IFF - Clariant: A Good Opportunity For Long-Term Dividend Investors

2023-11-02 16:55:22 ET

Summary

- Sales are decreasing as demand for durable goods is declining worldwide, and the recovery will likely be slow.

- EBITDA margins are currently impacted by currency headwinds and weakening demand.

- The latest acquisition should drive future growth and profitability.

- The dividend will likely have very limited growth in the coming years due to increased interest expenses, but the yield on cost is now higher than usual.

- This represents a good opportunity for long-term dividend investors.

Investment thesis

On April 23, 2023, I wrote an article about Clariant ( CLZNF ) ( CLZNY ) as strong inflationary pressures, labor shortages, and supply chain issues were generating doubts among investors who did not know how to qualify the recent changes derived from the restructuring process carried out in recent years as the macroeconomic context was marked by many uncertainties and operational volatility. Also, uncertainty increased even further due to growing concerns of a potential recession as a consequence of interest rate hikes. Since then, the share price decreased by a further 10% as the company is already starting to face a global panorama marked by lower consumption.

In recent months, operational performance has weakened as a consequence of the current recessionary landscape, and the company recently agreed to acquire Lucas Meyer Cosmetics in order to continue expanding its Care Chemicals segment. As a result, interest expenses are expected to increase significantly in the coming quarters, but in the long term, this acquisition brings the opportunity to provide very acceptable revenue growth rates in a business with a very high profitability profile.

Certainly, the current situation is delicate as sales and the EBITDA margin have suffered a significant impact in the third quarter of 2023 mostly caused by weaker demand and foreign exchange headwinds. Furthermore, everything indicates that the recovery will not arrive in 2024. Therefore, dividend investors will have to be patient and maintain perspective because, in my opinion, the accumulated 55% decline in the share price since 2018 represents a good opportunity to achieve higher dividend yields on cost in the long run as the company is still generating enough cash from operations to cover interest expenses, dividend payments, and capital expenditures, while headwinds are likely of a temporary nature due to their direct link with the current macroeconomic landscape.

A brief overview of the company

Clariant is a Swiss-based leading specialty chemicals company. It is the result of the spin-off from the Sandoz Chemicals division in 1995 and it operates 70 manufacturing facilities around the world that employ over 11,000 workers.

{kind=link}

The company operates under three business segments: Care Chemicals, which provided 57% of the company's total net sales in 2022, Catalysis, which provided 19%, and Adsorbents & Additives, which provided 24%. The company also enjoys strong geographical diversification as 39% of sales are generated in the EMEA, 31% in the Americas, and 30% in Asia-Pacific.

After a past marked by a growth strategy based on the acquisition of businesses, the company has more recently undergone a period of restructuring as it has divested less profitable businesses in order to focus on those with higher profit margins, especially since 2019, although this has not stopped it from continuing to find acquisition opportunities (you can see a list of recent acquisitions and investments in my last article) as the company keeps performing acquisitions.

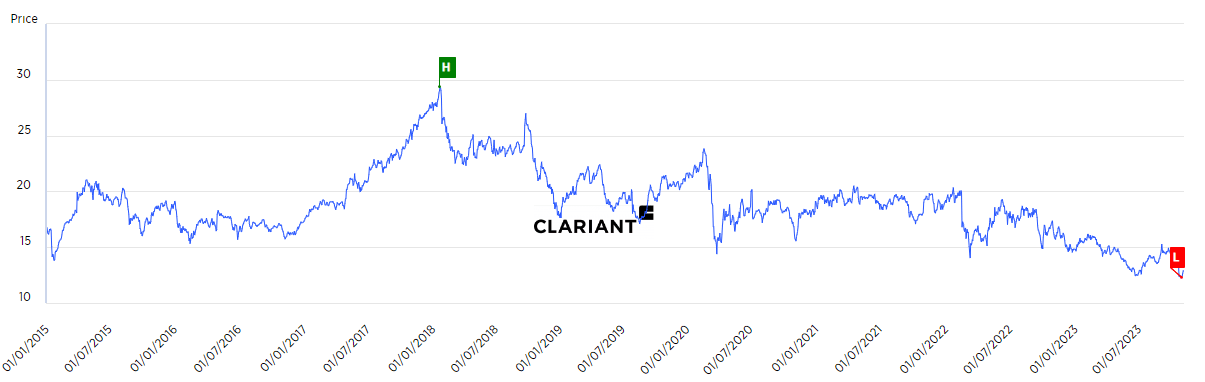

Clariant share price (Clariant.com/es/Investors/Share-and-Bonds/Share-Price)

{kind=link}

The share price decreased by a further 10.03% since the last article I wrote as it currently stands at CHF 13.27, which represents a 54.83% decline from decade-highs of CHF 29.38 reached on January 22, 2018. Although it is true that the situation is not as buoyant as it had been in 2018, the company has not stopped restructuring its business in order to achieve a superior profitability profile, and although sales are currently suffering due to weakening demand, the benefits of the restructuring should be seen as soon as the global economy improves again.

The Lucas Meyer Cosmetics acquisition is a major one

On October 30, 2023, the company announced the acquisition of Lucas Meyer Cosmetics , a leading provider of high-value ingredients for the cosmetics and personal care industry, from International Flavors & Fragrances ( IFF ) for ~CHF 720 million.

Lucas Meyer Cosmetics (Lucasmeyercosmetics.com)

The acquired business serves over 2,900 customers, many of which are blue-chip companies, in over 80 countries as it manufactures over 150 different products worldwide, and it generates annual revenues of ~$100 million, but the two main advantages are that it is a highly profitable business (since it is asset-light) with annual revenue growth rates of around 10% as the company plans to expand its revenues to $180 million by 2028 by launching new products under the business.

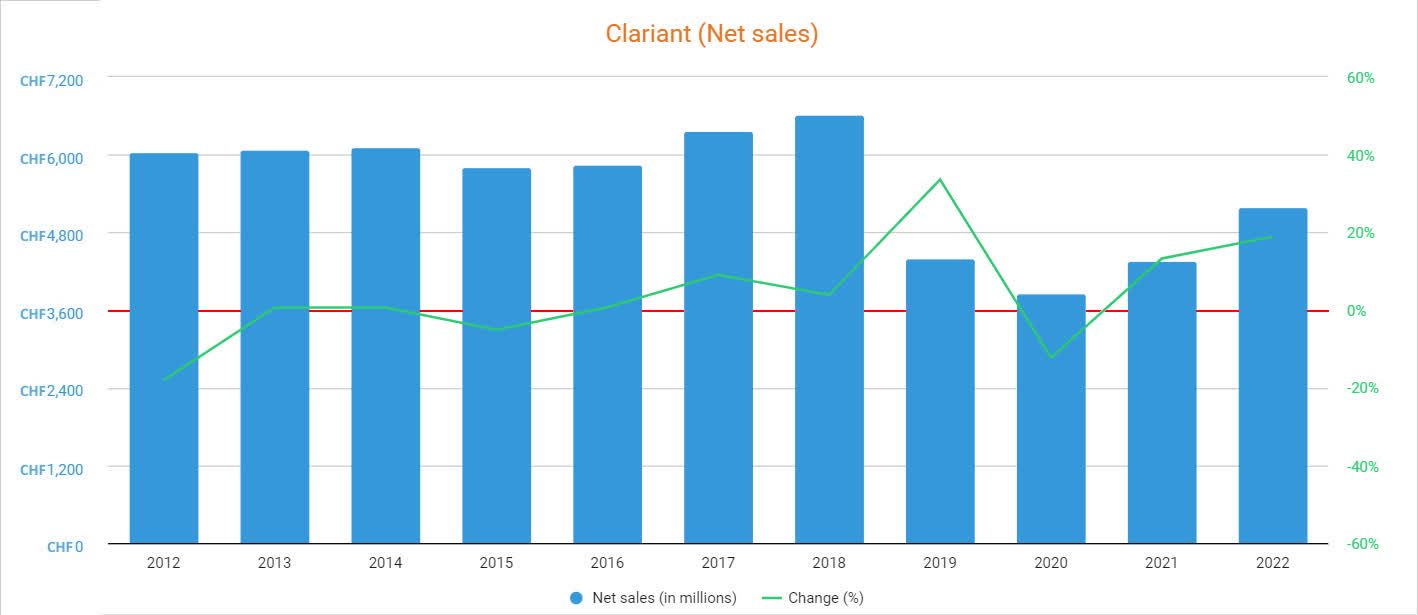

Net sales are not quite taking off

In recent years, sales have been depressed as a result of a series of divestitures carried out to improve profit margins as the company sold less profitable businesses, and although this has been accompanied by significant improvements in profit margins, it seems that the current reason for stagnant sales is weakening demand due to the current recessionary macroeconomic landscape.

{kind=link}

In this regard, sales declined by 8% year over year organically to CHF 1.031 billion during the third quarter of 2023 (and by 5 % sequentially) after increasing by 13.26% in 2021 and 18.89% in 2022, mostly impacted by weaker demand in the additives business as the company's product pricing decreased by 3% year-on-year and volumes by 5%. Nevertheless, the catalysts business actually improved in both volume and pricing as the weakening demand is mostly related to lower consumption of durable goods, which is typical of recessionary periods. Also, China's economic recovery is less intense than expected, and the management doesn't expect a significant recovery in sales during 2024 given the current complex macroeconomic landscape.

Nevertheless, the company keeps launching new products in order to maintain its leadership position in the market. Only in October 2023, it launched new solutions to its portfolio of high-performing pharmaceutical ingredient solutions and also launched TexCare Gemini SG Terra , a high-performing soil release polymer for laundry liquid applications, as well as a PFAS/PTFE-free agent with texturing effects for architectural powder coatings.

Despite this, what is currently most concerning is that in addition to weakening sales, profit margins are now also taking a negative hit not only due to declining volumes but also as a consequence of currency headwinds, and this comes at a time when the company will need to generate enough cash to cover increased debt costs.

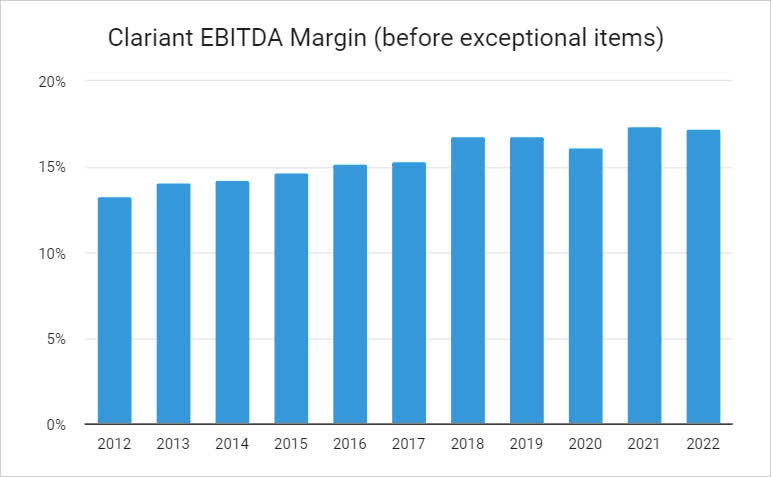

Margins are declining, yet the company remains profitable

As can be seen in the graph below, the company has managed to systematically improve its EBITDA margins in recent years, which has largely compensated for the drop in sales derived from recent divestitures as the EBITDA margin (before exceptional items) surpassed the 15% mark in 2016 continued improving in recent years.

{kind=link}

Still, the EBITDA margin decreased year over year to 15.4% during the third quarter of 2023 (vs. 16.8% during the same quarter of 2022), strongly impacted by negative currency translation and weakening demand, but improved by 340 basis points sequentially thanks to cost measures and operational improvements, and the company expects to continue adjusting costs in the coming quarters. Furthermore, raw material costs eased by 16% year over year during the quarter, and the management expects material costs to remain lower compared to recent quarters, which means EBITDA margins should soon start recovering some lost ground, but lower volumes are expected to be a headwind that will extend, at least, until 2025.

For this reason, investors will need to be patient especially considering the company's interest expenses are likely going to increase significantly in the coming quarters as a result of the acquisitions of Lucas Meyer Cosmetics. In this regard, Clariant should be seen, in my opinion, as a long-term investment as digesting the acquisition will likely not be a walk in the park.

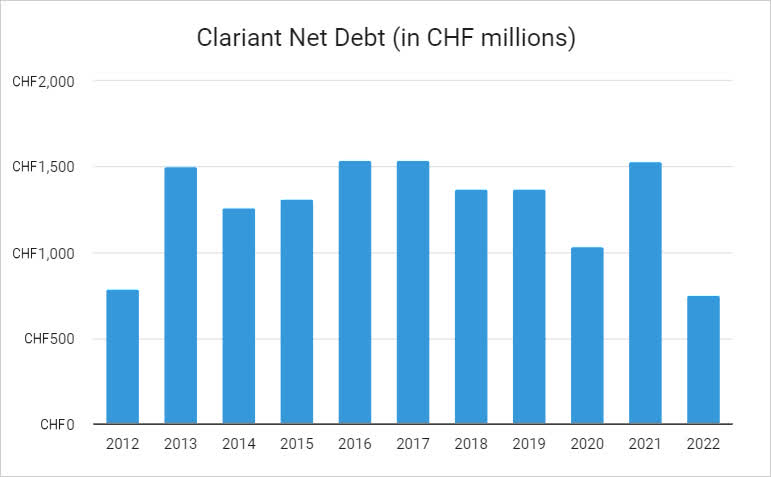

Net debt is again on the rise

The company has maintained highly manageable net debt levels in recent years as it has tried to divest less profitable businesses before performing significant acquisitions in order to not cause a significant increase in interest expenses, but the latest acquisition will put some pressure on the balance sheet for a few years.

{kind=link}

Net debt increased from CHF 750 million in the first half of 2022 to CHF 908 million in the first half of 2023, and the acquisition of Lucas Meyer Cosmetics will cost the company around CHF 720 million, which means net debt will be again dancing around the CHF 1.5 billion mark. This will have a direct impact on interest expenses as the company already paid CHF 55 million in 2022, which adds even more to Clariant's risks in the short and medium term. Also, cash and equivalents declined to CHF 285 million in the first half of 2023 (from CHF 394 million in the first half of 2022), so the room for maneuver is becoming more limited.

Still, I do not consider short and medium-term risks to be too catastrophic as the company keeps generating enough cash from operations to cover interest expenses, capital expenditures, and dividends paid, so the balance sheet should begin to strengthen as soon as foreign exchange headwinds relax. In this regard, the company seems prepared to start a deleveraging phase (albeit starting at a very slow pace given current headwinds) that should unlock shareholder value in the long run while positioning the company for future growth through further acquisitions.

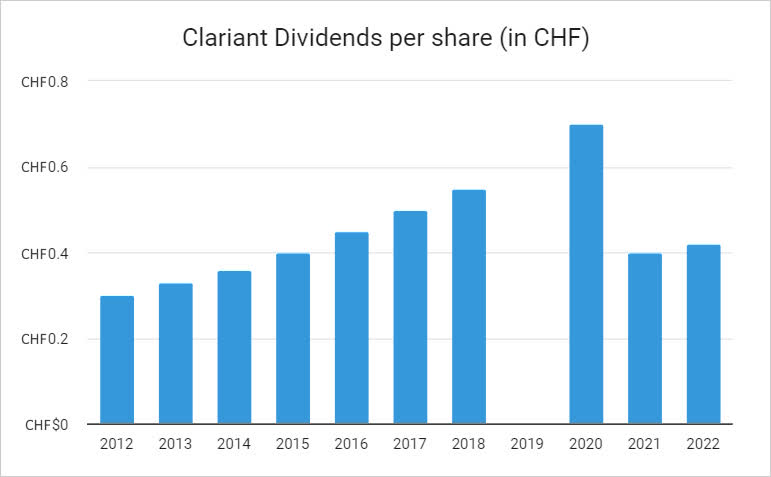

The dividend looks safe, but don't expect much growth

The company paid CHF 0.42 per share in 2023 (based on 2022 performance) in the form of dividends as it raised the annual dividend by 5% compared to 2022, which means the company's dividend yield currently stands at 3.17% considering a share price of CHF 13.27. This dividend is still 24% below the dividend of CHF 0.55 paid for 2018 as the company cut the dividend in 2019 and 2020 to CHF 0.35 per share (which were paid as a single dividend due to the disruptions derived from the coronavirus) and has cautiously increased it in 2021 and 2022.

{kind=link}

In 2022, the company paid CHF 138 million in dividends and CHF 55 million in interest expenses, and the company reported CHF 502 million in cash from operations. Conversely, the company reported CHF 78 million in cash from operations in the first half of 2023. Still, inventories increased by CHF 8 million during the same period, and while accounts receivable declined by CHF 59 million, accounts payable decreased by CHF 171 million, which means the company should have no problem continuing to cover the dividend and interest expenses in the future because, although interest expenses are expected to increase in 2024 as a result of the acquisition, cash from operations should also increase thanks to the sales reported by the business.

In this regard, cash flow from operating activities before changes in working capital and provisions was CHF 300 million in the first half of 2023, which despite representing a significant drop compared to the CHF 440 million reported in the same period of 2022, is enough to cover the dividend, interest expenses, and annual capital expenditures as the company has targeted capital expenditures of CHF 220 million for the full 2023 as it keeps launching new products to the market.

Risks worth mentioning

In the long term, I consider Clariant's risk profile to be relatively low thanks not only to the large size of its business but especially due to the high profit margins of its products as they are highly differentiated. Additionally, the company should be able to continue covering the dividend, capital expenditures, and interest expenses with cash from operations alone while generating some excess cash. But still, there are certain risks that I would like to highlight for the short and medium term.

- Recent interest rate hikes could trigger a global recession, which could have a direct impact on sales and profit margins.

- The current panorama marked by weak demand could extend beyond 2024, which would significantly delay the company's growth plans and make the deleveraging process more difficult than expected.

- If inflationary pressures intensify again, EBITDA margins could contract again, which would have a direct impact on the company's ability to cover interest expenses, dividends paid, and capital expenditures.

- In the event that the global economic outlook continues to worsen, the company could opt to cut the dividend again in order to preserve as much cash as possible.

- Lucas Meyer Cosmetics results might not be as good as expected, which would likely cause even more pessimism among investors as it would worsen the company's prospects.

Conclusion

Restructuring processes usually require a lot of patience from the point of view of an investor. Clariant has been selling unprofitable businesses for years while buying more profitable ones, which means that a higher EBITDA margin partially compensates for depressed sales. The latest acquisition represents a very important addition for Clariant as it promises high growth and profitability rates, but still, the high operational volatility experienced since the outbreak of the coronavirus pandemic in 2020 makes it very difficult to evaluate the results of the changes carried out, and interest expenses will rise in the coming quarters.

Foreign exchange headwinds, negative pricing, and weaker demand due to the current recessionary environment caused a decline in both sales and EBITDA margins in the third quarter of 2023, and the situation is not expected to improve much in 2024 regarding demand, so a lot of patience will be needed. Meanwhile, dividend investors will likely not enjoy the growth rates achieved before the coronavirus pandemic in 2020.

Despite this, I believe that one should not lose perspective when given opportunities like these. Clariant is a highly profitable leading company that generates enough cash from operations to sustain itself while generating some excess cash to strengthen its balance sheet, even with the current headwinds. Furthermore, these headwinds are likely of a temporary nature due to their direct link with the current macroeconomic context and dividend investors will enjoy higher dividend yields on cost in the long run in exchange for the patience that is being required of them at this time. For this reason, I believe that the 55% decline in the share price since 2018 represents a good opportunity for long-term dividend investors.

For further details see:

Clariant: A Good Opportunity For Long-Term Dividend Investors