CINF - Cincinnati Financial: Not Great RoR Yet But A Solid Upside Here

2023-08-09 06:20:03 ET

Summary

- Cincinnati Financial is a solid insurance company with potential for outperformance.

- The company is not heavily exposed to the challenging insurance market in California, making it an attractive play with little downside in terms of this market.

- CINF has a conservative valuation and offers a decent upside for investors, even at today's valuation, but requires moderation of expectations going forward.

Dear readers/followers,

I've covered Cincinnati Financial (CINF) twice before, both times with a "BUY" rating. While my position in the company is at a positive RoR, that positive RoR is barely better than the average market. While the company is a very good one, it has failed to "pop" beyond one instance before going back down again.

Seeking Alpha CINF (Seeking Alpha)

CINF is, as I see it, what you would characterize as "great business". That's why I own the company's common shares. At a good price, this company has not only the potential or possibility of outperformance, I believe it has a very real likelihood of such outperformance.

In this article, I will update my thesis on Cincinnati Financial after the recent bounce in valuation, and see why I still see a long-term upside for the company.

Cincinnati Financial - Its upside and fundamentals are still very solid

While not the most undervalued in its segment- not even close to it, as a matter of fact - the company still makes up for that with above-average quality. This doesn't just include the safety implied by its above-average credit rating of BBB+, even though insurance companies with this or above are getting rare. It's also things like market returns over the longer timeframe, which still are at good levels.

Now, property & Casualty insurance is getting a more tricky field - not just in the US, but everywhere. You might have heard that several companies including Allstate (ALL) are actually currently not writing new policies in California, at least insofar as home and car insurance goes. Geico seems to have also left the state behind for the time being, even going so far as closing down all California locations. Why is that?

Well, when an insurer in the P&C sector does this, it's because they can no longer get "the math" to work. In California, there are several reasons why it's unfavorable to be an insurance company, from Proposition 103 back in the 80s, requiring Insurance companies to get "prior approval" from the California Department of Insurance before implementing property and casualty insurance rates. In California, there is also a rather unique, politically elected commissioner who's tasked with overseeing the industry and potential rate increases. Needless to say, due to the political nature of the office, that person is not incentivized to work with these insurance companies or allow them to raise rates. These factors coupled with increasing wildfire severity have created a situation where many homeowners in California, including at least 1 acquaintance of mine, are no longer "insurable" on the P&C front.

It's not just the USA either. After the floods in Germany a few years back, there was open talk about not insuring the homes after they had been rebuilt - though part of the "positive" for insurance at the time (if it can be called such, given the human catastrophe), was that many homeowners had a massive protection gap against exact flooding and the like, due to a non-compulsory nature of hazard insurance, much in the same way that third-party liability insurance is for the driver of cars. In Germany, the discussion so far has stayed on the level of providing insurance for much higher premiums.

But in parts of the USA, specifically California, many people have found themselves "uninsurable". ( Source ) ( Source ) And even if they are insured, their premiums for things like natural hazards drive policy increases in the case of lapses, from $1800/year to upwards of $6000-$8000/year in a single 12-month period. (Source: California Insider)

So what's CINF's stance here?

For the time being, Cincinnati Financial still offers active coverage of Auto, Home, Excess/Surplus, and Life in California - though it states clearly that Excess & Surplus homeowner policies are available only in California and Florida. ( Source )

However, unlike some of the other examples mentioned, California is not a massive exposure to CINF in terms of total liability.

2Q23 results for the company are somewhat tricky YoY due to recognizing a $363 million second-quarter 2023 after-tax increase in the fair value of equity securities still held. It brought the net income to around $530M, compared to a net loss of $818M in the YoY period. We should instead view the company's results from a more long-term perspective, much like we do with Lincoln National (LNC) and other companies which have gone up and down in earnings. That is exactly what CINF has done, after all.

{kind=link}

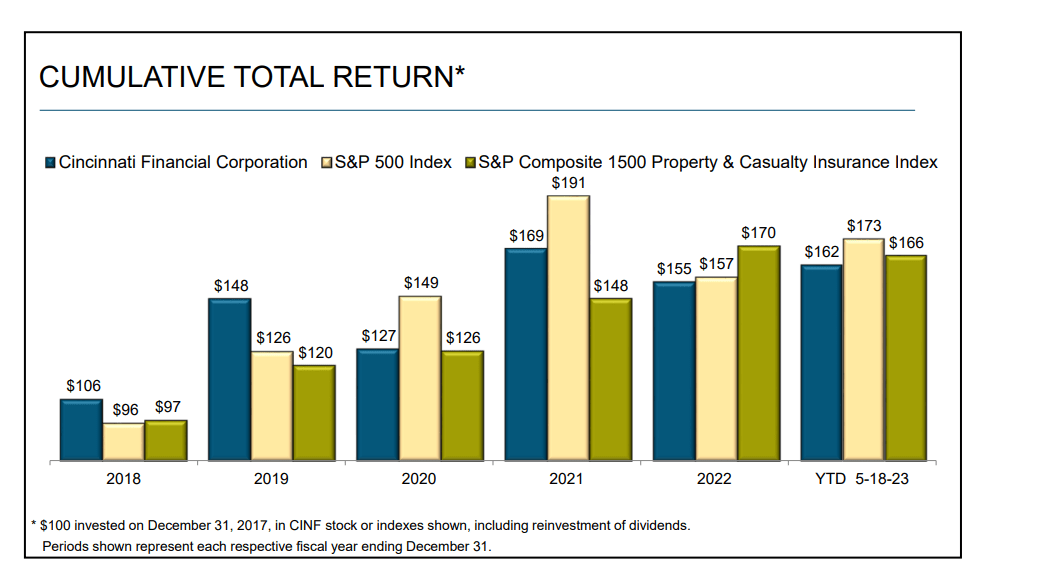

CINF compares to peers like LNC in a very favorable manner on several levels. The company has a 60+ year dividend history without a cut, for one, and it's an equity-heavy insurance company on the investment side, with over 42% of its investments held in stocks. The combination of local decision-making and expertise coupled with national scale is a very strong argument for this company and has seen the company usually outperform both the S&P500 and the relevant comp index.

{kind=link}

The company's value creation targets are positive, based on the performance drives of above-average premium growth (obviously not in areas like California), a solid combined ratio, investment contribution, and compounded overall portfolio return.

The company, not being heavy in life, has no material COVID-19 comorbidity or block impacts and hasn't had any material effects since 2020. What CINF saw was a slowdown in premium growth, but that was it for some time, with a $85M annual loss for 2020 that was pandemic-related. That means that CINF is one of the least-impacted insurance operations here.

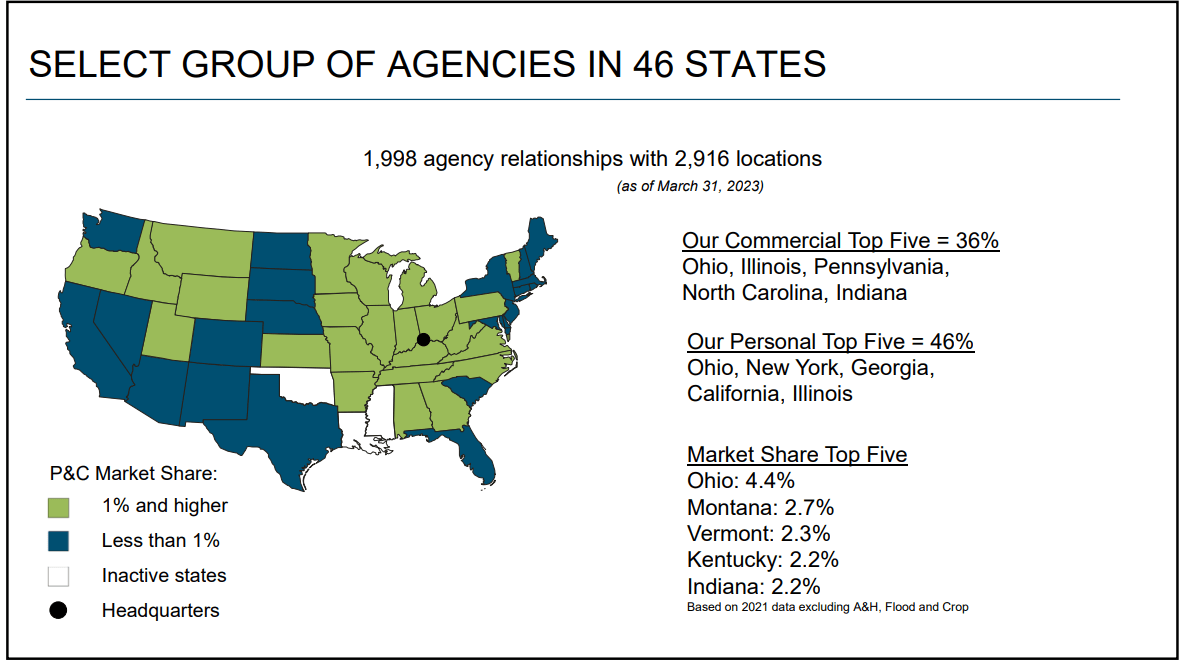

Due to the company's agency structure, CINF is also a bit better structured and diversified than many, and its lack of Cali exposure here is a net positive.

{kind=link}

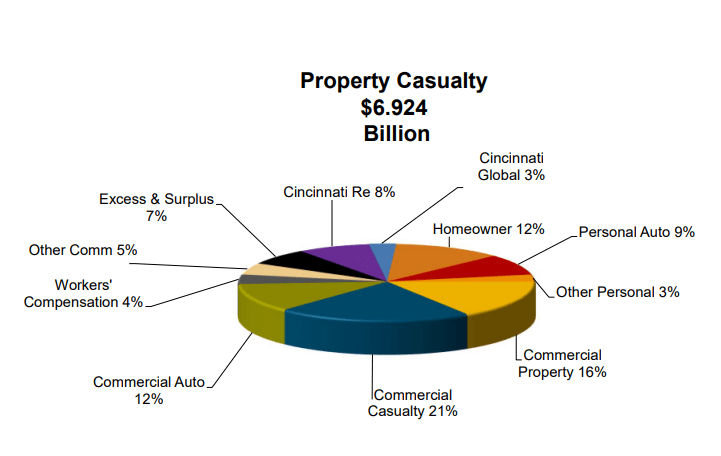

It also retains a very appealing business and risk mix, with only 23% personal lines, 56% commercial, and 4% life. Its Prop/Casualty size is at close to $7B, with the following mix.

{kind=link}

Even to begin with, the company's exposure to personal auto or personal property/homeowner is extremely small in relation to other exposures. It's one of the top-25 US P&C insurers, with over $7B in premiums with only 23% total personal, and a time-tested agency-centered model.

The problem I see is that the political part of society seems to be actively working against allowing insurance companies to work the numbers to make their business models work for them. In Oregon, an effort to map Wildfires was rejected simply out of fear of a premium spike. ( Source )

But what these politicians need to understand is that if you disallow predictive modeling or ways of working that insurance companies determine are needed, they will simply cease covering the area or refuse to accept new policies. That's what's happening now, and going by both anecdotal and the sentiment in media, it seems that the legislature is only taking this seriously for the past 1-3 months or so.

This leaves exposed Californians with little recourse except to move into state pools such as the California Fair Access to Insurance Requirements Plan. This provides basic fire insurance coverage for properties in high-risk areas when traditional insurance companies will not, and enrollments for this have jumped in recent years to 272,846 homes in 2022.

I also want to clarify that California is not the only area facing this exodus - there are trends pointing to similar developments in Louisiana, Florida and Colorado - but these states have very different regulations that allow some more leniency on the part of insurance company calculations and premiums.

All in all, CINF had a very good 2Q23. I would look at the longer-term rather than the quarterly trends for this company because massive income swings are a thing here due to losses from securities still held in the company's equity portfolio, which in this case runs through the net income calculation. It's a very challenging insurance market to be sure, but I view CINF as a prime navigation of this market.

What I would keep an eye on is the company's high-level mix. Current trends include the likelihood that CINF could become a major policy writer in these states - including California (Which CINF has already confirmed). However, CINF is doing this on what is known as an excess/surplus line basis. Without wanting to make this an "Insurance 101" class, Surplus line insurance is a special insurance that covers things that most companies won't insure - known in the vernacular as "E&S", and also includes things like construction, building, roofing, and commercial transport. This is how CINF now treats writing homeowners businesses in California.

Beyond that, I expect CINF to continue to outperform. It's an exciting business, and I'm happy to keep investing in it as they remain undervalued.

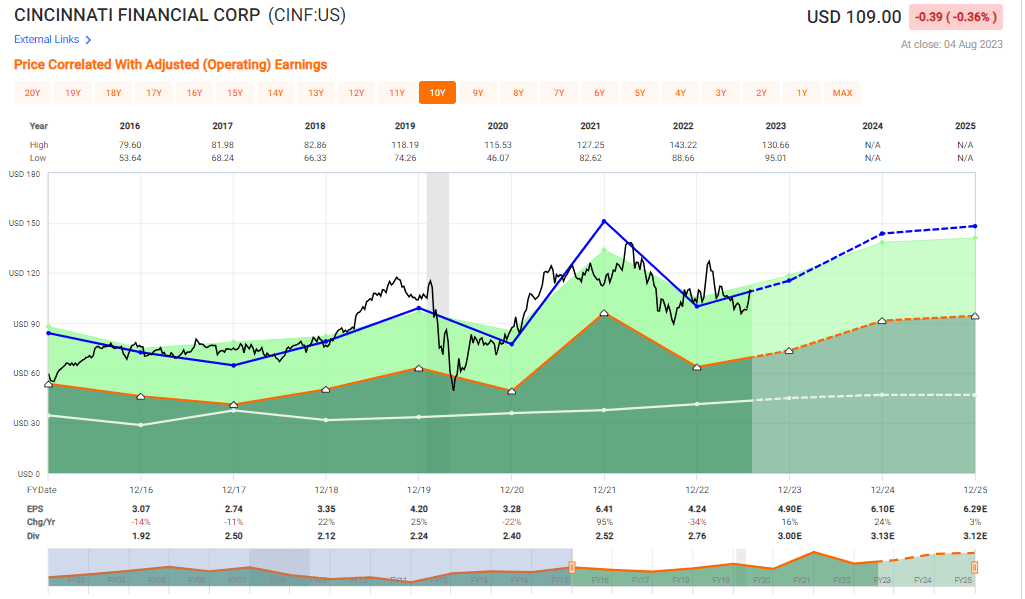

Cincinnati Financial valuation - A premium exists, but an upside exists as well

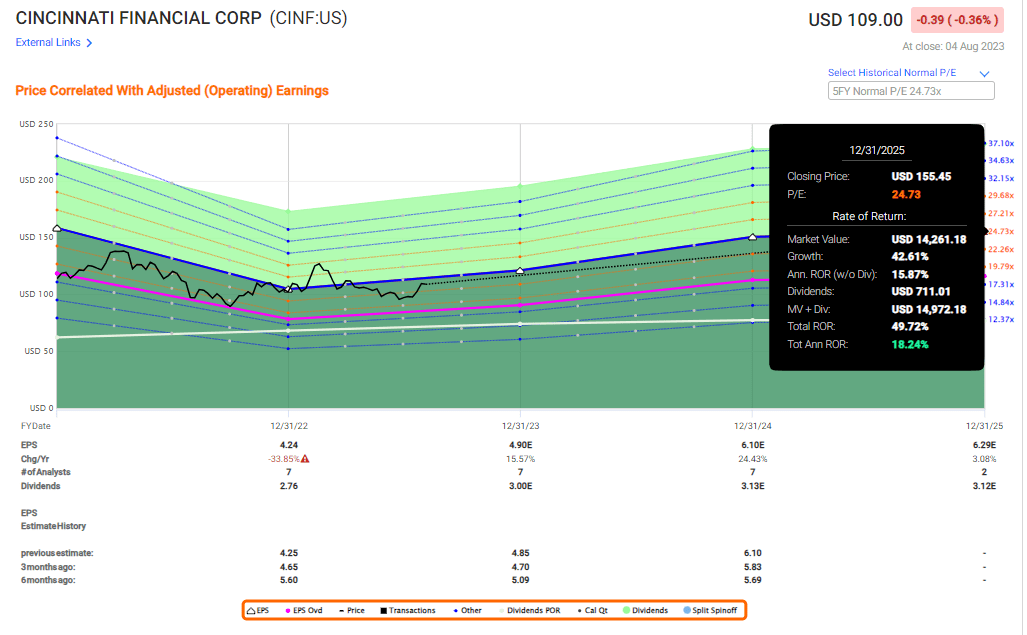

My previous target for CINF was a conservative $110/share. That means that as of the current PT of $109, the company is close to fairly valued. Very close in fact.

I considered for some time raising my overall PT here based on positive, double-digit EPS forecasts for both this and the next fiscal but decided in the end that the current macro and the likelihood of such materializations as well as basing this on almost a 2x P/E premium of other insurance companies was not feasible.

The company does have an impressive upside - on a 24x forward P/E, which is the 5-year average.

{kind=link}

Any significant negative miss here could derail that RoR, which is why the statistical 25% negative miss ratio on a 10-year basis with a 10% margin of error worries me somewhat (Source: FactSet). Based on this I'm neither raising PT nor changing targets. I'm also not overexposing CINF here, it's not "cheap". Not even close to it, as a matter of fact.

In line with my previous estimates, CINF is a "BUY" here, but barely one with a significant enough upside. I like their operations, but I'm also not fooling myself that they're the best and cheapest around - they are not.

Current analyst targets are higher than mine. S&P Global has 5 analysts following the company with averages starting at $115 and going up to $130/share with an average of $121. Based on this, every single analyst should be a "BUY" here, but only 1 out of 5 actually is, and the majority is at a "HOLD" rating.

I believe CINF still has upside left to give, and growth, so I don't change my rating - yet. But I am now being careful with this company, and give you the following update for my thesis.

Thesis for Cincinnati Financial's common shares

- This is a conservative, appealing insurance company and one of the market leaders in insurance in the USA. The company has some of the most qualitative portfolios and track records out there, being a dividend king with more than 60 years' worth of dividend increases under its belt.

- At the right valuation, this company becomes a "must-buy". Even at today's valuation, CINF has a decent overall upside to a conservative valuation based on average historical valuations.

- Based on this, I still consider CINF to be a "Buy" here and do not change my rating on the company. I give the company a current conservative share price target of $110/share.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them. ( italicized )

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

It remains a stretch to call CINF "Cheap", but it's definitely buyable here.

For further details see:

Cincinnati Financial: Not Great RoR Yet, But A Solid Upside Here