CFG - Citizens: A Buy Despite An Interest Rate Misstep

2023-10-19 13:19:32 ET

Summary

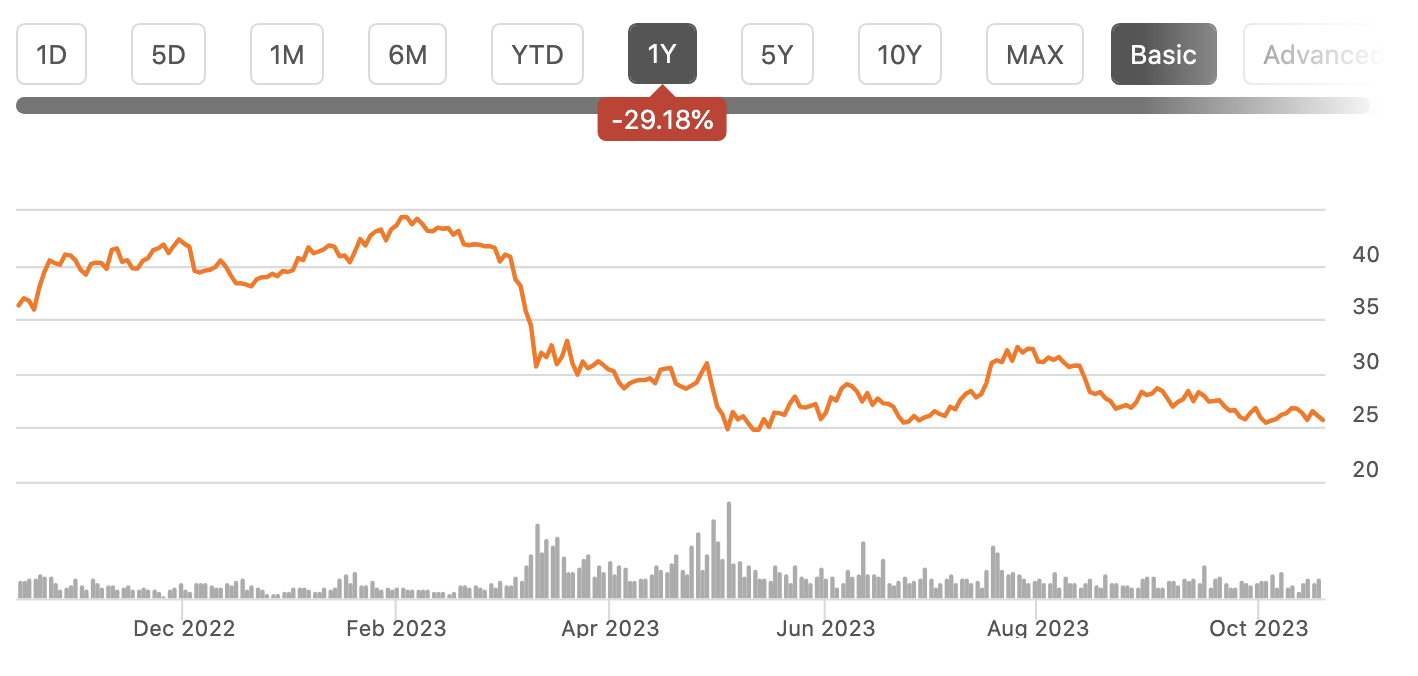

- Shares of Citizens Financial Group have performed poorly over the past year, losing about one-third of their value.

- The company reported messy Q3 results, with earnings down 32% from last year due to rising funding costs and lower noninterest bearing deposits.

- Despite the challenges, the valuation of the stock suggests that investors are being paid to wait for a recovery.

Shares of Citizens Financial Group (CFG) have been a poor performer over the past year, losing about one-third of their value. Regional banks as a sector have done badly ever since the Q1 banking crisis spurred by the failure of Silicon Valley Bank; still, its poor performance has been particularly disappointing as I recommended it as "strong buy" last October . Shares fell on Wednesday after the company reported Q3 results. The quarter was messy, and 2024 will be a transition year, but at this valuation, I do think investors are being paid to wait.

{kind=link}

In the company's third quarter , Citizens earned $0.89 in non-GAAP EPS relative to a $0.91 consensus . This was down by 32% from last year as rising funding costs and lower noninterest bearing deposits squeeze results. Last year, I thought CFG would have about $5.50 in earnings power; instead, the bank is set to earn under $4. There are two primary reasons for this: interest rates have risen more dramatically than I expected, which has weighed on results, and depositing funding became more competitive after the crisis, increasing its funding costs. Progress moving past these challenges has also been slow.

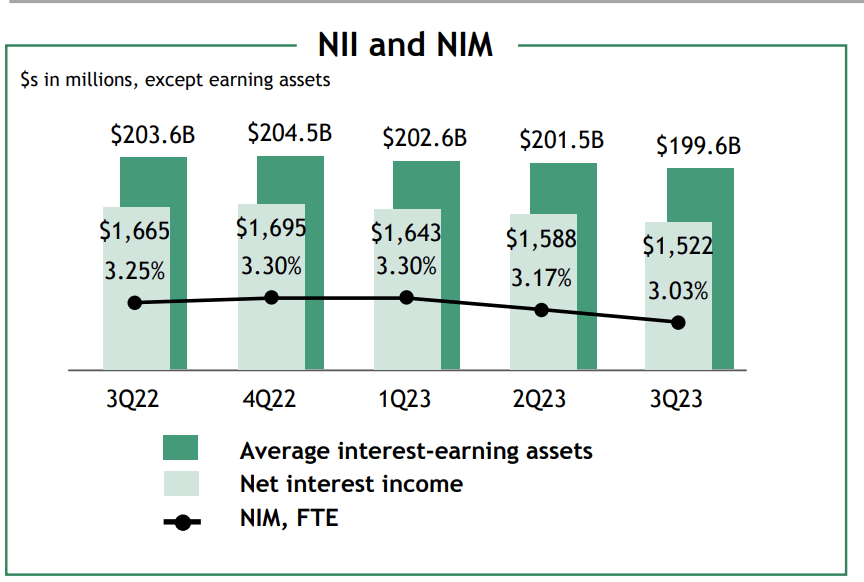

In the quarter, net interest income fell by 9% from last year to $1.522 billion. There are two drivers of net interest income: interest earned on assets and interest paid out on liabilities. As with many banks, CFG is saddled with a securities portfolio of high-quality fixed income bought when yields were lower. Its portfolio is $34 billion and has an over $3 billion mark to market losses, which is the primary contributor to its $5.3 billion loss in accumulated other comprehensive income. This portfolio has a duration of 5.2 years, and so over time, these bonds will mature and can be reinvested at higher yields, but it will be a multiyear process.

The majority of its loans are floating rate, and so here, Citizens is seeing a benefit from higher yields. Loan yields rose 14bp to 5.66% (up 149bp from last year). Loan balances fell 2% to $150.8 billion, on average during the quarter, with noncore declines of 10% and core declines of 1%. The bank's loan to deposit ratio is healthy at 84%, providing some room for loan growth.

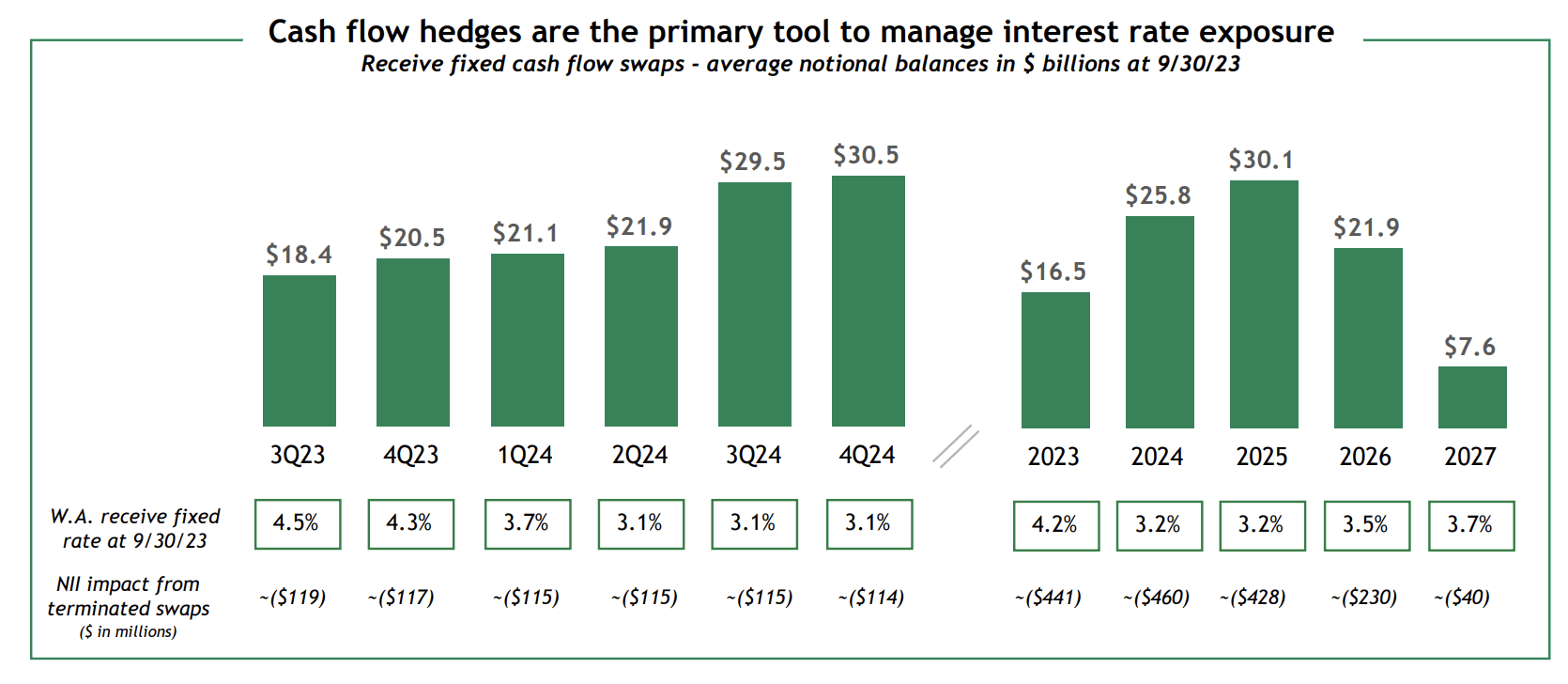

The other problem Citizens faces, which is much greater than I expected it would be last year, was that management locked in rates via swap contracts over the past two years aggressively. After years of low rates, when long-term rates began to move higher, it wanted to lock that in to protect against a return to low rates. At the time, it seemed fairly prudent, but it hindsight by doing so, it left a lot of money on the table that could have been earned by waiting longer to lock in rates.

As you can see below, CFG swapped out about $19 billion of notion assets this past quarter. The reason why I stated earlier that 2024 will be a transition year is that this ramps up to $30 billion in H2 2024 at 3.1%, which will be a ~$115 million headwind relative to the forward curve. Now of course, if a shock occurs and the Fed dramatically lowers rates, these swaps would suddenly be profitable and seem wise, but at the moment, they are set to be a drag, effectively turning 20% of its loan portfolio from floating rate to fixed rate. This headwind should gradually improve over 2025, assuming the forwards curve (which assumes three rate cuts next year) plays out. If rates stay higher, these swaps are more of a drag and vice versa.

{kind=link}

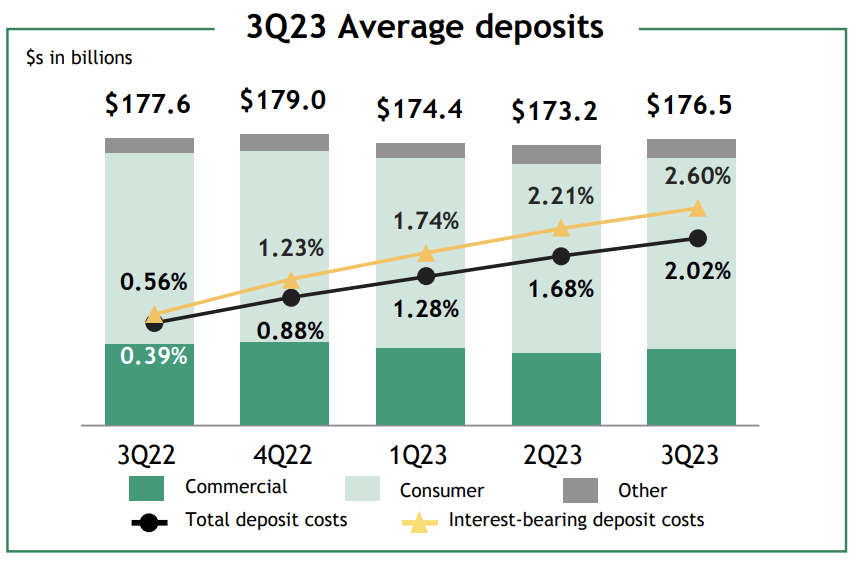

At the same time, deposit funding has become much more expensive since SVB's failure. Now, CFG has acquitted itself relatively well in the fight for deposits. Deposits are essentially flat from last year's level, recovering $3.3 billion from trough levels in Q2. There has been a mix shift though with 22% of deposits noninterest bearing from 26% in Q1. 70% of its deposits are insured, a bit above industry average, and 67% come from consumers rather than businesses. Both are likely reasons its deposit balances have held in fairly well.

{kind=link}

However, these deposits have become much more expensive. Deposits costs are 2.02% from 0.39% last year. That 34bp sequential increase is quite similar to the 40bp rise in Q2 and Q1. With the Fed raising rates just 25bp in Q3, it is disappointing to see deposit costs rise that much. I would have expected to see deposit costs rise at a more gradual pace. Management has said that the pace of low-cost deposit attrition is slowing, so hopefully that shows in Q4 results, but this result was disappointing.

The combination of higher funding costs and too much fixed-rate exposure led net interest margin to fall 14bp in Q3, slightly worse than the 13bp in Q2. Again some deterioration was to be expected as higher funding costs in Q2 fully filtered through to results, but I expected to see a sequential improvement, not degradation.

{kind=link}

Aside from interest rates, I would hit on several other points. Noninterest income fell 3% to $492 million, primarily due to weaker capital markets activity; with some deals postponed into Q4, management is expecting some sequential improvement here. One bright spot is that mortgage servicing rights saw a $10 million benefit from higher rates-higher rates reduce refinancing, which means CFG will be servicing (i.e. collecting payments) these loans for longer, making those rights more valuable. This should be a further small tailwind in Q4 as rates have continued to rise.

In terms of credit quality, I am fairly comfortable with how CFG is positioned. Provisions for credit losses were $172 million, down $4 million sequentially but up $49 million from last year. Its allowance for credit losses is 1.55% of outstanding loans, which is 25bp more than its normalized level. This is because management is assuming a moderate recession over the next two years, which may even prove conservative. Its $2.3 billion in allowances provide 179% coverage of its $1.3 billion in nonaccrual loans.

Commercial real estate has also been an area of focus, in particular office space. CFG has $3.7 billion in office loans, a bit over 2% of its total loan book, which is quite manageable. CFG is being quite conservative here. Allowances are 9.5% against office loans at $354 million. This balance would protect against a 20% default rate at a 68% decline in valuation. This would be a very dramatic downturn in office space. As such, I do not foresee the need for a material increase in allowances here.

Next quarter, management is expecting about a 2% drop in net interest income, partially offset by improved capital markets activity. That would imply about $0.85-0.88 in EPS next quarter. Management is also expecting net interest margin to deteriorate, though at a much slower pace to about 3.00%, or slightly lower. Next year, given the swaps portfolio, the bank should see limited exposure, positive or negative, to changes in interest rates with NIM hopefully able to exit 2024 still near 3% as excess liquidity is deployed, but it could stay in the 2.90% area. Some of this will also depend on whether deposit yields can be brought down as quickly as they increased recently, should the Fed cut rates.

While its swap contracts have left over $100 million in quarterly potential interest income on the table, the bank still has $3.2-$3.40 in earnings power, given my view it should not need to build credit allowances further, for an 8x earnings multiple.

CFG is also well capitalized with a common equity tier one (CET1) ratio of 10.4%, up from 9.8% last year. Management expects this to rise to 10.5% in Q4. Citizens has been building capital because it will gradually need to include its $5.3 billion AOCI loss into its CET1 calculation.

Importantly, this AOCI loss will shrink as bonds pull to par and mature and its fixed rate swap contracts are paid out. Based on the forward curve, there will be $1.7 billion improvement by the end of next year and a further $600 million benefit in 2025. This narrowing loss combined with the retention of excess capital will enable Citizens to manage through this regulatory phase-in without problems.

To accelerate this process though, management sees a " modest " level of share repurchases going forward to retain more capital. Last quarter, it bought back $250 million in stock, and its share count is down 6% over the past year. I would expect buybacks to run at or below $100 million, meaning 2-3% share count reduction is a more reasonable estimate. Its $0.42 dividend is secure given CFG's earnings power, and that does provide a 6% yield.

Citizens has a tangible book value per share of $27.73. This value includes all of the losses housed in AOCI, excluding which book value would be nearly $39. With $1.7 billion in AOCI improvement to come next year alongside the retention of earnings, tangible book value is well positioned to get to $32 by the end of next year.

This is why I come to the conclusion that CFG is too low to sell here. The swaps and securities portfolio are headwinds that will reduce earnings; this much is clear. That said, shares are now trading 8% below tangible book value, which includes the mark-to-market impact of these decisions. That feels excessive, and I believe it is due to investor disappointment in Citizens' performance as well as the realization that it will take about 18 months to get through the majority of this pain. That is a long time to play out for many investors who like me feel burned because what had been a deposit growth story twelve months ago turned into a bank poorly positioned for a surprisingly large move in interest rates.

At less than 8x earnings with an attractive dividend and appropriately reserved loan book that will see double-digit tangible book value growth just by virtue of these swaps and bonds maturing, the negativity towards CFG feels over-done. There is no quick fix here, but I believe investors are paid to be patient. Importantly, the underlying franchise is still retaining deposits better than peers and is well capitalized. In my view, a bad interest rate bet is less problematic than a problem with the core business as the passage of time will at least get us through these maturing contracts.

I do think that CFG should at least be trading at tangible book value, which in a year will be above $30. That combined with its dividend yield creates a 20% return potential. I suspect it will be a slow recovery in shares as it requires patience. In this case, I do think patience will be a virtue and in 12-18 months, investors will be glad not to have sold CFG in frustration after this quarter. Buying 12 months ago was a mistake, but I believe buying today will prove to be an opportunity.

For further details see:

Citizens: A Buy Despite An Interest Rate Misstep