CTAS - Cintas: Plenty To Like Except The Valuation

2023-06-06 18:06:39 ET

Summary

- I have consistently viewed Cintas as overvalued and uninvestable for the past three years, despite recognizing its premium status in the market segment.

- I believe better investments have been made during this time of overvaluation both by me and by others, highlighting the company's current lackluster appeal.

- The latest results and thesis do not justify a change in my stance, and I maintain a "HOLD" rating on the company.

Dear readers/followers,

I've been reviewing Cintas ( CTAS ) for years at this point, but my stance has very rarely been positive. The company is, simply put, expensive for what it offers investors in context to the greater market and the undervaluations out there. There is no doubt to me that Cintas is one of the best companies out there in the segment, and you'll never find me arguing with you that Cintas deserves some sort of premium. Because it does.

However, the degree of premium is what is in question here, and which has made Cintas uninvestable in my eyes, for near-on 3 years at this point excepting the crash in COVID-19. Cintas has never really normalized again, and maybe it won't. That's fine, but it also means I don't really get to invest in Cintas because I don't invest in overvalued companies.

So, here's the performance of the company since my last article.

Seeking Alpha Cintas (Seeking Alpha)

While you could technically argue outperformance here, I'll say it's a close thing here - and I've made better investments since that time.

Let's see if the latest results and the thesis justifies any sort of change here, or why I am still somewhat negative on this company - or at least at a "HOLD".

Updating on Cintas - a lot to like, but valuation isn't one of those things

Cintas is one of the best-quality companies in the entire business services industry, a massive sector with hundreds of relevant businesses to compare it to. The qualifying fact here with which I justify this, is profitability and fundamentals. Very few businesses compare to this company when it comes to this.

Looking at operating margins, net margins, returns on assets, equity, invested capital, and capital employed, this company is a "monster", between the 86th to 95th percentile in the entire sector. Profitability over a 10-year period is unbroken, making it better than 99,9% of all companies here (Source: GuruFocus, Morningstar). The company is a good example of why you should invest in quality businesses, and never let them go unless they become excessively overvalued.

And let me be clear - while I do consider the company overvalued, I do not consider it excessively so. To put it simply, if I had a $100k Cintas position, which I do not, I probably would not sell it - at least not yet. I would hold it and let it "ride".

Recent results confirm the quality of the company. Revenue increased by double digits for the 3Q22 fiscal, coming up above $2B. The company even managed an increase in gross margins of 15.1%, with an even better increase in operating income of almost 21%.

The positives in this quarter speak for themselves. Strong volume growth from new customers and existing customers resulted in this increase - in short, Cintas is still recording increasing demand and also successfully increasing prices, despite much of the COVID-19 environment no longer being around.

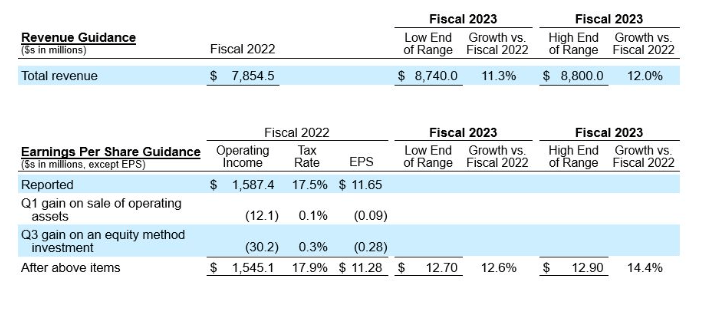

This quarter also included a raising of the guidance , now expecting upwards of $8.8B for the 2023E year, with a diluted EPS range as high as $12.9/share.

{kind=link}

The company has more than a million customers across both the US and Canada, servicing customers in both service sectors and goods sectors at a split of around 70/30. Organic revenue growth that you would not necessarily expect out of a company like this is nonetheless part of this company's M.O., with 11,000 distributing products and services in routes. The company has a superb track record of growing adjusted EPS for more than 51 years out of the last 53 and has increased its annual dividend since before I was born, in 1983.

CTAS IR (CTAS IR)

Cintas as a company is a very impressive operation. It takes annual revenues that are currently over $8B forecasted, or $7.9B for the last complete fiscal, with around 80% of revenues coming from the uniform rental and facility services, and manages COGS of less than 55%, one of the lowest I've seen in the segment, with a very streamlined 26% OpEx. $15.7 out of every $100 of revenue is turned into net income - and that's extremely impressive.

{kind=link}

The company also managed the COVID-19 period with aplomb. Supply chain disruptions for Cintas were surprisingly minimal, and Cintas did increase its inventory of various supplies, such as PPE, in accordance with demands. It's unfair to say that Cintas has many NA-based peers - at least in one way. While competition does exist, the way that these services work is that most of Cintas direct peers are minimal and regional in comparative size. Cintas competes with national, regional, and local providers, and it goes without saying that the smaller the company, the less likely the competition is to be able to deliver any significant economies of scale, impacting the margins it can get, as well as the prices it needs to charge to make a profit.

The only issue or two issues with Cintas is its valuation, which we'll look at closer in a bit, as well as the dividend yield - because that dividend yield at this time is less than 1%.

The company is A-rated, has a market cap that's closing in on $50B, and an otherwise quality and profitability that's impressive, based on current operating, net margins and return metrics. Despite macro pressures and inflation, the company has held up its ROIC well in the face of increasing WACC.

Cintas Profitability (GuruFocus)

{kind=link}

Its net income share of revenue as a percentage has held steady. The only two fundamental criticisms I can levy at this business is its increasing use of debt in relation to its cash over the past 10 years, and the fact that it increasingly lowered the share of SE, or stockholder equity as a percentage of total assets. None of these indicate anything fundamental by themselves, and with the otherwise positive picture of the business, I call this "good", and nothing you really need to worry about.

It would be wrong to say that I am the only investor that's growing cautious though, or that other investors aren't selling off their shares. Ray Dalio is a recent investor who sold his entire CTAS stake back in March/April of 2023. Insiders for this company are doing only one thing over the past 3 years - and that's selling their shares, not buying new ones.

So while this company is a great business, it also comes with a high price premium - and some market participants, including myself, are wondering if this company is really worth over 37x P/E. That's where we start our foray into CTAS valuation for June of 2023.

Cintas Valuation for 2023 - It's looking worse

CTAS Valuation (F.A.S.T graphs)

{kind=link}

As you can see above, Cintas isn't exactly cheap or easy to argue for here. From very good valuations over 6-10 years ago, we're now in what I would consider a very excessive sort of place. Cintas is valued at over 37.5x to P/E which is a valuation I would only consider valid for something like LVMH ( LVMUY ), which provides products and services loved and not provided by anyone else. Not a company that essentially rents out uniforms and cleans various spaces, because this is a commoditized service. Anyone with a mop and a bucket and other supplies can do what Cintas does - granted, not even close to the same quality, scale, or specifics that the company does, but nothing of what the company does is unique, except the scale or way in which it does it.

This makes evaluating hard. It's easy to continually say that "Oh, it's too expensive", but it might also be that we won't really see a massive decline coming here at any time in the near future.

However, even at the high premiums that Cintas wants for its business, what we have here is expensive. The 5-year average is 31x P/E. On a 31x forward P/E with an 11-12% growth rate, which seems likely given recent results, your annualized RoR comes to less than 2.5%.

F.A.S:T graphs CTAS upside (F.A.S.T graphs)

{kind=link}

Not exactly impressive, that. Even at 37x P/E, you're barely at double digits for this company, and then you're allowing the company to trade at multiples it, at least in my view, has absolutely no business trading at. The implied share price for a 2025E 37.5x P/E is currently almost $600/share.

That's not something I can get on board with.

Cintas does have competition like I said. At least, it has company we can compare it to, including Rollins ( ROL ), Tetra Tech ( TTEK ), Stericycle ( SRCL ), Casella ( CWST ), Brink's ( BCO ), though none really does what CTAS does as well as CTAS does it. Despite this, overvaluation is not uncommon in this segment - Casella is at over 60x P/E, though with Brink at below 15x, the variance here is absolutely massive. The only thing that can be said is that quality companies in business services, based on broad averages, can command a premium of 30x P/E.

CTAS is nowhere near that though. A 30x P/E would imply something close to a $380/share price, which is over $100/share less than we currently have. My previous PT for the company was somewhat unclear, so let me clarify it further here. I would go ahead and pay $350/share for Cintas - I might go as high as $380/share, but I would consider a 28-29x P/E to be safer in the long run.

So $350/share is the currently highest I would pay - though I can't really say that I see a downward catalyst in the near term for the company to reach this level.

Current analyst averages remain very high and exuberant. $384 is the lowest analyst target, with $550/share being the highest. The average is almost $500/share. However, despite this, only 6 analysts are at a "BUY" here, and we have an increasing number of analysts going to "underperform" or "SELL" here.

For that reason, and the valuation-related reasoning I gave you, I am remaining at "HOLD" for this company after the recent quarter under the following thesis.

Thesis

My current thesis for Cintas is:

- The company is fundamentally an excellent services company with a high premium - and is better bought, as proven by history, at cheap valuations.

- With cheap prices and fear, this company can easily generate triple-digit returns, even if the dividend is comparatively low.

- At current valuations, even a forward premium of 30X+ results in potential market underperformance, or a bare-bone upside close to the market. This is a no-go in terms of what you "should" invest in at this particular time.

- Given current trends, I consider Cintas a "HOLD". It's not as dangerous to invest in as a few months back at peak valuations, but it's nowhere near where I'd want to buy the business. I would also say that if you hold Cintas, it is time to consider rotating.

- I give Cintas a PT of $350/share as of June 2023.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

It's a great company but lacks cheapness and a realistic upside to an attractive fair valuation. For that, I give this a "HOLD".

For further details see:

Cintas: Plenty To Like, Except The Valuation