CMPR - Cimpress: Solid Top Line Growth Yet Profitability Pressures Remain Stark

2023-03-29 11:24:33 ET

Summary

- Cimpress has come out of the pandemic period and returned to quality top-line growth, achieving a record revenue level even before releasing fiscal Q4 figures.

- However, it has seen a deterioration in both gross margin and net income, having accrued a loss for the past 3 years.

- This has forced the firm to accrue high levels of debt and has also seen its cash flow go negative on a levered basis; additionally, book value has gone negative.

- Nonetheless, Cimpress has moderated its OpEx footprint and could see the other metrics start to add up if revenues continue climbing and costs moderate; for now, it's a hold.

Overview

Cimpress (CMPR) is a commercial printing company. The company is an owner of a portfolio of 'mass customization' businesses, each of which is a distinct commercial printing entity operating across distinct locales. The company has operations primarily across both the USA and the European Union.

{kind=link}

cimpress.com

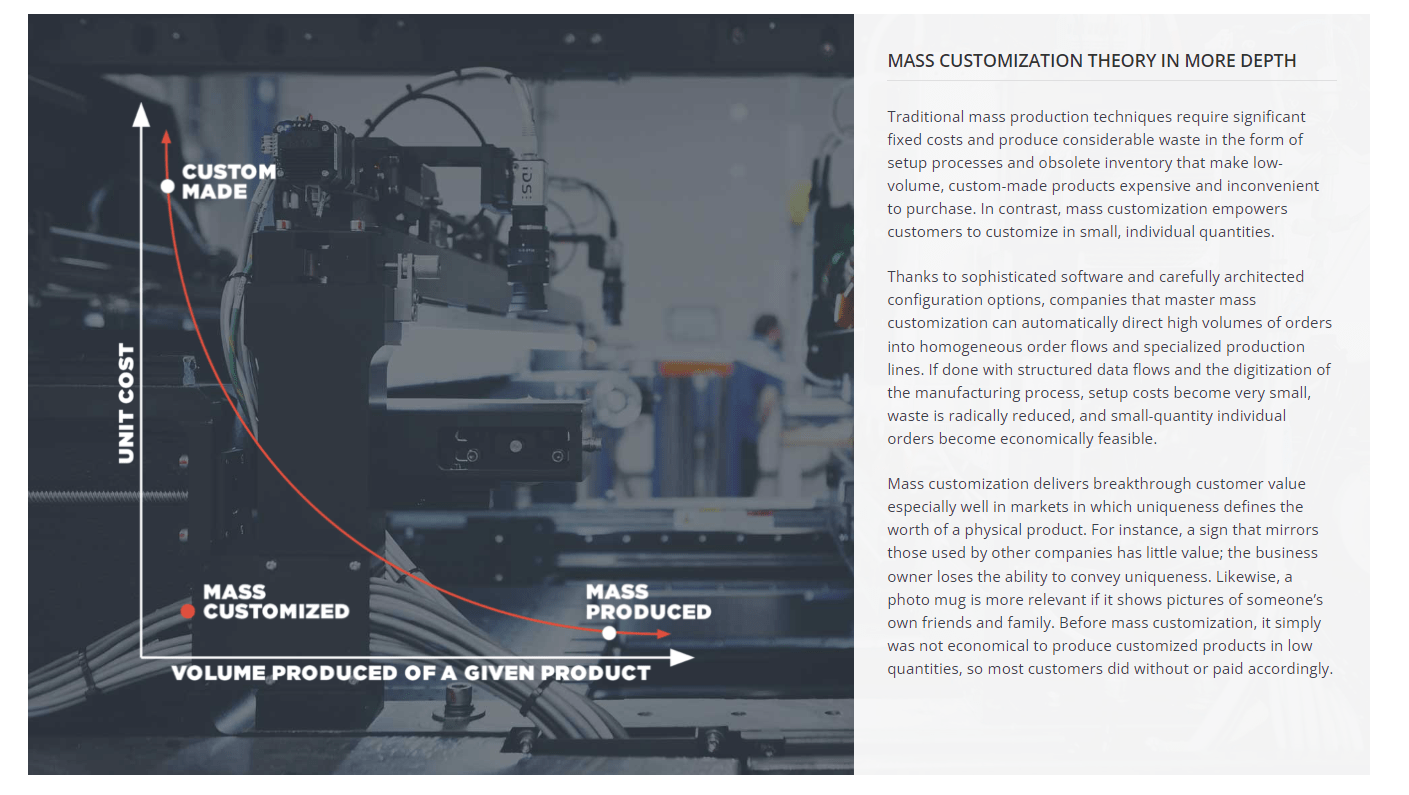

The firm makes clear that its mass customization is distinct from standard commercial printing; this ain't your grandpa's commercial printing. Mass customization involves manufacturing custom orders in relatively small order sizes, all the while maintaining the economics of truly mass-produced products. I do believe this is actually a credible differentiator for the firm.

{kind=link}

Indeed, the company appears to have a shared technical backbone implemented via services (in the software sense) across all of its businesses. This is reminiscent of how Amazon Web Services first built up its business in 2006 and how many other software firms do so today. If done properly this service-based architecture drives information and technology economics across the firm.

Of course, the real secret sauce here - the enabler of economic mass customization - is going to occur in manufacturing facilities. What is interesting here is that Cimpress has layered these pieces of software across its physical infrastructure, allowing employees to control manufacturing processes on a modular and granular level - enabling mass customization.

cimpress.com

The Stock

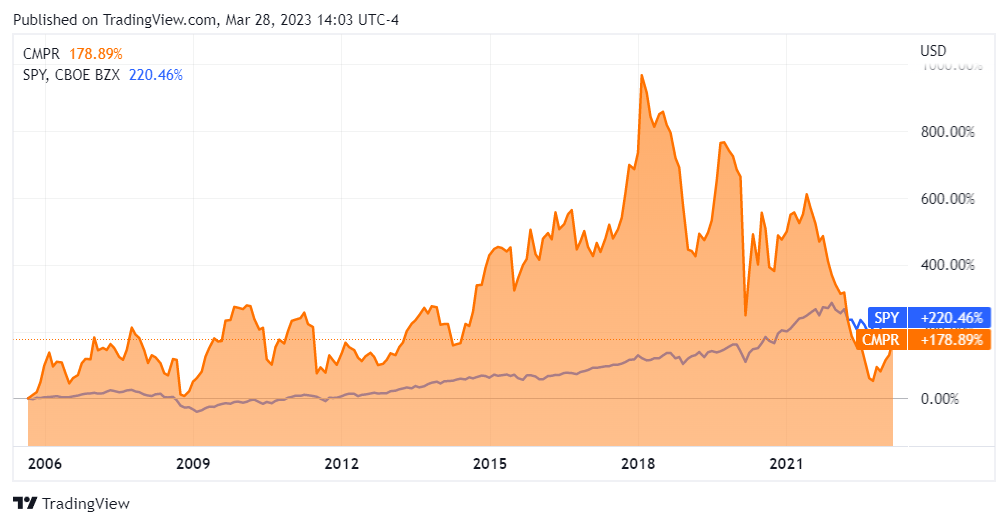

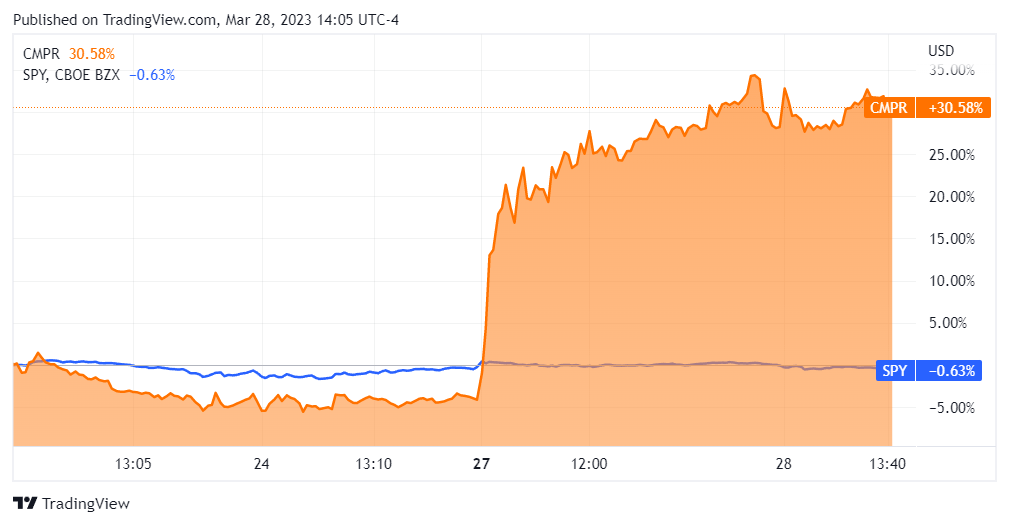

While generally CMPR is a relatively high-quality stock that has outperformed the S&P500 (indexed through SPY, unadjusted for dividends), it appears to have been sold off significantly from Q2 2021 through to Q3 2022 and is now underperforming the index.

{kind=link}

Zooming in to this somewhat, we see that CMPR has been rapidly clawing back to parity with the S&P500 - something it still hasn't achieved - even through 2 earnings misses.

{kind=link}

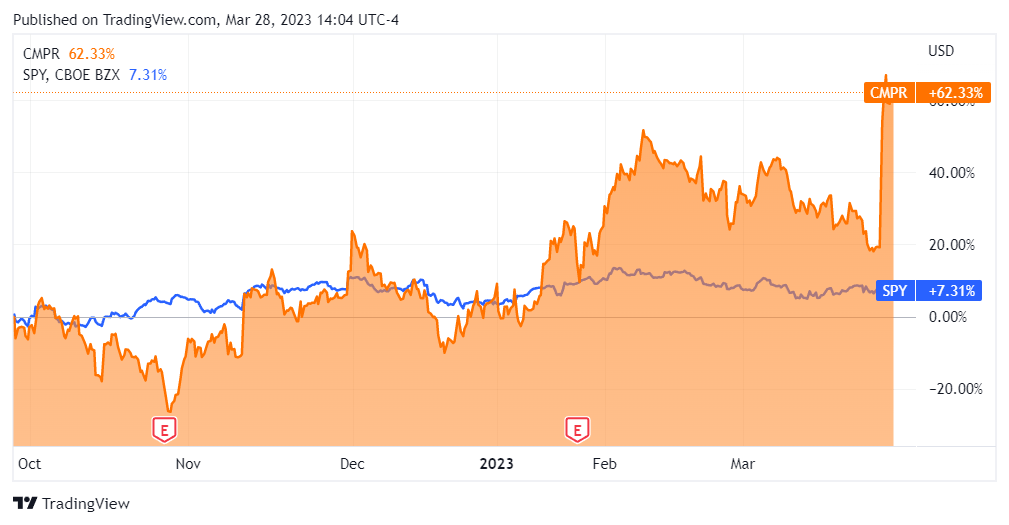

Indeed, the stock appreciated significantly on March 27th, 2023, gaining over 30% in one day. This caught my eye and made me consider looking into it. There doesn't appear to be an immediately identifiable catalyst for this move, but makes the story all the more interesting since the stock is still below where one may expect it to be across its historical trading multiple vis-à-vis the S&P.

{kind=link}

Considering these interesting technical aspects around the stock, I thought it would be worthwhile to review the fundamentals and see how sensible Cimpress' current valuation really is.

Financials

Since this is a relatively mature company that has been operating since 1994 (and public since 2005, formerly as Vistaprint) we can analyze it holistically. Please note that this firm's fiscal year concludes in June of each calendar year.

Starting with revenues, we see an overall picture of growth. Generally growing each and every year, the part worth looking at here is the revenue decline during the pandemic period that started in 2020. This was a first-of-its-kind event for Cimpress that saw its top line decrease 9.8%. As of Q2 2022, the company is back on its feet and has posted results that are higher than they were pre-pandemic. Indeed, its current year appears to be a record setter as it has already beat previous yearly revenue figures before disclosing results for Q1 2023 (Q4 in fiscal terms). This is a good trendline.

{kind=link}

The counterpoint here would be the gross margin pressure that the company has been facing, something that has been brought up on earnings calls as an ongoing concern - albeit a moderating one - for the firm. As we can see, Cimpress is operating with a lower and lower gross margin every quarter, with this figure having dropped 19.07% over the last decade. Unsurprisingly this has translated into a higher cost of revenues for the company and may be impacting the bottom line.

{kind=link}

Looking over at net income, the effects of these cost pressures are apparent. What was once a relatively consistently profitable company has now had 3 years of net losses - with the largest net loss yet seen already accrued in the first 3 fiscal quarters of this year. This is disconcerting to say the least.

{kind=link}

The company's operations are going to determine if it can swing itself back to a profit or not. Here, the picture is mixed. The first thing that I would like to note is that overall OpEx has also declined significantly over the past decade, having been under 50% over the last 5 years. This roughly tracks the company's decline in gross margin and may leave room for a profit after all. We can't infer too much from the negative operating income number as the fiscal year at present is not yet complete.

{kind=link}

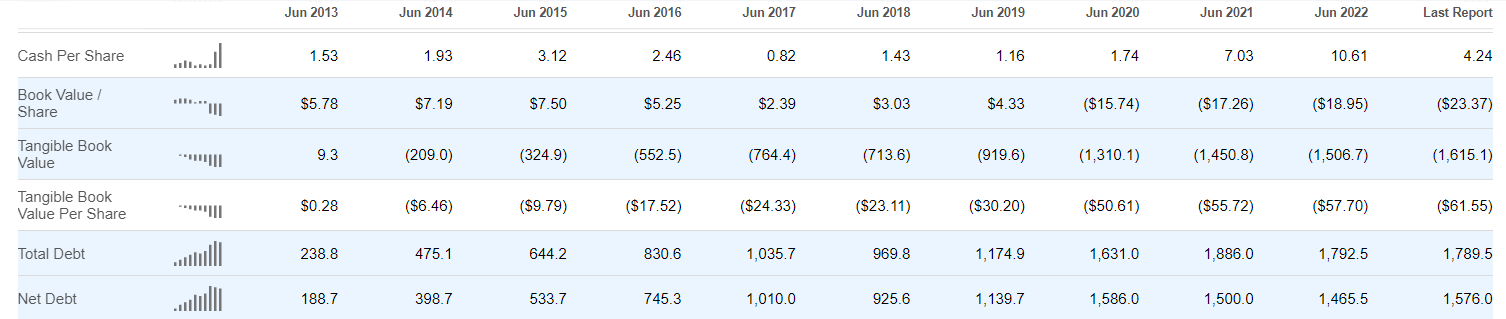

Given the rough operating metrics we need to now look at the balance sheet. Here there are certainly some red flags as well in my view. The first is the fact that the company has swung into negative book value as a result of increasing debt levels. Keep in mind this is a company with a lot of PPE - property, plant, and equipment - by virtue of being a manufacturer. Generally firms of this nature have a significant backstop as to physical capital, providing what may be considered a margin of safety for investors. Unfortunately this has evaporated - and appears to be worsening. Total debt and net debt, while not at record levels, are within a stones throw of these.

{kind=link}

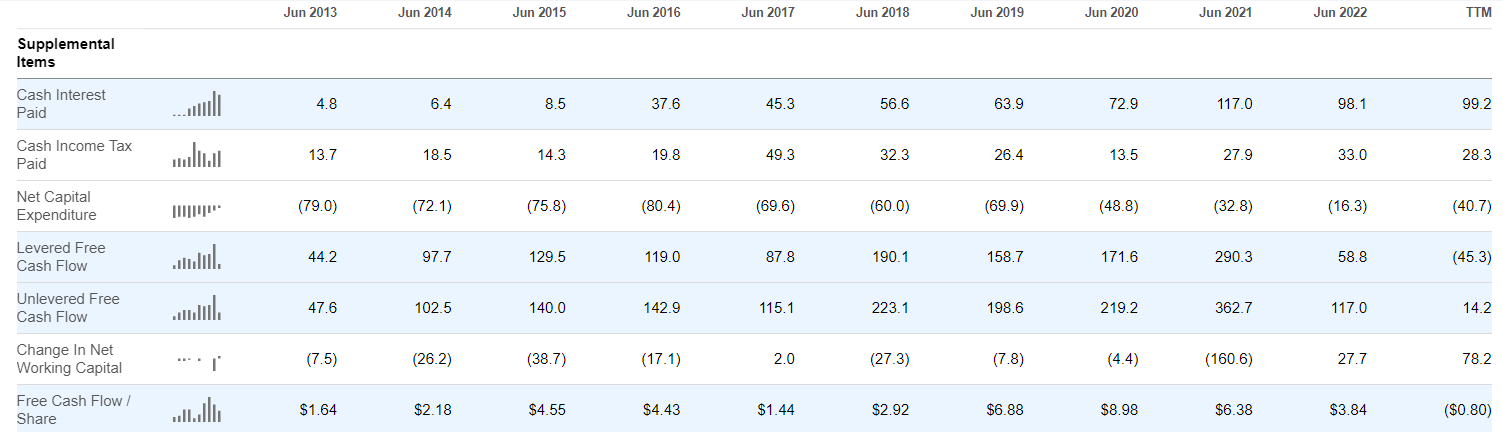

These debt levels have also resulted in the company being record levels of interest, which has led to negative cash flow so far this year. While the fiscal year is not yet over, this is a certainly a point of concern. I would not be surprised if the fiscal year ended up negative as to cash flow given the significant levels of debt that the company is paying for.

{kind=link}

Conclusion

Overall the financial picture for Cimpress is quite mixed. Over the last decade, gross margins have compressed materially - but so have operating expenditures. Net income has become negative in the last 3 years. Book value has gone starkly negative as debt has ticked up. Most critically, free cash flow is now negative and very well could be negative for the fiscal year. The only bright spot here is what appears to be a return to significant revenue growth. Having come out of the pandemic period, the firm is posting record revenues. This will be the metric to watch with this stock. Revenue will either continue growing and make everything else add up - or it won't.

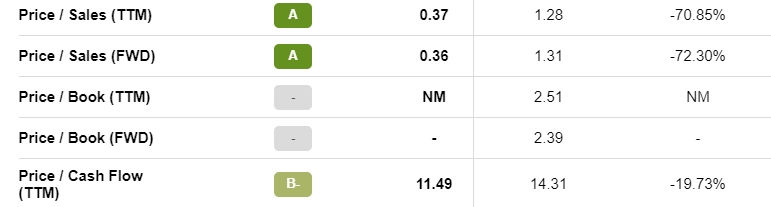

This stock is trading very cheaply on a sales basis and quite cheaply on a cash flow basis. Of course, since cash flow is still trailing negatively for the most recent fiscal year, I would be cautious about this metric. The next filing could see that number become negative, and it now stands as negative when we take out 1 quarter from the last 4.

The cheap sales valuation makes sense in light of the other metrics. However, the other metrics are stark enough that I wouldn't be so keen on entering the stock. The market's recent action may indicate that some parties disagree with this sentiment, although I am not as yet convinced. What I want to see with the next earnings report will be continuing revenue growth, moderating cost pressures, and a stabilizing cash flow figure. Until we shine a light on these metrics, I think it's fair to call this a hold.

{kind=link}

For further details see:

Cimpress: Solid Top Line Growth, Yet Profitability Pressures Remain Stark