CLAR - Clarus: Intriguing M&A Choices

2024-01-06 07:39:59 ET

Summary

- Clarus operates under three segments: Outdoor, Adventure, and the soon-to-be-sold Precision Sport segment.

- The company has historically had quite a weak profitability, and the soon-to-be-sold segment has recently been the company's most profitable, making the transaction intriguing.

- The company's financials should clear up from the M&A activity and poor demand in a couple of years, giving investors better clarity on future earnings.

- At the moment, the valuation seems to have upside, but as the transactions' effects are still a bit unclear, I only have a hold rating for the time being.

Clarus (CLAR) sells outdoor equipment in the United States as well as internationally. The company operates under three segments - Outdoor with the Black Diamond, ClimbOn, and PIEPS brands, soon-to-be-sold Precision Sport with Sierra Bullets and Barnes Bullets brands, and Adventure with Rhino-Rack, MAXTRAX and TRED.

Clarus November Investor Presentation

{kind=link}

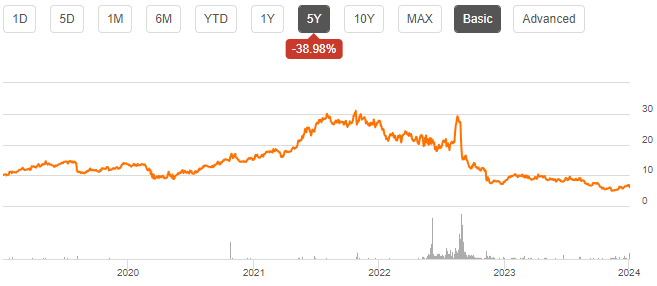

Clarus' earnings have been quite shaky, and the company hasn't found a very great path to long-term earnings growth. As a result, the stock has so far been quite a poor investment, with the stock losing 39% of its value in the past five years. The company pays out a small dividend with a current expected yield of 1.63% , far from covering the historical losses in the period.

Five Year Stock Chart (Seeking Alpha)

{kind=link}

Financials

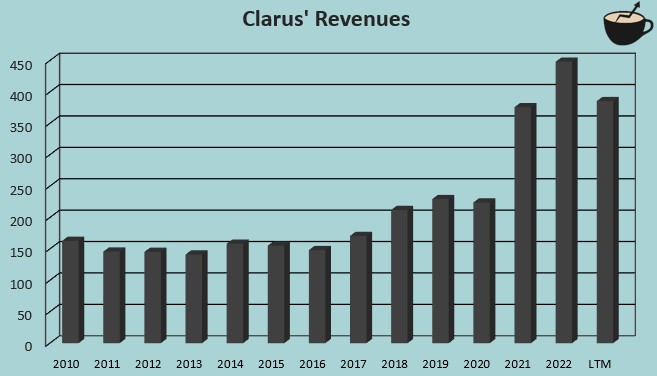

Clarus has historically had some revenue growth. From 2010 to 2019, representative of a period with no disturbance from the Covid pandemic, the company achieved a CAGR of 3.9%. The pandemic largely disrupted the outdoors equipment industry, boosting Clarus' demand in 2021 and 2022 along with the 2021 acquisition of Rhino-Rack . The company doesn't have very large catalysts for organic growth, but seems to hold the line with revenues on a long-term basis with minimal growth.

Author's Calculation Using TIKR Data

{kind=link}

So far in 2023, Clarus has seen declining demand. Revenues are guided in the Q3 earnings call to be down by around 18% in the year, as demand normalizes and the company sees a challenging period due to macroeconomic headwinds and retailers' high outstanding inventory levels. The challenges don't seem to be going away yet as the 2023 guidance also implies a poor Q4 performance.

Clarus has quite a thin profitability. Prior to the pandemic in 2019, the company had an EBIT margin of 5.1% , but since has had turbulence with the pandemic and current weakening demand. The EBIT margin reached 9.6% in 2021 but is currently back into an even lower than pre-pandemic level at 2.8%. The profitability is somewhat higher than GAAP numbers would imply, as the company has $13.1 million (3.4% of revenues) currently in trailing amortization from previous acquisitions. Still, the company operates at quite thin cash flow margins.

Sale of Precision Sport Segment & Acquisition of TRED Outdoors

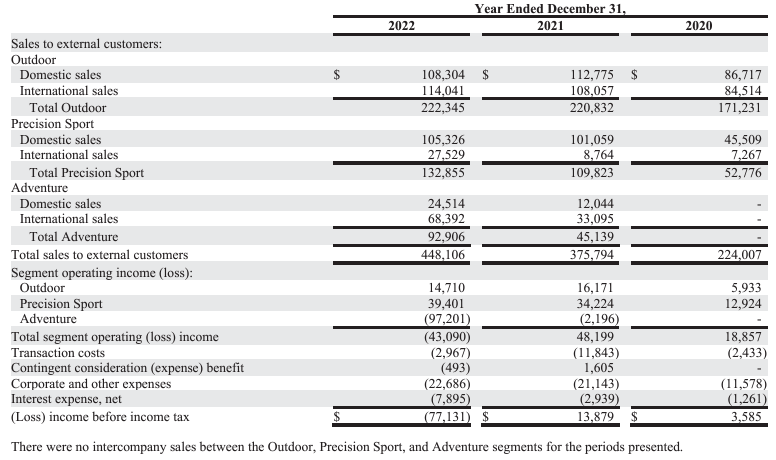

In late December, Clarus announced that the company is selling its Precision Sport division for an appreciation of $175 million to an undisclosed buyer. The segment includes Sierra Bullets and Barnes Bullets, representing around 29% of Clarus' revenues in 2022 according to the year's annual report .

Worryingly, the Precision Sport segment's profitability is by far the best out of Clarus' segments. In 2022, the segment had an operating income of $39.4 million, compared to the Outdoor segment's operating income of just $14.7 million and the Adventure segment's slightly negative operating income even when excluding the impairment of goodwill associated with the segment. On the Adventure segment, it must also be noted that the operating income includes a large amount of amortization that don't effect cash flows, with an amount of $11.6 million in 2022 - the segment is still quite constantly profitable on a cash flow basis. Still, the soon-to-be-sold Precision Sport segment is by far the company's most profitable segment, making the divestment for $175 million quite an intriguing choice in my opinion with the company's already quite thin margins.

Segment Sales & Profitability (Clarus 2022 Annual Report)

{kind=link}

The transaction is expected to close in the first quarter of 2024. Clarus plans to use the proceeds partly to pay off its interest-bearing debts, as the company currently has around $126 million in current and long-term portions of long-term debt on the balance sheet . Other clear uses for the proceeds aren't communicated, but I would expect the company to be active in M&A going forward as the company has had an active history in acquisitions.

Clarus also recently announced the completed acquisition of TRED Outdoors in October, an outdoor brand operating in offroad, 4x4 automotive touring, camping, and caravan sections. TRED Outdoors has operations in mostly Australia, but also in other markets including Canada, Middle East, and the US. The acquisition is described as a fast-growing business, but other financials or terms about the acquisition were not disclosed. As the terms are unclear, it is difficult to evaluate the acquisition's worthiness until further information comes out. With the Q4 earnings, the cash acquisition sum should be available though, showing the acquisition price in cash acquisitions as the transaction has been completed. The Q3 earnings call did include a mention of TRED Outdoors adding around $1.5 million to $2.0 million in sales in Q4, adding some context to the addition.

Cheap But Unclear Valuation

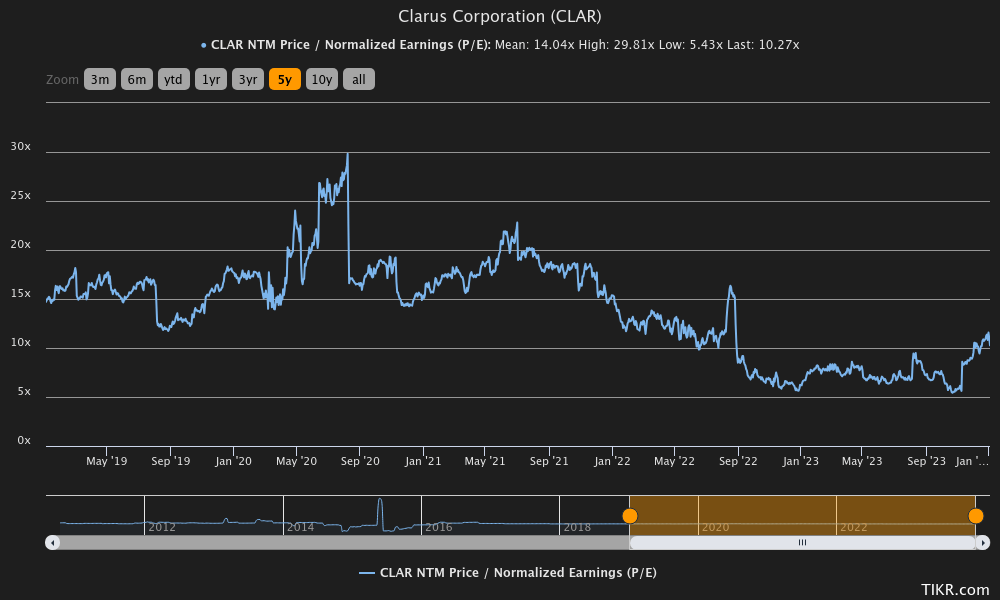

Clarus doesn't have a very expensive valuation, as the stock trades at a forward P/E of 10.3, below the stock's five-year average of 14.0.

{kind=link}

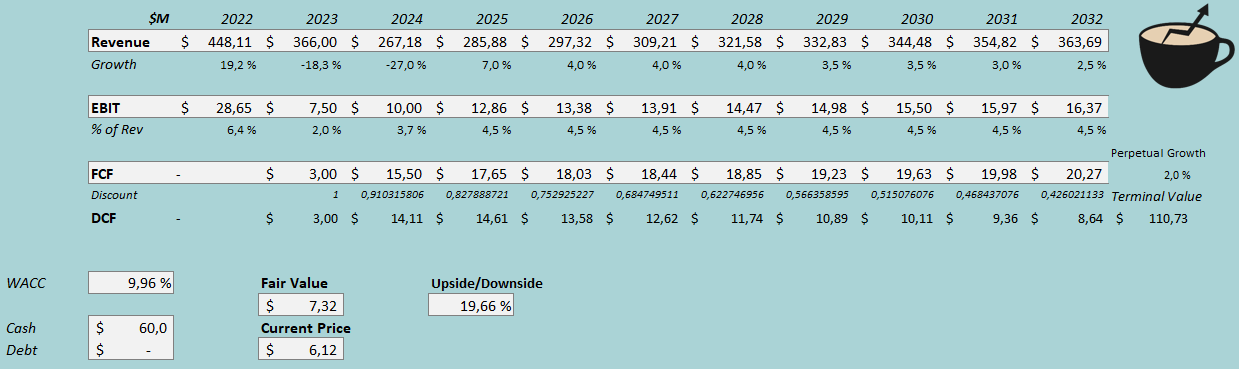

The company's recent divestment and possibly the acquisition shake up the company's financials. I constructed a discounted cash flow model that accounts for the Precision Sport divestment, but not for the TRED Outdoors acquisition as terms aren't well disclosed at the moment.

In the DCF model, I model a scenario where the company pays off its debts and expands its cash reserves with the divestment. As a result, I estimate 2024 revenues to come down by 27%, also representing a very modest organic performance due to challenges in demand. In 2025, I estimate a demand recovery with a revenue growth of 7%, that slows down in sequential years into an eventual perpetual growth of 2%.

The margins are likely to continue as thin. After a 2023 EBIT margin estimate of 2.0%, I estimate the margin to scale into 4.5% in the next two years, as demand normalizes. The estimate is below Clarus' pre-pandemic level as the most profitable segment is divested, and as overhead will take more of Clarus' revenues with the lower revenues. Because of a large amount of amortization, Clarus still has healthy cash flows with a very good cash flow conversion.

With the mentioned estimates along with a cost of capital of 9.96%, the DCF model estimates Clarus' fair value at $7.32, around 20% above the current stock price at the time of writing. The stock seems to have an undervaluation, but the fair value can be quite volatile in coming quarters - the sale of the Precision Sport segment and the unaccounted TRED Outdoors acquisition can still vary the valuation largely with differing margin and revenue outcomes.

DCF Model (Author's Calculation)

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

Clarus currently has a good amount of interest-bearing debt, but the company plans to pay off its debts with the proceedings of the divestment. As such, I estimate the company to have no debt in its financing in the future, with a long-term debt-to-equity ratio estimate of 0%. For the risk-free rate on the cost of equity side, I use the United States' 10-year bond yield of 3.96% . The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate for the United States, made in July. Yahoo Finance estimates Clarus' beta at a figure of 0.93 . Finally, I add a liquidity premium of 0.5%, crafting a cost of equity and WACC of 9.96%.

Takeaway

The pandemic and currently planned divestment of Precision Sport shake up Clarus' financials. The company is underneath a modestly growing business with quite thin margins, and the divestment further underlines Clarus' thin profitability in the future as the segment was Clarus' most profitable. The company has also acquired TRED Outdoors, but as terms are mostly unknown, the transaction's effects on value are unknown at the moment. The current valuation seems to suggest some upside for the stock, but as the effects of recent M&A are yet to be seen, I remain on the side of caution with a hold rating for the time being. With a slightly lower price, or a proven post-divestment financial execution at least in line with my expectations would turn my rating into a buy.

For further details see:

Clarus: Intriguing M&A Choices