VODAF - CK Hutchison Holdings: A Safe Harbor In Stormy Times

2023-03-23 04:49:08 ET

Summary

- This Hong Kong-based global conglomerate delivered another good year in 2022.

- On paper, CK Hutchison Holdings offers good value at a low P/E of 5 and P/NAV of 0.36.

- The dividend is well covered and yields about 5.5%.

- Yet, it is hard to find a catalyst that could close the difference between the share price and the NAV per share.

CK Hutchison Holding logo (Ck Hutchison Holding )

Investment thesis

Despite the fact that the world seems to be going from one crisis to another, some companies are still doing well.

CK Hutchison Holdings Limited ( OTCPK:CKHUY ) is one such company. They have again proven resilient with their latest financial results which came out on the 16th of March 2023.

We like the business and the company, and we are invested in other companies within Li-Ka Shing's empire but have been reluctant to allocate capital to CKHUY in the past.

Let us look closer at the numbers and revisit the thesis of January this year.

2022 FY Financial Results

On the top line, revenue increased by 2.6% from HK$445.4 billion in 2021 to HK$457.2 billion in 2022.

Reported earnings were up from HK$33.48 billion to HK$36.68 billion in 2022, with EPS increasing by 10% from HK$8.70 to HK$9.57.

Based on a share price of HK$48.15 we get a very attractive P/E of just 5.0.

With this good jump in the EPS, management decided to pay out a dividend of HK$2.926 per share, which is also an increase of 10% from the previous year. We had hoped that they would increase the payout ratio but they chose to keep it at the same level of 30%.

CK Hutchison Holding's EPS and dividend history (Data from CKHUY. Graph by author.)

{kind=link}

As we can see from the graph above, even in exceptional circumstances like it was in 2015, they did not distribute 30% of their EPS as dividends.

Earnings are one thing, but we like to look at cash generation from their operation. This is less "noisy" than the accounting principle of earnings which takes into account the mark-to-market of assets and other "non-cash items.

Net cash from operation in 2022 was HK$56.71 billion. That was 8.7% higher than the HK$52.18 billion it recorded in 2021.

We look at their balance sheet and start by looking at their assets. Their non-current total assets were HK$924 billion at the end of 2022.

Out of this, CKHUY has a significant amount of intangible assets under goodwill and brand names. Goodwill which came from various acquisitions over the years amounted to HK$268 billion and brand names were an additional HK$67 billion.

In 2022, CKHUY took an impairment of goodwill of HK$11 billion relating to their telecom business in Italy.

Now on to their liabilities. It is positive that CKHUY's net debt decreased from HK$167.65 billion to HK$134.61 billion at the end of 2022.

One way to determine if a company's debt level is too high is to look at its net debt to EBITDA as it gives us an indication of its ability to service its debt. Generally speaking, anything higher than a 2 to 3 ratio is not ideal.

CKHUY had an EBITDA of HK$119 billion, so we get a comfortable net debt to EBITDA ratio of 1.13.

Inflation is not going away as soon as central banks around the world had anticipated and hoped for. Despite concerns about the financial well-being of some banks and what that can do to the economy, central banks have, for now, decided to keep increasing the interest rate in order to get the inflation down to approximately 2% which is what is considered to be "ideal".

Higher interest rates will mean a higher cost of financing.

As of 31st December 2022, CKHUY had approximately 34% of the Group's total principal amount of its debts on floating rates and the remaining 66% were at fixed rates. They have made interest rate swap agreements with banks to swap up to HKD21.36 billion of their floating rates to fixed rates. Should they take up these options the floating rate portion goes to about 27%.

Their average cost of debt remains low at 2.0% in 2022 and the average maturity is 4.8 years.

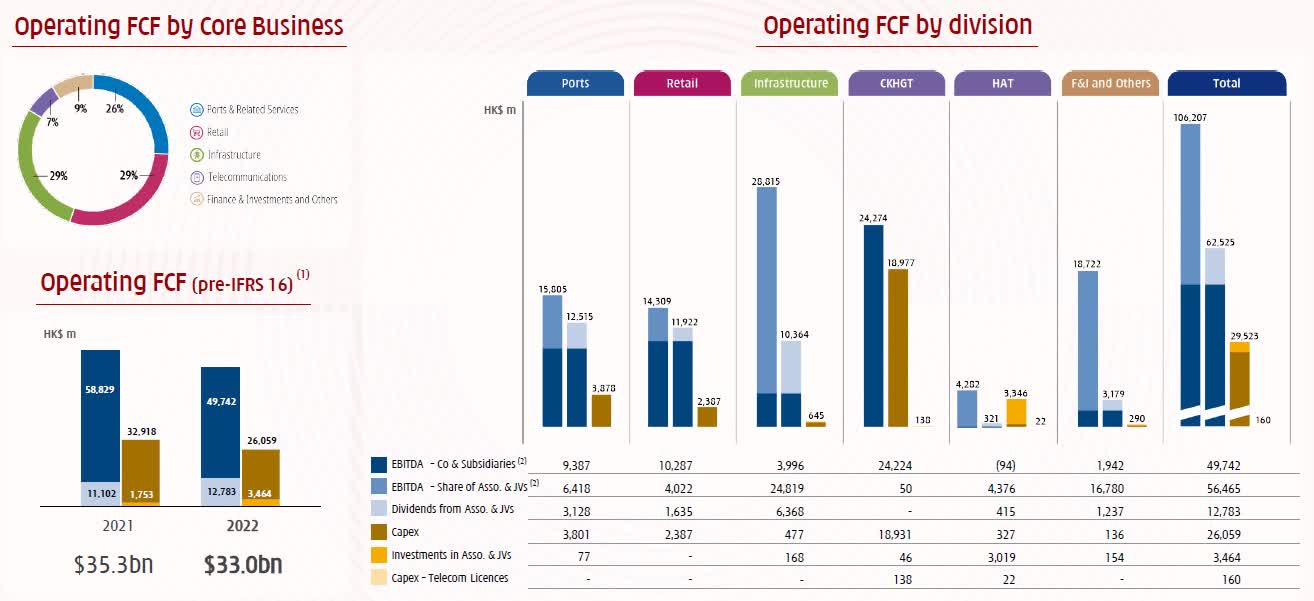

We like to go through the main results of the group's divisions. Bear in mind that CKHUY does not disclose a breakdown of their net operating profit in the various divisions, as all finance costs, amortization, and depreciation is done on a group level through their finance division.

We do get EBITDA which is what we report and a graph showing the free cash flow the various divisions generated.

- Ports and Related Services

CKHUY has the world's leading port network and has interests in 51 ports comprising 295 operational berths in 25 countries as of the end of 2022. This division operates container terminals in six of the 10 busiest container ports in the world. CKHUY holds an 80% interest in the Hutchison Ports group of companies and a 30% interest in the Hutchison Port Holdings Trust ( OTCPK:HCTPF ), which is listed in Singapore and where we have been shareholders for a long time.

The EBITDA was HK$15.81 billion which was 13% of their total EBITDA.

Due to slower volumes of containers being shipped globally, we do expect lower EBITDA from this division in 2023.

- Retail

Under the umbrella of a fully owned company called A. S. Watson, CKHUY has the world's largest international health and beauty retailer with a loyalty member base of 141 million customers. They operate 12 retail brands with 16,142 stores in 28 markets worldwide as of the end of 2022.

Its EBITDA in 2022 was HK$14.31 billion, which contributed 12% to the group's total EBITDA.

With traveling to and from Hong Kong and China, we believe CKHUY will have higher EBITDA from retail in 2023.

- Infrastructure

This division comprises CKHUY's 75.67% interest in, a subsidiary with a separate listing on the HK Stock Exchange. It also gets 10% economic benefits from the Group's direct holdings in 6 other infrastructure investments co-owned with CK Infrastructure Holdings. These are Northumbrian Water, Park'N Fly, Australian Gas Networks, Dutch Enviro Energy, Wales & West Utilities and UK Rails.

This division had an EBITDA of HK$28.82 billion which was 24% of the total.

We do not expect much change to EBITDA from this division in 2023.

- Telecom

Telecom has become the biggest division in CKHUY.

It consists of CK Hutchison Group Telecom Holdings which consolidates the 3 Group businesses in Europe and a 66% interest in Hutchison Telecommunications, which has a separate listing on the HK Stock Exchange, as well as Hutchison Asia Telecommunications.

In our last article , we did report that CKHUY started a dialog with Vodacom ( OTCPK:VODAF ) for a potential merger for their 3 UK with them. According to a recent article by Reuters , Vodafone's CFO says that the discussion is moving in the right direction. A consolidation should bring synergies and cost savings for both parties.

The EBITDA for the entire telecom division was HK$41.61 billion. That constitutes 35% of the total EBITDA for the group.

We have seen positive signs from the telecom companies in Asia that we follow, namely Singtel ( OTCPK:SGAPY ), China Mobile ( OTCPK:CHLKF ), and Taiwan's Chunghwa Telecom ( CHT ) as income from roaming is picking up with more traveling taking place. This could potentially also boost CKHUY's telecom income in 2023.

- Finance & Investments and Others

The division consists of the corporate head office operations and the returns earned on the Group's holdings of cash and liquid investments.

Under the division comes investments such as an 88% interest in the Australian-listed Hutchison Telecommunications Australia, Hong Kong-listed pharma company HUTCHMED ( HCM ), TOM Group, CK Life Sciences Int'l., (Holdings) Inc., and Canadian listed oil & gas company Cenovus Energy ( CVE ).

This division's EBITDA in 2022 was HK$18.47 billion, which was 16% of the total.

We round up by looking at the free cash flow by divisions.

Hutchison Holdings operating free cash flow by divisions (Hutchison Holding 2022 Annual Financial Report Presentation)

{kind=link}

Business prospects

From year-to-year CKHUY often recognizes large net gains, or losses, from their various M&A activities. In 2022, they recorded a gain of more than HK$10 billion from such moves.

Management has informed that although their operating performances continue to be steady and solid, looking at the Group's M&A pipeline for the coming year, such one-off gains of similar magnitude may not materialize.

CKHUY is a huge company. What that mean is that there are always many exciting new business prospects. To get an idea of some of them, it is useful to read our last article as it too gives the reader an idea of some of the potential new areas for growth.

In addition to these, we also want to point out one very interesting new business development for CKHUY.

If you follow the political landscape in Hong Kong, you will be aware of the "hot potato" that is the government's inability to provide "affordable housing".

To try to help solve some of this, CKHUY has made a proposal to the government to turn a waterfront dockyard that is owned by Hutchison's Hongkong United Dockyards, into the city's second-largest housing development.

Their submitted proposal calls for building 34 residential towers, each between 27 and 48 floors, with other amenities such as shops. The residential units will hold 10,370 apartments plus 4,700 public housing units on their site and an adjacent government plot of land.

The land value is estimated at HK$22 billion after the payment of the land premium and assuming that the developer is not required to bear the cost of building the public homes.

If they get approval, it will be another profitable business for CKHUY.

Risks to the thesis and conclusion

As with so many value-stock, it is hard to determine if and when CKHUY's share will be priced closer to its fair value.

CK Hutchison Holdings difference between NAV and share price (Data from CKHUY. Graph by author)

{kind=link}

We always try to look for a catalyst.

It is a good company with solid fundamentals, but at the moment we struggle to find what could be a potential catalyst that could send the share price higher.

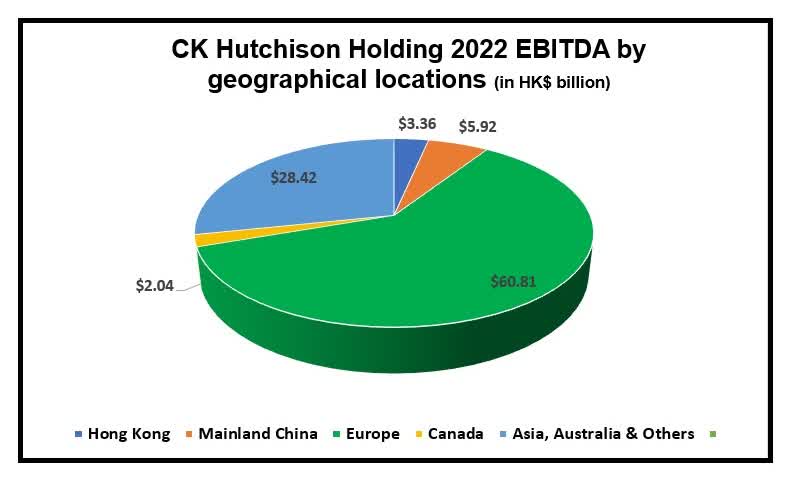

Some might assume that you invest mostly in China and Hong Kong if you invest in CKHUY, but that is not the case.

CK Hutchison Holdings EBITDA by geographical locations (Data from CKHUY. Graph by author.)

{kind=link}

Most of their EBITDA comes from Europe and not China.

Despite their good numbers over the years and the ability to grow, we have been reluctant to give CKHUY a Buy stance in the past. One of the reasons we put forward in our January article on " What to Expect from CKHUY FY 2022".

It will be interesting to see what they decide to do with the dividend for SH 2022. We think their payout ratio could be somewhat higher. It has been 31% for the last few years. In view of the low debt, we feel it should be somewhat higher."

We know that their argument against increasing the dividend would be to focus on reinvesting the excess cash into their business. That is a valid point, however since investors seem to pay little attention to the fact that CKHUY is trading at such a large discount to its net book value, it is hard to see how shareholders will benefit from all these reinvestments.

Perhaps a more aggressive return of capital to shareholders could be the catalyst but we do not see that as likely to happen.

As such we maintain a Hold stance.

For further details see:

CK Hutchison Holdings: A Safe Harbor In Stormy Times