CCAP - CION Investment: This BDC Looks Like A Future Superstar But Is It Too Soon To Tell?

2024-01-04 17:00:00 ET

Summary

- CION Investment Corporation is a newcomer in the BDC sector and has the potential to be a future superstar.

- The company has been defensively positioning its portfolio, with a focus on first-lien investments and a strong Q3 performance.

- CION has been decreasing its net-debt-to-EBITDA and has strong dividend coverage, but faces risks from a potential recession and declining Nll due to expected rate cuts.

- Due to their smaller market cap and shorter track record as a publicly traded BDC, I think CION is a hold.

- Because of their shorter track record, I think the market still has questions about CION, and this could be the reason the BDC trades at more than a 41% discount to its NAV.

Introduction

With 2023 in the books and the sector ( BIZD ) performing well due to higher interest rates, many may be wondering what 2024 will bring. With interest rates expected to be below 3% this year , many may be wondering how BDCs will fare. In my opinion, prices will likely fall due to some investors rotating out of the sector with the anticipation that their net & total investment income will fall. I do think some may experience lower income, but BDCs have been strengthening their portfolios over the years, and thanks to the banking crisis in March 2023, I think they are in great positions moving forward.

With tighter lending standards from banks, the sector stands to benefit as some will likely take market share for the foreseeable future. I think the sector will only become more popular, making BDCs not only attractive investments because of the extra income from their predominantly floating rate portfolios, but great long-term investments as well. One fairly newcomer is CION Investment Corporation ( CION ). In this article, I discuss why I think this BDC has the potential to be a future superstar in the sector.

Who Is CION Investment Corp?

Having debuted publicly in late 2021, the BDC has a short track record. But the company was actually a non-traded BDC from 2012 until IPO. Like their peers, CION loans to middle-market companies with an EBITDA of $25 to $75 million. At the end of Q3 their portfolio companies had a median EBITDA of $33.7 million.

They prefer to invest in media, healthcare, pharmaceuticals, and business & consumer services to name a few. They also differ slightly as they invest in the chemicals, plastics, and rubber industries. This accounted for 4.8% of their total portfolio at the end of Q3.

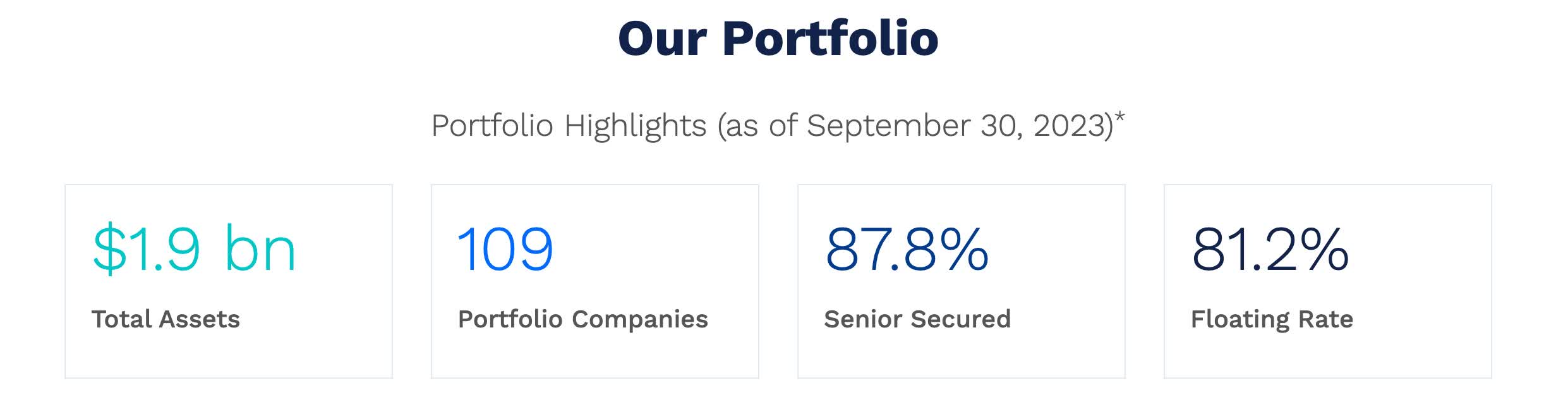

The company has a total of 109 companies for a total value of $1.9 billion. And 87.8% of their investments are in senior secured loans with 81.2% of their debt investments being floating rate. The company is defensively positioned for economic downturns with their focus on first-lien investments which is something I like to see from BDCs.

{kind=link}

These account for nearly 86% of their portfolio. This is in comparison to two of my favorites, and more popular peers in the sector, Ares Capital ( ARCC ) & Capital Southwest ( CSWC ). Both have a first-lien focus of 43% & 84.4% respectively. Furthermore, CION has more than 11% in equity investments.

Since going public, the BDC has been impressively growing, focusing on strong relationships and core partnerships. Over the last 6 years, CION has been focusing on further strengthening its portfolio with over 84% of their investments in senior secured, first-lien loans.

Strong Q3

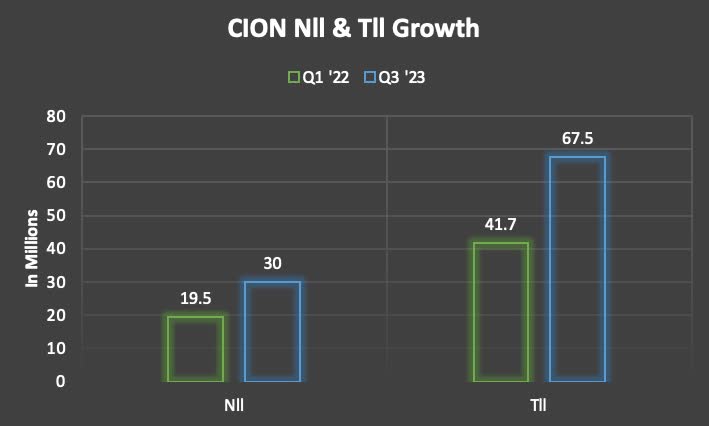

During their Q3 earnings back in November, CION continued this focus with $97 million in 3 new investments and 11 existing portfolio companies. Furthermore, their net and total investment incomes were both driven higher by their strong quarter. Nll of $30 million, or $0.55 a share increased more than 28% from Q2's $23.4 million. Tll also increased by double-digits from $58.5 million in the prior quarter to $67.5 million.

Since Q1 2022, both net investment income & total investment income grew nearly 54% and 62% respectively. Their strong quarter also led to NAV growth of $0.49 to $15.80. Part of this was owed to the BDC out-earning its dividend of $0.34.

{kind=link}

Creating Value For Shareholders

Another reason the BDC saw a huge increase in its NAV was the accretive share repurchases it conducted during the quarter. In Q3 CION repurchased more than 168,000 shares at an average price of $10.71. This is accretive since the company trades at a significant discount to its NAV.

With the BDC being fairly new, I suspect the market is not quite sure what to make of CION, but they seem to be doing all the right things. NAV growth, out-earning the dividend, and buying back shares. Since August 2022, management has repurchased more than 2.5 million shares, totaling $24.1 million. And have stated that they plan to continue taking advantage of the discount. This will likely drive NAV & earnings growth for the foreseeable future, two metrics I like to see from my BDC holdings.

Healthy Balance Sheet

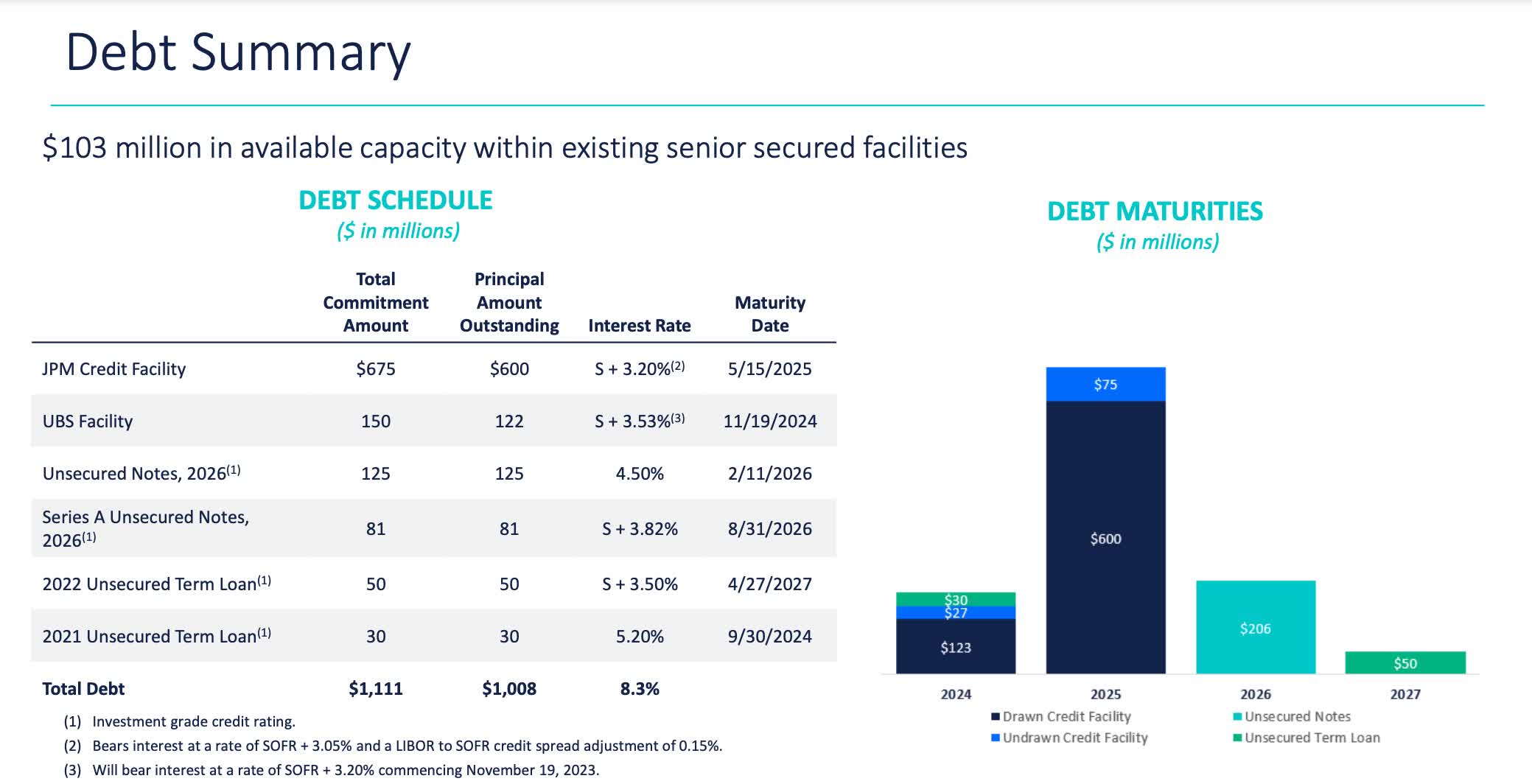

CION has also been doing a good job decreasing its net-debt-to-EBITDA over the past 12 months. Quarter-over-quarter they managed to decrease this from 1.04x to 1.03x. Although, this did increase from 0.99x year-over-year. Additionally, the BDC's debt maturities are also well-laddered with most of their debt maturing in 2025.

{kind=link}

However, they do have some debt maturing in November this year that they will likely have to refinance at a higher rate. And although cash did decrease from $162 million in Q1 to $120 million in the latest quarter, CION has ample liquidity available with an additional $100 million under the credit facilities. Their dry powder still remains strong, allowing management to pursue new investments in growth and working capital needs for their portfolio companies going forward.

Strong Dividend Coverage

CION has impressively covered its dividend, which played a huge part in the company's NAV growth. For being an externally-managed BDC, CION has rewarded its shareholders handsomely during the high interest rate environment. Unlike ARCC, who prefers to be more conservative, CION has declared a few specials & supplementals.

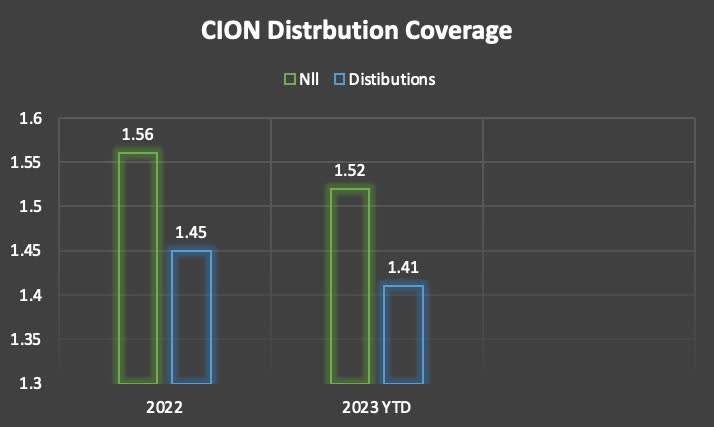

Speaking of specials, the BDC recently announced a $0.15 end-of-year special, payable at the end of January. This is on top of the $0.05 supplemental the BDC declared for Q4. Analysts estimate Q4 net investment income to be $0.42, which would put total Nll for the fiscal year at $1.94. I expect the net investment income to be in a range of $0.45 to $0.50 for the BDC giving them a total Nll of $1.97 - $2.02. Even if this comes in on the lower end, this would give CION a distribution coverage of 1.01x. That's assuming another $0.34 regular dividend for Q4.

{kind=link}

Risk Factors

CION Investment has done a good job at keeping their non-accrual percentage manageable during the high interest rate environment. Furthermore, they managed to decrease this from Q2 of 2022 when non-accruals accounted for 1.5% & 3.6% of their total investment portfolio.

At the end of their latest quarter, non-accruals fell to 1.03% of fair value due to restructuring. This is in comparison to Crescent Capital BDC, Inc.'s ( CCAP ) 2.3% & 1.8% of their total portfolio value at the end of their Q3. This was also down from 1.69% in the previous quarter but still remains slightly lower than the BDC average of 1.2% of fair value. This speaks volumes to management, especially as market conditions have caused slower growth of portfolio companies.

But with a mild recession expected, CION could see this number increase again as portfolio companies face financial pressure from a slowed economy. Another huge risk for BDCs is a rise in PIK income. This could also place downward pressure on the company's financials going forward.

Another risk that could affect CION in the coming months is their distribution coverage. With their predominantly floating rate portfolio and three rate cuts expected, the coverage ratio could suffer as Nll retracts from here. This is something investors should keep an eye on in the coming quarters.

As previously mentioned, I expect CION to cover the recently announced special along with the supplemental & regular dividend in Q4, but coverage will likely become tighter if rates fall as expected.

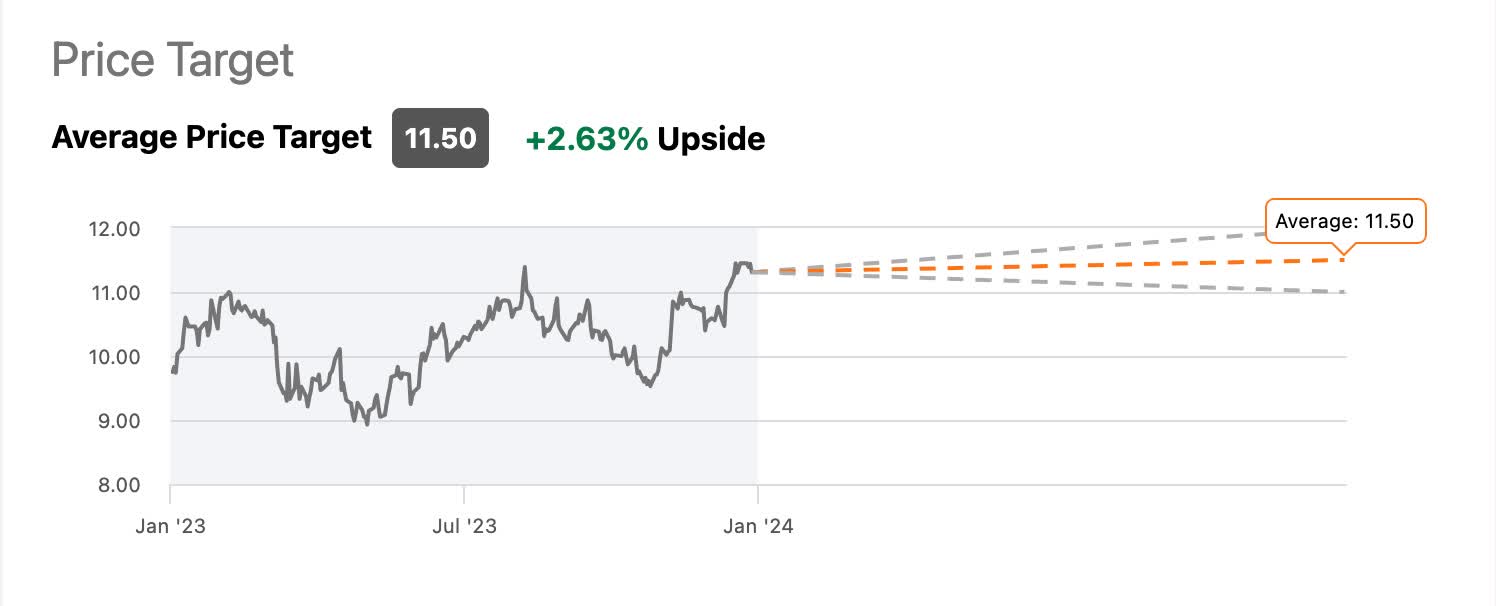

Undervalued

At the time of writing, CION trades significantly lower than its NAV price of $15.80 at $11.15. That's more than a 41% discount currently. But with the BDC being fairly new, the market may be still waiting to see more from the company having only been public for roughly 2 years.

If you believe in the long-term outlook of the company, then CION is trading at a great valuation. If you're like me, you would like to see more from the company because of their short track record. Furthermore, CION offers barely any upside to its price target, so investors get no margin of safety here. If you're looking to add, I would wait for a pullback in price, likely in the coming months when interest rates fall.

{kind=link}

Bottom Line

CION Investment Corporation is an up-and-coming BDC that has all the makings of a future superstar in the sector. Despite the challenging economic backdrop, the company has done fairly well, focusing on first-lien investments and keeping their non-accruals manageable. Additionally, their balance sheet remains sturdy with most of their debt maturing in 2025, when rates will likely be much lower. They also have a decent amount of cash on hand and available liquidity, which is important if the economy does fall into a recession.

But with rates expected to fall significantly in 2024, the company is at risk of declining Nll, which could affect the dividend going forward. However, the BDC has been repurchasing a substantial number of shares, which will likely increase earnings over time. But due to their smaller market cap, and shorter track record in addition to expected rate cuts, CION is one I will be watching in the coming months. For now, I rate the stock a hold as I would like to see more from the company.

For further details see:

CION Investment: This BDC Looks Like A Future Superstar But Is It Too Soon To Tell?