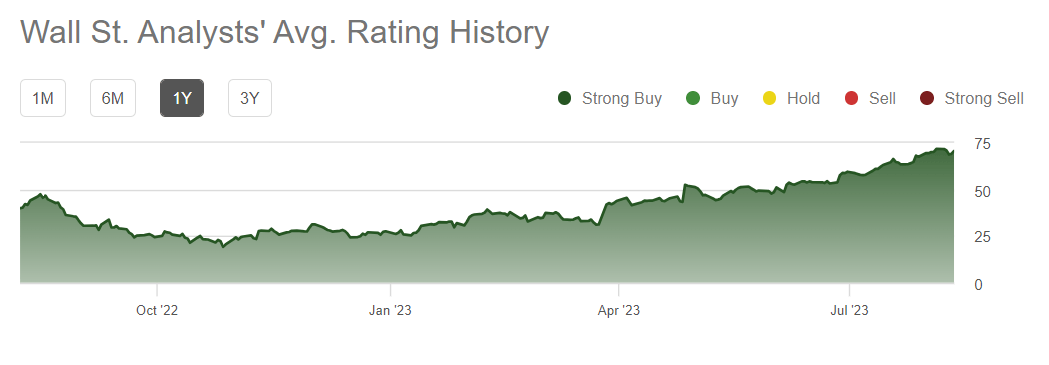

Analyst Target Price And Rating

{kind=link}

Seeking Alpha

According to Seeking Alpha , two analysts rated CMPR a "buy" (including "Strong Buy"), while none recommended a "hold" or a "sell." The consensus target price is $89, which indicates ~26% upside potential at the current price.

Why Do I Change My Call?

In my previous article, I described why I was relatively bearish on the stock. The company’s technology infrastructure appeared to fall short of acquiring new customers, which, in turn, can dilute its brand. The industry activity indicators were not favorable. Its finances were in the doldrums, given the negative shareholders’ equity. I wrote :

Because the company has committed to long-term marketing spend while pursuing a new business model, if the economic growth falters, it can have a resounding effect on its costs and profit margin.

After Q4 2023, CMPR had a few things going for it, including better pricing, adding new customers, and increased bookings. The industry environment has brightened. And the company’s cost rationalization efforts will dent the effect of higher input costs. Although its balance sheet and relative valuation do not suggest any turnaround, I think the stock is apt for a “hold” at this level.

What’s The Take on CMPR?

{kind=link}

Seeking Alpha

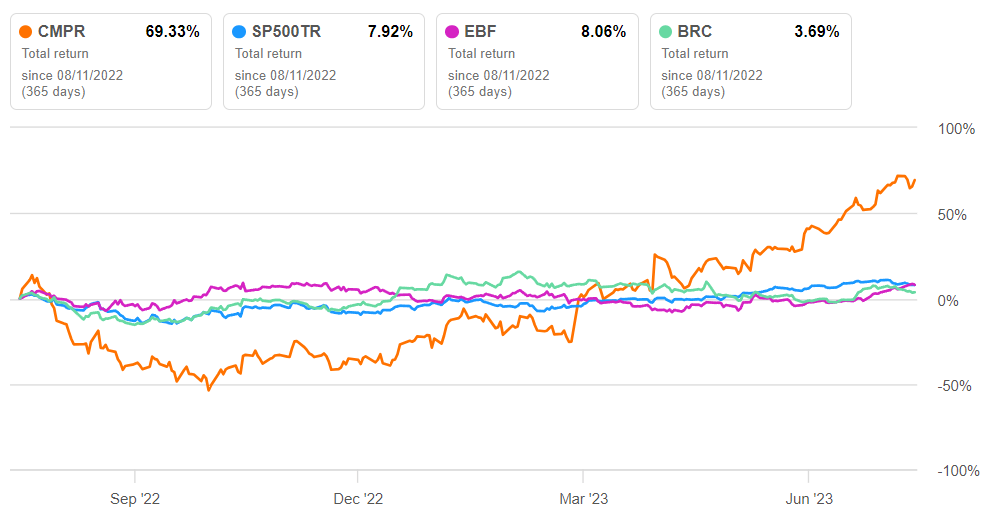

After the end of FY2023, better pricing, new customer additions, and robust order bookings reflect a healthier state for Cimpress. In a competitive market, it focused on marketing development. Vista, the most prominent of its segments, witnessed a well-balanced margin expansion in Q4. As pricing maintains its positive momentum, it will likely see continued margin expansion in FY2024. The company’s cost curtailment exercises will also help its operating margin growth. So, the stock outperformed the SPDR S&P 500 ETF ( SPY ) in the past year.

On the other hand, seasonality can affect the company’s operating margin in early FY2024. The economic conditions remained mixed, and there is uncertainty over the medium-term state of the economy. The promotional products category benefited its Vista segment handsomely in Q4 but may dip in the next quarter. A more pressing issue is the balance sheet, where negative shareholders’ equity has kept the issue of financial risks high. However, the risk factors have been prevalent for many quarters while the company looks to deleverage. Given the relative valuation, investors may “hold” it for a modest return in the short-to-medium term.

For further details see:

Cimpress Moves Forward Despite The Balance Sheet Concerns (Rating Upgrade)