CINF - Cincinnati Financial: Equity Market Exposure And Improved Underwriting Create A Compelling Opportunity

2023-10-16 21:40:56 ET

Summary

- Cincinnati Financial's shares have remained flat over the past year, but the company's underwriting improvement and investment portfolio make them attractive.

- The company's operating income doubled to $191 million, driven by a decrease in its combined ratio to 97.6%.

- Cincinnati Financial's investment income rose 13% due to higher interest rates, and its equity portfolio provides for long-term value creation.

Shares of Cincinnati Financial ( CINF ) have spent much of the year stuck between $100 and $110, flat over the past twelve months, and generating about an 8% return since my buy recommendation last October . I continue to view shares as attractive, given underwriting improvement and the market’s under-appreciation of the value creation in its relatively uniquely structured investment portfolio.

{kind=link}

In the company’s second quarter , Cincinnati Financial reported EPS was $3.38, up dramatically from -$5.12 last year. Mark-to-market movements in its investment portfolio flow into net income, which is why we can see wild swings in GAAP earnings to the point they are of little value in determining the performance of the insurance operations. $8.11 of its $8.50 increase in GAAP earnings was due to the market swing (the market fell last Q2 and rose in Q2 2023). Instead, we can look to operating income, which excludes market movements, and this measure doubled to $191 million, or $1.21 a share from $0.59 last year.

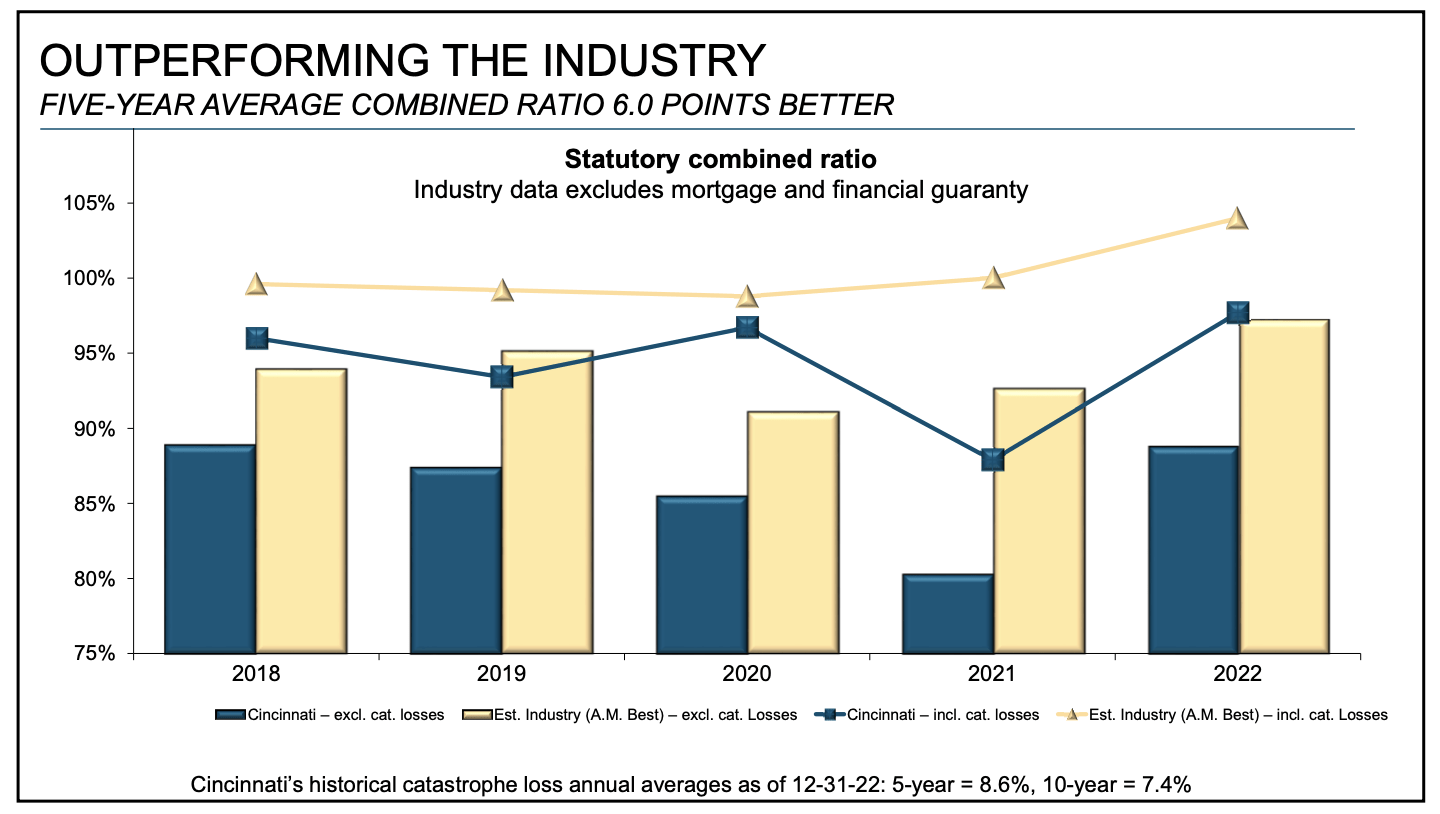

This improvement in operating income was due to CINF’s combined ratio coming down 5.6pts to 97.6%, in-line with management’s 95-100% target. This ratio compares what CINF pays out on its insurance policies relative to what premiums it earns, with 100% representing breakeven. In other words, during the quarter, CINF was earning $2.4 for every $100 of insurance.

This improved result came even as CINF saw a 12-point contribution from catastrophic weather events, which can be volatile quarter to quarter. Management expects to see this contribution from catastrophes fall during the balance of the year, and indeed, it has been a relatively quiet hurricane season, which should be helpful to results. As such, we should continue to see improved underwriting results in coming quarters . While last year underwriting results were weaker than normal, this improvement is consistent with the fact CINF has been an industry-leading insurer for years.

{kind=link}

Last year, CINF’s combined ratio rose, but this was widespread in the industry. A major reason for this was excess inflation. When a car or property is destroyed, the insurer needs to pay to replace or fix it, and those costs rose more than expected making losses more “severe” than modelled. In response to this, insurers have been raising prices. CINF reported its net written premiums rose 9% thanks to mid-single digit pricing increases; higher prices should guard against increased costs and are helping to bring results back to normal levels.

Alongside improved underwriting, investment income rose 13%, which was primarily due to a 19% increase in interest income as CINF benefits from higher rates. CINF maintains a $23.4 billion investment portfolio, which essentially has two roles: to cover future insurance losses and to drive book value growth.

For the first role, it maintains a conservative fixed income portfolio, which provide 108% coverage against its $11.9 billion in insurance reserves. The average bond it holds is A2/A rated with just 5% of the portfolio rated below investment grade. It has a 4.6 year duration, which means about one quarter of the portfolio matures over the next three years. As bonds issued in the 2019-2021 low-rate environment mature and are reinvested at today’s rates, we see the yield on its portfolio steadily rise.

Indeed, the portfolio’s after-tax yield was up from 3.31% last year to 3.59% last quarter. We should see continued increases from here. Each of the next three years, just by rolling over maturities at rates consistent with the forward curve, annual operating earnings will rise by about $0.05-$0.08. This may not seem like much, but that does provide a 1% boost to annual earnings growth over the next three years without actually having to do things or grow new business--this occurs even with the markets pricing in three cuts next year . Should the Fed hold rates steady or raise them further, these net interest gains will be larger. CINF should ultimately see portfolio yield increase for the next four to six years, based on current bond market pricing, making it a rare winner from higher rates.

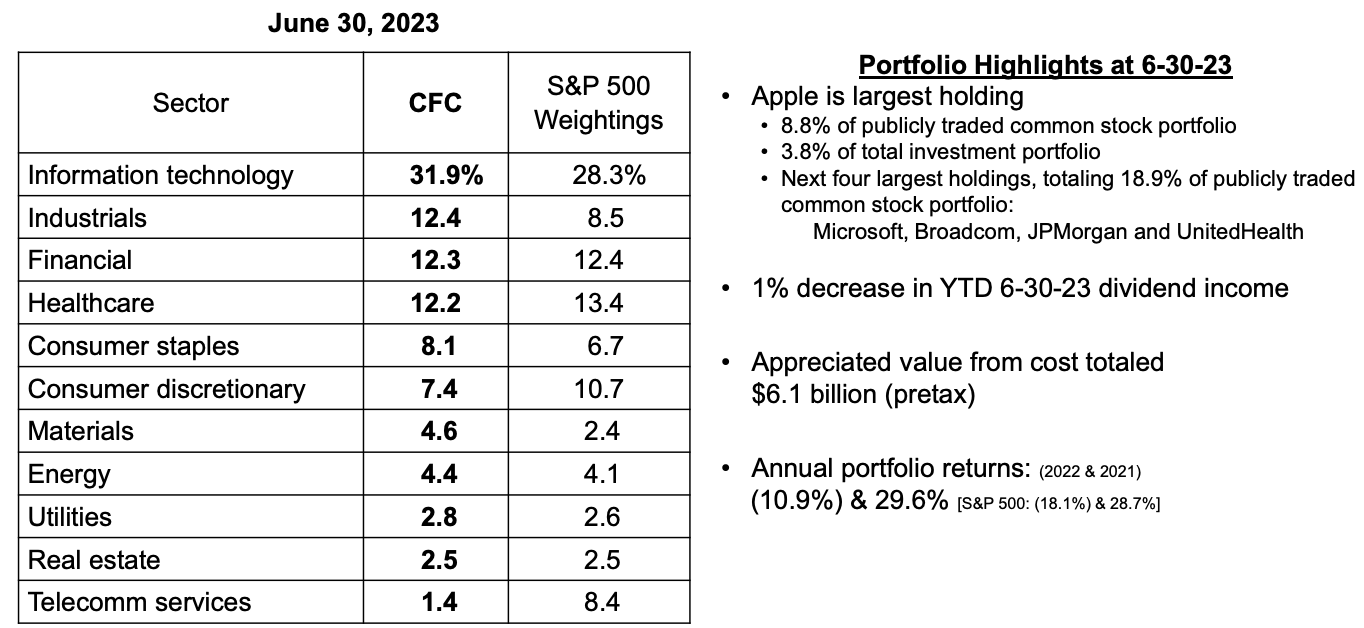

With insurance reserves covered by this fixed income portion of the portfolio, CINF invests the remainder in stocks to generate higher long-term returns. Its equity portfolio was $10.1 billion at the end of Q2. This is somewhat similar to how Berkshire Hathaway ( BRK.B ) has managed is insurance business to great success for shareholders. I would note though that unlike Berkshire, CINF does not make as concentrated investments. While there are some differences, as you can see below the portfolio is aligned to be fairly similar to the S&P 500. This portfolio is up about 150% from its cost basis, speaking to the value creation of this structure.

{kind=link}

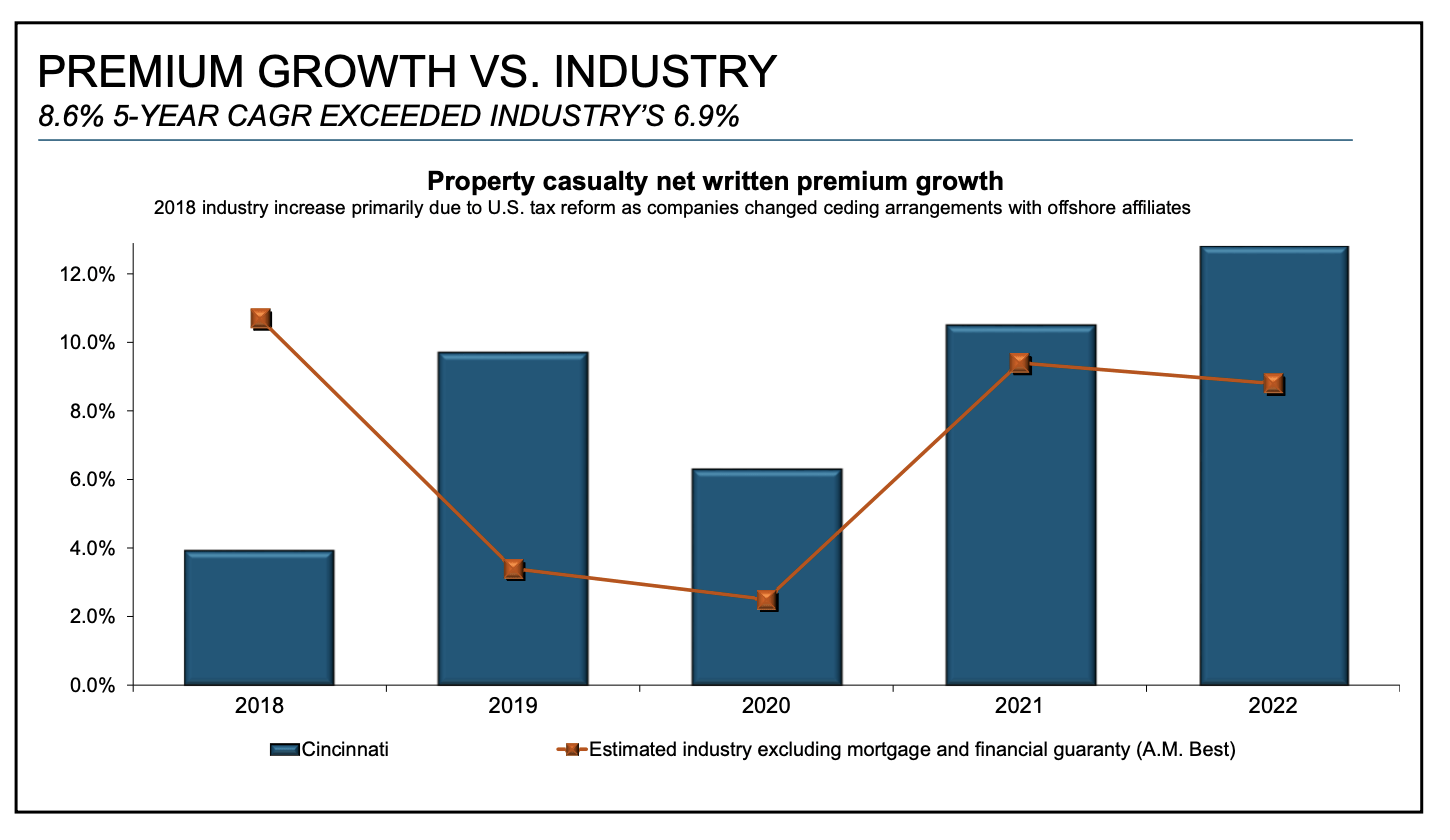

The $11.9 billion insured reserves essentially is the “float” from which CINF borrows from policyholders (who pay premiums today for claims in the future) into which it invests in bonds, and its surplus beyond that is invested in equities. However, because CINF generates an underwriting profit over time (a combined ratio below 100), it only pays policyholders back 95-100% of what it was paid, essentially borrowing at a negative rate. Meanwhile, it earns interest on its fixed income holdings, adding to its profits. This is how its float becomes a profit driver, which is why I like to see premiums and reserves grow over time. That has been happening, with reserves growing $600 million this year. As you can see, CINF has been a steady premium grower over time thanks to pricing increases and market share gains.

{kind=link}

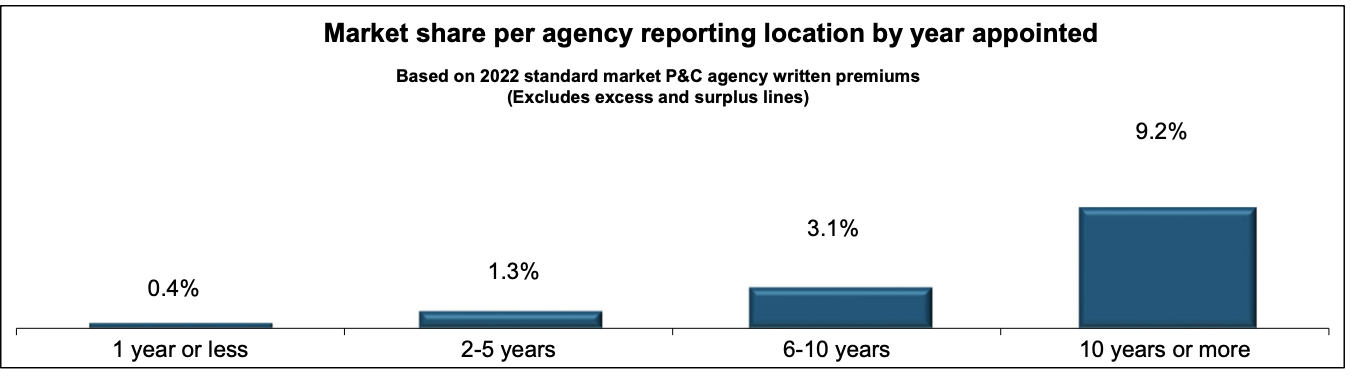

It is particularly encouraging to see how the longer an insurance agent works with CINF the higher the share of their business CINF earns, speaking to fair customer service and pricing. CINF is also a smaller firm than an AIG ( AIG ) or Travelers (TRV), so new agents may not as quickly pivot their business towards them but do so over time as they see positive experiences. I highlight this because CINF has been aggressively signing up agents—209 last year and 159 in H1 2023. As these relationships mature, CINF is well positioned to see ongoing premium growth, in turn adding to its float and increasing its investment income.

{kind=link}

Q3 Preview

When the company reports third quarter earnings, I will be particularly interested to hear updates on how CINF is faring with new agents. About 55% of CINF's business comes from commercial lines, 23% personal lines, and the remainder a series of niche products. Commercial lines have been growing more slowly but tend to be more profitable as plans can be specifically tailored for a business's needs. With these agents gradually spending more time on Cincinnati's platform, I am hoping to see some reacceleration in growth here and the composition of premiums shift somewhat away from personal.

A shift away from personal will also help to provide further momentum in lowering its combined ratio. Having fallen back below 100, CINF is again generating an underwriting profit, but 97.6 is weaker than normal. Given the relatively mild storm season, an important benchmark to watch will be its catastrophe losses. I am looking for them to fall to about 10 pts from 12 pts in Q2; this should provide a nice tailwind to underwriting profits and provide further confirmation that CINF is returning to form on underwriting.

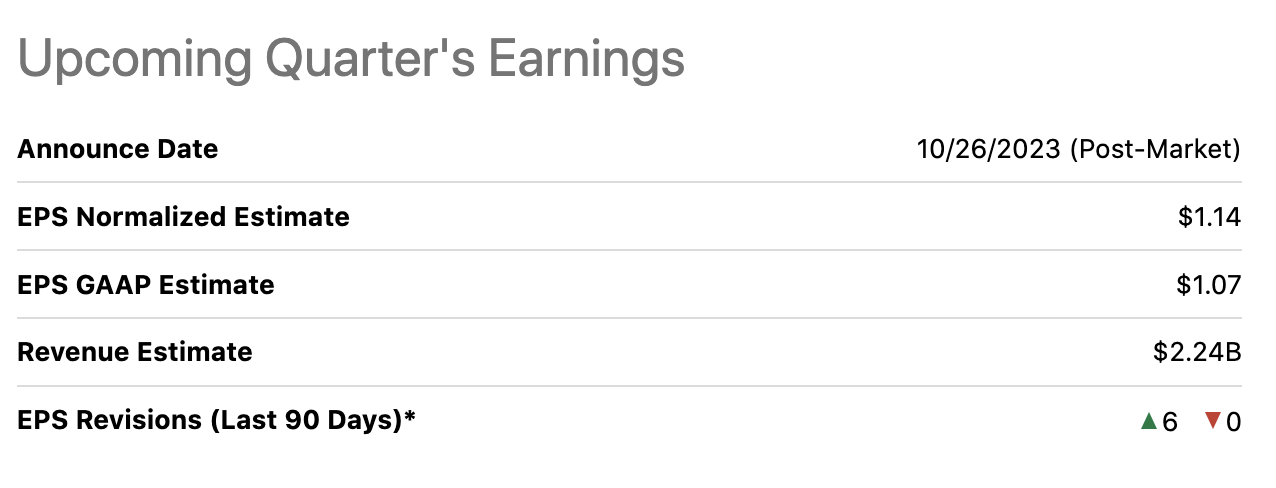

As of now, normalized consensus is $1.14 for CINF's Q3 results to be reported later this month. This consensus excludes the mark-to-market movements on its investment portfolio discussed above. That would actually mark a slight decline quarter over quarter. Given interest income should be a $0.01-$0.02 tailwind and that catastrophe losses in my view are likely to improve, I think CINF is relatively well positioned to beat estimates and I am expecting earnings in the $1.21-$1.25 area.

I would note that the last six analyst revisions to estimates have been higher, and so others may be seeing some of the positive momentum that I am.

{kind=link}

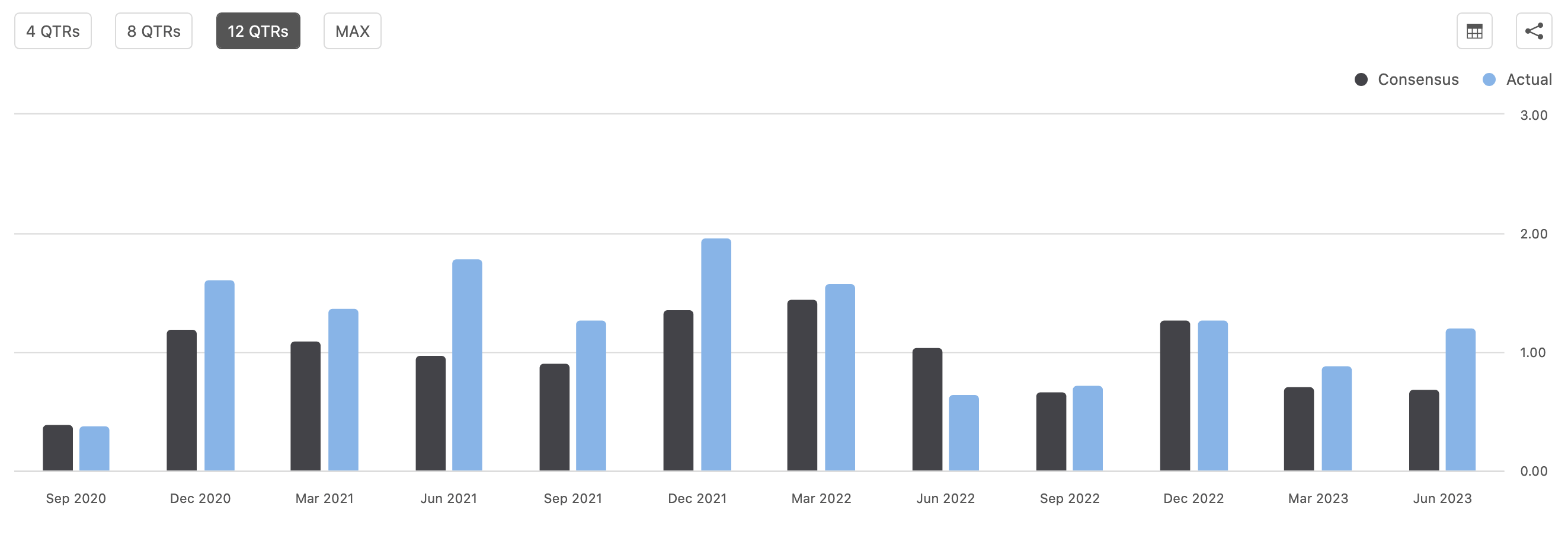

CINF has also historically beaten consensus, and that includes two consecutive strong beats as its underwriting profits have steadily improved. With the pricing increases that the company has pushed through and the fact that inflation has moderated, which should reduce the severity of losses, I believe CINF is positioned well to exceed expectations, adding to my view investors should look to add shares.

{kind=link}

Conclusion

At a 95% combined ratio, alongside interest income yields rising about 10bp due to reinvestments, the insurance and float will generate about ~$775-825 million in after tax income over the next year. At even 10x earnings, that is an ~$8 billion business. Importantly, the earnings power of this unit continues to grow as it increases its business and adds to its floats.

Its 8% fixed income overflow provides another ~$600 million of value, which when combined with a $10 billion equity portfolio, provides a fair market value of ~$18.6 for CINF or about $120 per share. At the current price, it is trading at less than 7x its operating profits when netting out its equity portfolio. Given its growth in premiums, I view a 10x multiple for its insurance business as a conservative valuation.

I would continue to be a buyer of CINF shares. Investors should recognize that if the stock market were to fall, CINF’s fair value would too, given much of its value comes from its equity holdings. But over time if you believe in a rising market, CINF is a strong investment as you get S&P 500-like exposure while also buying a solid insurance franchise at a discount valuation. This makes shares attractive in my view.

For further details see:

Cincinnati Financial: Equity Market Exposure And Improved Underwriting Create A Compelling Opportunity