CTAS - Cintas: Is This Red-Hot Dividend Aristocrat A Buy?

2023-12-25 02:51:57 ET

Summary

- Most Dividend Aristocrats have been left in the dust in 2023.

- Cintas' revenue and diluted EPS climbed higher in its fiscal second quarter.

- The company maintains an A- credit rating from S&P on a stable outlook.

- Cintas' massive rally in 2023 appears to have overstretched the valuation.

- The stock could perform in line with the S&P 500 from the current valuation. But I don't see the risk/reward ratio as compelling right now.

Those familiar with my investing approach know that I prefer to build my portfolio around businesses that have long demonstrated a commitment to shareholders.

One of the most obvious signs of a company that values its shareholders is a reputation for consistent dividend growth. This is because achieving reliable dividend growth for decades on end is a feat that only the most battle-tested, shareholder-friendly businesses can achieve.

That is what makes Dividend Aristocrats such appealing investments in my opinion. No S&P 500 ( SP500 ) company just accidentally ends up raising its payout for at least 25 consecutive years. There must be both strong fundamentals to justify and sustain dividend growth for one. Not to mention that the desire to put shareholders first is also a prerequisite to making the cut as a Dividend Aristocrat.

{kind=link}

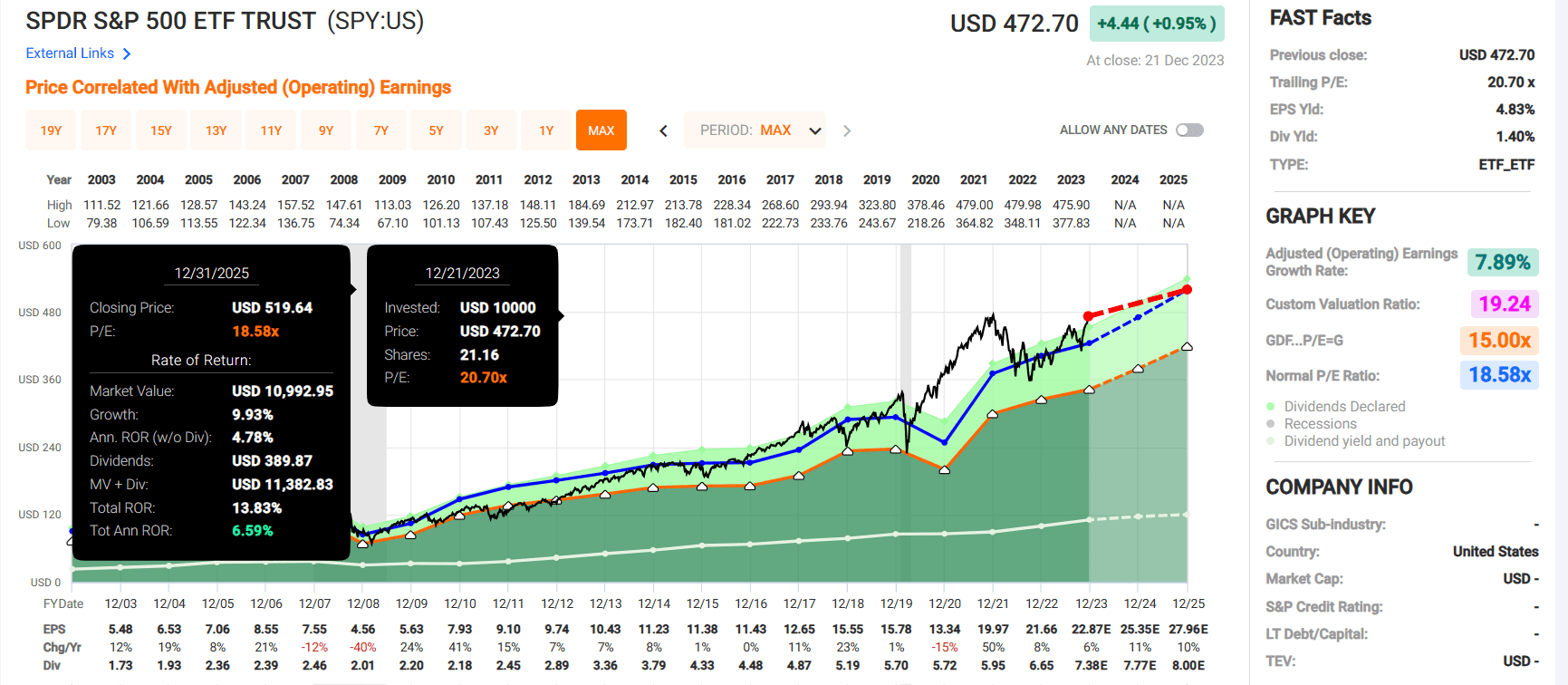

Value has been shunned in 2023. For proof of this argument, the ProShares S&P 500 Dividend Aristocrats ETF ( NOBL ) has gained just 5% year to date. That lags well behind the 24% gains of the S&P 500 index over that time.

Not all Dividend Aristocrats have fared poorly in 2023, however. The more growth-oriented Dividend Aristocrat, Cintas Corporation ( CTAS ), has rallied nearly 33% so far this year. But is it still a buy? Let's dig into the company's fundamentals and valuation to unpack this question.

{kind=link}

Relative to the 1.5% yield of the S&P 500, Cintas' 0.9% dividend yield isn't going to attract much attention from dividend-focused investors. As an investor with a likely longer investment timeframe than most, the company is appealing to me.

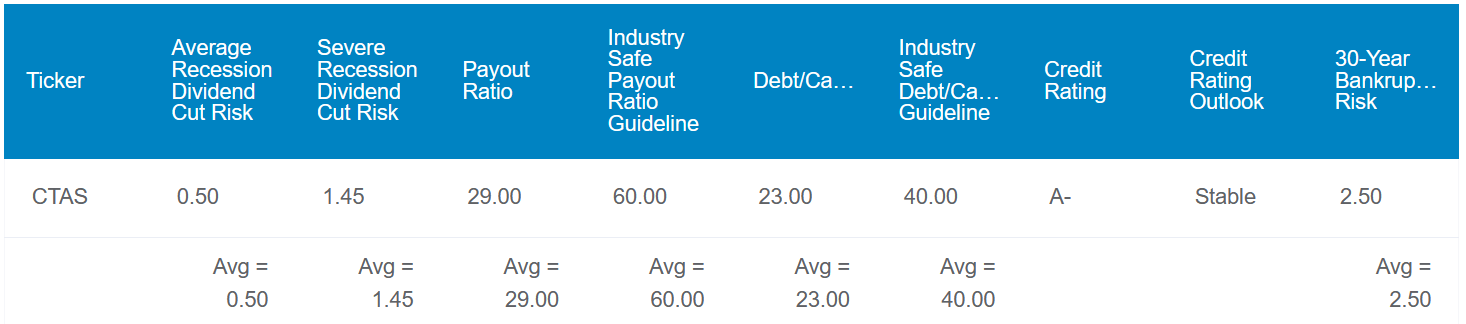

This is because Cintas' 29% EPS payout ratio is less than half of the industry-safe 60% EPS payout ratio put forth by rating agencies. This alone hints that there is plenty of room for the dividend to grow long-term, which I will expand on as the article progresses.

Financially speaking, Cintas is also an exceptional business. The company's 23% debt-to-capital ratio is far below the 40% that rating agencies consider safe for its industry.

Given these characteristics, it's not surprising to learn that S&P awards an A- credit rating to Cintas on a stable outlook. According to Dividend Kings, that suggests the 30-year probability of the company defaulting on its debt is just 2.5%.

This is why Dividend Kings pegs the risk of Cintas cutting its dividend in the next average recession at 0.5%. A severe recession would push this risk up to a still low 1.45%.

{kind=link}

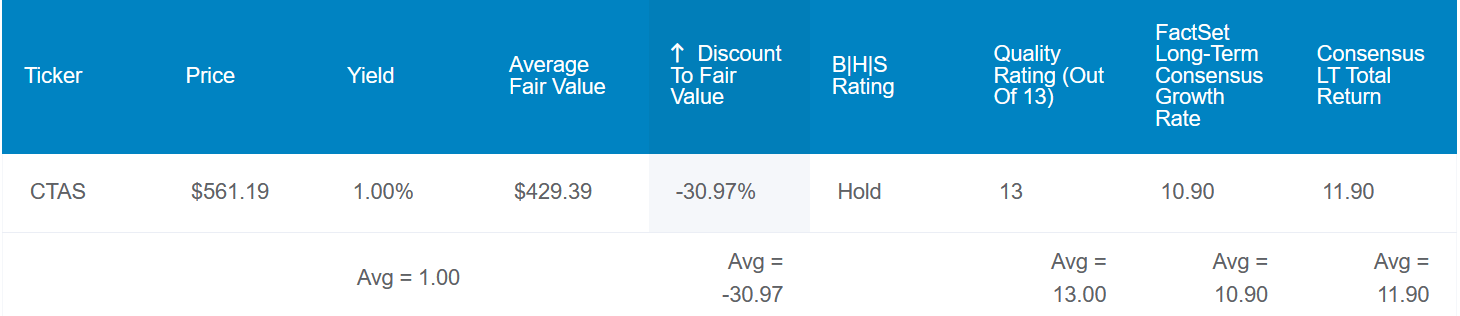

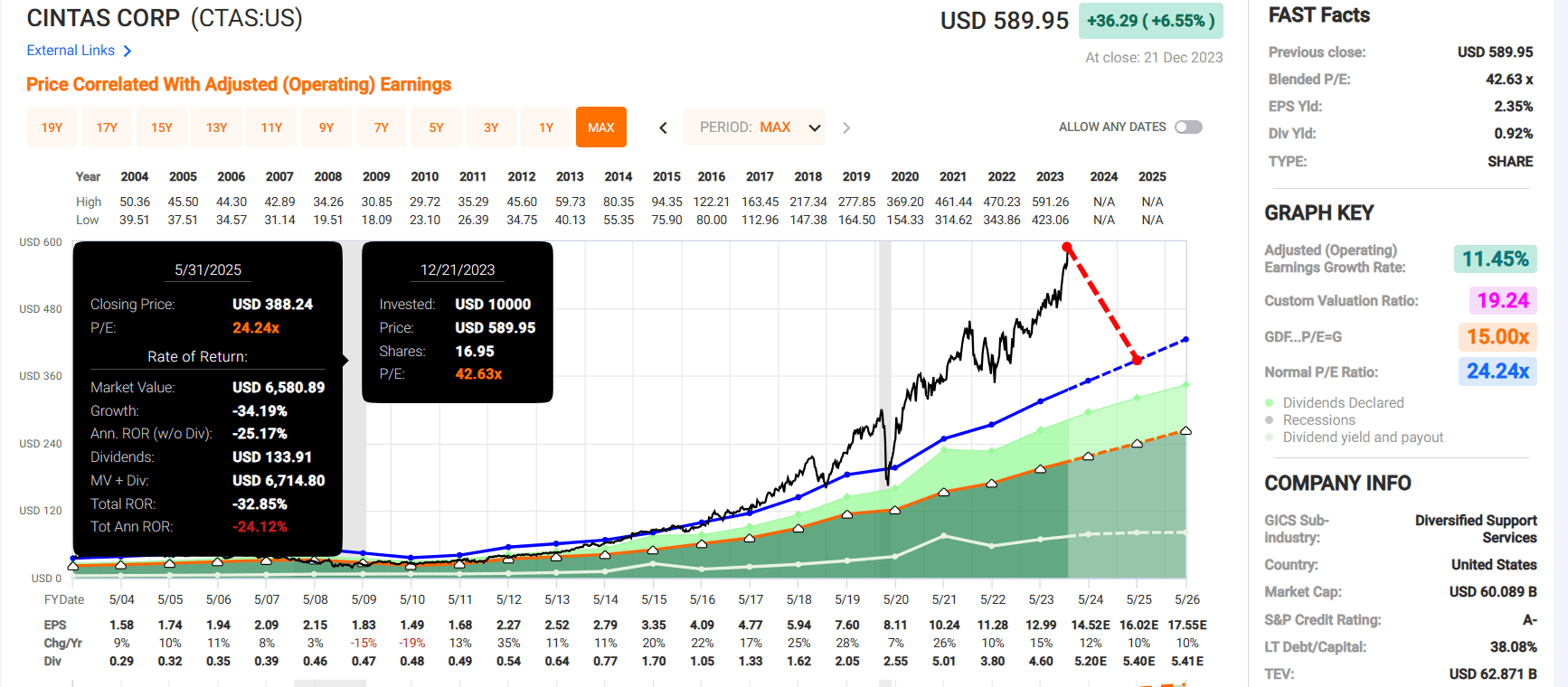

At the start of its rally this year, Cintas was much closer to its fair value than it is currently. Based on historical dividend yield and P/E ratio, Dividend Kings estimates shares of Cintas are worth $429 each. Stacked up against the current $591 share price (as of December 22, 2023), the industrial is 38% overvalued .

If Cintas meets growth expectations and returns to Dividend Kings' estimated fair value, here is the total return consensus through 2033:

- 0.9% yield + 10.9% FactSet Research annual earnings growth consensus - 3.1% annual valuation multiple contraction = 8.7% annual total return potential or a 130% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P 500 or a 128% 10-year cumulative total return

A Business Firing On All Cylinders

Cintas Fact Sheet

Through 11,000 routes across the U.S. Canada, and Latin America, Cintas serves over 1 million customers. At a glance, Cintas is one of those businesses that may not seem exciting. After all, it sells uniforms, mops, mats, first aid products, and safety training to businesses, including healthcare and hospitality. This isn't exactly a high-tech business model.

The benefit is that it is very easy to understand for one. The need for the services and products that Cintas provides explains how it has grown sales and adjusted EPS in 51 out of the last 53 years.

Despite its notable success, the company also appears to have room for growth: Cintas estimates that there are still 15 million businesses in North America that it hasn't yet reached.

{kind=link}

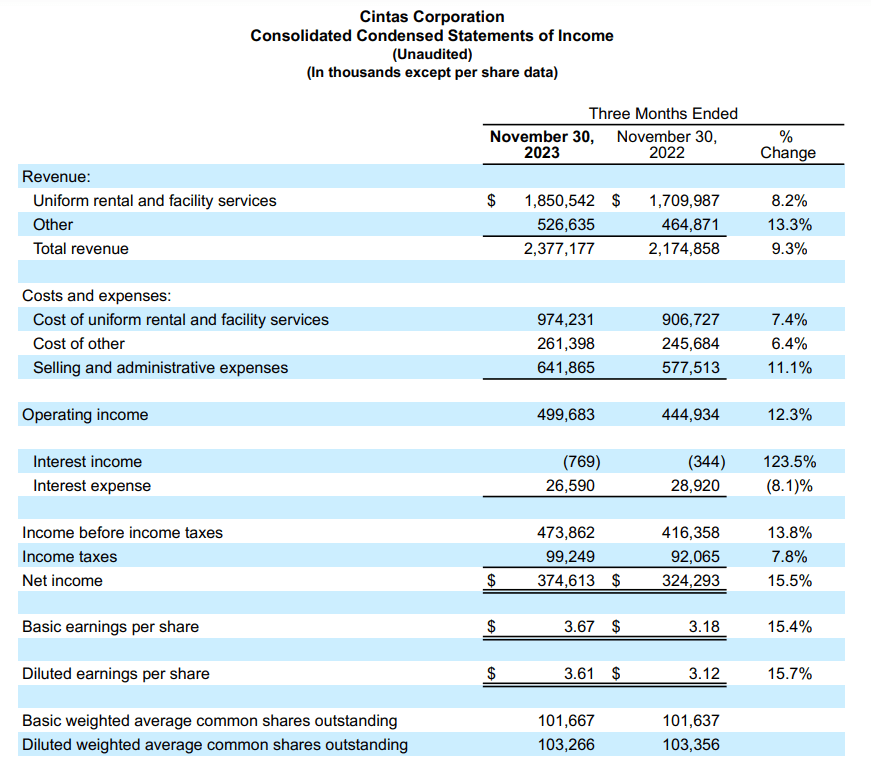

Cintas' recent results for the second quarter ended November 30 serve as confirmation of its incredible growth potential. The company's $2.4 billion in revenue during the quarter grew by 9.3% year-over-year, topping the analyst consensus by $40 million .

Leveraging its trusted name, Cintas' results were powered by across-the-board organic growth. According to CFO Mike Hansen's opening remarks in the Q2 2024 earnings call , fire protection services organic revenue growth of 17.8% led the way in the second quarter. Not far behind, first aid and safety services organic revenue rose by 12.7%. Uniform rental and facilities services notched 7.9% organic revenue growth and uniform direct sales were also up 4.7% for the quarter.

Cintas posted $3.61 in diluted EPS during the quarter, which was 15.7% higher than the year-ago period. This beat the analyst consensus by $0.13. The greater revenue base combined with an 85 basis point expansion in its net profit margin to 15.8% were the two factors that contributed to this vigorous diluted EPS growth.

Through the first six months of 2023, Cintas' interest coverage ratio was 20. This is indicative of a financially sound business.

The Dividend Growth Potential Is Sizable

Cintas switched from an annual dividend to a quarterly dividend in 2021. Adjusting for this fact, the company's dividends paid soared by 143.9% from $2.05 in the calendar year 2018 to $5 in the calendar year 2023. Significant dividend growth should also persist moving forward.

Cintas' 10-Q filing for the second quarter won't be released for approximately another two weeks. But in the first quarter of its current fiscal year, the company generated $230.2 million in free cash flow. Compared to the $117.6 million in dividends paid during this time, that is a free cash flow payout ratio of just 51.1% (page 7 of Cintas' Q1 2023 10-Q filing ).

Risks To Consider

Cintas is a 13/13 ultra SWAN per Dividend Kings' quality rating, but it faces risks like any other business.

Unlike many businesses, recessions don't tend to cause Cintas' growth to invert from positive to negative. However, recessions usually do temporarily weigh on the company's growth prospects.

Operating in a competitive industry, Cintas must stay on top of its game to attract and retain customers. If the company can't properly execute, it would risk losing market share to other competitors.

Another risk to Cintas is the potential for a breach of its computer systems. In such a case, customer information could be compromised and the company's operations could be disrupted. If this were to occur, it could result in damage to the investment thesis through litigation and an altered view of Cintas' widely respected brand.

Summary: A World-Class Business I Want To Own When The Price Is Right

{kind=link}

{kind=link}

Cintas is a company that I would love to eventually own within my dividend growth stock portfolio. However, that comes with the caveat that it must be trading at least somewhat close to fair value before I would consider opening a position.

As it stands now, Cintas' 42.6 blended P/E ratio is materially above its normal P/E ratio of 24.2 per FAST Graphs. Factoring in a reversion to its normal P/E ratio, the stock could shed a third of its value through May 2025. Long-term, returns could still slightly exceed the S&P with this gross overvaluation. However, this immediate downside risk doesn't justify a buy rating from my perspective. That is why I am initiating coverage in Cintas with a hold rating for now.

For further details see:

Cintas: Is This Red-Hot Dividend Aristocrat A Buy?