CVX - Civitas Resources: Predictable Performance And Low Valuation Make It A Target

2023-05-23 02:40:58 ET

Summary

- For 1Q23 Civitas cranked out another strong, "routine" quarter.

- Former regulatory headwinds have become tailwinds but valuation remains low for the strong capital efficiency, fortress balance sheet, and unparalleled shareholder return program.

- Chevron's move to acquire Wattenberg peer PDCE places a target on Civitas as they become the last smid cap standing in the play.

We've written on Bonanza Creek and the subsequent Civitas Resources ( CIVI ) many times over the years, most recently here . The company is a conservatively run upstream name focused on the DJ Basin of Colorado. We view them as better positioned now than at any time in the past with a strong location inventory and improving well results while offering a nearly unparalleled shareholder return program, and a fortress balance sheet. Monday's announcement that Chevron ( CVX ) is acquiring DJ Basin peer PDC Energy Inc ( PDCE ) prompts to once again highlight this still quite inexpensive, consistent E&P player.

A little recent history.

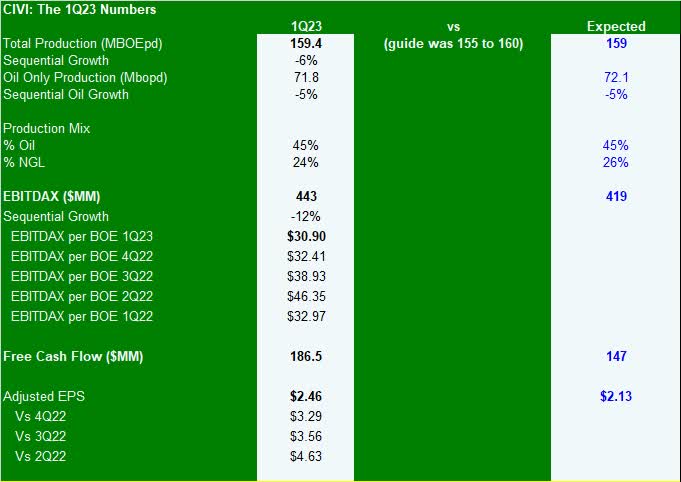

1Q23 was better than expected. Earlier this month Civitas reported another strong quarterly performance as noted in our summary table.

{kind=link}

As you noted above, production was modestly ahead of expectations while capex was modestly below guidance. EBITDAX was 6% above Street expectations and Free Cash Flow was a whopping 27% above Street consensus.

Management reaffirmed 2023 Guidance for spending and volumes and without a major change in the oil strip we would expect 2024 to be another flattish volumes year given commodity prices and service costs. They continue to manage to an optimized free cash flow model for maximization of cash to return to shareholders.

Shareholder Return - Best in Show.

Dividend Provides Double Digit Implied Yield at $75 Oil. With the first quarter:

- Management, as anticipated, maintained the Base dividend of $0.50 per quarter. However, more interestingly, the Variable Dividend did not collapse with lower commodity prices as we saw with almost all of their U.S. upstream peers, instead only easing from $1.65 in 4Q22 to $1.62. We have been fans of the smoothing effect of their TTM Variable calculation since they rolled it out. While 2Q23 will bring further retreat in the variable component as lower prices roll through the calculation this dampening of volatility in the implied yield should be welcomed by investors who abhor the "ok what about next quarter?" dividend question. The variable calculation is straight forward and further delineated in the cheat sheet below. As such, the combined implied dividend yield did not collapse and remains in the low teen %'s. On our Base Case $80 deck we see a TTM based yield at year end near 11% and at $70 oil, our Sub Case, this edges down to about 8%.

Z4 Energy Research

- On the share repurchase front they also have a $1 B repurchase authorization in place after having opportunistically repurchased $300 mm in 1Q23. This represents near 20% of outstanding shares at current pricing.

Balance Sheet: Civitas' balance sheet has been in a net cash positive for the past four quarters and they have nothing drawn on the revolver with only the single tranche of $400 mm senior notes due in 2026. We note the cash balance remains robust at > $0.5 B despite the aforementioned buyback.

In other highlights from the quarter, the company continues to reap improved drilling and completion efficiencies and they are seeing no well performance degradation. At the current pace of activity the company has an approximate 10 year location inventory and they are 100% permitted for 2023 (at this point in 2022 they were far from fully permitted) and they are well on the way to permitting their 2024 and 2025 programs.

A few comments on the CVX proposed acquisition of PDCE.

In our view the deal makes sense for Chevron and PDCE. The primary focus of this transaction is the DJ Basin though PDCE does have a smaller Delaware Basin wedge.

- For Chevron deal is accretive in the near and medium term time frames and both companies see the footprint as well delineated. This deal cores up Chevrons DJ holdings and makes it a top 5 play for them in terms of both production and free cash flow. Given CVX's massive $17.5 B buyback they are set to take in the deal related shares in less than two quarters.

- For PDC they become a larger part of a bigger company that is focused on shareholder returns and prosecution of their DJ acreage will benefit from scale as well as spacing and well design optimization as the two teams put their heads together.

- For CIVI, we note a number of interesting dislocations vs PDCE (see table below). In quick summary, CIVI is less levered than PDCE, CIVI's production is oilier than PDCE, CIVI generates better EBITDAX per BOE margins, and it trades at a markedly lower TEV / barrel of produced oil at present. CIVI also offers a better implied dividend yield on their base dividend. And then there's the strong balance sheet. And yet, based upon the deal valuation, CIVI trades at a significant TEV/EBITDA valuation in 2023 and 2024 using Street or our own numbers. We're not saying Chevron is paying too much. We are saying the market continues to overly discount the Civitas story.

Z4 Energy Research

A quick comment on Z4's model. To be more conservative, since quarter end, we tweaked our volume view on the year from top of range to just above middle given the potential for slowing if commodity prices do not move as expected in 2H23. Also, both our Sub and Base cases now utilize $3 natural gas. We'd rather be low and wrong than the opposite any day.

Nutshell: We view the proposed PDCE acquisition by CVX as further evidence of a less fearful regulatory environment in Colorado and one that highlights CIVI's low valuation despite strong relative year to date performance. CIVI is up 24% this year vs PDCE (up 12% at the implied $72 acquisition price) vs the ( XOP ) which is off 7% so far in 2023. With this deal, CIVI is not only cheap but becomes the "last smid-cap standing" in the in the DJ Basin (we included short interest at the bottom of the preceding as we find this somewhat odd). We continue see CIVI as underpriced for the combination of FCF generation, high yield, the buyback, the deep inventory position, high margins, and strength of balance sheet. Our expectation remains that CIVI can carry a 4x multiple of our 2023 Base Case yielding an upside target of $102.50 in the next 6 to 9 months. We continue to own CIVI as the largest holding in our portfolio.

{kind=link}

For further details see:

Civitas Resources: Predictable Performance And Low Valuation Make It A Target