CTAS - Cintas: Paying Up For Quality Has Its Limits

2023-10-08 21:24:32 ET

Summary

- Cintas has outperformed the market many times over the last decade.

- Dissecting the performance into dividends, earnings multiple, earnings growth, and share count shows a clear trend.

- Cintas is unlikely to continue its outperformance after most levers have been pulled.

- At its current price, the stock looks to be unattractive.

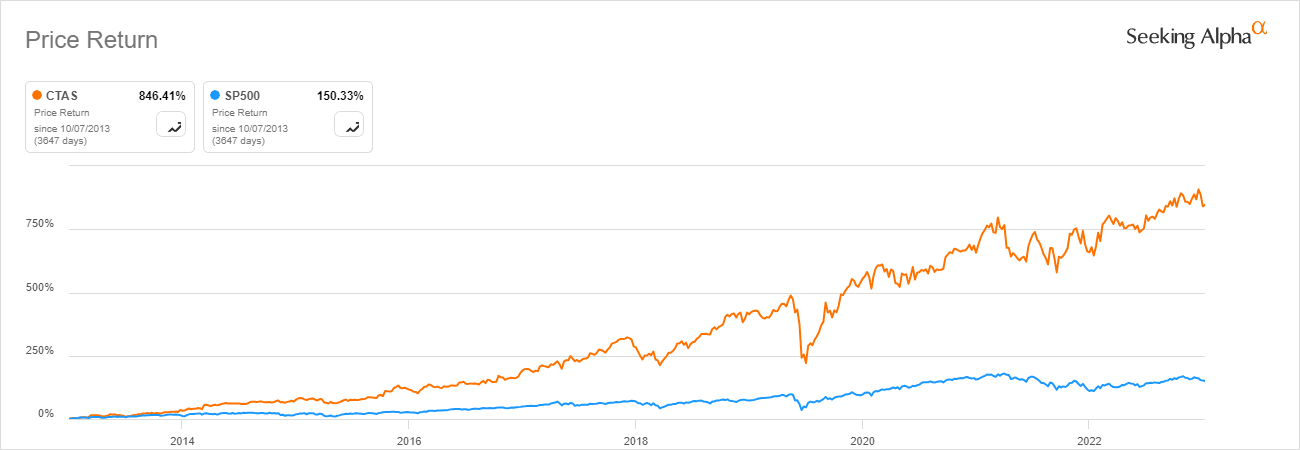

Cintas Corporation (CTAS) has massively outperformed the S&P 500 over the last decade. Let's see how they managed to do that and if it is likely to continue similarly.

Cintas long-term outperformance (Seeking Alpha)

{kind=link}

What are returns made of?

First, let's ask ourselves what returns in the stock market are made of. There are two main variables: Stock price appreciation and dividends. We can then further segment stock price into an earnings multiple, earnings growth, and the number of shares outstanding. Let's review all four parts.

Dividend

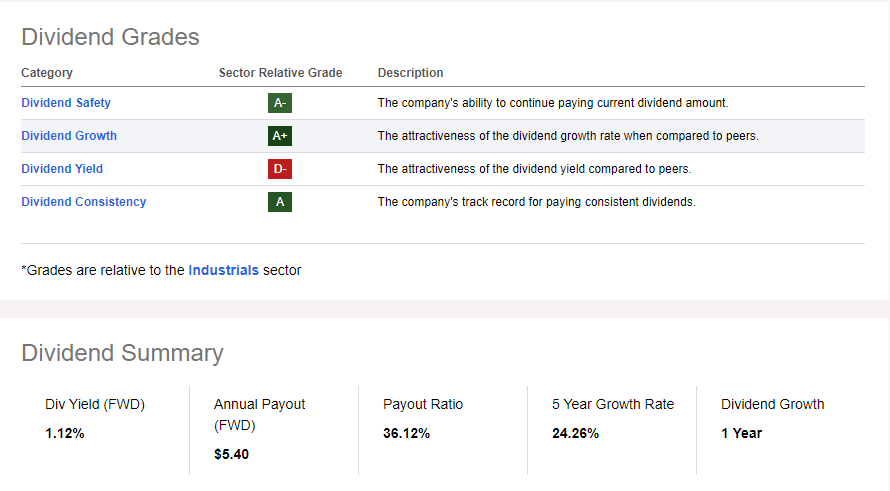

Cintas has excellent dividend grades on Seeking Alpha , except for yield. Cintas has a safe dividend with under 50% of earnings and most importantly, cash flows paid out as dividends. Over the past three, five, and ten years, the dividend grew by at least 22%. It is an awe-inspiring growth rate, but analysts expect a sharp deceleration to just 11% dividend growth next year. As growth expectations slow down, more on that later, investors should expect the dividend growth to decelerate meaningfully as well from the 22% CAGR. Over the last decade, $2.29 billion was paid out in dividends.

Cintas Dividend Scorecard (Seeking Alpha)

{kind=link}

Earnings multiples

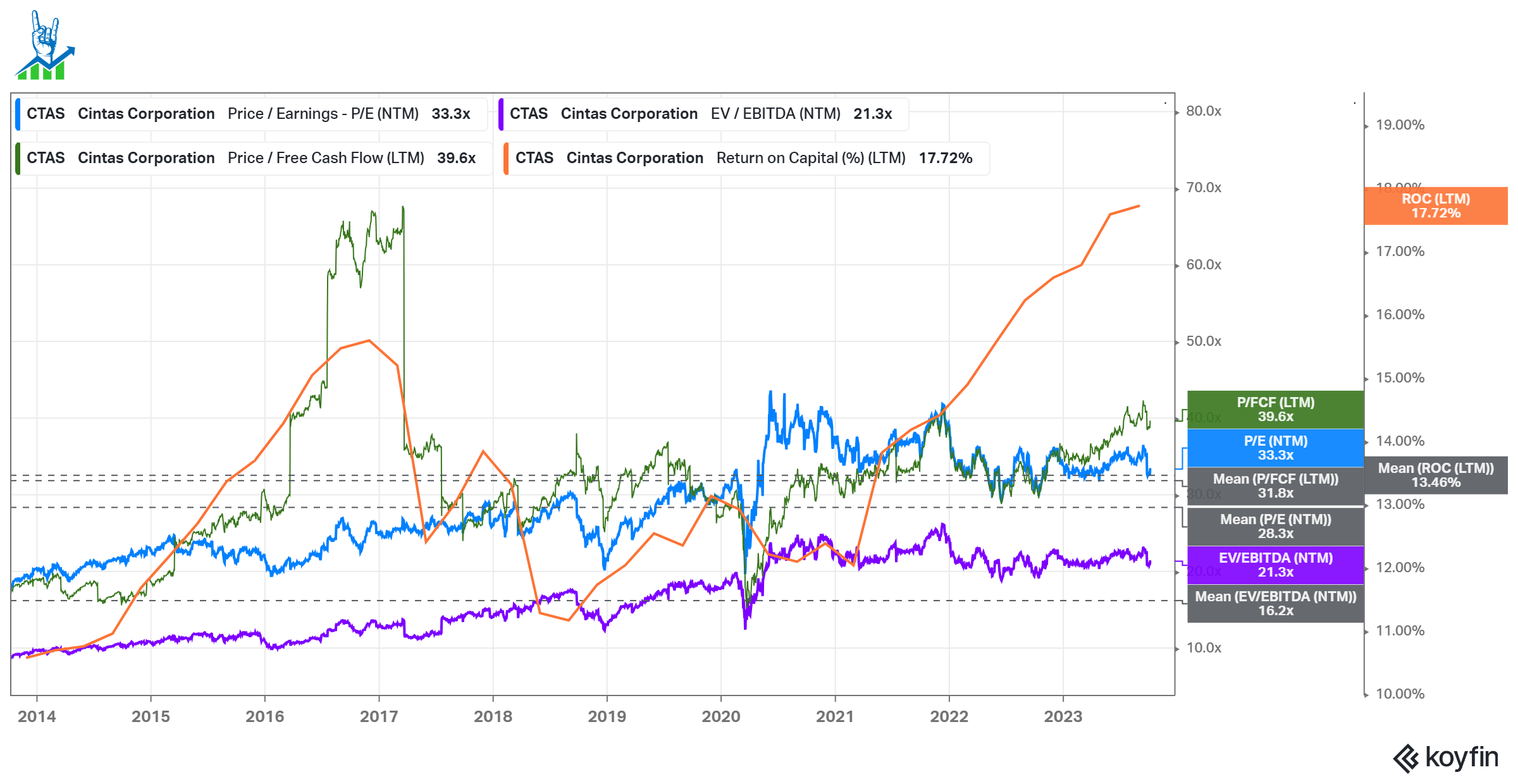

The chart below shows the development of three earnings multiples and the return on capital. We can see that all trend higher over time and that Cintas currently trades significantly over its mean earnings multiples over the last decade. This has led to a massive tailwind for investors, as each dollar of earnings translated into more share price growth. While the multiple expansion is somewhat justifiable by the improved returns on capital, we should not expect this expansion to continue. We should be prepared for multiples to revert to the mean. Cintas trades at elevated multiples, which can change quickly if the market loses interest.

Cintas Multiple expansion (Koyfin)

{kind=link}

Earnings Growth

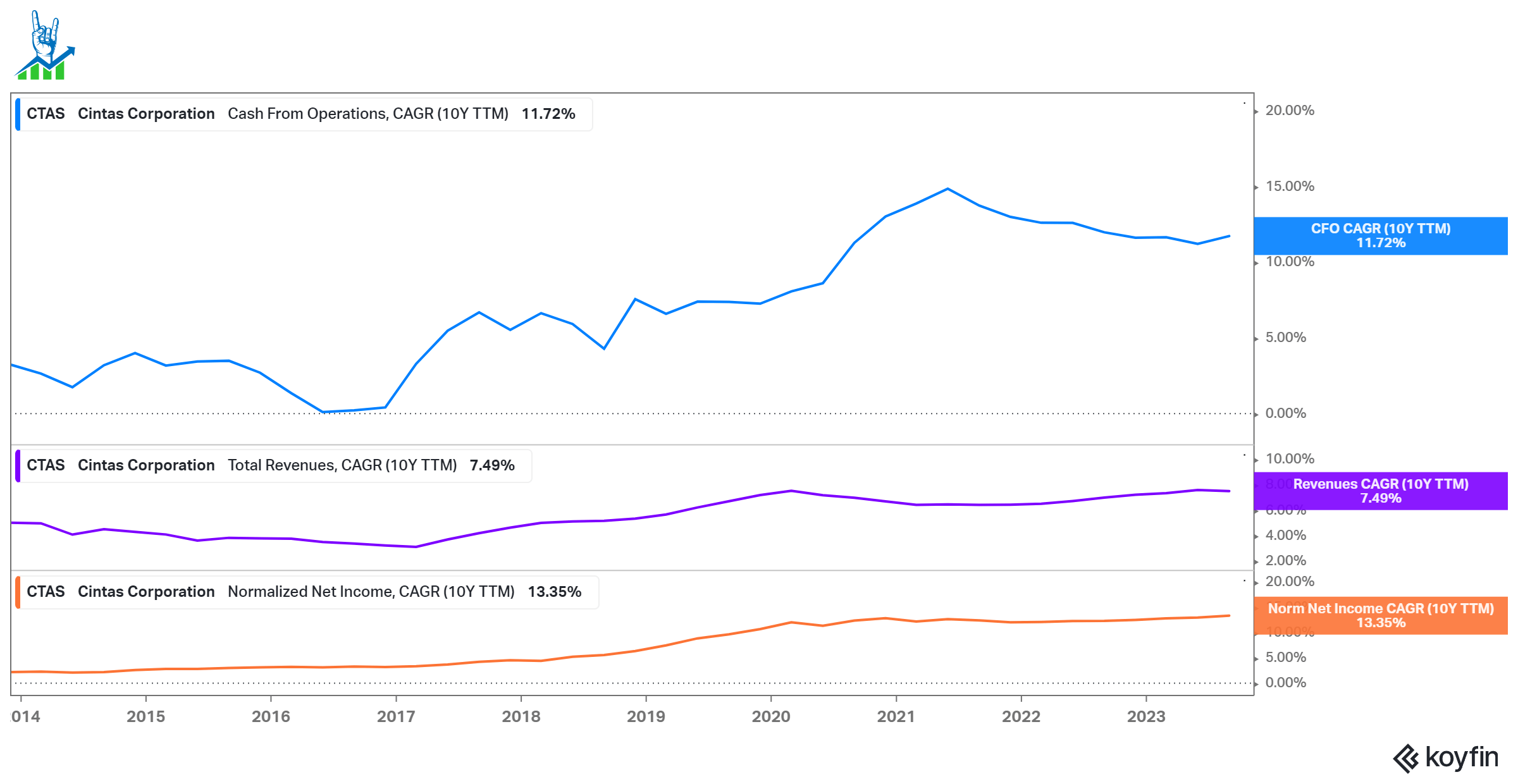

Over the last decade, earnings grew by 13%, cash flows by 11% and revenues by 7%. The outperformance of cash flows versus revenues has come from EBIT margins increasing from 13% to 20.7%, while gross profit margins increased from 41% to 47%. SG&A margin has remained pretty stable and only decreased slightly. This type of lever won't be repeatable over the next decade. EBIT margins would need to increase to around 33% to get a similar result. Over the last decade, Cintas spent $2.63 billion on acquisitions compared to $2.33 billion in cumulative capital expenditures. Cintas guides organic revenue growth to stay between mid to high single digits, so there is no acceleration compared to the last decade. Incremental margin improvements should elevate EPS (which we can use as a proxy for cash flows as well) into the double digits.

Cintas earnings growth (Koyfin)

{kind=link}

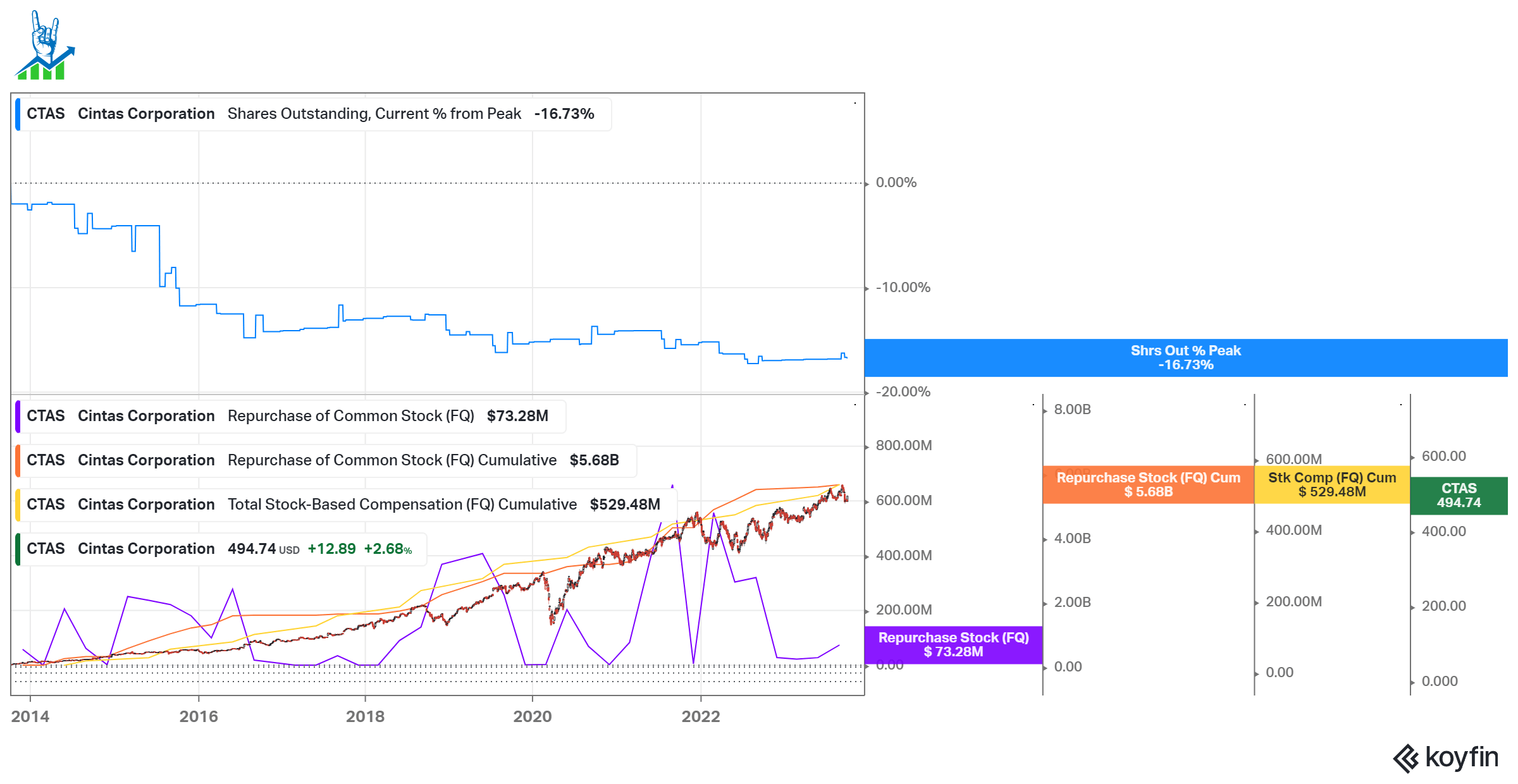

Shares outstanding

Shares outstanding declined by 16.7% over the last decade, a positive development for shareholders. Cintas continuously bought back shares for $5.68 billion while diluting shareholders by $529 million via stock-based compensation. 16.7% of shares outstanding at today's prices would cost $8.4 billion, so the buybacks created tremendous value for shareholders. Especially as valuation multiples climbed, the early repurchased shares created value. Over the same period, Cintas generated $7.69 billion in free cash flows, paid out $2.29 billion in dividends, and spent $2.63 billion on M&A. Buybacks and dividends represent pretty much the entirety of the free cash flows, so the M&A was financed by debt. At 1.1 times net debt to EBITDA and 17 times interest expense coverage, Cintas has a good balance sheet and is not excessively levered. In the future, buybacks will have less effect as the company trades at higher multiples. The mean buyback yield of 2.75% over the last decade is higher than the current FCF yield of 2.4%. Investors should expect buybacks to create less value in the future. We can also see that in the shares outstanding chart: Most of the share reduction was in the early years when Cintas traded at lower multiples.

Cintas shares outstanding (Koyfin)

{kind=link}

Q1 Earnings

In late September Cintas reported its Q1 for fiscal 2024. Revenues saw an increase of 8.1% with organic revenue growth at the same 8.1%. Gross profits increased 11%, partially due to lower gasoline, natural gas, and electricity costs. Operating income increased 13.7%, driving margins from 20.3% to 21.4%. Operating cash flow increased 12.7%, while Free cash flow only increased 1%, driven by a $36 million increase in capital expenditures in the quarter.

The quarterly dividend was raised by 17.8%, a deceleration from the 22% CAGR over the recent past, but still very rapidly. Full-year guidance was slightly raised, the company now expects $9.4 to $9.52 billion in sales (6.5-7.9% growth) and $14 to $14.45 earnings per share (7.7% to 11.2% growth). This would be a deceleration from the past 10-year growth history. While these results are still strong, every metric is decelerating compared to the 10-year history.

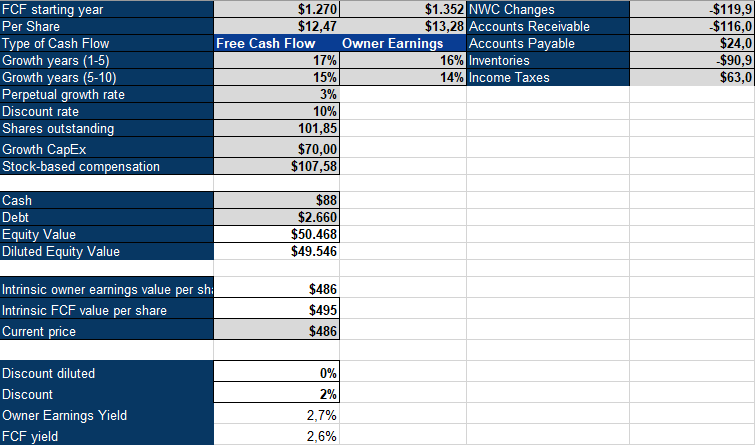

A high Valuation

I will also use an inverse DCF model to value Cintas because cash flow is my preferred metric to look at and what drives long-term value. I adjust FCF with growth capex, stock-based compensation, and net working capital changes.

Cintas Inverse DCF Model (Author's Model)

{kind=link}

To arrive at $70 million growth capex, I subtract D&A costs ($296 million) from capex ($367 million). Using these numbers, we arrive at a required cash flow growth rate of 16% for the next five years, followed by five years of 14% growth. This is below the historical growth rates of operating cash flows, revenues, and net income. Throughout this article, we saw a pattern: Cintas looks great in the rear mirror, but the future looks less rosy. Multiples are expanded and at risk of shrinking; earnings growth is more challenging after margins have already increased a bunch and buybacks have less effect at higher multiples. For these reasons, I will put a hold rating on Cintas. It is a great company but does not look like a compelling investment. Of course, the company can prove me wrong and outgrow my expectations, but I wouldn't say I like the odds.

For further details see:

Cintas: Paying Up For Quality Has Its Limits