CTAS - Cintas: Sound Business Model But Grossly Overvalued

2023-07-26 07:31:55 ET

Summary

- Cintas is a leading provider of products and services like uniforms, floor mats, bathroom supplies, and compliance training, catering to over one million businesses across various industries.

- Cintas' market position, impressive diversification efforts, and strong corporate culture have served the company well over the years.

- However, I believe that the stock is currently overvalued, and assign it to a "Hold" rating.

Investment Thesis

Cintas Corporation (CTAS) is the market leader in its industry and addresses a large total addressable market. The company has scaled remarkably, and its impressive diversification efforts and strong corporate culture give the business added resilience and a competitive advantage.

Although I like Cintas as a company, its stock is grossly overvalued. Using Seeking Alpha's valuation metrics and a discounted cash flow analysis, I believe that Cintas is overvalued at $507, and for that reason, I assign a "Hold" to the stock.

Company Overview

Cintas Corporation is a leading provider of a variety of products and services, including uniforms, floor mats, bathroom supplies, first aid and fire safety products, and compliance training.

The company caters to a diverse clientele of over one million businesses across various industries. Their customers range from small manufacturing companies to mid-sized hotel chains and even major corporations.

Cintas provides rental apparel programs, which include professional laundering, inspection, and delivery services. Additionally, they offer replenishment of essential cleaning supplies, hand sanitizer, as well as hygiene and paper products for restrooms. The company also supplies entrance mats, reusable microfiber products, disinfectants, and sanitizers. Lastly, they offer restocking services for first aid and safety supplies, along with testing and inspection of fire protection equipment.

The company's primary business segment is its Uniform Rental and Facility Services, which account for 80% of revenue. Its key costs are the cost of goods sold and selling and administrative expenses.

Market Leader in a Large Total Addressable Market

Cintas holds a dominant position as the market leader in a substantial total addressable market ((TAM)) valued at $39 billion, as reported by Robert W. Baird & Co. This significant TAM presents a multitude of opportunities for Cintas as it continues to grow and strengthen its market leadership.

Moreover, Cintas maintains a remarkable market share of 14%, surpassing its competitors Aramark and Unifirst, which hold 7% and 5% of the market, respectively. This clear market leadership provides Cintas with a competitive edge and allows the company to set industry standards and influence market trends.

As the rental of uniforms is a scale business, Cintas is able to drive superior margins compared to its competitors. Using TTM figures, Cintas enjoyed an operating margin of ~20% while Aramark and Unifirst only had margins of ~3.8% and ~6.13% respectively.

The company's strategic advantage lies in its greater route density and market position, which enable it to leverage its fixed costs and maximize capacity utilization.

Young Hamilton Blog

In the infographic above, we can see a general correlation between route density and margins and can expect the company's margins to grow alongside route density. Hence, I believe that Cintas has much room for growth, and is well-positioned to capitalize on the large uniform rental market.

Impressive Diversification Efforts

Cintas has strong resilience to both demand and supply side shocks due to the company's strong ecosystem of partners, and clever diversification. Since its inception, the company has formed strategic partnerships with the likes of brands such as Carhartt, JW Marriott , and more.

Cintas' exclusive partnership with Carhartt, one of the most renowned workwear brands globally, provides the company with a significant competitive advantage and contributes to building a wide moat around its business.

{kind=link}

Additionally, Cintas' management has shown commendable diversification efforts, benefiting both the demand and supply aspects of the business. With 42 million units sourced from 3000 suppliers across 21 countries annually, the company maintains a robust and diversified supply chain which will help it weather unfavorable macroeconomic conditions.

Furthermore, Cintas has well-diversified end markets, with 70% in the services sector and 30% in manufacturing. More importantly, no single industry contributes more than 10% of the company's revenue.

These strategic moves enhance the company's resilience to macroeconomic fluctuations, as Cintas avoids sole reliance on any specific market or industry. This diversification fosters stability and reduces vulnerability to adverse economic conditions, positioning Cintas for sustained success.

{kind=link}

Strong Corporate Culture

Cintas follows a profit-sharing business model where each facility functions as a separate profit center, and employees are regarded as "partners." Their dedication is rewarded through a generous profit-sharing program and company ownership, fostering a strong sense of ownership and motivation.

{kind=link}

This profit-sharing agreement is also extended to the company's drivers, which are more than mere drop-off service providers. These drivers play a crucial role in nurturing relationships with local clients and engaging in cross-selling efforts as they are compensated based on revenue generated on their route.

Cintas' practice of incentivizing employees creates a robust corporate culture focused on customer satisfaction and continuous improvement. This culture, in turn, fuels the company's top-line growth, giving Cintas a significant and difficult-to-replicate advantage over its competitors.

Valuation

I believe that the stock is currently overvalued, and will analyze its valuation using industry valuation metrics and a discounted cash flow analysis.

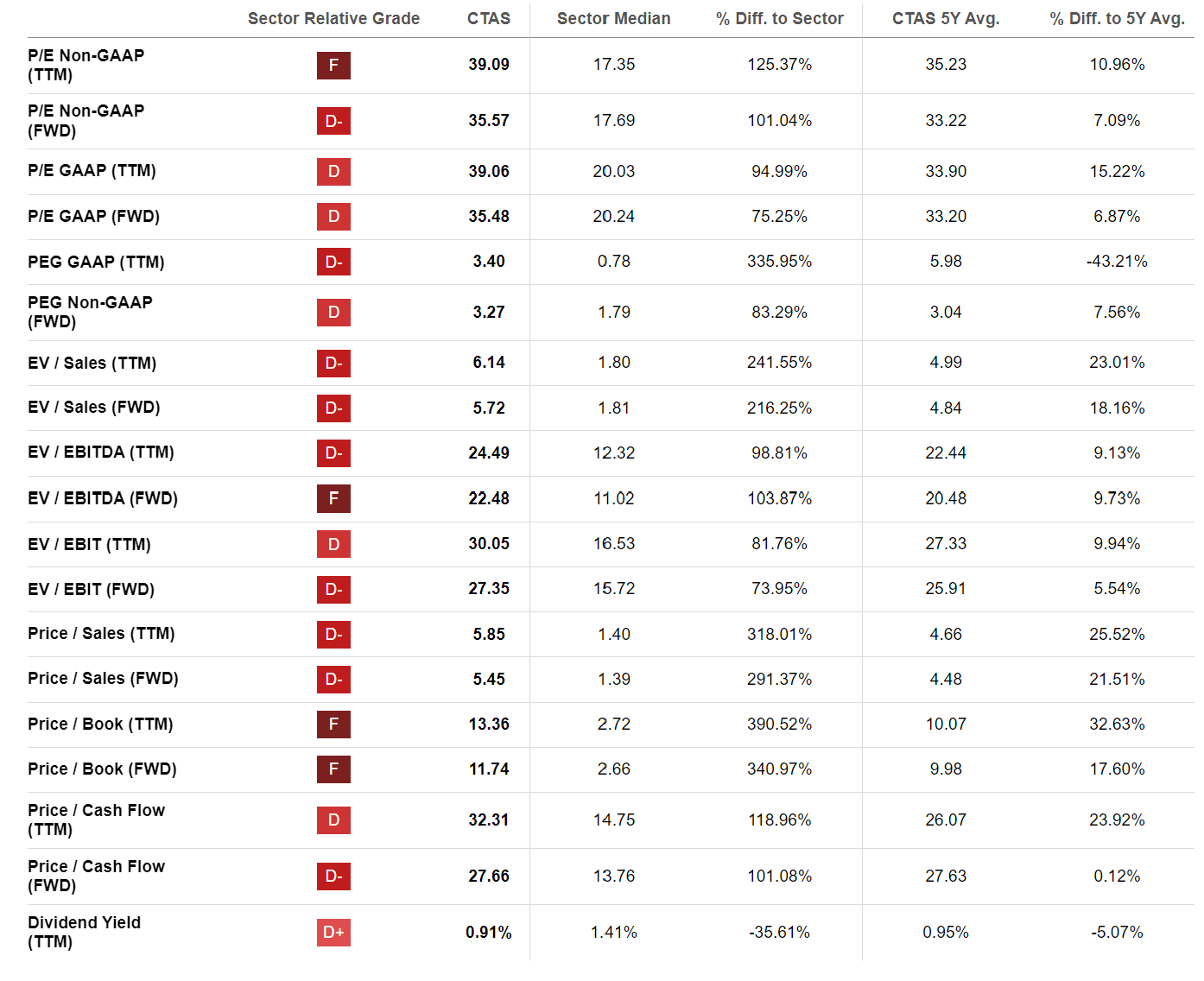

Valuation Metrics

{kind=link}

Using Seeking Alpha's valuation metrics, we can see that the company performs poorly in every metric, and is overvalued in comparison to its peers. For the reason above, I would not enter a position in Cintas at its current valuation.

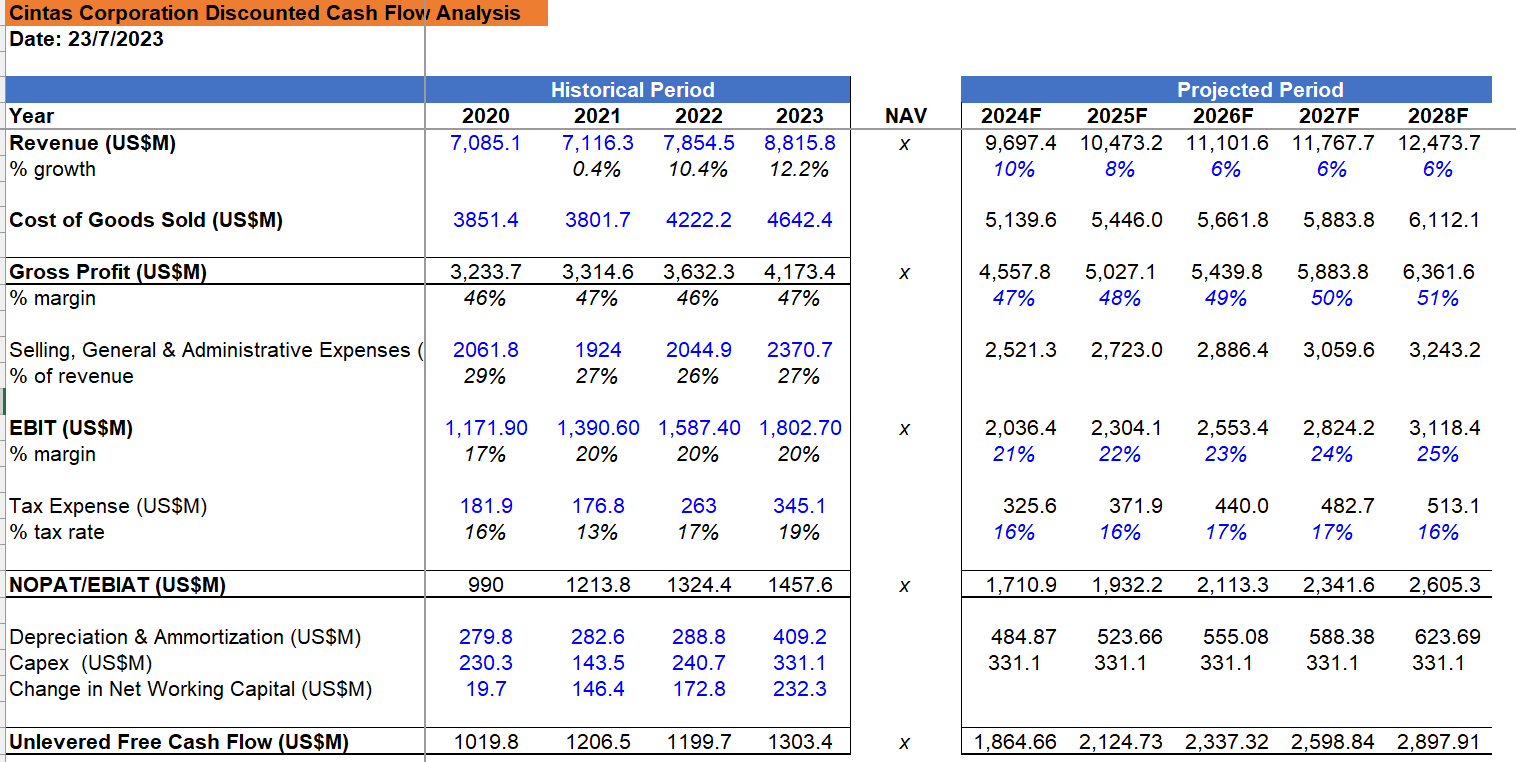

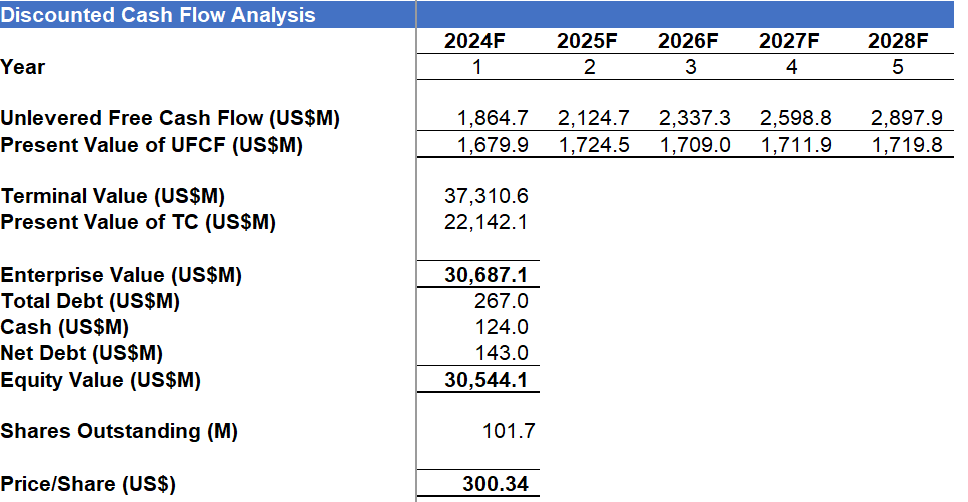

Discounted Cash Flow Analysis

Next, I perform a discounted cash flow valuation to determine the company's intrinsic value. I use a weighted average cost of capital of 11% and a terminal growth rate of 3%. I also assume that there is no change in shares outstanding.

{kind=link}

I taper revenue growth assumptions by 2% in 2024 to be in line with management guidance and also because the strong growth in 2023 can be attributed to easing COVID restrictions and improving business sentiments.

I also expect the business to slightly improve gross profit and operating margins in the following years.

{kind=link}

Using these assumptions, I arrive at a Price/Share of $300, which suggests that the company is currently overvalued at its current price of $507.

Risks

Cintas operates in a cyclical industry and could be susceptible to macroeconomic conditions. Unfavorable economic conditions and high unemployment rates would result in weaker demand for uniforms and ancillary services, affecting Cintas' core business segments.

Current customers might also take longer to pay, leading to higher account receivables days and hence a longer working capital cycle.

Investor Takeaways

Before initiating a position in Cintas, I would like to see the stock reach a fairer valuation and for the company to be able to scale other business segments, such as its uniform direct sales segment and first aid, safety, and fire protection segment.

Although I like Cintas as a business due to its unique market position, diversification efforts, and its strong corporate culture, I believe the stock is currently overvalued and hence assign it a "Hold" rating.

For further details see:

Cintas: Sound Business Model But Grossly Overvalued