ORCC - CION Investment: This Strong BDC Outperforms In 2023

2023-04-16 09:45:29 ET

Summary

- CION makes investments in middle market companies to generate market beating returns due to their expertise in private credit and rigorous lending practices.

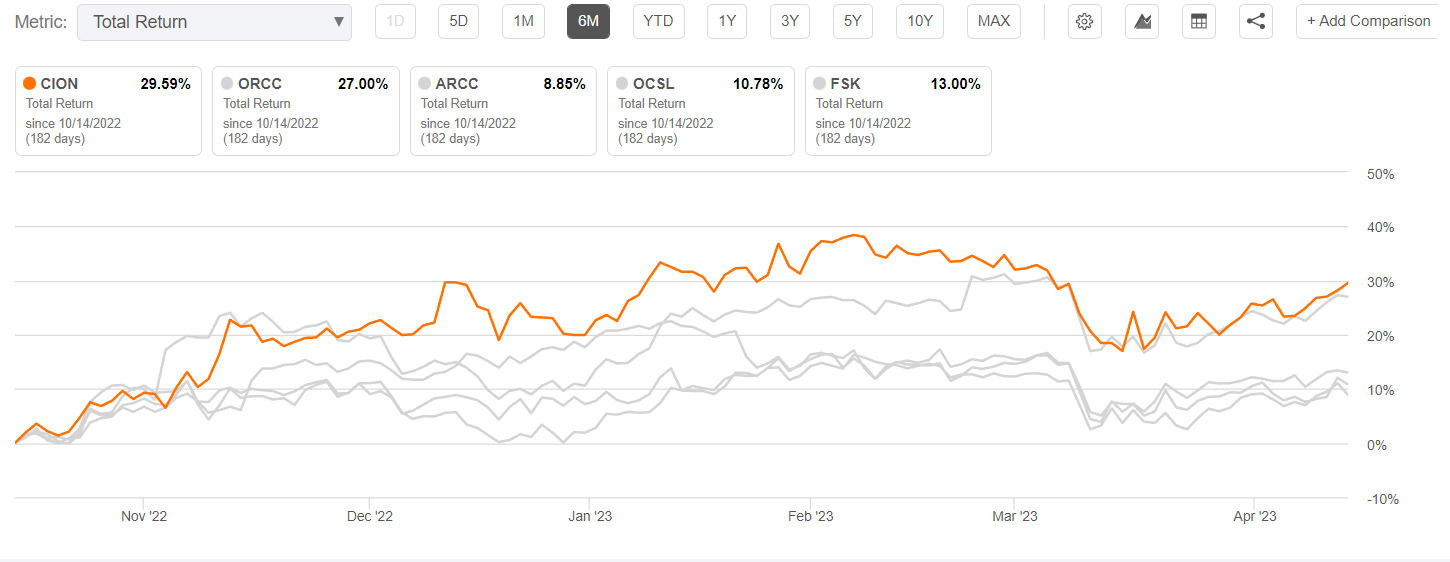

- CION has outperformed most of its peer BDCs over the past 6 months including ARCC, ORCC, FSK, and OCSL.

- The regular quarterly dividend was recently increased by nearly 10% and now yields over 13% on an annual basis going forward.

While several articles have been hitting the SA headlines recently regarding some of the larger and more popular BDC (Business Development Company) choices such as Ares Capital (ARCC), the lesser known and better performing CION Investment Corporation ( CION ) has been quietly outperforming most BDCs over the past 6 months. One of several BDCs that I own in my No Guts No Glory Income Compounder portfolio , CION only recently did a public offering (October 2021) and was operating privately for nearly 10 years prior to the public listing of the stock.

When I last wrote about CION back in September 2022, I discussed how their access to private credit markets helps to boost the total portfolio value and provides a higher total return than other peer BDCs as a result. In the 6 months or so since I wrote that article, CION has outperformed most of its peers, as well as the S&P 500, by a wide margin. This is what I wrote back in September describing the private credit advantage.

Meanwhile, the CION portfolio managers will likely deploy funds to take advantage of the opportunities that may prevail in private credit markets to further increase the portfolio NAV and thereby enabling continued growth in future distributions.

Seeking Alpha

Comparing CION to ARCC and several other BDCs that I currently own or am following including FS KKR Capital (FSK), which I wrote about here , Owl Rock Capital (ORCC), and Oaktree Specialty Lending Corporation (OCSL), the total return over the past 6 months has been the highest for CION closely followed by ORCC. The others are not far behind and appear to be catching up so far in 2023, although they all took a hit in March due to the banking crisis that impacted the entire financial sector.

{kind=link}

Nevertheless, 2023 is shaping up to be a good year for most BDCs, especially those that lend to upper and middle market companies like CION does, and as banks are struggling to maintain their balance sheets and may cut back on lending as a result, offering a further opportunity for BDCs to step in. As my fellow SA analyst, ADS Analytics , suggests:

An interesting question is which BDCs stand to benefit from this dynamic? A first order guess is that because bank lending is typically focused on larger companies, it is those BDCs that directly compete with banks that should benefit the most from additional lending opportunities. That means BDCs that operate at the upper end of the middle-market segment such as ARCC, OCSL and ORCC.

Another BDC that stands to gain from the cutbacks in bank lending is CION with the opportunity to take advantage of private credit markets as a bonus, as I discussed in my previous article based on commentary from CION:

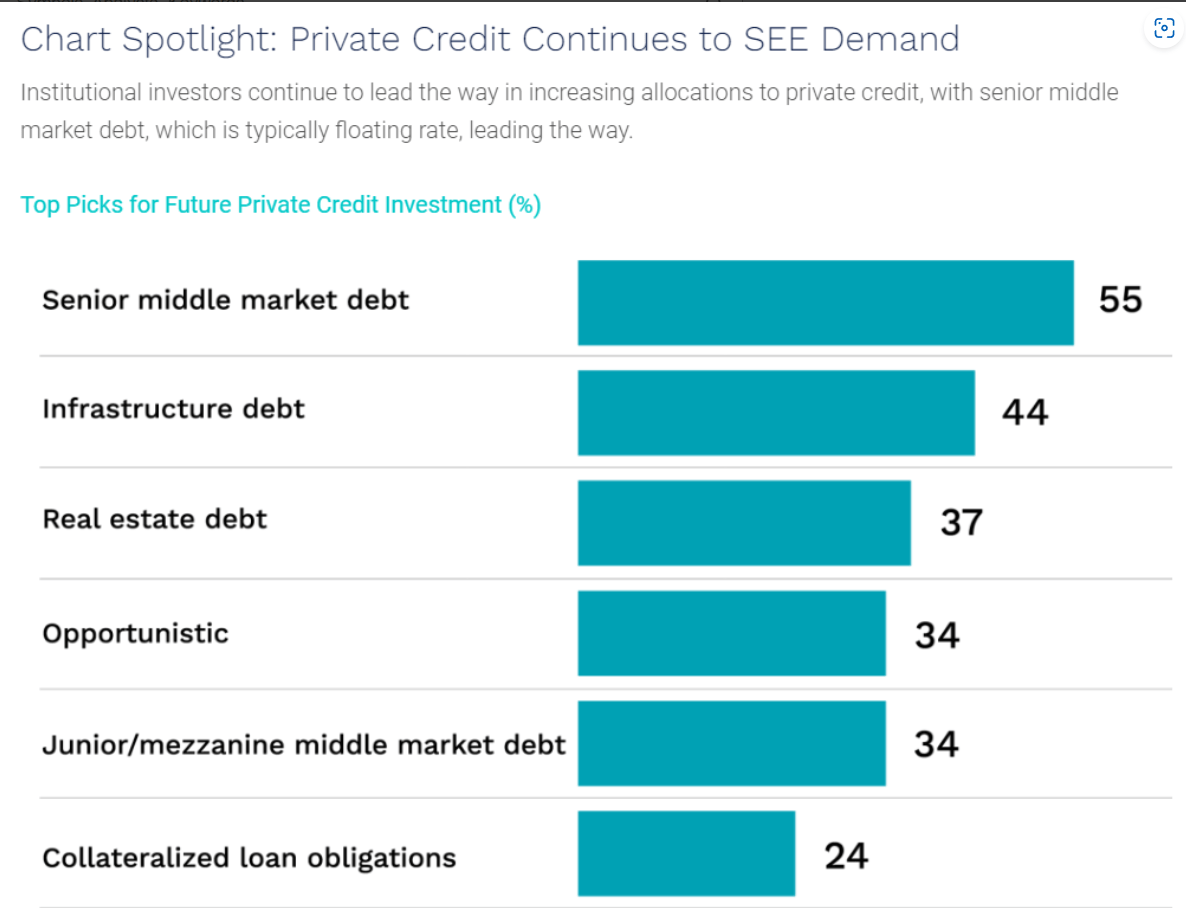

CION invests primarily in the debt of private middle market companies through the issuance of 94% senior secured loans which are about 85% floating rate, so this BDC stands to benefit from rising rates. In addition, the commentary notes that future expectations are expected to remain negative with further softening of demand over the next six to twelve months. Price pressures are expected to persist at least through the end of the year. The silver lining in all of this is that opportunities exist to invest more in private credit, which is expected to see continued demand as illustrated in this chart from the article.

{kind=link}

While CION is not the only BDC that operates in private credit markets, nor is it the only one that benefits from rising rates (which may not yet be done rising), CION has demonstrated strong performance over the past six months despite the weakening credit markets over that same period. On March 16, 2023 when CION announced Q1 2023 (quarter ending 12/31/22) earnings , they also announced a nearly 10% increase in the dividend. And even though the NAV dropped slightly from the previous quarter from $16.26 to $15.98, they reported NII of $0.43 per share, more than covering the increased dividend.

CION also announced that, on March 13, 2023, its co-chief executive officers declared a first quarter 2023 regular distribution of $0.34 per share payable on March 31, 2023 to shareholders of record as of March 24, 2023, which is an increase of $0.03 per share, or 9.7%, from the $0.31 per share regular distribution paid by CION during the fourth quarter of 2022.

Non-accruals remained low at 1.3% based on portfolio fair value and 2% at amortized cost. The debt to leverage ratio increased slightly from 1.05x to 1.08x in the quarter. The company repurchased more than 900,000 shares at an average cost of $9.06. And they added new investment commitments of $92 million with $83M in funded commitments. They also reported sales and prepayments amounting to $144 million.

Not to be forgotten, the company also paid a special dividend in the quarter of $0.27 per share in addition to the regular quarterly dividend. Meanwhile and subsequent to the report, the company completed a public offering in Israel on February 28, 2023, in which the company issued $80.7 million in unsecured Series A notes due 2026 at a rate equal to SOFR + 3.82% per year payable quarterly. The offering was oversubscribed by Israeli Tier 1 institutional investors to the tune of 1.3x raising about $100M for the company to put to work on new investment opportunities.

The company ended the year on a strong note and feel that they are well positioned heading into 2023, based on comments from co-CEO, Michael A. Reisner:

“As we have mentioned several times, since 2021 when we saw the first signs of potential economic slowdown, we have been operating under a business strategy focused on building a defensive portfolio to withstand turbulent times. Today, we believe that due to our long-term strategy, we have positioned our portfolio well to overcome any potential headwinds our portfolio companies might face this year.”

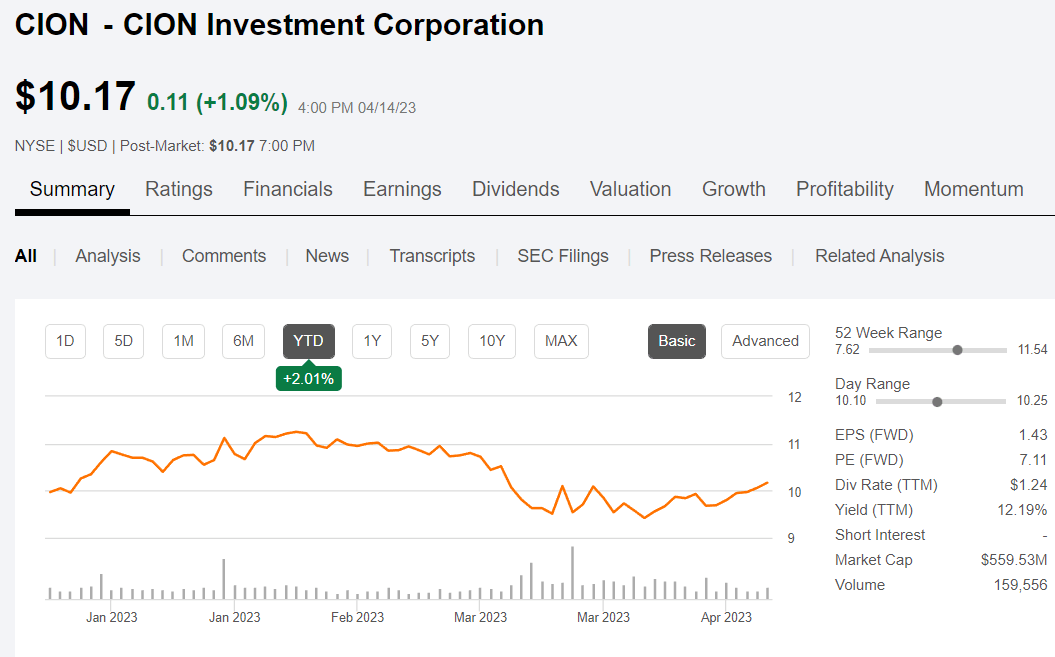

At the market price of $10.17 as of the close on 4/14/23, CION is trading at a discount to book value of nearly 40% while offering an annual yield of 13.3% based on the current quarterly dividend of $0.34. That assumes no additional special or supplemental dividends or additional increases going forward. Given that they have excellent dividend coverage based on the previous quarter’s results and the positive outlook for 2023, I would conclude that it is quite possible that they will declare an additional increase in the distribution at some point in the next few months.

{kind=link}

While other BDCs may also have elevated dividend coverage levels, they are not as forthcoming in passing along the extra income to shareholders, as was the case with ARCC who maintained their dividend at $0.48 with no supplemental declared. There may be a reason to hold onto the buffer in distribution coverage due to the expectation that interest rates may start to fall at some point soon, however, that is not necessarily going to happen before late summer, or even before the end of the year as the Fed is expected to increase another 25 bps in May and then hold steady after that, unless inflation declines dramatically over the summer.

Externally Managed by CIM and Apollo

From the company’s latest 10-K, the relationship with CIM, CION Investment Management, is explained:

Pursuant to an investment advisory agreement with us, CIM oversees the management of our activities and is responsible for making investment decisions for our portfolio. CIM is a controlled and consolidated subsidiary of CION Investment Group, LLC, or CIG, our affiliate. Additionally, Apollo Investment Management, L.P., or AIM, a subsidiary of Apollo Global Management, Inc. (APO), or Apollo, also a member of CIM and a registered investment adviser under the Advisers Act, performs certain services for CIM, which include, among other services, providing ((A)) trade and settlement support; ((B)) portfolio and cash reconciliation; ((C)) market pipeline information regarding syndicated deals, in each case, as reasonably requested by CIM; and ((D)) monthly valuation reports and support for all broker-quoted investments. AIM may also, from time to time, provide us with access to potential investment opportunities made available on Apollo’s credit platform on a similar basis as other third-party market participants. All of our investment decisions are the sole responsibility of, and are made at the sole discretion of, CIM’s investment committee, which consists entirely of CIG senior personnel.

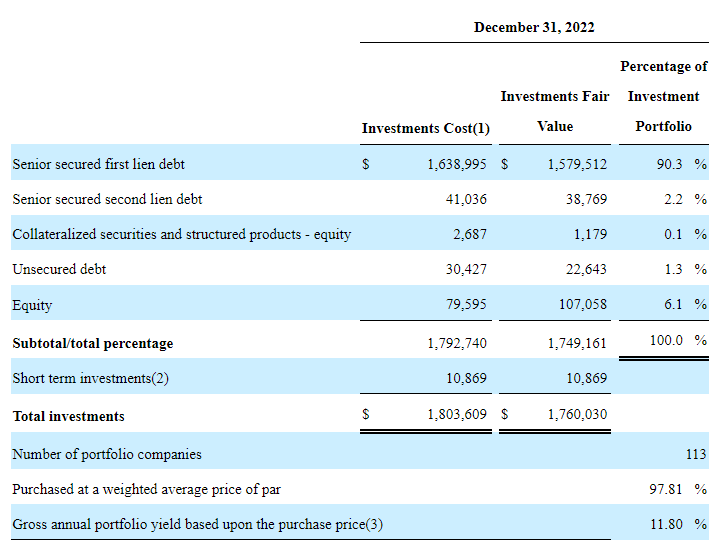

In other words, although you may not have heard of CION, they have been around for a while (since 2011) and they have some big names in the financial world involved in managing their business. The following table from the annual report summarizes portfolio investment composition as of 12/31/22.

{kind=link}

The company also completed a public listing and commenced trading of the company’s common stock under the ticker CION on the TASE, Tel Aviv Stock Exchange, as of February 26, 2023.

The Market Opportunity for CION

From the company’s latest Annual Report, the market opportunity for CION is spelled out in detail. I will summarize a few key points from that section of the report below for investors to consider.

The middle-market is a large addressable market.

With approximately 200,000 middle market companies in the US employing roughly 48 million people and accounting for about a third of private GDP, those companies combined contribute an estimated $10 trillion in annual revenue. Middle market companies are defined as those with $10M to $1 billion in annual revenue, or those that possess $75 million EBITDA or less. Investments in those companies generally range from $5 million to $50 million each.

Secular shift in the ownership of middle-market companies.

The number of US private equity companies is at the highest level since 2000, while the number of publicly listed companies has dramatically declined during that period.

Changes in business strategy by banks have reduced the availability of capital to middle-market companies.

Banks are focusing more on lending to larger companies and corporations, reducing the availability of debt capital to middle market companies.

There is a large pool of private equity capital available to finance strategic transactions.

From the annual report Business Overview section, this language highlights the opportunities with private equity:

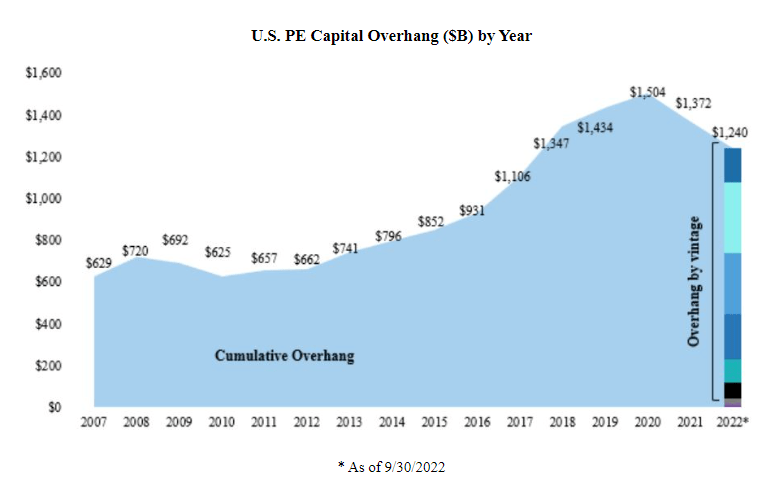

As depicted in the chart below, almost $1.24 trillion of unfunded private equity commitments were outstanding through the third quarter of 2022 (Source: Pitchbook's Q3 2022 Global Private Market Fundraising Report).

{kind=link}

The trend is toward active private equity focus on small and middle market companies.

Private equity funds tend to leverage their investments in smaller and middle market companies with a combination of equity capital combined with senior secured and mezzanine loans from other sources. CION can offer the role of leverage provider in some of those instances.

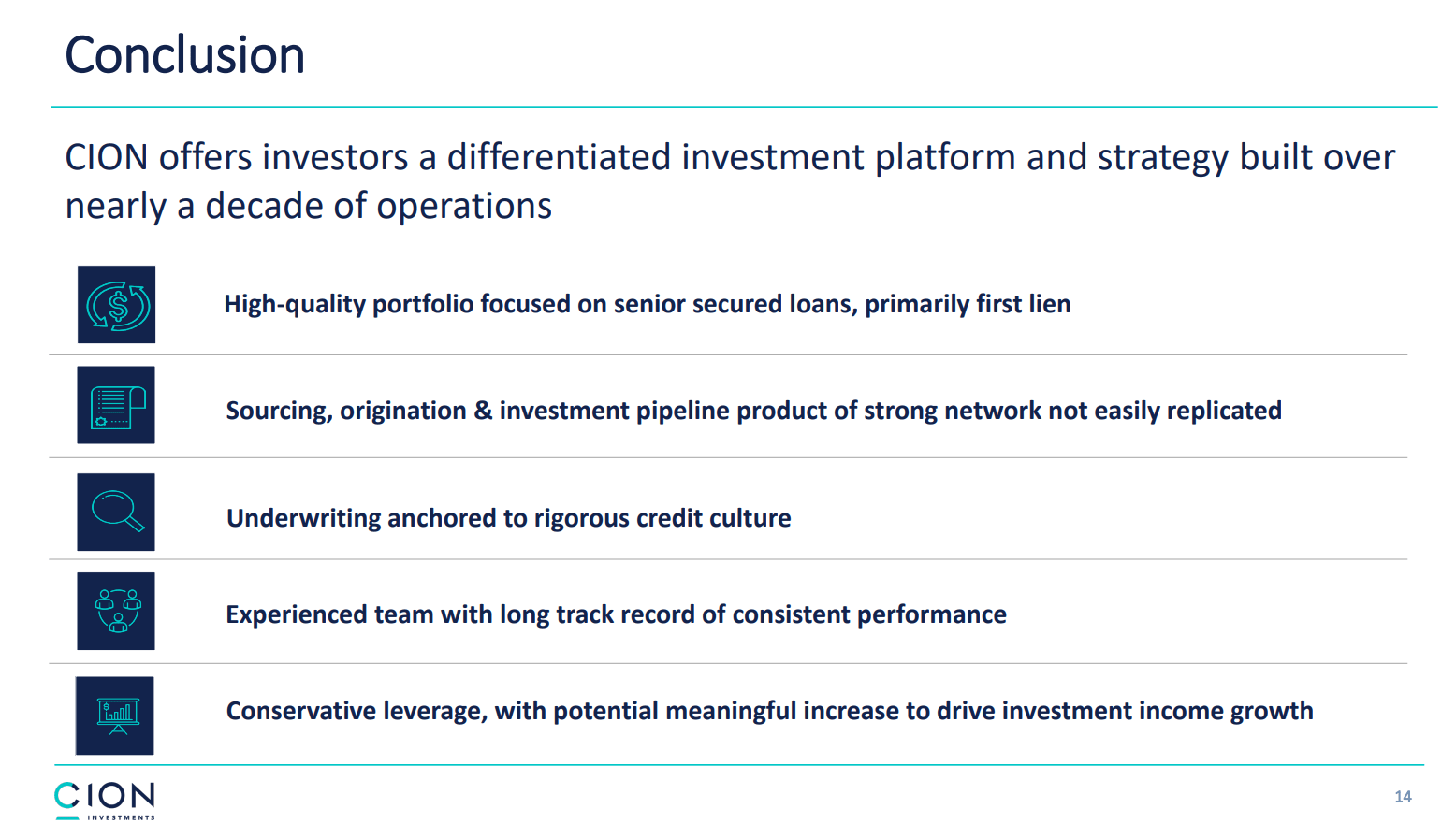

Summing it all up in a single slide in the company’s investor presentation , CION offers investors a differentiated investment platform and strategy to generate strong returns.

{kind=link}

As I mentioned in the beginning of this article, I like CION for its high dividend yield and potential for capital appreciation. It currently trades at a significant discount to book value, has increased the distribution and paid a year-end special dividend, and has good coverage of the distribution going forward. I believe that CION is a BDC that any income or total return oriented investor should consider for long-term investment, and it is a Buy at the current price of just over $10 per share.

For further details see:

CION Investment: This Strong BDC Outperforms In 2023